Autonomou Construction Equipment Market

Autonomou Construction Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705195 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Autonomou Construction Equipment Market Size

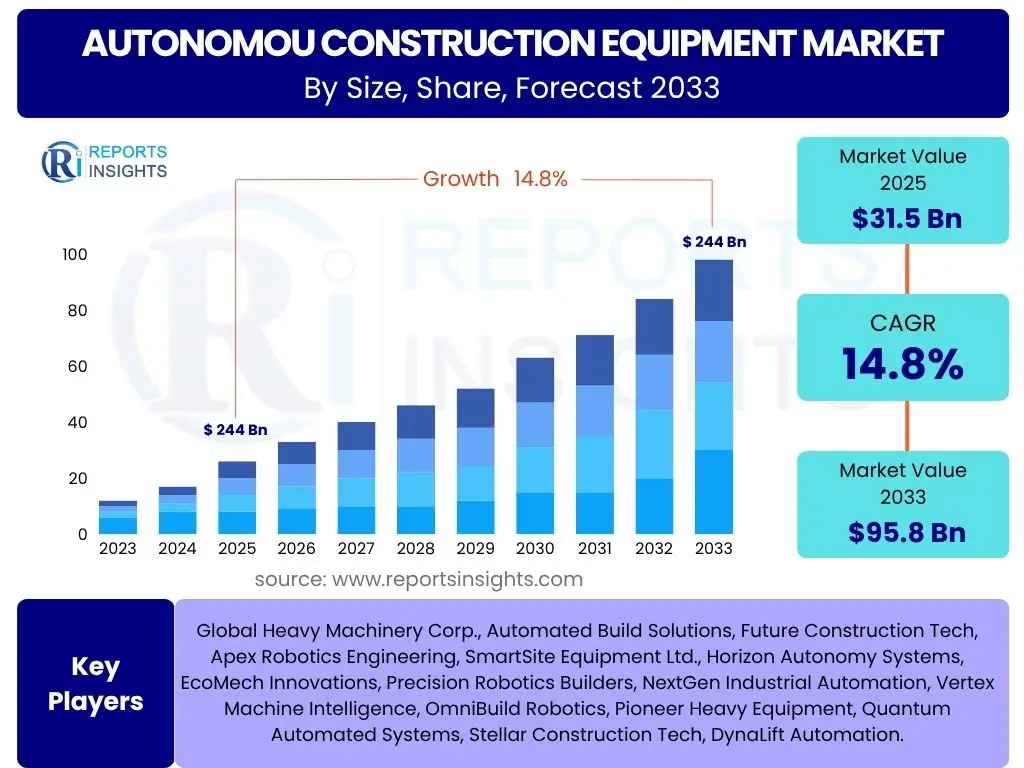

According to Reports Insights Consulting Pvt Ltd, The Autonomou Construction Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.8% between 2025 and 2033. The market is estimated at USD 31.5 billion in 2025 and is projected to reach USD 95.8 billion by the end of the forecast period in 2033.

Key Autonomou Construction Equipment Market Trends & Insights

User inquiries regarding trends in the autonomous construction equipment market frequently center on how these technologies are enhancing operational efficiency, safety, and project timelines. There is significant interest in the integration of advanced data analytics and real-time monitoring capabilities, which are seen as critical for predictive maintenance and optimized resource deployment. Furthermore, the evolving landscape of regulatory frameworks and their impact on widespread adoption, alongside the push for electrification within autonomous fleets, are prominent areas of user curiosity. The trends indicate a profound shift towards more interconnected and intelligent construction sites.

Another area of focus for users revolves around the impact of supply chain resilience and global economic shifts on the pace of autonomous equipment deployment. The discussion often includes the role of public-private partnerships in funding research and development, as well as infrastructure necessary for advanced connectivity. Users are keenly observing how leading manufacturers are investing in research and development, bringing novel solutions to market that address specific industry pain points such as labor shortages and the demand for sustainable practices. The convergence of hardware innovation with sophisticated software algorithms is a recurring theme in user questions about market progression.

- Increased adoption of remote operation and telematics for enhanced control and data collection.

- Rising demand for fully autonomous solutions in repetitive or hazardous tasks.

- Growing integration of Internet of Things (IoT) and cloud-based platforms for real-time monitoring and data analytics.

- Focus on electrification and alternative fuel sources for autonomous construction equipment to meet environmental regulations.

- Development of swarm robotics for coordinated execution of large-scale construction projects.

- Expansion of autonomous capabilities into diverse equipment types beyond traditional earthmoving machinery.

- Emphasis on human-machine collaboration (HMC) for augmented operational efficiency and safety.

AI Impact Analysis on Autonomou Construction Equipment

Common user questions related to the impact of AI on autonomous construction equipment primarily revolve around how artificial intelligence enhances decision-making capabilities, optimizes operational workflows, and improves safety protocols on construction sites. Users are keen to understand AI's role in predictive maintenance, collision avoidance, and the dynamic allocation of resources to maximize project efficiency. There is also significant curiosity about AI's capacity for learning from operational data to continuously refine autonomous functionalities and adapt to varying site conditions. Concerns about data security and the ethical implications of AI-driven decision-making in critical environments are also frequently raised.

Furthermore, inquiries often delve into the specific AI algorithms and machine learning models that underpin the intelligence of autonomous equipment, such as deep learning for object recognition or reinforcement learning for task optimization. Users seek clarity on how AI contributes to faster project completion times and reduced operational costs through intelligent route planning, load optimization, and real-time anomaly detection. The integration of AI with other advanced technologies like 5G connectivity and digital twins is a key area of interest, promising more comprehensive and responsive autonomous systems. The ability of AI to mitigate human error and operate in extreme conditions is also a central theme in user expectations for future developments.

- Enhanced autonomous decision-making through real-time data processing and predictive analytics.

- Optimization of task execution, resource allocation, and project timelines.

- Improved safety through advanced object detection, collision avoidance, and hazard recognition systems.

- Predictive maintenance capabilities, leading to reduced downtime and extended equipment lifespan.

- Autonomous learning from operational data to adapt to diverse environments and optimize performance.

- Facilitation of human-machine collaboration, allowing for more complex tasks to be performed efficiently.

- Development of sophisticated navigation and mapping capabilities for complex construction sites.

Key Takeaways Autonomou Construction Equipment Market Size & Forecast

User questions about the key takeaways from the autonomous construction equipment market size and forecast consistently highlight the significant growth trajectory and the underlying technological advancements driving this expansion. There is a strong interest in understanding the primary factors contributing to the market's substantial projected value, such as increasing demand for efficiency, enhanced safety standards, and solutions to labor shortages. Users frequently inquire about the long-term investment potential within this sector and how the evolving regulatory landscape might shape market dynamics. The insights reveal a clear perception that autonomous equipment is not merely an innovation but a transformative force for the entire construction industry.

Another crucial area of user concern relates to the strategic implications for stakeholders, including manufacturers, contractors, and technology providers. Questions often touch upon where the most significant opportunities lie, whether in specific equipment types, autonomy levels, or regional markets. The competitive landscape, the emergence of new players, and the potential for consolidation are also topics of keen interest. These inquiries underscore the need for a comprehensive understanding of market dynamics to inform strategic planning and investment decisions, emphasizing that the market's robust growth is underpinned by both technological maturity and compelling economic incentives.

- The autonomous construction equipment market is poised for robust growth, driven by efficiency and safety imperatives.

- Significant market expansion is anticipated, with substantial valuation increases over the forecast period.

- Technological advancements, particularly in AI and IoT, are critical enablers of market growth.

- The market presents substantial opportunities for manufacturers, technology providers, and construction firms.

- Addressing challenges such as high initial costs and regulatory complexities will be crucial for sustained adoption.

- North America and Asia Pacific are expected to remain key growth regions, supported by infrastructure development.

- Sustainability and environmental considerations are increasingly influencing the development and adoption of autonomous solutions.

Autonomou Construction Equipment Market Drivers Analysis

The autonomous construction equipment market is primarily propelled by a confluence of factors aimed at revolutionizing construction site operations. Key drivers include the escalating demand for increased operational efficiency and productivity, as autonomous systems can operate continuously and optimize workflows, significantly reducing project timelines and costs. Furthermore, the global shortage of skilled labor in the construction sector acts as a substantial catalyst, pushing companies to adopt automated solutions to maintain output levels and mitigate workforce challenges. Enhanced safety standards are another crucial driver; autonomous equipment minimizes human exposure to hazardous environments and reduces the risk of accidents on site.

Beyond operational benefits, governmental initiatives and regulatory support for infrastructure development also play a pivotal role in market growth, creating a favorable environment for the adoption of advanced construction technologies. The continuous advancements in core technologies such as artificial intelligence, IoT, GPS, and advanced robotics further enable the development of more sophisticated and reliable autonomous systems. Additionally, the growing focus on environmental sustainability drives the adoption of electric and hybrid autonomous equipment, aligning with global efforts to reduce carbon emissions and improve energy efficiency in construction processes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Acute Labor Shortages | +3.5% | North America, Europe, Asia Pacific | Short- to Mid-term (2025-2030) |

| Increased Demand for Operational Efficiency & Productivity | +4.2% | Global | Long-term (2025-2033) |

| Emphasis on Enhanced Site Safety | +3.8% | Global | Long-term (2025-2033) |

| Advancements in AI, IoT, & Robotics | +4.0% | Global | Long-term (2025-2033) |

| Government Initiatives for Infrastructure Development | +2.5% | Asia Pacific, North America, Middle East | Mid-term (2027-2032) |

| Sustainability & Environmental Regulations | +2.0% | Europe, North America, China | Long-term (2028-2033) |

Autonomou Construction Equipment Market Restraints Analysis

Despite the compelling advantages, the autonomous construction equipment market faces several significant restraints that could impede its rapid expansion. A primary constraint is the substantial upfront capital investment required for acquiring and implementing these advanced machines. The high cost of autonomous equipment, coupled with the need for specialized infrastructure and software, can be prohibitive for many small and medium-sized construction firms, limiting widespread adoption. Additionally, the complexity associated with integrating autonomous systems into existing fleet operations presents a considerable challenge, often requiring extensive retraining of personnel and significant overhauls of traditional workflows.

Another major restraint involves the evolving and often fragmented regulatory landscape across different regions and countries. The absence of standardized guidelines and certifications for autonomous equipment can create legal uncertainties and hinder cross-border deployment. Furthermore, concerns regarding cybersecurity threats to highly connected autonomous systems, as well as potential job displacement for human operators, contribute to resistance towards adoption. The reliability and performance of autonomous systems in diverse and unpredictable real-world construction environments, especially in adverse weather conditions, remain areas of concern that require continuous technological refinement and rigorous testing.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -3.0% | Global, particularly developing regions | Short- to Mid-term (2025-2030) |

| Technical Complexities & Integration Challenges | -2.5% | Global | Mid-term (2026-2031) |

| Lack of Standardized Regulations & Infrastructure | -2.8% | Global, especially emerging markets | Long-term (2025-2033) |

| Cybersecurity Risks & Data Vulnerabilities | -1.5% | Global | Long-term (2025-2033) |

| Resistance to Change & Workforce Retraining Needs | -2.0% | Global | Short- to Mid-term (2025-2029) |

Autonomou Construction Equipment Market Opportunities Analysis

Significant opportunities exist within the autonomous construction equipment market for companies capable of innovating and adapting to evolving industry needs. One key opportunity lies in the development of AI-driven platforms that not only control autonomous machines but also offer comprehensive data analytics for predictive maintenance, operational optimization, and project management. This shift towards data-centric solutions can create new revenue streams and enhance the value proposition of autonomous equipment. Furthermore, the expansion of autonomous technology into specialized or niche applications, such as hazardous environment operations (e.g., demolition, disaster response) or precision farming within construction contexts, presents untapped market segments with high growth potential.

Another promising area is the retrofitting of existing conventional construction equipment with autonomous capabilities, offering a more cost-effective entry point for contractors unwilling to make full upfront investments in new autonomous fleets. This approach can accelerate adoption and broaden the market reach. Moreover, public-private partnerships focused on developing smart city infrastructure and large-scale, digitally-integrated construction projects provide fertile ground for the deployment and testing of advanced autonomous solutions. The increasing global focus on sustainable construction practices also opens doors for autonomous electric and hybrid equipment, aligning technological advancements with environmental mandates and offering a competitive advantage.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of AI-driven Data Analytics Platforms | +3.0% | Global | Mid- to Long-term (2027-2033) |

| Expansion into Niche & Hazardous Applications | +2.5% | Global | Long-term (2028-2033) |

| Retrofitting Solutions for Existing Fleets | +2.2% | North America, Europe, Asia Pacific | Short- to Mid-term (2025-2030) |

| Public-Private Partnerships for Infrastructure Projects | +1.8% | Asia Pacific, Middle East, North America | Mid-term (2026-2031) |

| Integration with Sustainable & Electric Technologies | +2.0% | Europe, North America, China | Long-term (2028-2033) |

Autonomou Construction Equipment Market Challenges Impact Analysis

The autonomous construction equipment market faces distinct challenges that require strategic solutions for sustained growth and widespread adoption. A significant challenge is the establishment of robust and pervasive connectivity infrastructure, such as 5G networks, which is essential for real-time data exchange and remote operation of autonomous machinery, especially in remote construction sites. The absence of universal interoperability standards among different manufacturers' equipment and software platforms creates integration hurdles, preventing seamless operation within mixed fleets and complicating data management. Public perception and acceptance of autonomous machinery, particularly concerning safety, job displacement, and overall reliability, also pose a considerable hurdle, necessitating effective communication and demonstration of benefits.

Furthermore, the high cost and complexity of developing and deploying advanced sensor technologies, such as LiDAR and radar, capable of operating reliably in harsh construction environments, remain a technical challenge. Ensuring the security and privacy of the vast amounts of operational data collected by autonomous equipment is also critical, as breaches could lead to significant financial and reputational damage. The legal liability framework for accidents involving autonomous equipment is still evolving, creating uncertainty for manufacturers and operators alike. Addressing these challenges will require collaborative efforts across industry, government, and technology sectors to foster an environment conducive to autonomous technology proliferation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inadequate Connectivity Infrastructure (e.g., 5G) | -2.0% | Global, particularly rural areas | Short- to Mid-term (2025-2030) |

| Lack of Interoperability Standards | -1.8% | Global | Mid-term (2026-2031) |

| Public Acceptance & Trust Issues | -1.5% | Global | Long-term (2025-2033) |

| Complexity of Sensor & AI System Development | -1.2% | Global | Mid-term (2027-2032) |

| Evolving Legal & Liability Frameworks | -1.0% | Global | Long-term (2028-2033) |

Autonomou Construction Equipment Market - Updated Report Scope

This market research report provides an in-depth analysis of the autonomous construction equipment market, encompassing its current size, historical performance, and future growth projections through 2033. It meticulously examines key market trends, identifies the underlying drivers and significant restraints, and highlights emerging opportunities and persistent challenges impacting market dynamics. The report further details the technological advancements, particularly in AI and IoT, that are shaping the market's evolution, alongside an analysis of the competitive landscape. Through comprehensive segmentation and regional insights, it aims to offer a holistic view for stakeholders seeking to navigate and capitalize on this transformative sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 31.5 Billion |

| Market Forecast in 2033 | USD 95.8 Billion |

| Growth Rate | 14.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Heavy Machinery Corp., Automated Build Solutions, Future Construction Tech, Apex Robotics Engineering, SmartSite Equipment Ltd., Horizon Autonomy Systems, EcoMech Innovations, Precision Robotics Builders, NextGen Industrial Automation, Vertex Machine Intelligence, OmniBuild Robotics, Pioneer Heavy Equipment, Quantum Automated Systems, Stellar Construction Tech, DynaLift Automation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The autonomous construction equipment market is extensively segmented to provide a granular understanding of its diverse components and facilitate targeted strategic planning. This segmentation allows for a detailed examination of market dynamics across various dimensions, including the specific types of equipment, the level of autonomy integrated, the broad range of applications they serve, and the propulsion technologies utilized. Analyzing these segments individually and in combination reveals critical insights into demand patterns, technological preferences, and regional adoption trends, providing a comprehensive framework for market assessment.

Understanding these distinct segments is crucial for identifying high-growth areas, recognizing evolving user requirements, and tailoring product development and marketing strategies effectively. For instance, the differing adoption rates between semi-autonomous and fully autonomous equipment highlight the market's maturity and readiness for advanced solutions, while the breakdown by application illustrates the most impactful use cases for these technologies. This comprehensive segmentation ensures that stakeholders can pinpoint specific opportunities and challenges within the market, optimizing their investment decisions and competitive positioning.

- By Equipment Type: Dozers, Excavators, Loaders, Dump Trucks, Paving Equipment, Others (e.g., Graders, Compaction Equipment)

- By Autonomy Level: Semi-Autonomous, Fully Autonomous

- By Application: Material Handling, Earthmoving, Road Construction, Mining, Demolition, Site Preparation

- By Propulsion Type: Diesel, Electric, Hybrid, Other (e.g., Fuel Cell)

Regional Highlights

- North America: A leading region in autonomous construction equipment adoption, driven by severe labor shortages, high emphasis on safety, and significant investment in smart infrastructure projects. The presence of key technology developers and a robust construction sector contribute to its strong market share.

- Europe: Characterized by stringent environmental regulations and a strong focus on sustainable and efficient construction practices. Adoption is propelled by smart city initiatives and government funding for automation research, with a growing trend towards electrification of autonomous fleets.

- Asia Pacific (APAC): Poised for rapid growth due to massive infrastructure development projects, increasing urbanization, and a willingness to embrace advanced technologies, particularly in countries like China, India, and Japan. Government support and large-scale industrialization are key accelerators.

- Latin America: Emerging market with nascent but growing interest in autonomous construction, primarily driven by mining and large-scale public infrastructure projects. The region presents opportunities as it seeks to improve efficiency and safety in traditionally labor-intensive sectors.

- Middle East and Africa (MEA): Significant potential fueled by ambitious megaprojects, diversification efforts away from oil economies, and a strategic push towards technological modernization in construction. Investment in smart cities and large-scale residential and commercial developments are key drivers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Autonomou Construction Equipment Market.- Global Heavy Machinery Corp.

- Automated Build Solutions

- Future Construction Tech

- Apex Robotics Engineering

- SmartSite Equipment Ltd.

- Horizon Autonomy Systems

- EcoMech Innovations

- Precision Robotics Builders

- NextGen Industrial Automation

- Vertex Machine Intelligence

- OmniBuild Robotics

- Pioneer Heavy Equipment

- Quantum Automated Systems

- Stellar Construction Tech

- DynaLift Automation

- Advanced Construction Robotics

- Industrial Autonomy Group

- RoboWorks Heavy Equipment

- IntegraBuild Solutions

- MechSmart Technologies

Frequently Asked Questions

Analyze common user questions about the Autonomou Construction Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is autonomous construction equipment?

Autonomous construction equipment refers to heavy machinery that can perform tasks with little to no direct human intervention, utilizing technologies like AI, GPS, sensors, and robotics for navigation, operation, and task execution on construction sites. These machines are designed to enhance efficiency, safety, and productivity by automating repetitive or hazardous tasks.

What are the primary benefits of adopting autonomous construction equipment?

The main benefits include significant improvements in operational efficiency and productivity through continuous operation, enhanced safety by removing human operators from dangerous environments, reduced labor costs due to automation, and increased precision and consistency in tasks, leading to higher quality project outcomes.

What are the major challenges hindering the widespread adoption of autonomous construction equipment?

Key challenges include the high initial capital investment, the complexity of integrating new autonomous systems with existing infrastructure, a lack of standardized regulations across different regions, concerns regarding cybersecurity and data privacy, and the need for significant workforce retraining to manage and maintain these advanced systems.

How does Artificial Intelligence (AI) impact autonomous construction equipment?

AI is fundamental to autonomous construction equipment, enabling intelligent decision-making, real-time obstacle detection, predictive maintenance, and optimized task execution. AI algorithms allow machines to learn from data, adapt to changing site conditions, and perform complex operations with greater precision and autonomy, significantly boosting performance.

What is the future outlook for the autonomous construction equipment market?

The autonomous construction equipment market is projected for substantial growth, driven by continued technological advancements, increasing demand for efficiency and safety solutions, and government investments in infrastructure. The market is expected to expand globally, with increasing integration of AI, IoT, and sustainable energy sources, transforming traditional construction practices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted