Passenger Car Clutch Market

Passenger Car Clutch Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678219 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

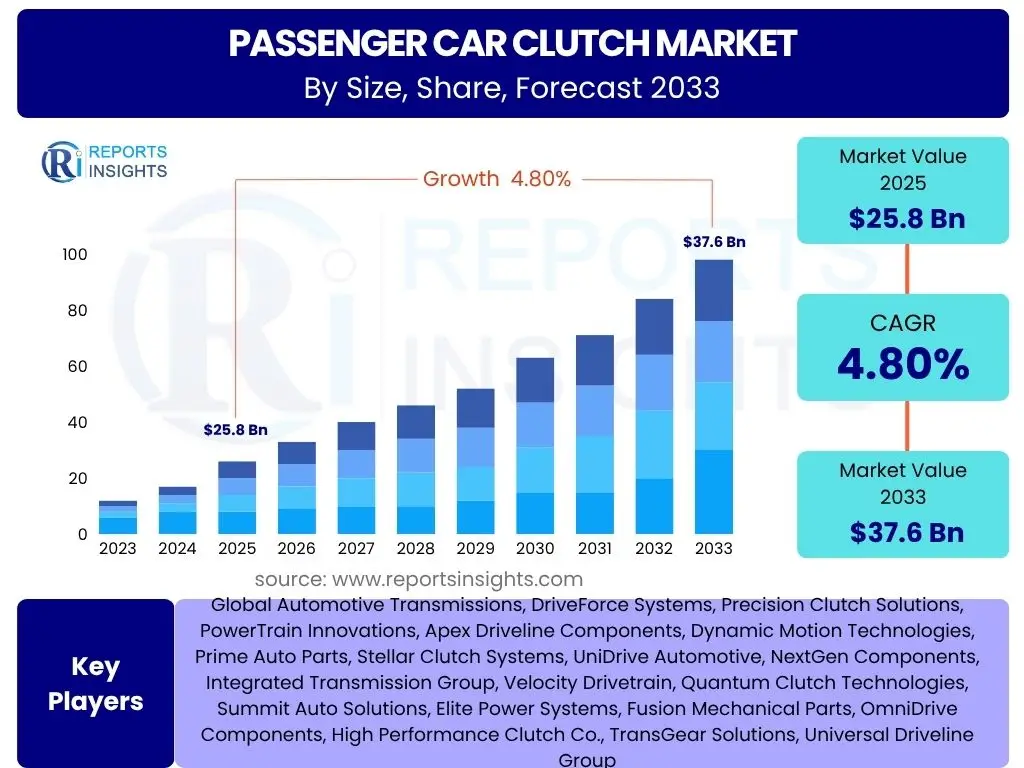

Passenger Car Clutch Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, valued at USD 14.5 Billion in 2025 and is projected to reach USD 23.0 Billion by 2033 at the end of the forecast period.

Key Passenger Car Clutch Market Trends & Insights

The passenger car clutch market is currently navigating a period of significant evolution, driven by shifts in consumer preferences, technological advancements, and the global push towards electrification. While manual transmissions, and thus clutches, face headwinds from the increasing adoption of automatic transmissions and electric vehicles, demand persists, particularly in emerging markets and for replacement needs. Key trends include the ongoing development of more efficient and durable clutch systems, the integration of advanced materials to reduce weight and improve performance, and the growing importance of the aftermarket segment as vehicle lifespans extend. Manufacturers are focusing on optimizing existing clutch technologies to meet evolving performance and environmental standards, ensuring that even as the landscape shifts, the fundamental need for reliable power transmission in internal combustion engine (ICE) vehicles remains a market cornerstone. The market also sees a trend towards lighter components and more sophisticated engagement mechanisms to enhance driver comfort and fuel efficiency.

- Increasing demand for manual transmission vehicles in cost-sensitive and emerging markets.

- Technological advancements in clutch materials for enhanced durability and performance.

- Growing focus on lightweight clutch designs to improve fuel efficiency.

- Significant growth in the aftermarket segment driven by vehicle aging and replacement cycles.

- Development of semi-automatic clutch systems as a bridge technology.

- Stringent emission regulations indirectly influencing clutch design towards greater efficiency.

AI Impact Analysis on Passenger Car Clutch

Artificial Intelligence (AI) is set to exert a profound, albeit indirect, influence on the passenger car clutch market, primarily through its transformative impact on manufacturing processes, supply chain management, and predictive maintenance. While AI does not directly interact with a mechanical clutch during vehicle operation in traditional ICE cars, its application in smart factories enables highly optimized production lines, reducing waste and improving precision in clutch component manufacturing. Furthermore, AI-driven analytics can forecast demand patterns with greater accuracy, leading to more efficient inventory management for both original equipment manufacturers (OEMs) and aftermarket suppliers. In the long term, AI's role in advanced vehicle diagnostics and prognostics could facilitate more timely and efficient clutch replacements, potentially boosting the aftermarket segment by identifying wear before critical failure, optimizing service intervals and enhancing overall vehicle reliability for consumers. This predictive capability ensures that clutches are replaced proactively rather than reactively, contributing to sustained demand for replacement parts.

- AI-powered predictive maintenance enhancing aftermarket service and clutch replacement cycles.

- Optimization of clutch manufacturing processes through AI and automation for cost efficiency.

- AI-driven supply chain management improving logistics and material sourcing for clutch components.

- Advanced simulation and design using AI to innovate clutch performance and durability.

- AI in quality control ensuring higher precision and fewer defects in clutch production.

Key Takeaways Passenger Car Clutch Market Size & Forecast

- The global Passenger Car Clutch Market is projected to reach a valuation of USD 23.0 Billion by 2033.

- The market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033.

- In 2025, the market size stood at an estimated USD 14.5 Billion.

- The growth is primarily driven by consistent demand for manual transmission vehicles in emerging economies and robust aftermarket sales.

- Despite the shift towards automatic transmissions and electric vehicles, the large existing fleet of ICE vehicles ensures sustained demand for replacement clutches.

- Asia Pacific is expected to remain a dominant region, contributing significantly to market volume and value.

Passenger Car Clutch Market Drivers Impact Analysis

The Passenger Car Clutch Market is significantly propelled by several key drivers that sustain its growth trajectory amidst evolving automotive trends. A primary driver is the ongoing production of internal combustion engine (ICE) vehicles, particularly in developing economies where manual transmission cars remain a popular and affordable choice. These regions often prioritize cost-effectiveness and durability, attributes that manual transmission systems inherently offer. Another crucial driver is the robust demand from the aftermarket segment. As the global parc of older ICE vehicles continues to grow, the need for replacement clutches due to wear and tear becomes increasingly prevalent, creating a steady revenue stream for manufacturers. This consistent demand ensures market stability, even as new vehicle sales in some regions lean towards automatic or electric options. Furthermore, technological advancements in clutch materials and design contribute to market growth by offering improved performance, fuel efficiency, and extended lifespan, which encourages both OEM adoption and aftermarket upgrades. These innovations enhance the appeal and functionality of manual clutch systems. The expansion of manufacturing capabilities in emerging economies, coupled with their rising middle-class population, further fuels the demand for new manual transmission vehicles, solidifying their position as critical growth engines for the clutch market.

The affordability of manual transmission vehicles compared to their automatic or electric counterparts makes them highly attractive in price-sensitive markets. This economic advantage translates directly into sustained production volumes for vehicles equipped with clutches, underpinning the foundational demand for these components. Additionally, the increasing average age of vehicles on the road, particularly in established markets, necessitates a consistent supply of replacement parts, with clutches being among the most frequently serviced components due to their operational wear. This creates a predictable and resilient demand segment that is less susceptible to immediate shifts in new vehicle sales trends. Innovations such as lighter composite materials for clutch components, advanced friction materials for better engagement, and designs that reduce pedal effort are continuously improving the driving experience for manual transmission users, indirectly supporting their continued preference and market share in specific segments. These drivers collectively form a comprehensive framework that supports the ongoing relevance and growth of the passenger car clutch market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sustained Production of Manual Transmission ICE Vehicles | +1.5% | Asia Pacific, Latin America, Africa | Mid-term to Long-term |

| Robust Aftermarket Demand for Replacement Clutches | +1.2% | Global, especially North America, Europe, Asia Pacific | Short-term to Long-term |

| Technological Advancements in Clutch Materials and Design | +0.8% | Europe, North America, Japan, South Korea, China | Mid-term |

| Economic Affordability of Manual Transmission Vehicles | +0.7% | India, China, Southeast Asia, Brazil, Mexico | Short-term to Mid-term |

Passenger Car Clutch Market Restraints Impact Analysis

The Passenger Car Clutch Market faces significant headwinds from several influential restraints that could temper its growth trajectory. The most prominent restraint is the accelerating global shift towards automatic transmission (AT) vehicles, particularly in developed markets like North America and Europe. Consumer preference for the convenience and ease of driving offered by ATs directly reduces the demand for manual transmission (MT) vehicles, thereby impacting the OEM demand for clutches. Concurrently, the rapid proliferation of electric vehicles (EVs) represents a long-term existential threat to the clutch market. EVs typically do not require a multi-speed transmission or a clutch in the traditional sense, as electric motors provide instant torque and a wide power band, fundamentally altering the drivetrain architecture. This structural shift in automotive technology significantly curtails the potential for future market expansion for clutches. Furthermore, volatile raw material prices, particularly for steel, aluminum, and friction materials, can impact manufacturing costs and profit margins for clutch producers, adding to market instability. Adherence to increasingly stringent environmental regulations, which often incentivize more fuel-efficient or zero-emission vehicles, also indirectly acts as a restraint by pushing manufacturers away from traditional ICE manual vehicles.

Beyond the fundamental technological shifts, market saturation in certain developed regions, coupled with a general decline in driving enthusiasm among younger demographics, can contribute to slower vehicle turnover and reduced new car sales, indirectly dampening the OEM clutch market. The complexity and cost associated with developing advanced manual clutch systems that can compete with the smooth operation of modern automatic transmissions also pose a challenge, limiting investment in new MT vehicle models. Moreover, public perception and driver training programs increasingly emphasize automatic transmissions, further sidelining manual driving skills and preferences. This cumulative effect of shifting consumer tastes, revolutionary drivetrain technologies, and economic pressures creates a challenging environment for sustained growth in the passenger car clutch market, necessitating strategic adaptation from manufacturers to explore niche segments or diversify their product portfolios.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Automatic Transmissions (AT) | -1.8% | North America, Europe, parts of Asia Pacific | Short-term to Long-term |

| Rapid Growth and Proliferation of Electric Vehicles (EVs) | -1.5% | Global, especially China, Europe, North America | Mid-term to Long-term |

| Volatility in Raw Material Prices | -0.6% | Global, impacting manufacturing hubs | Short-term |

| Stricter Emission Norms and Fuel Economy Standards | -0.5% | Europe, North America, Japan, China | Mid-term |

Passenger Car Clutch Market Opportunities Impact Analysis

Despite the prevailing restraints, the Passenger Car Clutch Market presents several significant opportunities that can be leveraged for sustained growth and profitability. One prominent opportunity lies within the vast and expanding aftermarket segment. With millions of manual transmission vehicles currently on the road globally, and an average vehicle lifespan increasing, the demand for replacement clutches due to natural wear and tear will remain substantial for many years to come. This provides a stable and predictable revenue stream for manufacturers, allowing them to focus on developing durable and cost-effective aftermarket solutions. Furthermore, the burgeoning automotive markets in developing regions, particularly in Asia Pacific, Latin America, and Africa, continue to exhibit strong demand for affordable manual transmission vehicles. As these economies grow and vehicle ownership rises, the OEM demand for clutches in these regions offers significant expansion potential. Manufacturers can strategically focus their production and distribution networks to cater to these high-growth markets. The ongoing development of advanced clutch systems, such as those with improved damping characteristics, lighter designs, and enhanced friction materials, also creates opportunities. These innovations can cater to niche markets or specific vehicle segments that still prefer manual control, enhancing the performance and driving experience of manual transmission vehicles.

Another crucial opportunity arises from the potential for product diversification within the clutch market, focusing on specific applications like performance cars, commercial light vehicles, or even retrofitting solutions for classic cars, where manual transmissions hold cultural or practical significance. The advent of semi-automatic or automated manual transmissions (AMTs), while reducing the driver's direct interaction with the clutch pedal, still utilizes clutch components, presenting an opportunity for clutch manufacturers to adapt their product lines. Investing in research and development to integrate smart features, such as sensors for predictive maintenance, into clutch systems can create value-added propositions, enhancing product utility and opening new revenue channels. Additionally, expanding distribution networks, particularly in underserved regions and through online channels for the aftermarket, can significantly improve market reach and accessibility. These opportunities collectively provide a multi-faceted approach for clutch manufacturers to innovate, expand their market footprint, and secure their position in a transforming automotive landscape, emphasizing adaptability and responsiveness to evolving consumer needs and technological trends.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of the Aftermarket Segment | +1.5% | Global, especially mature markets (North America, Europe) | Long-term |

| Growth in Emerging Automotive Markets (OEM demand) | +1.3% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Mid-term to Long-term |

| Development of Advanced and Lightweight Clutch Systems | +0.9% | Europe, Japan, China, North America | Mid-term |

| Niche Markets and Performance Vehicles | +0.6% | Global, specific enthusiast segments | Short-term to Mid-term |

Passenger Car Clutch Market Challenges Impact Analysis

The Passenger Car Clutch Market faces several significant challenges that require strategic navigation for sustained success. Foremost among these is the intense competitive landscape, characterized by a mix of established global players and regional manufacturers, leading to pricing pressures and the constant need for product differentiation. This competition necessitates continuous innovation and investment in research and development to stay relevant. Another major challenge is adapting to the rapid technological shifts within the broader automotive industry, particularly the accelerating transition towards automatic transmissions and, more critically, electric vehicles. As these technologies gain traction, the overall addressable market for traditional manual clutches shrinks, forcing manufacturers to either diversify their product offerings or focus on niche and aftermarket segments. Furthermore, meeting increasingly stringent global regulatory standards for vehicle emissions and fuel efficiency presents a complex challenge. While clutches themselves don't emit, they are part of the powertrain system that needs to be optimized for these standards, requiring advanced materials and precision engineering that can increase manufacturing costs. The dynamic nature of global supply chains also poses a persistent challenge, with potential disruptions impacting the availability and cost of raw materials and finished components, leading to production delays and increased operational expenses.

Beyond these, the declining preference for manual transmissions in several key markets, influenced by convenience and traffic conditions, represents a direct consumer-side challenge. This shift in consumer behavior means that manual driving skills are becoming less common, further reducing the overall demand base. The high investment required for manufacturing advanced clutch systems, coupled with uncertain long-term returns in a market facing fundamental technological disruption, can deter new investments and slow down innovation. Moreover, counterfeiting and the proliferation of low-quality, cheaper clutch parts in the aftermarket can erode the market share and reputation of legitimate manufacturers, impacting brand trust and profitability. Effectively managing these multifaceted challenges requires a strategic blend of technological agility, market responsiveness, and robust supply chain management. Companies in this sector must innovate not only in product design but also in business models, perhaps by focusing on lifecycle services or exploring emerging mobility solutions that still require power transmission components, even if not traditional clutches.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Declining Preference for Manual Transmissions in Key Markets | -1.0% | North America, Europe, Japan | Short-term to Mid-term |

| Intense Competition and Pricing Pressures | -0.7% | Global | Short-term to Mid-term |

| High R&D Costs for Advanced Clutch Technologies | -0.5% | Europe, Japan, North America | Mid-term |

| Supply Chain Volatility and Geopolitical Risks | -0.4% | Global, especially Asia Pacific manufacturing hubs | Short-term |

Passenger Car Clutch Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Passenger Car Clutch Market, offering critical insights into its current state, future projections, and the factors influencing its growth. The scope covers detailed market segmentation, regional dynamics, competitive landscape analysis, and an assessment of key market drivers, restraints, opportunities, and challenges. Designed for stakeholders, investors, and decision-makers, this report offers a robust foundation for strategic planning and informed business decisions within the automotive components sector. It integrates a thorough examination of both OEM and aftermarket segments, highlighting their respective contributions and growth prospects within the forecast period.

| Report Attributes | Report Details |

|---|---|

| Report Name | Passenger Car Clutch Market |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 23.0 Billion |

| Growth Rate | CAGR of 2025 to 2033 5.8% |

| Number of Pages | 280 |

| Key Companies Covered | ZF Friedrichshafen, Aisin Seiki, BorgWarner, Eaton, Schaeffler, EXEDY Corporation, Valeo, F.C.C., CNC Driveline, Zhejiang Tieliu, Ningbo Hongxie, Hubei Tri-Ring, Changchun Yidong Clutch, Wuhu Hefeng, Rongcheng Huanghai, Guilin Fuda, Hangzhou Qidie, Dongfeng Propeller |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:-- Friction Clutch: This segment includes the most common types of clutches found in manual transmission vehicles, relying on friction between components to transmit torque. They are characterized by their robust design and widespread application across various passenger car models. Friction clutches encompass single-plate, multi-plate, and centrifugal clutch designs, each suited for different power requirements and vehicle applications. Their market dominance is driven by their proven reliability, cost-effectiveness, and ease of maintenance, making them a staple in the automotive industry for decades.

- Electromagnetic Clutch: While less common in standard passenger cars for power transmission between engine and gearbox, electromagnetic clutches find niche applications, particularly in hybrid vehicles for controlling power flow from electric motors or in auxiliary systems like air conditioning compressors. These clutches operate based on electromagnetic principles, offering precise engagement and disengagement without mechanical linkage, allowing for smoother transitions and potentially greater efficiency in specific hybrid powertrain configurations. Their adoption in passenger cars is primarily limited to specialized functions rather than primary driveline engagement.

- OEMs (Original Equipment Manufacturers): This segment refers to the direct sales of clutches to automotive manufacturers for installation in new passenger vehicles during the assembly process. The OEM market is highly influenced by global vehicle production volumes, shifts in consumer preferences towards transmission types, and the adoption of new vehicle technologies such as electric vehicles. Manufacturers in this segment often engage in long-term supply agreements and collaborate closely with vehicle makers on design and technological integration. Demand here is characterized by large volume orders and adherence to stringent quality and performance specifications set by car manufacturers.

- Aftermarket: The aftermarket segment encompasses the sales of replacement clutches for existing passenger vehicles that require maintenance or repair. This market is driven by the size of the global vehicle parc, average vehicle age, driving habits, and the lifespan of original clutch components. As clutches are wear-and-tear parts, consistent demand from the aftermarket ensures a stable revenue stream for manufacturers, even as new vehicle sales trends fluctuate. This segment includes sales through independent repair shops, franchised dealerships, and retail channels, catering to a diverse range of vehicle models and owner needs, emphasizing durability, availability, and often, cost-effectiveness.

Regional Highlights

- Asia Pacific: This region is projected to be the leading market for passenger car clutches, driven by robust vehicle production volumes and high adoption rates of manual transmission vehicles in countries like India, China, and Southeast Asian nations. The burgeoning middle class, coupled with the affordability and fuel efficiency advantages of manual cars, sustains strong OEM demand. Furthermore, the large existing vehicle parc contributes significantly to the aftermarket segment, ensuring continuous demand for replacement clutches across the region. Rapid urbanization and economic growth also fuel the expansion of the automotive sector, making APAC a powerhouse for clutch market growth.

- Europe: While showing a gradual shift towards automatic transmissions and EVs, Europe remains a significant market for passenger car clutches, especially in countries with a strong tradition of manual driving such as Germany, Italy, and Eastern European nations. The region is a hub for technological advancements in clutch design, focusing on lightweight materials and improved performance for both OEM and aftermarket segments. Stringent emission regulations push manufacturers to innovate in terms of efficiency, indirectly benefiting clutch development. The established automotive infrastructure and a large vehicle fleet ensure consistent aftermarket demand.

- North America: Historically dominated by automatic transmissions, the North American market for passenger car clutches is primarily driven by the aftermarket segment. The immense number of older manual transmission vehicles still on the road generates a steady demand for replacement parts. While new manual transmission vehicle sales are comparatively low, niche segments, such as performance cars and compact economy models, maintain some OEM demand. The region's focus on vehicle longevity and maintenance also reinforces the aftermarket's importance.

- Latin America: This region represents a growing market, similar to parts of Asia Pacific, driven by the strong preference for affordable manual transmission vehicles. Countries like Brazil and Mexico are significant manufacturing hubs, contributing to both OEM and aftermarket demand. Economic development and increasing vehicle ownership rates contribute to a consistent need for clutches. The market here is characterized by a balance between cost-effectiveness and durability.

- Middle East and Africa (MEA): The MEA region is an emerging market for passenger car clutches, characterized by increasing automotive sales and a growing demand for cost-efficient manual transmission vehicles, particularly in African countries and parts of the Middle East. Infrastructure development and a rising disposable income support vehicle adoption, leading to both new car sales and a developing aftermarket. The market is influenced by imports and the establishment of local assembly plants, which drive OEM demand.

Top Key Players:

The market research report covers the analysis of key stake holders of the Passenger Car Clutch Market. Some of the leading players profiled in the report include -:- ZF Friedrichshafen

- Aisin Seiki

- BorgWarner

- Eaton

- Schaeffler

- EXEDY Corporation

- Valeo

- F.C.C.

- CNC Driveline

- Zhejiang Tieliu

- Ningbo Hongxie

- Hubei Tri-Ring

- Changchun Yidong Clutch

- Wuhu Hefeng

- Rongcheng Huanghai

- Guilin Fuda

- Hangzhou Qidie

- Dongfeng Propeller

Frequently Asked Questions:

What is the projected market size of the Passenger Car Clutch Market by 2033?

Response: The Passenger Car Clutch Market is projected to reach an estimated market size of USD 23.0 Billion by the end of 2033. This growth is driven by sustained demand from the aftermarket and continued production of manual transmission vehicles in emerging economies.

How will the increasing adoption of electric vehicles (EVs) impact the Passenger Car Clutch Market?

Response: The increasing adoption of electric vehicles (EVs) is a significant restraint on the Passenger Car Clutch Market. EVs typically do not require traditional clutches due to their different powertrain architectures, which utilize electric motors for direct power delivery. This fundamental shift reduces the long-term OEM demand for clutches. However, the large existing fleet of internal combustion engine vehicles ensures continued aftermarket demand for the foreseeable future.

What are the key drivers for growth in the Passenger Car Clutch Market?

Response: Key drivers for growth in the Passenger Car Clutch Market include the sustained production of manual transmission internal combustion engine vehicles, particularly in emerging markets where they offer economic advantages. Additionally, t

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted