Agricultural Tractor Market

Agricultural Tractor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705806 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

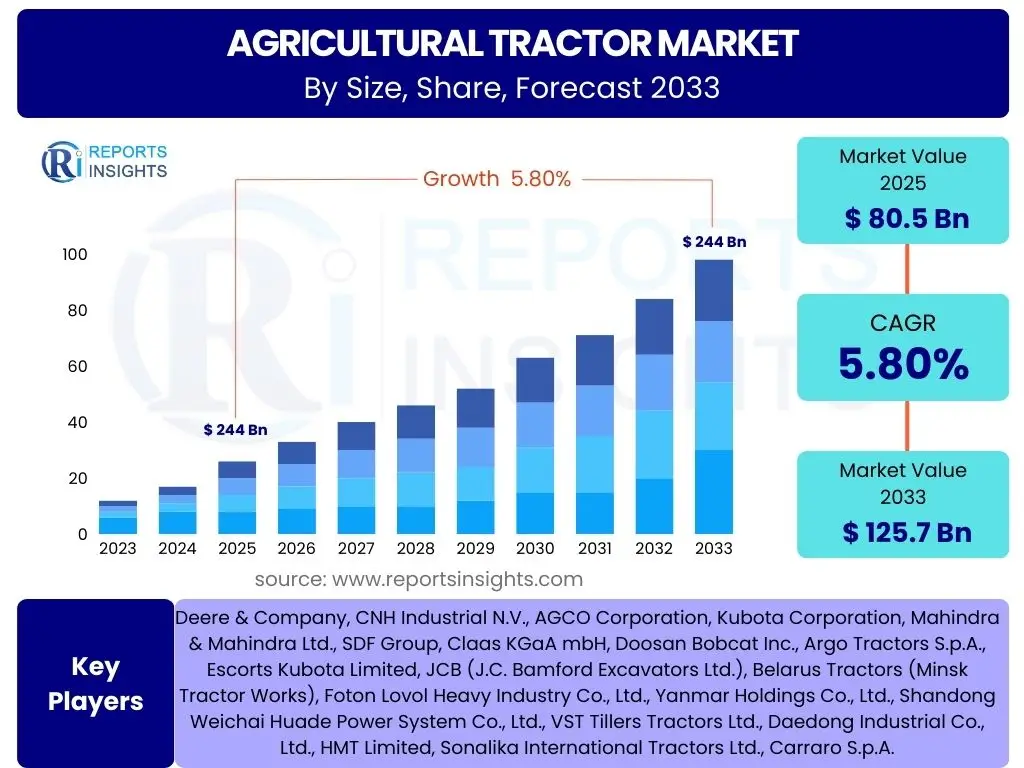

Agricultural Tractor Market Size

According to Reports Insights Consulting Pvt Ltd, The Agricultural Tractor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 80.5 billion in 2025 and is projected to reach USD 125.7 billion by the end of the forecast period in 2033.

Key Agricultural Tractor Market Trends & Insights

The agricultural tractor market is undergoing a transformative period driven by technological advancements and evolving agricultural practices. Key trends indicate a significant shift towards smart farming solutions, aiming to optimize efficiency, productivity, and sustainability in crop cultivation and livestock management. Farmers and agricultural enterprises are increasingly seeking equipment that integrates seamlessly with digital ecosystems, offering real-time data analysis and automation capabilities. This demand is not only for new purchases but also for retrofitting existing machinery, highlighting a broader industry movement towards intelligent agriculture.

Another prominent trend involves the adoption of alternative fuel sources and electric propulsion systems. Concerns over environmental impact and fluctuating fossil fuel prices are compelling manufacturers and end-users alike to explore more sustainable power solutions. While diesel remains dominant, research and development efforts are intensifying in electric, hybrid, and even hydrogen-powered tractors. This transition is expected to gain momentum, especially in regions with supportive regulatory frameworks and readily available charging or refueling infrastructure, signaling a long-term shift towards greener agricultural machinery.

Furthermore, the market is observing a growing emphasis on enhanced operator comfort and safety, alongside the integration of advanced telematics and connectivity. Modern tractors are being designed with ergonomic cabins, intuitive controls, and comprehensive sensor arrays that improve operational safety and reduce operator fatigue during long working hours. The ability to connect tractors to cloud-based platforms for remote diagnostics, predictive maintenance, and operational monitoring is also becoming a standard expectation, improving overall fleet management and operational uptime for large farming operations and contractor services.

- Integration of precision agriculture technologies (GPS, sensors, AI).

- Increasing adoption of electric and hybrid agricultural tractors.

- Development of autonomous and semi-autonomous tractor models.

- Growing demand for higher horsepower and specialized tractors for diverse applications.

- Emphasis on ergonomic design and enhanced operator comfort and safety.

- Expansion of digital farming platforms and telematics solutions for data-driven decision-making.

- Shift towards rental and leasing models for agricultural machinery.

AI Impact Analysis on Agricultural Tractor

The integration of Artificial Intelligence (AI) is fundamentally reshaping the agricultural tractor landscape, addressing common user questions regarding efficiency, autonomy, and data utilization in farming. Farmers are increasingly curious about how AI can enhance productivity, minimize operational costs, and reduce manual labor dependency. AI-powered systems enable tractors to perform tasks with unprecedented precision, such as optimized planting, targeted spraying, and precise harvesting, by analyzing vast datasets on soil conditions, crop health, and weather patterns. This capability moves beyond simple automation, allowing for highly adaptive and context-aware agricultural operations, leading to improved yields and reduced input waste.

AI's influence extends significantly into the realm of predictive analytics and machine maintenance for agricultural machinery. Users frequently inquire about preventing costly downtime and extending equipment lifespan. AI algorithms can monitor tractor performance in real-time, identifying potential mechanical failures before they occur by analyzing vibration, temperature, and fluid data. This predictive maintenance capability allows for scheduled servicing, significantly reducing unexpected breakdowns and ensuring maximum operational uptime during critical farming seasons. Such advancements directly address farmer concerns about equipment reliability and the economic impact of machinery malfunctions.

Moreover, the advent of AI is paving the way for advanced levels of autonomy in agricultural tractors, sparking discussions about labor requirements and the future of farming. While fully autonomous tractors are still evolving, AI is already powering features like self-driving capabilities within defined boundaries, automated implement control, and intelligent path planning. These capabilities mitigate the impact of labor shortages in the agricultural sector and allow farmers to manage larger areas with fewer personnel. The ongoing development of AI in this sector is set to redefine conventional farming practices, promising a future where agricultural operations are smarter, more efficient, and increasingly autonomous.

- Optimized resource utilization (fuel, water, fertilizer) through AI-driven analytics.

- Enhanced precision agriculture capabilities, including variable rate application.

- Development of advanced autonomous navigation and operation systems for tractors.

- Predictive maintenance for reduced downtime and extended equipment lifespan.

- Real-time monitoring and analysis of crop health and soil conditions.

- Improved safety features through AI-powered obstacle detection and avoidance.

- Data-driven decision-making for planting, irrigation, and harvesting schedules.

Key Takeaways Agricultural Tractor Market Size & Forecast

The agricultural tractor market is poised for robust growth through 2033, a key insight stemming from common inquiries about the future trajectory and investment potential within the sector. This expansion is primarily driven by the escalating global demand for food, which necessitates increased agricultural productivity and the widespread adoption of mechanization, particularly in developing economies. The forecast indicates that growth will be substantially fueled by continuous innovation, with a focus on integrating advanced technologies like AI, IoT, and automation into tractor design and functionality. This technological evolution is critical for addressing modern farming challenges, including labor shortages, climate change impacts, and the need for sustainable practices.

Another significant takeaway is the increasing bifurcation of demand within the market. While high-horsepower tractors continue to be essential for large-scale commercial farming, there is also a burgeoning demand for compact and utility tractors in smaller farms and specialized applications. This diverse demand profile highlights the adaptability of manufacturers to cater to a wide spectrum of agricultural needs across different farm sizes and regional contexts. Furthermore, the market's resilience is underscored by its capacity to integrate eco-friendly solutions, such as electric and alternative fuel-powered tractors, responding to global environmental regulations and consumer preferences for sustainable agriculture.

The market forecast also emphasizes the critical role of government support and subsidies in accelerating market growth, particularly in emerging agricultural economies. Policies promoting farm mechanization, offering financial assistance for equipment purchases, and encouraging sustainable farming practices are instrumental in driving tractor sales. Concurrently, the expansion of rental and leasing services for agricultural machinery is lowering the barrier to entry for smaller farmers, further contributing to market penetration and accessibility. These factors collectively indicate a dynamic and expanding market, characterized by technological evolution, diverse demand, and supportive external influences.

- Significant market expansion anticipated, driven by global food demand and mechanization.

- Technological advancements, including AI and automation, are central to future growth.

- Strong demand across various horsepower segments, from compact to high-power tractors.

- Sustainable and eco-friendly tractor solutions are gaining increasing traction.

- Emerging economies are projected to be key growth engines due to increasing farm incomes and government support.

- The rental and leasing market for agricultural tractors is set to grow, enhancing accessibility.

Agricultural Tractor Market Drivers Analysis

The agricultural tractor market is significantly propelled by several key drivers, primarily the escalating global population and the resultant increase in demand for food. This fundamental requirement necessitates higher agricultural output, which in turn drives the adoption of advanced farm mechanization solutions to enhance productivity and efficiency. Furthermore, ongoing technological advancements, particularly in areas like precision agriculture and automation, are transforming tractors into sophisticated tools capable of optimizing various farming operations, making them indispensable for modern agricultural practices. These innovations not only improve yields but also address critical issues such as resource conservation and environmental sustainability.

Government initiatives and supportive policies in many countries play a crucial role in stimulating market growth. Subsidies, financial incentives, and schemes promoting farm mechanization encourage farmers to invest in new and technologically advanced tractors, especially in developing regions. Concurrently, a persistent shortage of agricultural labor in many parts of the world, exacerbated by rural-to-urban migration, is driving the demand for automated and efficient machinery that can perform tasks traditionally done manually, thereby reducing operational costs and dependency on human labor. These factors collectively create a robust environment for sustained growth in the agricultural tractor market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Food Demand | +1.5% | Global, particularly APAC & Africa | Long-term (2025-2033) |

| Rising Farm Mechanization | +1.2% | Asia Pacific, Latin America | Mid to Long-term (2025-2033) |

| Technological Advancements in Agriculture | +1.0% | North America, Europe, Developed APAC | Ongoing (2025-2033) |

| Government Support & Subsidies | +0.8% | India, China, EU, US | Mid-term (2025-2030) |

| Labor Shortages in Agriculture | +0.5% | North America, Europe, parts of Asia | Long-term (2025-2033) |

Agricultural Tractor Market Restraints Analysis

Despite robust growth prospects, the agricultural tractor market faces several significant restraints that could impede its expansion. One primary concern is the high initial investment cost associated with purchasing modern, technologically advanced tractors. This cost can be prohibitive for small and marginal farmers, especially in developing countries where access to credit and financial resources may be limited. The substantial capital outlay required acts as a significant barrier to adoption, slowing down the pace of farm mechanization in certain regions and segments.

Another critical restraint is the fluctuating prices of agricultural commodities. When crop prices decline, farmers' incomes are negatively impacted, leading to reduced purchasing power and a hesitation to invest in new machinery. This economic volatility directly influences demand for agricultural tractors, making it difficult for manufacturers to predict market trends and plan production schedules effectively. Furthermore, stringent environmental regulations and emission standards imposed by governments in various regions necessitate continuous research and development efforts to comply, which adds to the manufacturing cost and complexity, potentially increasing the final price for consumers.

The lack of adequate infrastructure and skilled labor in many emerging markets also presents a considerable challenge. The successful operation and maintenance of modern tractors, particularly those integrated with advanced digital technologies, require trained personnel for both operation and servicing. In regions where such expertise is scarce, the adoption of sophisticated machinery can be slow. Additionally, land fragmentation, common in some parts of Asia and Africa, limits the economic viability of large, high-horsepower tractors, favoring smaller, less efficient machines or traditional farming methods, thereby restraining market growth in these areas.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Cost | -0.9% | Developing Regions (APAC, Africa) | Long-term (2025-2033) |

| Fluctuating Agricultural Commodity Prices | -0.7% | Global | Short to Mid-term (2025-2028) |

| Lack of Skilled Labor for Advanced Machinery | -0.6% | Developing Regions | Long-term (2025-2033) |

| Stringent Environmental Regulations | -0.5% | Europe, North America | Ongoing (2025-2033) |

| Land Fragmentation | -0.4% | Parts of Asia, Africa | Long-term (2025-2033) |

Agricultural Tractor Market Opportunities Analysis

The agricultural tractor market presents substantial growth opportunities driven by evolving agricultural practices and technological innovation. The increasing adoption of precision agriculture techniques globally creates a significant demand for tractors equipped with advanced sensors, GPS, and data analytics capabilities. These technologies enable farmers to optimize input usage, enhance yield, and minimize environmental impact, representing a lucrative niche for manufacturers to develop and market specialized machinery and integrated solutions. The ongoing digital transformation in agriculture is thus opening new revenue streams for tractor manufacturers beyond traditional sales.

Furthermore, the growing global emphasis on sustainability and environmental protection offers a fertile ground for the development and commercialization of electric and hybrid tractors. As governments and consumers push for reduced carbon footprints, manufacturers have an opportunity to lead in the development of eco-friendly machinery that offers lower emissions, reduced noise, and potentially lower operating costs in the long run. Investments in research and development for alternative fuel sources and energy-efficient designs can position companies favorably in a market increasingly valuing green solutions.

Another significant opportunity lies in the expansion of rental and leasing services for agricultural machinery. This model addresses the high initial investment cost, making advanced tractors more accessible to small and medium-sized farms that might not be able to afford outright purchases. By offering flexible financing and usage options, manufacturers and third-party service providers can tap into a broader customer base, particularly in emerging economies where financial constraints are more prevalent. Additionally, the aftermarket services sector, including spare parts, maintenance, and technological upgrades, represents a continuous revenue stream, further enhancing market potential as the installed base of modern tractors grows globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Precision Agriculture | +1.3% | Global, especially North America, Europe | Long-term (2025-2033) |

| Development of Electric/Hybrid Tractors | +1.0% | Europe, North America, China | Mid to Long-term (2027-2033) |

| Growth in Rental & Leasing Services | +0.8% | Developing Regions (APAC, Latin America) | Mid-term (2025-2030) |

| Expansion in Emerging Economies | +0.7% | India, Brazil, Southeast Asia | Long-term (2025-2033) |

| Aftermarket Services & Parts | +0.6% | Global | Ongoing (2025-2033) |

Agricultural Tractor Market Challenges Impact Analysis

The agricultural tractor market faces a unique set of challenges that could hinder its growth and development. One significant hurdle is the vulnerability to global supply chain disruptions, as evidenced by recent events. The manufacturing of tractors relies heavily on a complex network of suppliers for components such as semiconductors, steel, and other raw materials. Any disruptions, whether due to geopolitical tensions, natural disasters, or pandemics, can lead to production delays, increased costs, and ultimately, a shortfall in product availability, directly impacting market stability and growth.

Another pressing challenge, particularly with the increasing digitalization of agricultural machinery, is the rising threat of cybersecurity risks. As tractors become more connected and reliant on integrated software and data systems for autonomous operations and precision farming, they become potential targets for cyberattacks. Such attacks could compromise sensitive agricultural data, disrupt operational control, or even disable machinery, leading to significant financial losses and erosion of trust in advanced agricultural technologies. Ensuring robust cybersecurity measures becomes paramount for manufacturers and users alike.

Furthermore, the rapid pace of technological innovation, while a driver of growth, also presents a challenge of technological obsolescence. Tractors purchased today might quickly become outdated as newer, more efficient, and more automated models enter the market. This can affect farmers' return on investment and create pressure on manufacturers to constantly innovate, increasing R&D costs and potentially shortening product lifecycles. Additionally, the intense competition within the market leads to price sensitivity, especially in segments focused on smaller or less technologically advanced tractors, pressuring profit margins for manufacturers and distributors.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions | -0.8% | Global | Short to Mid-term (2025-2027) |

| Cybersecurity Risks in Connected Tractors | -0.6% | Global (Developed Markets) | Long-term (2025-2033) |

| Rapid Technological Obsolescence | -0.5% | Global | Mid to Long-term (2028-2033) |

| Price Sensitivity in Competitive Markets | -0.4% | Global | Ongoing (2025-2033) |

| Infrastructure Limitations for Advanced Tech | -0.3% | Developing Regions | Long-term (2025-2033) |

Agricultural Tractor Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Agricultural Tractor Market, offering valuable insights into its current status, historical performance, and future growth trajectory. The scope encompasses detailed market sizing, trends, drivers, restraints, opportunities, and challenges affecting the industry across various segments and key geographical regions. It serves as a strategic guide for stakeholders, investors, and industry participants seeking to understand market dynamics and make informed decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 80.5 Billion |

| Market Forecast in 2033 | USD 125.7 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Mahindra & Mahindra Ltd., SDF Group, Claas KGaA mbH, Doosan Bobcat Inc., Argo Tractors S.p.A., Escorts Kubota Limited, JCB (J.C. Bamford Excavators Ltd.), Belarus Tractors (Minsk Tractor Works), Foton Lovol Heavy Industry Co., Ltd., Yanmar Holdings Co., Ltd., Shandong Weichai Huade Power System Co., Ltd., VST Tillers Tractors Ltd., Daedong Industrial Co., Ltd., HMT Limited, Sonalika International Tractors Ltd., Carraro S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The agricultural tractor market is comprehensively segmented to provide a granular view of its diverse components and sub-sectors. This segmentation allows for a detailed understanding of market dynamics based on tractor specifications, intended applications, level of automation, and fuel type. Each segment reflects specific demands and technological preferences, enabling a targeted analysis of growth opportunities and competitive landscapes. The engine power segment, for instance, categorizes tractors based on their horsepower, catering to varying farm sizes and operational requirements, from small-scale farming to heavy-duty commercial agriculture. Similarly, the drive type segmentation differentiates between 2-wheel drive and 4-wheel drive tractors, addressing needs related to traction, terrain, and efficiency.

Further segmentation by application highlights the versatility of modern tractors, which are used for a multitude of tasks beyond basic plowing, including harvesting, sowing, and haulage, reflecting the evolving needs of diversified farming practices. The burgeoning automation segment, encompassing manual, semi-autonomous, and autonomous models, illustrates the industry's shift towards intelligent farming solutions that reduce labor dependency and enhance precision. Lastly, the fuel type segmentation, covering diesel, electric/hybrid, gasoline, and other emerging alternatives, underscores the industry's commitment to sustainability and energy efficiency, driven by environmental regulations and fuel cost considerations. This multi-dimensional segmentation is crucial for understanding the intricate demand patterns and technological advancements shaping the global agricultural tractor market.

- By Engine Power:

- Below 40 HP

- 40-100 HP

- Above 100 HP

- By Drive Type:

- 2-Wheel Drive

- 4-Wheel Drive

- By Application:

- Plowing

- Harvesting

- Sowing

- Haulage

- Others

- By Automation:

- Manual

- Semi-Autonomous

- Autonomous

- By Fuel Type:

- Diesel

- Electric/Hybrid

- Gasoline

- Others

Regional Highlights

The global agricultural tractor market exhibits significant regional variations, influenced by factors such as farming practices, economic development, government policies, and technological adoption rates. Each major region contributes uniquely to the overall market landscape, presenting distinct growth opportunities and challenges. Understanding these regional nuances is crucial for strategic market entry and expansion.

- North America: This region represents a mature market characterized by large-scale commercial farming, high adoption of advanced precision agriculture technologies, and a strong emphasis on automation. Demand is driven by the need for high-horsepower tractors and integrated digital solutions to maximize efficiency and mitigate labor shortages. Government incentives for sustainable farming also encourage the adoption of newer, more eco-friendly models.

- Europe: The European market is highly influenced by stringent environmental regulations and a strong focus on sustainability. This drives demand for fuel-efficient, low-emission, and electric/hybrid tractors. Precision farming technologies are widely adopted, and there is a growing trend towards specialized tractors for vineyards, orchards, and smaller farms. Support for organic farming and smart agriculture initiatives further bolsters market growth.

- Asia Pacific (APAC): APAC is the largest and fastest-growing market for agricultural tractors, primarily driven by countries like China, India, and Southeast Asian nations. Increasing population, government support for farm mechanization, rising agricultural income, and a shift from subsistence to commercial farming are key factors. The region sees demand for a wide range of tractors, from compact models for small landholdings to high-horsepower units for large agricultural enterprises, coupled with growing adoption of basic and advanced mechanization.

- Latin America: This region is experiencing significant growth in agricultural output due to increasing global demand for food commodities, leading to rising investments in farm mechanization. Countries such as Brazil and Argentina are key markets, with large agricultural areas driving demand for high-horsepower tractors suitable for extensive cultivation. The expansion of agricultural exports and improved economic conditions are fostering market development.

- Middle East and Africa (MEA): The MEA region's agricultural tractor market is influenced by efforts to enhance food security, modernize traditional farming practices, and expand arable land. Government initiatives and international aid promoting agricultural development are contributing to market growth. While still emerging, there is increasing demand for robust and versatile tractors capable of operating in diverse and often challenging environmental conditions, particularly in regions prone to water scarcity and soil degradation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Agricultural Tractor Market.

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- SDF Group

- Claas KGaA mbH

- Doosan Bobcat Inc.

- Argo Tractors S.p.A.

- Escorts Kubota Limited

- JCB (J.C. Bamford Excavators Ltd.)

- Belarus Tractors (Minsk Tractor Works)

- Foton Lovol Heavy Industry Co., Ltd.

- Yanmar Holdings Co., Ltd.

- Shandong Weichai Huade Power System Co., Ltd.

- VST Tillers Tractors Ltd.

- Daedong Industrial Co., Ltd.

- HMT Limited

- Sonalika International Tractors Ltd.

- Carraro S.p.A.

Frequently Asked Questions

What factors are driving the growth of the agricultural tractor market?

The agricultural tractor market is primarily driven by increasing global food demand, necessitating greater agricultural productivity and efficiency. This is further supported by widespread farm mechanization efforts, particularly in developing economies, and continuous technological advancements in tractor design, including precision agriculture features and automation. Additionally, government initiatives and subsidies promoting modern farming practices, alongside a global shortage of agricultural labor, are significant accelerators for market expansion.

How is technology, particularly AI, transforming agricultural tractors?

AI is profoundly transforming agricultural tractors by enabling higher levels of precision, efficiency, and autonomy. AI-powered systems facilitate optimized resource use through variable rate applications, real-time crop health monitoring, and data-driven decision-making for planting and harvesting. Moreover, AI is crucial for developing advanced autonomous navigation capabilities, predictive maintenance systems that minimize downtime, and enhanced safety features, collectively leading to more sustainable and productive farming operations.

Which regions are expected to show significant growth in the agricultural tractor market?

The Asia Pacific (APAC) region is projected to be the largest and fastest-growing market, driven by extensive farm mechanization initiatives in countries like India and China, coupled with rising agricultural incomes. Latin America is also expected to exhibit strong growth due to increasing agricultural exports and the expansion of large-scale farming. Additionally, while North America and Europe are mature markets, they continue to grow with the adoption of high-tech and environmentally friendly tractor solutions.

What are the primary challenges faced by the agricultural tractor market?

The agricultural tractor market faces several challenges, including the high initial investment cost, which can deter small and marginal farmers. Fluctuating agricultural commodity prices directly impact farmers' purchasing power, creating market volatility. Furthermore, the industry contends with global supply chain disruptions for critical components, the growing threat of cybersecurity risks in connected tractors, and the rapid pace of technological obsolescence, which can impact equipment longevity and necessitate continuous R&D.

What are the key emerging trends in agricultural tractor design and functionality?

Key emerging trends include the widespread integration of precision agriculture technologies, such as GPS, sensors, and IoT connectivity, allowing for highly optimized farming. There is a growing focus on the development and adoption of electric and hybrid tractors to enhance sustainability and reduce emissions. Autonomous and semi-autonomous capabilities are also rapidly advancing. Additionally, manufacturers are prioritizing ergonomic design, advanced telematics for remote monitoring, and comprehensive digital platforms for improved operator comfort and data-driven farm management.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted