Car Audio Market

Car Audio Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710293 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

Car Audio Market Size

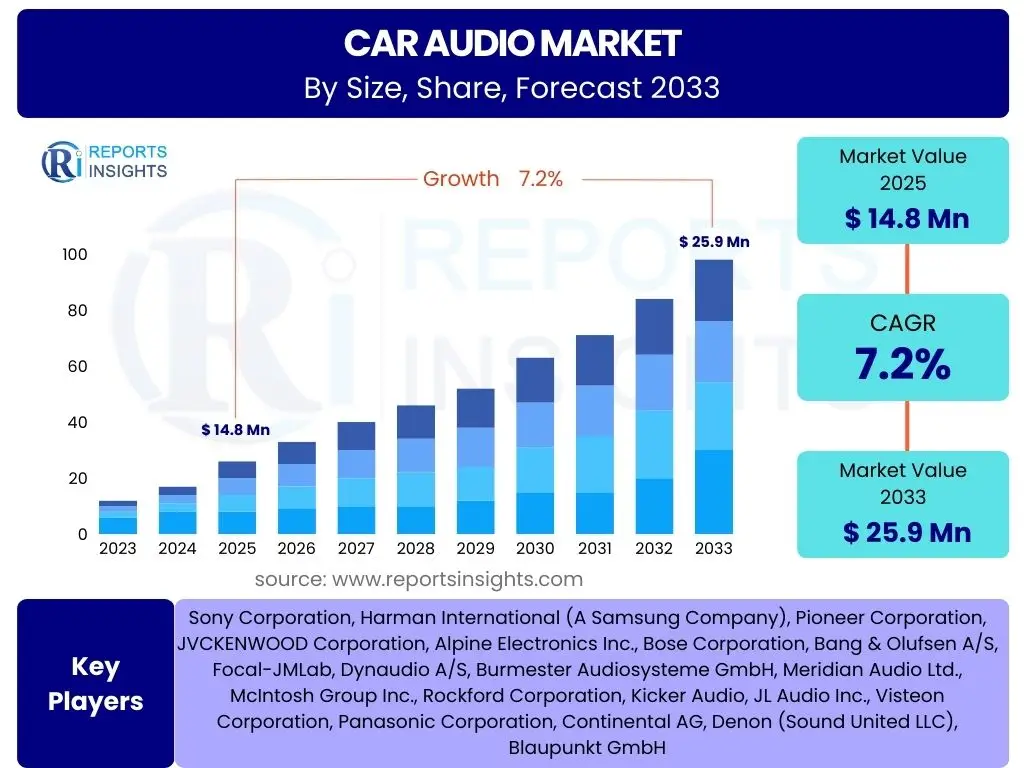

According to Reports Insights Consulting Pvt Ltd, The Car Audio Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 14.8 Billion in 2025 and is projected to reach USD 25.9 Billion by the end of the forecast period in 2033.

Key Car Audio Market Trends & Insights

The car audio market is undergoing a significant transformation, driven by consumer demand for superior sound quality, seamless connectivity, and personalized in-vehicle entertainment experiences. Users frequently inquire about the integration of advanced technologies, the evolution of sound systems from basic playback to immersive auditory environments, and the impact of smart vehicle ecosystems on audio design. A key trend involves the convergence of automotive infotainment with high-fidelity audio, creating a unified digital cockpit experience.

Another prominent insight reveals a growing emphasis on acoustic optimization tailored to specific vehicle interiors, moving beyond generic sound profiles. This includes active noise cancellation and sound enhancement technologies that adapt to driving conditions and passenger preferences. Furthermore, the aftermarket continues to innovate, offering diverse upgrade paths for consumers seeking customized solutions, while original equipment manufacturers (OEMs) are increasingly partnering with premium audio brands to differentiate their vehicles with signature sound experiences.

- High-resolution audio integration and lossless streaming capabilities.

- Wireless connectivity proliferation, including advanced Bluetooth codecs and Wi-Fi streaming.

- Personalized audio zones and multi-channel sound systems for immersive experiences.

- Active noise cancellation and sound enhancement technologies for optimal acoustic environments.

- Seamless integration with smartphone interfaces (Apple CarPlay, Android Auto) and voice assistants.

- Demand for premium branded audio systems in new vehicle offerings.

- Aftermarket innovation focusing on modular upgrades and digital sound processing.

AI Impact Analysis on Car Audio

Users frequently ask how artificial intelligence will revolutionize their car audio experience, specifically regarding voice commands, personalization, and adaptive sound. AI's influence extends beyond mere voice control, paving the way for highly intelligent and responsive audio systems that learn user preferences, optimize sound delivery based on cabin acoustics and external noise, and even integrate with advanced driver-assistance systems for safety alerts. This deep integration allows for a dynamic listening environment, where the audio system intelligently anticipates needs and adjusts accordingly.

The application of AI in car audio also encompasses predictive analytics for system maintenance and performance optimization, ensuring longevity and consistent audio quality. Furthermore, AI algorithms are becoming central to creating immersive soundscapes, enabling sophisticated spatial audio processing that adapts to the number of occupants and their positions within the vehicle. This means a more tailored and engaging audio experience for every passenger, transforming the car from a mere transport mode into a highly personalized entertainment hub.

- Enhanced voice AI for intuitive control of audio functions, navigation, and smart home integration.

- Adaptive sound optimization based on ambient noise, vehicle speed, road conditions, and passenger count.

- Personalized music recommendations and automatic playlist generation tailored to individual preferences and driving habits.

- Predictive maintenance for audio components, alerting users to potential issues before failure.

- Advanced digital signal processing (DSP) powered by AI for superior sound staging and clarity.

- Intelligent noise cancellation systems that learn and adapt to specific in-cabin acoustics.

- Integration with vehicle telematics for contextual audio delivery, such as traffic alerts or safety warnings.

Key Takeaways Car Audio Market Size & Forecast

Analyzing common user questions about the future of the car audio market reveals a strong interest in its growth trajectory, the underlying drivers, and the long-term viability of advanced in-vehicle entertainment solutions. The market is poised for robust expansion, primarily fueled by continuous technological advancements, increasing disposable incomes in emerging economies, and the growing consumer desire for sophisticated digital experiences within their vehicles. This growth is not merely volumetric but also qualitative, focusing on premiumization and integration.

A significant takeaway is the pivotal role of connectivity and smart vehicle integration in shaping future market dynamics. As vehicles become more connected and autonomous, car audio systems will evolve from standalone components into integral parts of a larger, intelligent infotainment ecosystem. The forecast indicates sustained investment in research and development to push the boundaries of acoustic engineering and user interface design, ensuring that the car audio sector remains a vibrant and innovative segment of the automotive industry.

- The market demonstrates strong growth potential, projected to reach USD 25.9 Billion by 2033.

- Technological innovation, particularly in digital processing, connectivity, and AI, is a primary growth engine.

- Consumer demand for premium sound quality and personalized in-car experiences is accelerating market expansion.

- Integration with smart vehicle ecosystems and infotainment platforms is crucial for future development.

- Aftermarket solutions continue to offer significant opportunities for customization and upgrades.

- Emerging markets present substantial untapped potential for both OEM and aftermarket segments.

Car Audio Market Drivers Analysis

The car audio market is significantly propelled by several key drivers that reflect evolving consumer expectations and technological advancements. A primary driver is the increasing demand for high-quality, immersive audio experiences within vehicles, mirroring the trend observed in home entertainment systems. Consumers are increasingly viewing their car as an extension of their digital lifestyle, expecting seamless integration with their personal devices and access to diverse streaming content. This expectation drives manufacturers to incorporate advanced features like high-resolution audio support, enhanced connectivity options, and sophisticated digital signal processing.

Furthermore, the steady growth in global vehicle production, particularly in developing economies, coupled with a rising preference for premium and luxury vehicles that often include advanced audio systems as standard, contributes substantially to market expansion. The rapid pace of innovation in areas such as wireless communication protocols, active noise cancellation, and personalized sound zones also acts as a strong catalyst. These innovations not only improve the listening experience but also differentiate products in a competitive landscape, encouraging upgrades and new purchases across both OEM and aftermarket segments. The shift towards electric vehicles also presents a unique opportunity for superior audio, given the quieter cabin environment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Premium Audio Experiences | +1.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Technological Advancements in Connectivity & DSP | +1.2% | Global, leading in developed economies | Medium to Long-term (2025-2033) |

| Growth in Vehicle Production and Sales | +0.8% | Asia Pacific, Latin America, Europe | Medium-term (2025-2030) |

| Proliferation of Connected Car Technology | +1.0% | Global, with strong adoption in North America, Europe | Long-term (2025-2033) |

| Rising Disposable Incomes in Emerging Markets | +0.7% | China, India, Brazil, Southeast Asia | Medium to Long-term (2025-2033) |

Car Audio Market Restraints Analysis

Despite robust growth, the car audio market faces several restraints that could impede its trajectory. A significant challenge is the relatively high cost associated with advanced audio systems, particularly those featuring premium components, sophisticated digital signal processing, and extensive acoustic tuning. This cost can deter price-sensitive consumers, especially in value-conscious market segments or during economic downturns, potentially leading them to opt for more basic factory-installed systems or entry-level aftermarket alternatives. The perception of diminishing returns on investment for ultra-premium systems also plays a role in consumer purchasing decisions.

Another major restraint is the increasing integration of infotainment systems directly into the vehicle's core architecture by original equipment manufacturers. These integrated solutions often make aftermarket upgrades more complex, expensive, or even impossible due to proprietary software, specialized wiring harnesses, and vehicle warranty concerns. Furthermore, the global supply chain disruptions for electronic components, exacerbated by geopolitical factors and increasing demand, can lead to production delays and higher manufacturing costs, thereby limiting market supply and impacting pricing strategies across the industry. The rapid obsolescence of technology also means significant R&D investment is required to stay competitive, adding to cost pressures.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Audio Systems | -0.9% | Global, more pronounced in emerging markets | Long-term (2025-2033) |

| Integration Complexity with OEM Systems | -0.7% | North America, Europe, China | Medium to Long-term (2025-2033) |

| Supply Chain Disruptions & Component Shortages | -0.6% | Global | Short to Medium-term (2025-2027) |

| Economic Volatility and Consumer Price Sensitivity | -0.5% | Global, especially sensitive economies | Short to Medium-term (2025-2028) |

| Rapid Technological Obsolescence | -0.4% | Global | Medium to Long-term (2025-2033) |

Car Audio Market Opportunities Analysis

The car audio market is ripe with opportunities, particularly in catering to the evolving landscape of electric vehicles (EVs) and the increasing sophistication of in-vehicle infotainment. EVs, with their inherently quieter cabins, present an ideal environment for showcasing high-fidelity audio systems, allowing nuances of sound to be appreciated without engine noise interference. This opens avenues for manufacturers to innovate with specialized acoustic designs and premium components optimized for the EV experience, making superior audio a key differentiator for these vehicles. Furthermore, the modular nature of EV platforms can sometimes offer greater flexibility for integrated audio solutions.

Another significant opportunity lies in the expansion into emerging markets, where rising disposable incomes and increasing vehicle ownership are fueling demand for both new cars and aftermarket upgrades. These regions represent a vast, relatively untapped consumer base eager for advanced entertainment features previously inaccessible. Additionally, the development of personalized audio zones, subscription-based services for premium audio content, and the integration of advanced haptic feedback within audio systems offer novel revenue streams and avenues for consumer engagement. Innovation in materials science for lighter, more efficient, and acoustically superior speaker components also presents a long-term growth opportunity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Electric Vehicle (EV) Market | +1.1% | Global, strong in Europe, China, North America | Long-term (2025-2033) |

| Expansion into Emerging Markets (e.g., APAC, LATAM) | +0.9% | China, India, Southeast Asia, Brazil, Mexico | Medium to Long-term (2025-2033) |

| Development of Personalized Audio Zones | +0.8% | North America, Europe, Japan | Medium to Long-term (2026-2033) |

| Subscription-based Audio Content & Services | +0.7% | Global, strong in developed markets | Medium to Long-term (2025-2033) |

| Innovation in Advanced Materials for Components | +0.6% | Global R&D centers | Long-term (2027-2033) |

Car Audio Market Challenges Impact Analysis

The car audio market faces several intrinsic challenges that demand strategic responses from manufacturers and suppliers. One significant challenge is the rapid pace of technological change, leading to short product lifecycles and the continuous need for research and development investment. Consumers expect the latest features, from advanced streaming capabilities to integrated voice assistants, which requires companies to frequently update their product lines, often at substantial cost. This can lead to market saturation with rapidly evolving technologies, making differentiation difficult and leading to pricing pressures.

Another major hurdle is the increasing complexity of integrating audio systems with sophisticated vehicle electronics and software architectures. Modern vehicles are essentially computers on wheels, and ensuring seamless compatibility, cybersecurity, and future-proofing for over-the-air updates requires deep technical expertise and collaboration across multiple automotive domains. Furthermore, intellectual property protection, particularly for digital signal processing algorithms and unique acoustic designs, remains a persistent challenge in a globally competitive market. Maintaining profitability amidst these complexities, while adhering to stringent automotive safety and reliability standards, poses a continuous test for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -0.8% | Global | Long-term (2025-2033) |

| Integration Complexity with Vehicle Architectures | -0.7% | Global, particularly OEM segment | Long-term (2025-2033) |

| Intellectual Property Protection & Counterfeiting | -0.6% | Global, more in Asia Pacific | Long-term (2025-2033) |

| Adherence to Evolving Safety & Regulatory Standards | -0.5% | Europe, North America, Japan | Medium to Long-term (2025-2033) |

| Cybersecurity Risks for Connected Audio Systems | -0.4% | Global | Long-term (2025-2033) |

Car Audio Market - Updated Report Scope

This report provides a comprehensive and in-depth analysis of the Car Audio Market, covering historical data, current market dynamics, and future projections. It delves into the key drivers, restraints, opportunities, and challenges shaping the industry, alongside a detailed segmentation analysis by component, technology, vehicle type, and distribution channel. The scope also includes a thorough examination of regional market trends and competitive landscape, offering actionable insights for stakeholders. The report aims to furnish a robust foundation for strategic decision-making and market forecasting within the car audio sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.8 Billion |

| Market Forecast in 2033 | USD 25.9 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sony Corporation, Harman International (A Samsung Company), Pioneer Corporation, JVCKENWOOD Corporation, Alpine Electronics Inc., Bose Corporation, Bang & Olufsen A/S, Focal-JMLab, Dynaudio A/S, Burmester Audiosysteme GmbH, Meridian Audio Ltd., McIntosh Group Inc., Rockford Corporation, Kicker Audio, JL Audio Inc., Visteon Corporation, Panasonic Corporation, Continental AG, Denon (Sound United LLC), Blaupunkt GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

A detailed segmentation analysis is crucial for understanding the intricate dynamics of the Car Audio Market, allowing for targeted strategies and identifying specific growth pockets across different product categories, technologies, and end-user demographics. This comprehensive breakdown provides insights into consumer preferences, technological adoption rates, and market saturation levels within various sub-segments. By examining these distinct categories, stakeholders can better identify lucrative opportunities, tailor product development, and refine marketing efforts to meet the diverse needs of the global automotive audio consumer base.

Each segment, from core components like head units and speakers to advanced technologies such as AI-driven personalization and specific vehicle applications, reveals unique trends and competitive landscapes. For instance, the distinction between OEM and aftermarket channels highlights varying consumer motivations and purchasing behaviors. Furthermore, analyzing the market by price range (entry-level, mid-range, premium) helps in understanding demand elasticity and the positioning of different product offerings across diverse economic strata. This granular view is essential for navigating the complexities of the market and making informed strategic decisions.

- By Component: Head Unit, Speakers, Amplifiers, Subwoofers, Digital Signal Processors, Cables & Wiring, Others

- By Technology: Bluetooth, USB, Auxiliary (AUX), Wi-Fi, Apple CarPlay, Android Auto, HD Radio, Satellite Radio, Voice Recognition, Gesture Control, ADAS Integration

- By Vehicle Type: Passenger Cars (Hatchback, Sedan, SUV, EV), Commercial Vehicles (Light Commercial Vehicles, Heavy Commercial Vehicles, Buses & Coaches)

- By Distribution Channel: Original Equipment Manufacturer (OEM), Aftermarket (Retail Stores, Online Sales, Specialty Shops)

- By Price Range: Entry-level, Mid-range, Premium

Regional Highlights

- North America: A mature market characterized by high consumer demand for premium audio systems and advanced infotainment features. The United States and Canada are key contributors, driven by a strong aftermarket segment and increasing integration of connected car technologies.

- Europe: Exhibits robust growth with a focus on high-fidelity sound and sophisticated acoustic engineering, particularly in Germany, the UK, and France. The region is a hub for luxury automotive brands and early adoption of advanced audio technologies, including personalized soundscapes.

- Asia Pacific (APAC): The fastest-growing region, fueled by rising vehicle production and increasing disposable incomes in countries like China, India, Japan, and South Korea. This region sees significant demand for both OEM-fitted systems and a burgeoning aftermarket, with a strong emphasis on smartphone integration and value-for-money propositions.

- Latin America: Demonstrates steady growth, with Brazil and Mexico leading the market. Consumer demand is largely driven by affordability and the integration of essential connectivity features. The aftermarket segment plays a vital role in this region due to consumer preference for customization.

- Middle East and Africa (MEA): An emerging market with growth opportunities, particularly in GCC countries due to high per capita income and a preference for luxury vehicles. South Africa is a notable market in the African continent, with a focus on both new vehicle sales and aftermarket upgrades.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Car Audio Market.- Sony Corporation

- Harman International (A Samsung Company)

- Pioneer Corporation

- JVCKENWOOD Corporation

- Alpine Electronics Inc.

- Bose Corporation

- Bang & Olufsen A/S

- Focal-JMLab

- Dynaudio A/S

- Burmester Audiosysteme GmbH

- Meridian Audio Ltd.

- McIntosh Group Inc.

- Rockford Corporation

- Kicker Audio

- JL Audio Inc.

- Visteon Corporation

- Panasonic Corporation

- Continental AG

- Denon (Sound United LLC)

- Blaupunkt GmbH

Frequently Asked Questions

Analyze common user questions about the Car Audio market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Car Audio Market?

The Car Audio Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033, reaching USD 25.9 Billion by the end of the forecast period.

How is AI impacting the Car Audio industry?

AI is significantly impacting car audio through enhanced voice control, adaptive sound optimization based on cabin conditions, personalized music recommendations, and predictive maintenance, creating a more intelligent and tailored listening experience.

What are the primary drivers of growth in the Car Audio Market?

Key growth drivers include increasing consumer demand for premium audio and immersive sound, advancements in connectivity and digital signal processing, growth in global vehicle production, and the proliferation of connected car technologies.

Which regions are leading the Car Audio Market?

North America and Europe are mature markets leading in premium demand and technological adoption, while Asia Pacific, particularly China and India, is the fastest-growing region driven by rising vehicle sales and disposable incomes.

What are the main challenges facing the Car Audio Market?

Major challenges include the high cost of advanced systems, complexity in integrating with modern vehicle architectures, supply chain disruptions, rapid technological obsolescence, and the need for robust intellectual property protection.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted