Car Subscription Service Market

Car Subscription Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702905 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

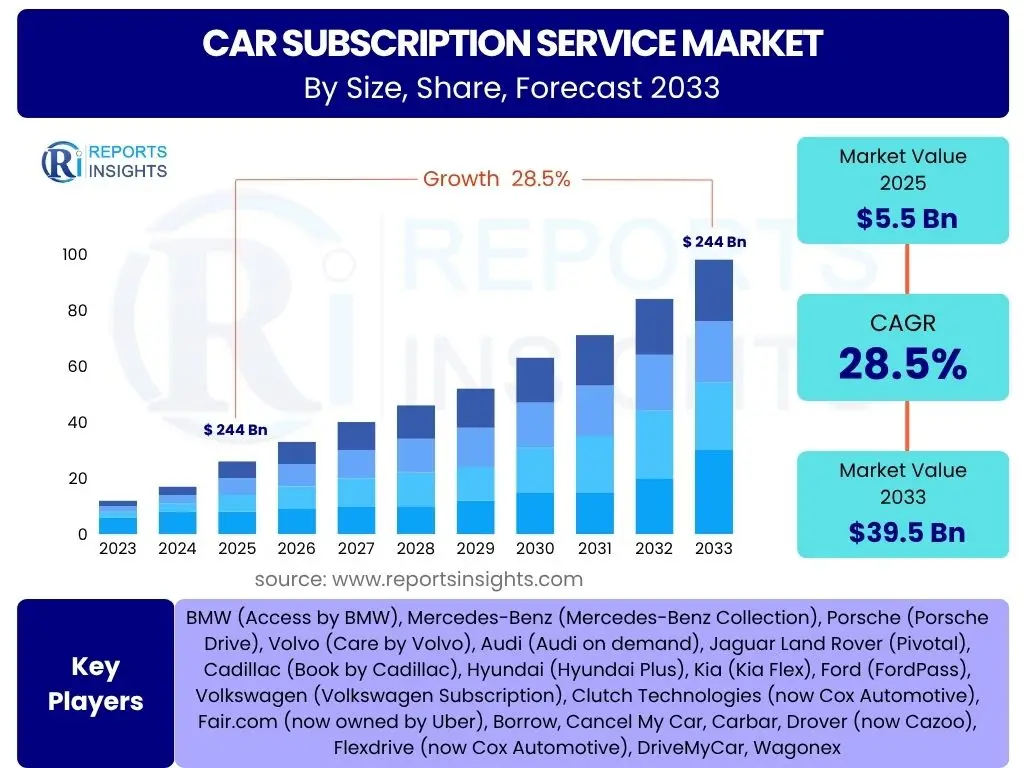

Car Subscription Service Market Size

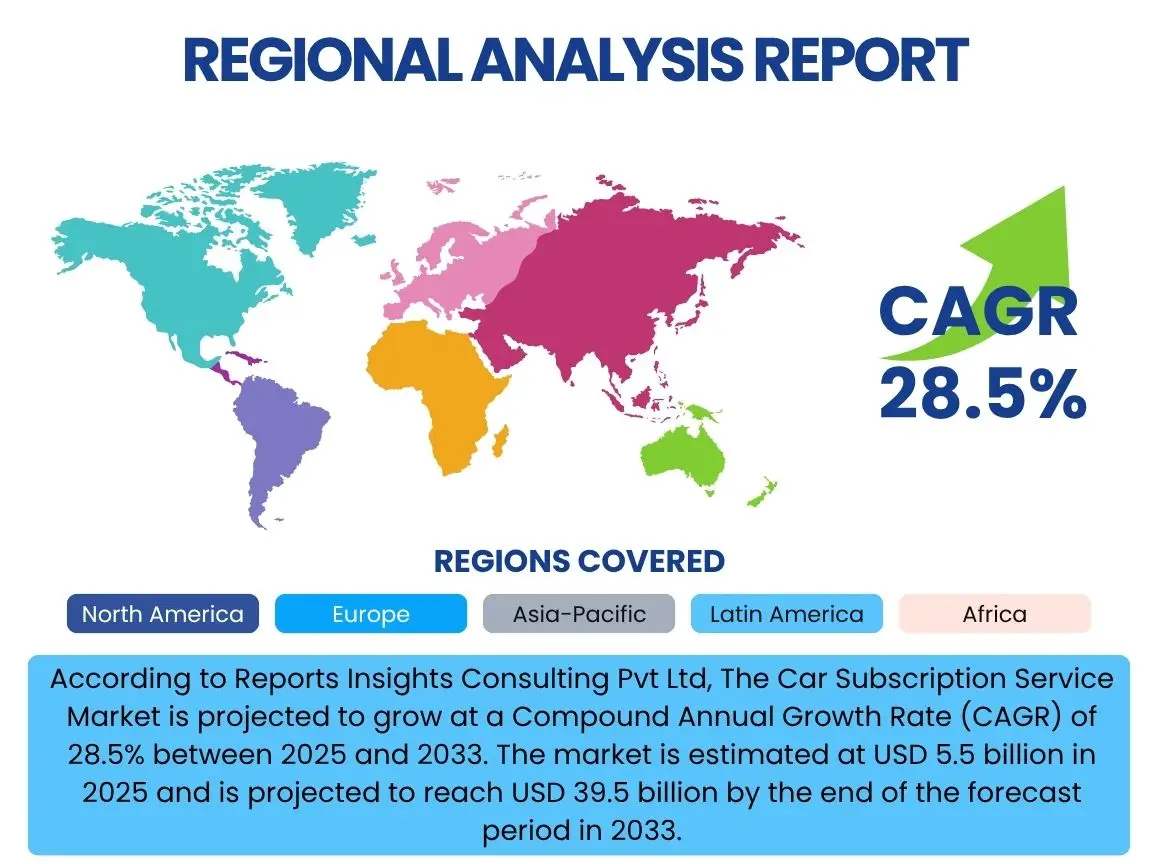

According to Reports Insights Consulting Pvt Ltd, The Car Subscription Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 5.5 billion in 2025 and is projected to reach USD 39.5 billion by the end of the forecast period in 2033.

Key Car Subscription Service Market Trends & Insights

User queries regarding the Car Subscription Service market frequently center on evolving consumer preferences for flexibility over ownership, the impact of technological advancements, and the expansion of service providers. The market is witnessing a significant shift towards on-demand mobility solutions, driven by urbanization and a growing emphasis on asset-light lifestyles. This paradigm shift is encouraging traditional automotive manufacturers and new entrants alike to innovate their offerings, moving beyond conventional sales models to embrace subscription-based services that cater to diverse customer needs for convenience and variety. The increasing availability of electric vehicles (EVs) within subscription fleets is also a notable trend, reflecting environmental consciousness and infrastructure developments.

Furthermore, there is a clear trend towards personalized subscription plans, allowing customers to tailor vehicle types, subscription durations, and included services such as maintenance, insurance, and roadside assistance. Data analytics and artificial intelligence are playing a crucial role in enabling these customized offerings and optimizing fleet management. The integration of digital platforms for seamless booking, vehicle swap, and payment processing is enhancing the user experience, making car subscription services an increasingly attractive alternative to traditional car ownership or long-term leasing. The market is also observing a consolidation of services, with major players acquiring smaller providers or forming strategic partnerships to expand their geographical reach and service portfolios, aiming to capture a larger share of the emerging mobility landscape.

- Shift from ownership to usership: Growing preference for flexible access over fixed asset ownership.

- Personalization of subscription plans: Tailored offerings for duration, vehicle type, and services.

- Integration of electric vehicles (EVs): Increasing availability of EVs in subscription fleets.

- Digital-first customer experience: Seamless online booking, management, and vehicle swaps.

- Rise of multimodal transportation integration: Car subscriptions complementing public transport and ride-sharing.

- Expansion of corporate subscription models: Businesses seeking flexible fleet solutions.

- Focus on sustainability and circular economy principles: Encouraging longer vehicle lifecycles and shared use.

AI Impact Analysis on Car Subscription Service

User inquiries about AI's impact on car subscription services often explore how artificial intelligence can enhance personalization, optimize fleet operations, and improve the overall customer experience. There is significant interest in AI's potential to predict vehicle demand, manage inventory efficiently, and automate critical processes from booking to maintenance scheduling. Users are keen to understand how AI-driven insights can lead to more competitive pricing models and more tailored vehicle recommendations, moving beyond static offerings to dynamic, responsive services.

AI's influence extends to predictive maintenance, where algorithms analyze vehicle data to anticipate service needs, thereby reducing downtime and improving vehicle availability for subscribers. Furthermore, AI-powered chatbots and virtual assistants are streamlining customer support, providing instant responses to inquiries and facilitating smoother interactions. The technology is also instrumental in fraud detection, optimizing insurance risk assessment, and refining user profiling for marketing personalized offers. As autonomous driving technologies advance, AI will further transform the subscription model by enabling self-repositioning vehicles, potentially reducing operational costs and enhancing convenience for users.

- Predictive demand forecasting: AI algorithms optimize fleet size and vehicle allocation based on user patterns.

- Personalized subscription recommendations: AI analyzes user data to suggest ideal vehicle types and plans.

- Dynamic pricing optimization: AI adjusts pricing based on real-time demand, availability, and market conditions.

- Enhanced customer support: AI-powered chatbots and virtual assistants provide instant assistance.

- Predictive maintenance: AI analyzes vehicle data to anticipate and schedule maintenance, reducing downtime.

- Automated vehicle logistics: AI optimizes vehicle delivery, pickup, and repositioning.

- Fraud detection and risk assessment: AI enhances security and streamlines insurance processes.

Key Takeaways Car Subscription Service Market Size & Forecast

Common user questions regarding key takeaways from the Car Subscription Service market size and forecast often revolve around its long-term viability, primary growth drivers, and potential disruptive forces. The most significant takeaway is the market's robust growth trajectory, demonstrating a fundamental shift in consumer behavior away from traditional ownership towards flexible access to mobility. This trend is fueled by urbanization, evolving lifestyle preferences for convenience, and a heightened awareness of the financial and environmental benefits associated with subscription models. The market is not merely a niche offering but a substantial, growing segment within the broader mobility sector, poised for significant expansion over the next decade.

Another crucial insight is the increasing diversification of service providers, encompassing not only automotive OEMs but also dedicated subscription platforms, rental companies, and even dealerships. This competitive landscape is fostering innovation and pushing service customization to new levels, making car subscriptions more appealing to a wider demographic. The forecast indicates that despite existing challenges like regulatory variations and capital intensity, the underlying market dynamics strongly support sustained expansion. As technological integration, particularly AI and telematics, further refines operational efficiencies and enhances user experience, the car subscription service market is expected to solidify its position as a key component of future urban and personal mobility ecosystems.

- High growth potential: Market projected for substantial expansion, reaching USD 39.5 billion by 2033.

- Consumer shift: Strong preference for flexible mobility solutions over traditional vehicle ownership.

- Diversifying ecosystem: OEMs, third-party providers, and rental companies increasingly adopting subscription models.

- Technological integration: AI and telematics are key enablers for operational efficiency and customer experience.

- Sustainability driver: Growing adoption of EVs within subscription fleets supports eco-friendly mobility.

- Urbanization impact: Increasing demand for convenient, asset-light transportation in metropolitan areas.

- Strategic partnerships: Collaborations between market players to expand reach and service offerings.

Car Subscription Service Market Drivers Analysis

The Car Subscription Service market is significantly propelled by a confluence of socio-economic shifts and technological advancements that redefine consumer expectations for personal mobility. A primary driver is the escalating preference for flexible and convenient access to vehicles without the burdens of ownership, such as depreciation, maintenance, and insurance. This shift is particularly prevalent among younger demographics and urban dwellers who seek agile solutions for their diverse transportation needs. The COVID-19 pandemic further accelerated this trend by highlighting the need for personal mobility options that avoid public transport and offer adaptable terms.

Additionally, the burgeoning adoption of electric vehicles (EVs) is acting as a substantial driver. Subscription services offer a low-commitment entry point for consumers hesitant about the upfront cost or long-term viability of EV ownership, allowing them to experience electric mobility without significant capital outlay. Furthermore, advancements in digital platforms, telematics, and data analytics empower service providers to offer highly personalized, efficient, and user-friendly services, ranging from seamless booking to predictive maintenance, thereby enhancing the overall value proposition for subscribers. These factors collectively contribute to the robust growth observed in the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Consumer Preference for Flexible Mobility | +7.5% | Global, particularly North America, Europe, Asia Pacific | Short to Medium-term (2025-2030) |

| Increasing Adoption of Electric Vehicles (EVs) | +6.0% | Europe, North America, China | Medium to Long-term (2026-2033) |

| High Costs and Hassles of Car Ownership | +5.0% | Urban Centers Globally | Short to Medium-term (2025-2029) |

| Advancements in Digital Platforms and Telematics | +4.5% | Global | Continuous (2025-2033) |

Car Subscription Service Market Restraints Analysis

Despite its significant growth potential, the Car Subscription Service market faces several notable restraints that could temper its expansion. One primary challenge is the capital-intensive nature of fleet acquisition and maintenance. Service providers require substantial upfront investments to build and diversify their vehicle fleets, which can be a barrier to entry for new players and strain the financial models of existing ones, particularly in a volatile economic environment where interest rates and vehicle prices can fluctuate significantly. This financial hurdle often limits the scale and variety of offerings, especially for smaller providers.

Another significant restraint is the varying regulatory landscape across different regions and countries. The legal and tax frameworks surrounding car subscription services are still evolving, leading to inconsistencies in licensing, insurance requirements, and taxation. This lack of standardization can create operational complexities and compliance risks for providers seeking to expand internationally, adding layers of administrative burden and potentially increasing operational costs. Furthermore, consumer awareness and trust, while growing, are still developing in some markets, as many consumers remain accustomed to traditional car ownership or leasing models, requiring significant marketing and education efforts to shift perceptions and build confidence in subscription services.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Fleet Acquisition | -3.0% | Global | Medium to Long-term (2025-2033) |

| Complex and Evolving Regulatory Landscape | -2.5% | Europe, Asia Pacific, Emerging Markets | Continuous (2025-2033) |

| Limited Consumer Awareness and Trust in Emerging Markets | -2.0% | Latin America, MEA, parts of APAC | Short to Medium-term (2025-2029) |

| Potential for High Operating Costs (Maintenance, Insurance) | -1.5% | Global | Continuous (2025-2033) |

Car Subscription Service Market Opportunities Analysis

The Car Subscription Service market presents numerous opportunities for innovation and growth, driven by untapped market segments and technological integration. A significant opportunity lies in expanding into corporate fleets and business-to-business (B2B) solutions. Companies are increasingly seeking flexible, cost-effective alternatives to traditional fleet ownership, enabling them to scale vehicle access up or down based on project needs or employee requirements without the administrative overhead of procurement and maintenance. This segment represents a substantial, largely underdeveloped market that can drive significant revenue growth for providers offering tailored corporate packages.

Furthermore, the rapid advancements in autonomous driving technology and vehicle connectivity open new avenues for subscription models. As autonomous vehicles become commercially viable, car subscription services could offer a seamless, driverless mobility experience, reducing operational costs related to human drivers and expanding accessibility. This futuristic integration could revolutionize urban transportation, making car subscriptions an even more compelling alternative. Additionally, geographical expansion into emerging economies, where car ownership rates are lower but demand for personal mobility is rising, coupled with strategic partnerships with automotive OEMs, dealerships, and mobility solution providers, will unlock new customer bases and optimize vehicle supply chains, fueling sustained market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Corporate Fleet Solutions | +5.5% | North America, Europe, Developed Asia Pacific | Medium to Long-term (2026-2033) |

| Integration of Autonomous Driving Technology | +4.0% | Global (initially North America, Europe, China) | Long-term (2028-2033) |

| Untapped Markets in Emerging Economies | +3.5% | Latin America, MEA, Southeast Asia | Medium to Long-term (2027-2033) |

| Strategic Partnerships with OEMs and Mobility Providers | +3.0% | Global | Short to Medium-term (2025-2030) |

Car Subscription Service Market Challenges Impact Analysis

The Car Subscription Service market encounters several significant challenges that could impede its trajectory. One major hurdle is intense competition from established alternatives such as traditional car rental services, car-sharing platforms, and long-term leasing options. These conventional models often offer competitive pricing or well-established infrastructure, requiring car subscription providers to differentiate themselves significantly through value-added services, vehicle variety, or superior flexibility. This competitive pressure can lead to pricing wars and reduced profit margins, making it difficult for new entrants to gain traction and for existing players to maintain profitability.

Another critical challenge is managing fleet utilization and inventory effectively. Underutilization of vehicles leads to significant capital drain, while overutilization can lead to vehicle unavailability and customer dissatisfaction. Balancing supply and demand, especially during peak seasons or for specific vehicle types, requires sophisticated predictive analytics and agile fleet management systems. Furthermore, the complexities associated with vehicle lifecycle management, including routine maintenance, repairs, depreciation, and remarketing of used vehicles, pose substantial operational challenges. These factors demand robust logistical capabilities and financial planning to ensure long-term viability and scalability in the evolving mobility landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Traditional Mobility Services | -3.0% | Global | Continuous (2025-2033) |

| Optimizing Fleet Utilization and Inventory Management | -2.5% | Global | Continuous (2025-2033) |

| High Customer Acquisition and Retention Costs | -2.0% | North America, Europe | Short to Medium-term (2025-2029) |

| Managing Vehicle Depreciation and Residual Value | -1.5% | Global | Continuous (2025-2033) |

Car Subscription Service Market - Updated Report Scope

This report provides an in-depth analysis of the global Car Subscription Service market, covering market size, growth drivers, restraints, opportunities, and challenges. It includes detailed segmentation by vehicle type, subscription model, end-user, service provider, and regional analysis. The scope encompasses current market dynamics, emerging trends, the impact of artificial intelligence, and a comprehensive competitive landscape, offering stakeholders actionable insights for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.5 billion |

| Market Forecast in 2033 | USD 39.5 billion |

| Growth Rate | 28.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BMW (Access by BMW), Mercedes-Benz (Mercedes-Benz Collection), Porsche (Porsche Drive), Volvo (Care by Volvo), Audi (Audi on demand), Jaguar Land Rover (Pivotal), Cadillac (Book by Cadillac), Hyundai (Hyundai Plus), Kia (Kia Flex), Ford (FordPass), Volkswagen (Volkswagen Subscription), Clutch Technologies (now Cox Automotive), Fair.com (now owned by Uber), Borrow, Cancel My Car, Carbar, Drover (now Cazoo), Flexdrive (now Cox Automotive), DriveMyCar, Wagonex |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Car Subscription Service market is segmented to provide a granular understanding of its diverse components and dynamics. This comprehensive segmentation allows for a detailed analysis of market performance across different vehicle categories, subscription durations, end-user demographics, and operational models, thereby pinpointing areas of high growth and specific market demands. Understanding these segments is crucial for strategic positioning and product development within the evolving mobility landscape.

The segmentation by vehicle type reflects consumer preferences for specific car classes, from economical options for urban commuting to luxury vehicles for premium experiences, and a growing demand for electric vehicles. Subscription models are differentiated by duration and flexibility, catering to both short-term needs and longer-term commitments. End-user segmentation highlights the distinction between individual consumers seeking personal mobility solutions and corporate entities looking for flexible fleet management. Lastly, segmenting by service provider offers insights into the competitive landscape, distinguishing between offerings from original equipment manufacturers (OEMs), independent third-party providers, and dealership-backed services.

- By Vehicle Type:

- Economy Vehicles

- Mid-Range Vehicles

- Luxury Vehicles

- Electric Vehicles (EVs)

- SUVs

- Others (e.g., Vans, Sports Cars)

- By Subscription Model:

- Short-term Subscriptions (e.g., daily, weekly, monthly)

- Long-term Subscriptions (e.g., 6 months, 12 months, 24 months)

- Flexible Subscriptions (e.g., month-to-month, pause/swap options)

- Fixed Subscriptions (e.g., defined duration with limited flexibility)

- By End User:

- Individual Consumers

- Corporate / Business Users

- By Service Provider:

- OEM-owned Services

- Third-Party Providers / Independent Platforms

- Dealership-backed Services

Regional Highlights

- North America: The largest market due to high disposable incomes, early adoption of subscription models, and a strong presence of key players and technological innovators. Urbanization and the rising cost of car ownership are primary drivers.

- Europe: A rapidly growing market, driven by increasing environmental awareness, stringent emission regulations promoting EVs, and a strong preference for flexible mobility solutions, particularly in Western European countries like Germany, the UK, and France.

- Asia Pacific (APAC): Emerging as a high-growth region, propelled by increasing urbanization, a burgeoning middle class, and government initiatives promoting electric vehicles. China, Japan, and South Korea are key markets, showing significant potential for both individual and corporate subscriptions.

- Latin America: An emerging market with significant growth potential, characterized by rising disposable incomes, growing demand for personal mobility, and the increasing adoption of digital services. Brazil and Mexico are leading the charge.

- Middle East and Africa (MEA): Gradually gaining traction, particularly in the GCC countries, driven by a young population, digital infrastructure development, and a desire for premium and flexible mobility options.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Car Subscription Service Market.- BMW (Access by BMW)

- Mercedes-Benz (Mercedes-Benz Collection)

- Porsche (Porsche Drive)

- Volvo (Care by Volvo)

- Audi (Audi on demand)

- Jaguar Land Rover (Pivotal)

- Cadillac (Book by Cadillac)

- Hyundai (Hyundai Plus)

- Kia (Kia Flex)

- Ford (FordPass)

- Volkswagen (Volkswagen Subscription)

- Clutch Technologies (now Cox Automotive)

- Fair.com (now owned by Uber)

- Borrow

- Cancel My Car

- Carbar

- Drover (now Cazoo)

- Flexdrive (now Cox Automotive)

- DriveMyCar

- Wagonex

Frequently Asked Questions

Analyze common user questions about the Car Subscription Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a car subscription service?

A car subscription service allows users to access a vehicle for a flexible period, typically month-to-month, with an all-inclusive fee covering the car, insurance, maintenance, and roadside assistance. It offers an alternative to traditional ownership or long-term leasing, providing greater flexibility and convenience.

How do car subscription costs compare to traditional car ownership?

While the monthly subscription fee may seem higher than a car payment, it often covers all associated costs like insurance, maintenance, and depreciation, which are separate expenses in traditional ownership. For many, the predictable all-inclusive fee and lack of long-term commitment make subscriptions a more financially transparent and flexible option.

What are the primary benefits of using a car subscription service?

Key benefits include enhanced flexibility (ability to swap cars or cancel anytime), convenience (all-inclusive pricing, no dealership visits for maintenance), no long-term commitment, and access to a variety of vehicles. It eliminates the hassles of depreciation, resale, and unexpected repair costs associated with ownership.

Are electric vehicles (EVs) available through car subscription services?

Yes, many car subscription services are increasingly incorporating electric vehicles into their fleets. This offers consumers a convenient way to experience EV technology without the significant upfront investment or long-term commitment, promoting sustainable mobility and addressing range anxiety concerns.

How does AI impact the car subscription market?

AI enhances car subscription services by optimizing fleet management, predicting vehicle demand, personalizing subscription plans, and streamlining customer service through chatbots. It also enables predictive maintenance, improving vehicle uptime and overall operational efficiency for providers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted