Passenger Car Clutch Market

Passenger Car Clutch Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700577 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

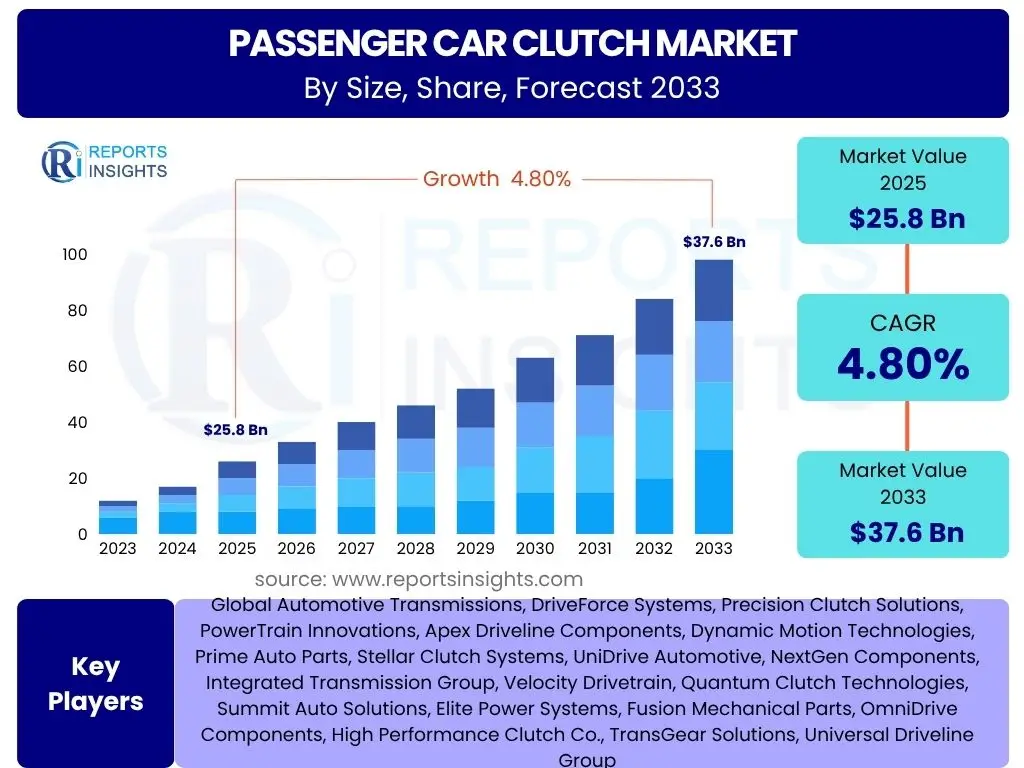

Passenger Car Clutch Market Size

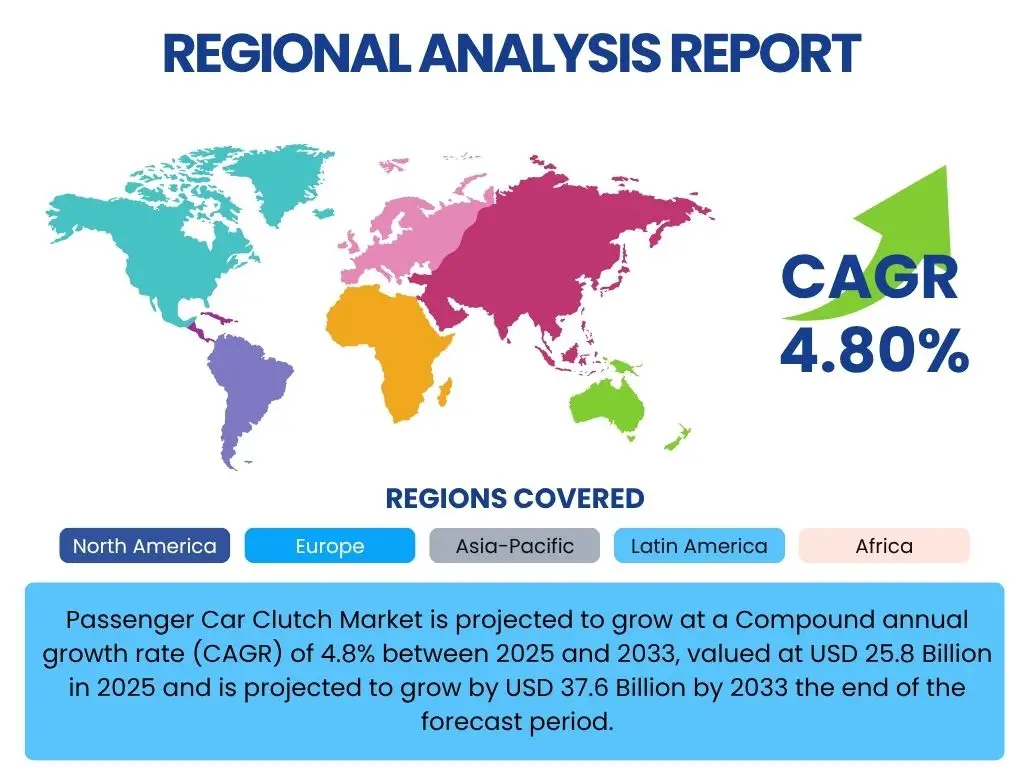

Passenger Car Clutch Market is projected to grow at a Compound annual growth rate (CAGR) of 4.8% between 2025 and 2033, valued at USD 25.8 Billion in 2025 and is projected to grow by USD 37.6 Billion by 2033 the end of the forecast period.

Key Passenger Car Clutch Market Trends & Insights

The Passenger Car Clutch Market is undergoing significant transformation, driven by a confluence of technological advancements, evolving consumer preferences, and stringent environmental regulations. Key trends shaping this market include the increasing demand for enhanced driving comfort and fuel efficiency, leading to the adoption of sophisticated clutch systems. Lightweighting initiatives in vehicle manufacturing are also influencing clutch material selection and design, aiming to reduce overall vehicle weight and improve performance. Furthermore, the robust growth in the aftermarket segment, fueled by an aging vehicle parc and consumer preference for maintenance over new purchases in certain regions, presents a consistent revenue stream. The emergence of advanced transmission technologies, even as electrification gains momentum, continues to drive innovation in clutch design for hybrid vehicles and certain high-performance internal combustion engine (ICE) models. The market also observes a geographical shift in manufacturing and demand, with Asia Pacific solidifying its position as a dominant hub for both production and consumption.

- Growing demand for advanced and lightweight clutch systems.

- Increasing adoption of high-performance and dual-clutch transmissions in premium segments.

- Significant growth in the aftermarket for replacement and repair.

- Focus on enhanced fuel efficiency and reduced emissions influencing clutch design.

- Rise of hybrid electric vehicles (HEVs) creating demand for specialized clutch components.

AI Impact Analysis on Passenger Car Clutch

Artificial Intelligence (AI) is increasingly influencing the automotive sector, including the Passenger Car Clutch Market, by enhancing design, manufacturing, and operational efficiencies. AI algorithms are being deployed in the early stages of product development to simulate and optimize clutch performance, predict material fatigue, and identify design flaws, thereby reducing prototyping costs and accelerating time-to-market. In manufacturing, AI-powered predictive maintenance systems monitor machinery on production lines, anticipating potential failures and minimizing downtime, which ensures higher output and consistent quality for clutch components. Supply chain management benefits from AI through improved demand forecasting and logistics optimization, leading to more efficient inventory management and reduced lead times for raw materials and finished products. Moreover, AI is instrumental in quality control, utilizing machine vision to detect microscopic defects in clutch components that might be missed by human inspection, thereby elevating product reliability and safety standards. While direct integration into a traditional clutch system is limited, AI's overarching impact on the automotive ecosystem indirectly but significantly shapes the market's efficiency and innovation trajectory.

- Optimized clutch design and material selection through AI-driven simulations.

- Enhanced manufacturing precision and efficiency with AI-powered robotics.

- Predictive maintenance for clutch systems in advanced vehicles.

- Improved supply chain forecasting and management for clutch components.

- AI-assisted quality control and defect detection during production.

Key Takeaways Passenger Car Clutch Market Size & Forecast

- The Passenger Car Clutch Market is projected for steady growth through 2033, driven by aftermarket demand.

- Despite the rise of electric vehicles, traditional and advanced clutch systems for ICE and hybrid vehicles maintain strong market presence.

- Technological advancements focus on lightweight, durable, and fuel-efficient clutch designs.

- Asia Pacific continues to be the dominant region in terms of both production and consumption.

- Dual-clutch transmissions (DCTs) are a key growth segment, particularly in premium and performance vehicles.

- Aftermarket segment is a crucial revenue stream, driven by vehicle longevity and maintenance cycles.

Passenger Car Clutch Market Drivers Analysis

The growth of the Passenger Car Clutch Market is fundamentally propelled by a combination of macroeconomic factors, evolving consumer demands, and advancements within the automotive industry. A primary driver is the continued global production of passenger vehicles, particularly in emerging economies where internal combustion engine (ICE) vehicles, including those with manual transmissions or advanced automatic systems requiring clutch components (like Dual-Clutch Transmissions), still constitute a significant market share. The increasing average age of vehicles on the road further stimulates the aftermarket segment, as clutches are wear-and-tear components requiring periodic replacement. Demand for improved driving experience, including smoother gear shifts and enhanced fuel efficiency, encourages the adoption of more sophisticated clutch technologies. Furthermore, the persistent popularity of manual transmission vehicles in specific regions and segments, valued for their driving engagement and cost-effectiveness, continues to underpin a steady demand for traditional clutch systems. The expansion of the automotive manufacturing base, especially in developing countries, also contributes directly to the demand for original equipment (OE) clutch components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Passenger Vehicle Production Growth | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium Term (2025-2029) |

| Rising Average Age of Vehicles and Aftermarket Demand | +1.5% | North America, Europe, Asia Pacific | Medium to Long Term (2027-2033) |

| Technological Advancements in Clutch Systems (e.g., DCT) | +0.8% | Europe, North America, East Asia | Short to Medium Term (2025-2030) |

| Preference for Manual Transmissions in Developing Regions | +0.7% | India, Southeast Asia, South America | Medium Term (2026-2031) |

| Increase in Automotive Manufacturing Investments | +0.6% | China, India, Mexico, Brazil | Short to Medium Term (2025-2030) |

Passenger Car Clutch Market Restraints Analysis

Despite the inherent drivers, the Passenger Car Clutch Market faces significant restraints that could temper its growth trajectory. The most prominent challenge stems from the accelerating global shift towards electric vehicles (EVs), which typically do not require traditional multi-plate friction clutches found in ICE vehicles for power transmission. While some EVs and hybrids may employ specialized clutch-like mechanisms, the conventional clutch demand diminishes significantly with full electrification. Furthermore, the increasing adoption rate of automatic transmissions (ATs), continuously variable transmissions (CVTs), and dual-clutch transmissions (DCTs) in new vehicle models, particularly in developed markets, reduces the demand for manual clutches. While DCTs incorporate clutch components, their design and replacement cycles differ from traditional manual clutches, impacting the market dynamics. Stringent emission regulations globally are also indirectly pressuring automakers to innovate towards more efficient powertrains, often favoring automatic systems, thus potentially sidelining manual transmissions. Moreover, the long lifespan of modern clutch systems and improved material durability can extend replacement cycles, slowing aftermarket demand in some segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Shift Towards Electric Vehicles (EVs) | -1.8% | Global, particularly Europe, China, North America | Medium to Long Term (2027-2033) |

| Increasing Adoption of Automatic & CVT Transmissions | -1.5% | North America, Europe, Japan, South Korea | Short to Medium Term (2025-2030) |

| Longer Lifespan and Durability of Modern Clutches | -0.5% | Global Aftermarket | Medium Term (2026-2032) |

| Fluctuations in Raw Material Prices | -0.3% | Global Manufacturing | Short Term (2025-2027) |

Passenger Car Clutch Market Opportunities Analysis

Despite existing restraints, significant opportunities are present within the Passenger Car Clutch Market, primarily stemming from evolving vehicle technologies, specific market demands, and geographical shifts. The hybrid electric vehicle (HEV) segment, distinct from fully electric vehicles, presents a niche but growing opportunity as many HEVs still employ clutches or clutch-like mechanisms to manage power flow between the engine, electric motor, and transmission. This creates a demand for specialized and advanced clutch systems. The aftermarket segment continues to be a resilient source of revenue, driven by the sheer volume of existing ICE vehicles and the ongoing need for maintenance and replacement parts over their operational lifespan. Emerging markets in Asia Pacific, Latin America, and Africa, characterized by lower vehicle penetration rates and a strong preference for cost-effective manual transmission vehicles, offer substantial untapped potential for both OEM and aftermarket sales. Furthermore, the increasing demand for high-performance and luxury vehicles, which often feature sophisticated clutch systems like multi-plate wet clutches and advanced DCTs, represents a premium segment opportunity. Innovation in lightweight and durable materials, coupled with enhanced manufacturing processes, also opens avenues for competitive advantage and market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Hybrid Electric Vehicle (HEV) Segment | +1.0% | Global, particularly Europe, Asia Pacific | Medium to Long Term (2027-2033) |

| Robust Aftermarket Demand for Replacements | +1.3% | Global, particularly North America, Europe, Asia Pacific | Long Term (2028-2033) |

| Untapped Potential in Emerging Automotive Markets | +0.9% | India, Southeast Asia, Brazil, Mexico | Short to Medium Term (2025-2030) |

| Increased Demand for High-Performance Clutch Systems | +0.6% | Developed Markets (Europe, North America, Japan) | Medium Term (2026-2031) |

| Technological Innovation in Materials and Design | +0.5% | Global | Short to Medium Term (2025-2030) |

Passenger Car Clutch Market Challenges Impact Analysis

The Passenger Car Clutch Market faces several inherent challenges that can impede its growth and require strategic responses from market participants. The most significant challenge is the rapid pace of electrification in the automotive industry; as electric vehicles become more prevalent, the fundamental need for a traditional clutch system diminishes, presenting a long-term existential threat to a core product category. Automakers are increasingly investing in and producing EVs, shifting focus away from conventional powertrain components. Moreover, the increasing complexity of modern clutch systems, such as dual-clutch transmissions, demands higher manufacturing precision and material quality, leading to increased production costs. This complexity also translates into higher repair and maintenance costs in the aftermarket, potentially influencing consumer choices towards simpler or fully automatic systems. Regulatory pressures, particularly stringent emission norms, indirectly push manufacturers towards more fuel-efficient automatic transmissions, which can reduce the market share of manual transmission vehicles. Supply chain disruptions, often triggered by geopolitical events, trade disputes, or global pandemics, can significantly impact the availability of raw materials and components, leading to production delays and increased costs for clutch manufacturers. Finally, a shortage of skilled labor for manufacturing and servicing advanced clutch systems poses a operational challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerating Transition to Electric Mobility | -2.0% | Global, particularly developed economies | Long Term (2028-2033) |

| High R&D and Manufacturing Costs for Advanced Systems | -0.7% | Global Manufacturing Hubs | Short to Medium Term (2025-2030) |

| Supply Chain Volatility and Raw Material Scarcity | -0.4% | Global | Short Term (2025-2027) |

| Intense Competition from Automatic Transmission Solutions | -1.2% | Developed & rapidly developing markets | Medium Term (2026-2031) |

| Stringent Emission Regulations and Fuel Efficiency Mandates | -0.6% | Europe, North America, China | Short to Medium Term (2025-2030) |

Passenger Car Clutch Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Passenger Car Clutch Market, providing a detailed understanding of its dynamics, trends, and future growth prospects. It encompasses a thorough examination of market size, segmentation, regional insights, and the competitive landscape. The report is designed to equip stakeholders with actionable intelligence, enabling informed strategic decision-making in a rapidly evolving automotive industry. It integrates historical data with future projections, offering a complete picture of market evolution and identifying key drivers, restraints, opportunities, and challenges influencing the sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.8 Billion |

| Market Forecast in 2033 | USD 37.6 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Automotive Transmissions, DriveForce Systems, Precision Clutch Solutions, PowerTrain Innovations, Apex Driveline Components, Dynamic Motion Technologies, Prime Auto Parts, Stellar Clutch Systems, UniDrive Automotive, NextGen Components, Integrated Transmission Group, Velocity Drivetrain, Quantum Clutch Technologies, Summit Auto Solutions, Elite Power Systems, Fusion Mechanical Parts, OmniDrive Components, High Performance Clutch Co., TransGear Solutions, Universal Driveline Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Passenger Car Clutch Market is meticulously segmented across various critical parameters to provide a granular view of its structure and dynamics. These segmentations are crucial for understanding demand patterns, identifying niche markets, and formulating targeted business strategies. Each segment reflects unique product characteristics, application areas, and sales channels that collectively define the market landscape.By Clutch Type: This segment differentiates the market based on the functional design and operating principle of the clutch mechanisms. Understanding the demand for each type is vital for manufacturers and suppliers, as it dictates design, material, and production processes. The dominance of dry friction clutches, especially in manual transmissions, contrasts with the growing complexity and performance orientation of wet clutches found in advanced automatic and dual-clutch transmissions. Electromagnetic and centrifugal clutches represent specialized applications, often linked to specific vehicle designs or performance requirements, offering insights into technological diversification.

- Dry Friction Clutch: Widely used in manual transmissions for its simplicity and cost-effectiveness.

- Wet Clutch: Predominantly found in dual-clutch transmissions and some automatic transmissions, offering superior heat dissipation and smoother engagement.

- Electromagnetic Clutch: Utilizes magnetic force for engagement, often found in specialized or auxiliary applications within the vehicle.

- Centrifugal Clutch: Engages automatically based on engine speed, less common in passenger cars but relevant in specific older models or unique setups.

By Transmission Type: This segmentation highlights the interplay between clutch technology and the overall vehicle powertrain architecture. While manual transmissions directly rely on traditional clutches, the surging popularity of dual-clutch transmissions (DCTs) represents a significant growth area for specialized wet or dry clutch packs. Analyzing this segment reveals the ongoing evolution of transmission systems and their direct impact on clutch component demand, indicating a shift towards more complex and performance-oriented clutch solutions even as manual transmission demand may stabilize or decline in certain markets.

- Manual Transmission: Requires a traditional friction clutch for gear changes, maintaining significant market share in developing economies.

- Dual-Clutch Transmission (DCT): Utilizes two separate clutches for odd and even gears, enabling faster and smoother shifts, driving demand for specific clutch modules.

By Vehicle Type: This segment categorizes clutch demand based on the type of passenger vehicle, reflecting varying design requirements, performance expectations, and price sensitivities. For instance, compact hatchbacks might prioritize cost-effective and robust clutch solutions, while luxury cars and SUVs may incorporate more advanced, high-performance clutch systems to accommodate higher torque outputs and provide a premium driving experience. This distinction is crucial for product development and market positioning, allowing manufacturers to tailor their offerings to specific vehicle segments.

- Hatchback: Typically employs simpler, cost-effective clutch systems due to their compact design and city driving focus.

- Sedan: Features a range of clutch types, from basic manual clutches to more advanced DCTs, depending on the segment (economy to luxury).

- SUV: Often requires robust clutch systems capable of handling higher torque and diverse driving conditions, including off-road capabilities.

- Luxury Cars: Incorporates highly engineered, often wet-type multi-plate clutches or sophisticated DCTs for superior performance, comfort, and durability.

By Sales Channel: This segmentation offers insight into the distribution and consumption patterns of passenger car clutches, differentiating between original equipment installed in new vehicles and replacement parts sold in the aftermarket. The OEM channel is driven by new vehicle production volumes and evolving vehicle designs, while the aftermarket is sustained by the existing vehicle parc and periodic maintenance needs. Both channels exhibit distinct supply chain dynamics, pricing strategies, and customer bases, making this analysis critical for sales and distribution planning.

- Original Equipment Manufacturer (OEM): Sales to vehicle manufacturers for installation in new cars during production.

- Aftermarket: Sales of replacement clutches for maintenance, repair, and upgrades of existing vehicles.

By Material Type: This segment analyzes the market based on the friction material used in clutch discs, which directly impacts performance, durability, and cost. Organic materials are standard for general-purpose applications due to their balance of friction, wear, and NVH (noise, vibration, harshness) characteristics. Ceramic and carbon fiber materials are increasingly used in high-performance or heavy-duty applications, offering superior heat resistance and higher friction coefficients, albeit at a higher cost. Understanding material trends is essential for research and development, influencing product innovation and manufacturing processes.

- Organic: Standard friction material offering good all-around performance and cost-effectiveness.

- Ceramic: Used in high-performance or heavy-duty applications for superior heat resistance and friction.

- Carbon Fiber: Employed in very high-performance and racing applications for extreme heat resistance and lightweight properties.

Regional Highlights

The global Passenger Car Clutch Market exhibits diverse dynamics across different geographical regions, influenced by varying automotive production landscapes, consumer preferences, regulatory frameworks, and economic development levels. Understanding these regional nuances is essential for market players to tailor strategies and capitalize on specific growth opportunities.- Asia Pacific (APAC) stands as the leading and fastest-growing region in the Passenger Car Clutch Market. This dominance is primarily driven by robust automotive production bases in countries like China, India, Japan, and South Korea, which account for a significant portion of global vehicle manufacturing. High population density, increasing disposable incomes, and a strong preference for manual transmission vehicles, particularly in emerging economies like India and Southeast Asia, contribute substantially to both OEM and aftermarket demand. The region also hosts numerous clutch manufacturers and automotive component suppliers, fostering a competitive and innovation-driven environment. Government initiatives supporting local manufacturing and the expanding vehicle parc further cement APAC's critical role in the market.

- Europe represents a mature yet technologically advanced market for passenger car clutches. While manual transmissions retain a considerable share, especially in entry-level and performance segments, the region is a pioneer in the adoption of advanced clutch technologies, including sophisticated dual-clutch transmissions (DCTs). Stringent emission regulations drive innovation towards more efficient and lightweight clutch systems. The strong presence of premium and luxury automotive brands, which often feature high-performance clutch components, also contributes significantly to market value. The aftermarket in Europe is well-established, supported by a large existing fleet of vehicles and a focus on quality replacement parts.

- North America is characterized by a strong preference for automatic transmissions, which traditionally limited the market for conventional manual clutches. However, the increasing popularity of performance vehicles and the growing hybrid vehicle segment are creating niche demands for advanced clutch systems. The region's robust aftermarket is a significant revenue generator, driven by the substantial vehicle parc and consumer inclination towards vehicle maintenance and longevity. Innovation in material science and manufacturing processes also influences the market, with a focus on durability and reduced maintenance.

- Latin America presents a growth market, largely driven by increasing vehicle ownership, expanding automotive manufacturing operations in countries like Brazil and Mexico, and a continued strong demand for manual transmission vehicles due to cost-effectiveness. The aftermarket segment is particularly vital as economic factors often lead to longer vehicle retention periods, necessitating more frequent clutch replacements. The region's market dynamics are closely tied to its economic stability and foreign investment in the automotive sector.

- Middle East and Africa (MEA) is an emerging market with gradual growth in the passenger car clutch sector. The market is influenced by a mix of new vehicle sales and a growing aftermarket. Countries in the Middle East show higher demand for premium vehicles which may include advanced clutch systems, while African markets, with a higher penetration of older vehicles, rely more heavily on aftermarket sales for conventional clutches. Infrastructure development and increasing urbanization are key factors supporting automotive market expansion in select countries.

Top Key Players:

The market research report covers the analysis of key stake holders of the Passenger Car Clutch Market. Some of the leading players profiled in the report include -- Global Automotive Transmissions

- DriveForce Systems

- Precision Clutch Solutions

- PowerTrain Innovations

- Apex Driveline Components

- Dynamic Motion Technologies

- Prime Auto Parts

- Stellar Clutch Systems

- UniDrive Automotive

- NextGen Components

- Integrated Transmission Group

- Velocity Drivetrain

- Quantum Clutch Technologies

- Summit Auto Solutions

- Elite Power Systems

- Fusion Mechanical Parts

- OmniDrive Components

- High Performance Clutch Co.

- TransGear Solutions

- Universal Driveline Group

- Superior Drivetrain Products

Frequently Asked Questions:

What is the projected growth rate of the Passenger Car Clutch Market?

The Passenger Car Clutch Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. This growth is driven by a combination of factors including consistent aftermarket demand, advancements in clutch technology for internal combustion engine (ICE) and hybrid vehicles, and continued vehicle production in emerging economies.How does the rise of electric vehicles (EVs) impact the Passenger Car Clutch Market?

The rapid rise of electric vehicles (EVs) poses a significant long-term restraint on the Passenger Car Clutch Market. EVs typically do not require traditional multi-plate friction clutches for power transmission, leading to a diminished demand for conventional clutch systems as EV adoption increases. However, hybrid electric vehicles (HEVs) may still utilize specialized clutch mechanisms, presenting a niche opportunity.What are the primary drivers for the Passenger Car Clutch Market?

Key drivers for the Passenger Car Clutch Market include the sustained global production of passenger vehicles, particularly in developing regions where manual transmissions remain popular. The increasing average age of vehicles on the road significantly boosts aftermarket demand for clutch replacements. Additionally, technological advancements in clutch systems, such as dual-clutch transmissions (DCTs), contribute to market growth in performance and premium segments.Which regions are key contributors to the Passenger Car Clutch Market growth?

Asia Pacific (APAC) is the leading region in the Passenger Car Clutch Market, driven by high automotive production volumes and strong manual transmission demand in countries like China and India. Europe and North America also remain crucial markets, characterized by demand for advanced clutch systems and robust aftermarket sales, respectively. Latin America and the Middle East & Africa are emerging as growth regions.What technological advancements are shaping the Passenger Car Clutch Market?

Technological advancements shaping the Passenger Car Clutch Market include the development of lightweight and durable materials for clutch components to improve fuel efficiency and performance. There is also a significant trend towards sophisticated clutch systems like multi-plate wet clutches and advanced dual-clutch transmissions (DCTs), designed for smoother engagement, faster shifts, and higher torque capacity in modern vehicles.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted