Outsourced Semiconductor Assembly and Test Market

Outsourced Semiconductor Assembly and Test Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700868 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

Outsourced Semiconductor Assembly and Test Market Size

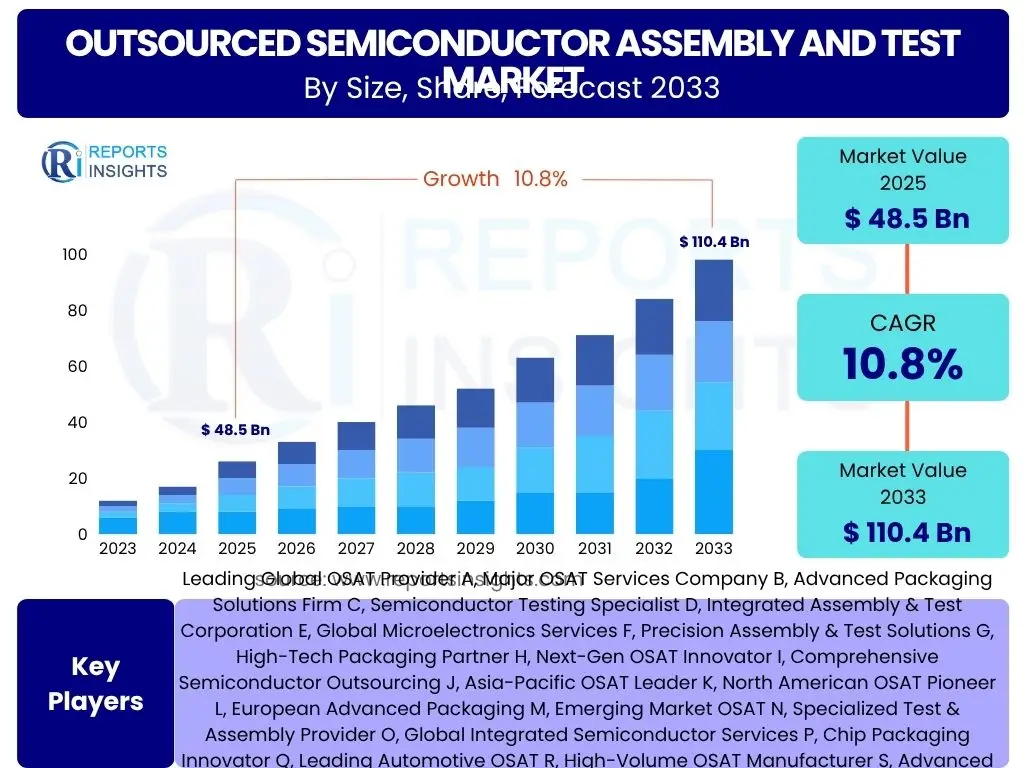

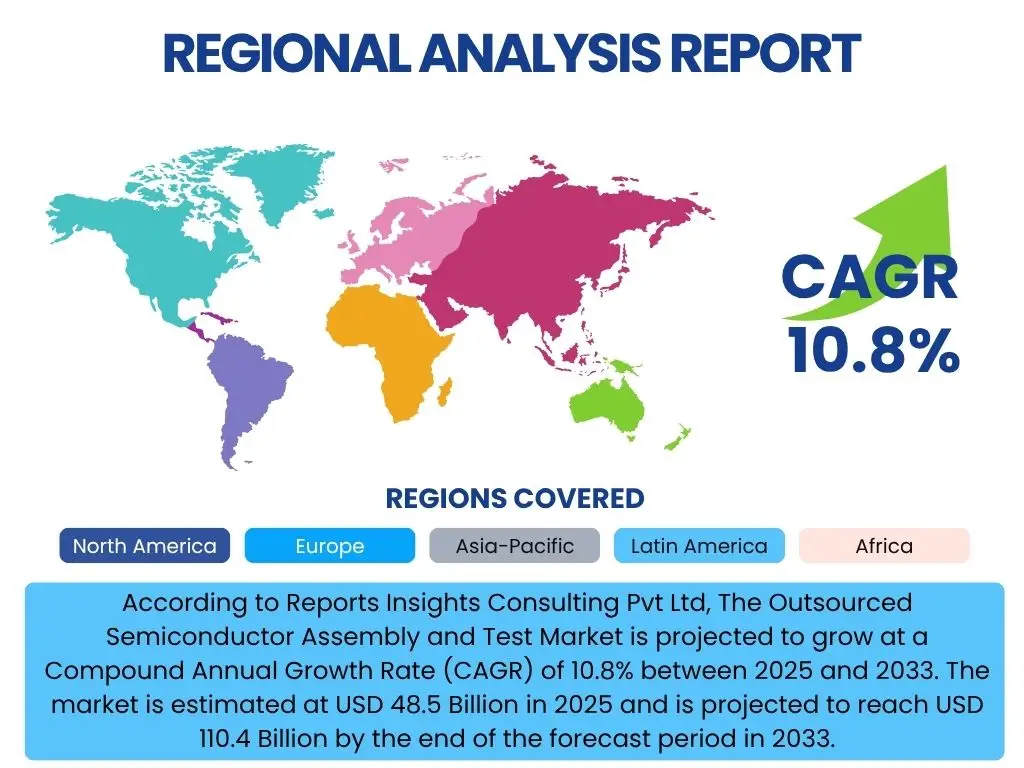

According to Reports Insights Consulting Pvt Ltd, The Outsourced Semiconductor Assembly and Test Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 48.5 Billion in 2025 and is projected to reach USD 110.4 Billion by the end of the forecast period in 2033.

The growth trajectory of the Outsourced Semiconductor Assembly and Test (OSAT) market is primarily driven by the increasing complexity of semiconductor devices, the escalating costs associated with in-house manufacturing, and the rapid expansion of end-use industries like consumer electronics, automotive, and artificial intelligence. Semiconductor companies, particularly fabless firms and integrated device manufacturers (IDMs), are increasingly relying on OSAT providers to manage the post-fabrication processes, including assembly, packaging, and final testing. This outsourcing trend allows companies to focus their resources on research, design, and intellectual property development, while leveraging the specialized expertise and capital-intensive infrastructure of OSAT providers.

The market's robust expansion is further fueled by the demand for advanced packaging technologies, which are critical for achieving higher performance, greater functionality, and reduced form factors in modern electronic devices. Innovations such as fan-out wafer-level packaging (FO-WLP), 2.5D and 3D integration, and system-in-package (SiP) solutions are becoming mainstream, requiring significant investment in sophisticated equipment and specialized process knowledge. OSAT companies are at the forefront of these technological advancements, offering scalable and cost-effective solutions that are difficult for individual semiconductor firms to replicate independently. The strategic importance of OSAT providers in the global semiconductor supply chain is thus continuously intensifying, supporting the proliferation of advanced electronics across diverse sectors.

Key Outsourced Semiconductor Assembly and Test Market Trends & Insights

Common inquiries from users about the Outsourced Semiconductor Assembly and Test (OSAT) market trends and insights frequently revolve around the adoption of new technologies, shifts in manufacturing strategies, and the impact of geopolitical factors on the supply chain. Users are keen to understand how advanced packaging is transforming the industry, the increasing emphasis on supply chain diversification and resilience, and the burgeoning demand from high-growth application areas. There is significant interest in the shift towards turnkey solutions, where OSAT providers offer a comprehensive suite of services from wafer processing to final product testing, streamlining the manufacturing process for their clients. Furthermore, the role of sustainability and environmental considerations in OSAT operations is also a growing area of concern for stakeholders seeking to understand responsible manufacturing practices.

- Advanced Packaging Adoption: Rapid proliferation of advanced packaging technologies such as 3D IC, 2.5D, fan-out wafer-level packaging (FO-WLP), and chiplet integration to meet performance, power, and form factor demands across various applications.

- Supply Chain Diversification and Regionalization: Increased focus on diversifying manufacturing footprints beyond traditional hubs, driven by geopolitical considerations and the need for more resilient, localized supply chains.

- Growth in High-Performance Computing (HPC) and AI Applications: Surging demand for OSAT services from data centers, AI accelerators, and high-performance computing segments requiring specialized packaging and testing for complex chips.

- Automotive Semiconductor Growth: Significant expansion in automotive electronics, including ADAS, infotainment, and electrification, driving the need for robust, high-reliability packaging and testing solutions.

- IoT and 5G Connectivity: Continued rise in IoT device adoption and 5G network deployment leading to demand for miniaturized, power-efficient, and cost-effective packaging solutions.

- Increased Automation and Digitalization: Integration of robotics, AI, and advanced analytics in OSAT facilities to improve efficiency, yield, and quality control throughout assembly and testing processes.

- Turnkey Solutions and Collaboration: Growing preference for OSAT providers offering comprehensive, integrated solutions from design services to final test and logistics, fostering deeper partnerships between OSAT firms and their clients.

AI Impact Analysis on Outsourced Semiconductor Assembly and Test

Users frequently inquire about the transformative impact of Artificial Intelligence (AI) on the Outsourced Semiconductor Assembly and Test (OSAT) market, focusing on how AI is revolutionizing manufacturing processes, enhancing operational efficiency, and addressing the increasing complexity of advanced packaging and testing. Key themes include AI's role in predictive maintenance, improving yield rates through data analytics, automating quality inspection, and optimizing production workflows. There is also a strong interest in how AI-driven design tools influence the requirements for packaging and testing of AI-specific chips, leading to demands for new service capabilities from OSAT providers. The overarching expectation is that AI will drive significant advancements in precision, speed, and cost-effectiveness within the OSAT domain, while also presenting new opportunities for specialized testing of AI hardware.

- Enhanced Automation and Robotics: AI drives advanced robotics in OSAT, enabling precise handling, assembly, and testing of highly complex and miniaturized components, reducing human error and increasing throughput.

- Predictive Maintenance: AI algorithms analyze equipment sensor data to predict potential failures, enabling proactive maintenance, minimizing downtime, and optimizing machinery utilization in OSAT facilities.

- Yield Optimization: AI-driven data analytics helps identify patterns and root causes of defects during assembly and test, leading to process adjustments that significantly improve manufacturing yield rates and reduce scrap.

- Automated Optical Inspection (AOI) and Quality Control: AI-powered vision systems enhance the accuracy and speed of quality inspections, detecting microscopic flaws and ensuring consistent product quality more efficiently than traditional methods.

- Test Program Optimization: AI algorithms can optimize test sequences and parameters, reducing overall test time while maintaining or improving test coverage, thereby lowering operational costs.

- Supply Chain Optimization: AI improves inventory management, logistics, and demand forecasting for OSAT operations, contributing to a more resilient and responsive supply chain.

- Design for Testability (DFT) and Manufacturability (DFM) for AI Chips: As AI chips become more complex, AI tools assist in designing for easier and more efficient testing and assembly, impacting OSAT service requirements.

Key Takeaways Outsourced Semiconductor Assembly and Test Market Size & Forecast

Common user questions regarding the key takeaways from the Outsourced Semiconductor Assembly and Test (OSAT) market size and forecast often highlight the need for concise, actionable insights into the market's future. Users are particularly interested in understanding the primary drivers of growth, the most impactful technological shifts, and the critical success factors for stakeholders. The analysis indicates a robust growth trajectory for the OSAT market, underpinned by relentless innovation in advanced packaging, the increasing adoption of chiplet architectures, and the pervasive demand for semiconductors across burgeoning end-use applications like artificial intelligence, 5G, and automotive electronics. The outsourcing model's inherent benefits, such as cost efficiency, access to specialized expertise, and scalability, will continue to drive market expansion, positioning OSAT providers as indispensable partners in the global semiconductor ecosystem.

- Consistent Robust Growth: The OSAT market is projected for significant expansion through 2033, driven by increasing semiconductor demand and the strategic shift towards outsourcing.

- Advanced Packaging as a Primary Catalyst: Innovations in 2.5D/3D integration, fan-out, and chiplet technologies are fundamental growth drivers, enabling higher performance and smaller form factors.

- Diversified End-Use Demand: Strong growth is expected from emerging applications such as AI, high-performance computing, automotive electronics, and IoT devices, requiring specialized OSAT services.

- Supply Chain Resilience Focus: Geopolitical factors and past disruptions are leading semiconductor companies to prioritize diversified and regionalized OSAT partnerships to enhance supply chain robustness.

- Technological Investment Criticality: OSAT providers must continually invest in cutting-edge equipment, automation, and R&D to meet evolving customer demands and maintain competitive advantage.

- Strategic Importance of OSAT: OSAT firms are becoming increasingly integral to the entire semiconductor value chain, offering essential services that enable rapid innovation and market entry for chip designers.

Outsourced Semiconductor Assembly and Test Market Drivers Analysis

The Outsourced Semiconductor Assembly and Test (OSAT) market is significantly propelled by several dynamic factors that reinforce its growth trajectory. The ever-increasing complexity of semiconductor designs and the relentless drive for miniaturization necessitate advanced packaging solutions that often require specialized expertise and capital-intensive equipment, which OSAT providers offer efficiently. Furthermore, the fabless business model, which separates chip design from manufacturing, continues to gain prominence, directly increasing the demand for outsourced assembly and test services. This model allows semiconductor companies to focus on their core competencies of design and intellectual property, offloading the expensive post-fabrication processes to dedicated OSAT firms.

Another pivotal driver is the proliferation of high-growth application sectors such as artificial intelligence, 5G connectivity, automotive electronics, and the Internet of Things (IoT). Each of these sectors demands unique and often highly sophisticated packaging and testing solutions to meet stringent performance, reliability, and power efficiency requirements. OSAT companies are instrumental in enabling these innovations by providing scalable and technologically advanced services that facilitate faster time-to-market for new semiconductor products. The economic advantages of outsourcing, including reduced capital expenditure for chip designers and access to global manufacturing flexibility, further solidify the market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Chip Complexity & Miniaturization | +1.5% | Global, particularly APAC (Taiwan, South Korea) | Long-term (2025-2033) |

| Proliferation of Fabless Business Model | +1.2% | Global, strong in North America, Europe, APAC | Mid-to-Long-term (2025-2033) |

| Growth in AI, 5G, IoT, Automotive Electronics | +1.8% | Global, high demand from China, US, EU, Japan | Short-to-Long-term (2025-2033) |

| Demand for Advanced Packaging Technologies | +1.7% | Global, concentrated in APAC (Taiwan, South Korea, China) | Long-term (2025-2033) |

| Cost Efficiency & Reduced Capital Expenditure for Clients | +1.0% | Global | Mid-term (2025-2029) |

Outsourced Semiconductor Assembly and Test Market Restraints Analysis

Despite its robust growth, the Outsourced Semiconductor Assembly and Test (OSAT) market faces several significant restraints that could temper its expansion. One primary concern is the substantial capital expenditure required for advanced packaging and testing equipment. OSAT providers must continuously invest heavily in state-of-the-art machinery and research and development to keep pace with rapid technological advancements in semiconductor manufacturing. This high investment barrier can limit the entry of new players and put financial strain on existing ones, especially during periods of market downturns or cyclical fluctuations inherent in the semiconductor industry.

Geopolitical tensions and trade disputes also pose a notable restraint. The globalized nature of the semiconductor supply chain makes it vulnerable to political instabilities, trade barriers, and export controls, which can disrupt material flows, increase operational costs, and force companies to reconsider their global manufacturing strategies. Furthermore, the cyclical nature of the semiconductor industry, characterized by boom and bust periods, leads to fluctuations in demand for OSAT services, making long-term capacity planning challenging and introducing revenue volatility. The increasing complexity of intellectual property protection in a highly outsourced environment also represents a growing concern for both OSAT providers and their clients, demanding robust security protocols and legal frameworks.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure & Investment Costs | -0.8% | Global | Long-term (2025-2033) |

| Geopolitical Tensions & Trade Protectionism | -1.0% | Global, particularly US-China, EU-Asia | Short-to-Mid-term (2025-2029) |

| Cyclical Nature of Semiconductor Industry | -0.7% | Global | Short-to-Mid-term (2025-2029) |

| Skilled Labor Shortage & Talent Retention | -0.5% | Global, acute in developed regions | Long-term (2025-2033) |

| Intellectual Property (IP) Protection Concerns | -0.4% | Global | Mid-term (2025-2029) |

Outsourced Semiconductor Assembly and Test Market Opportunities Analysis

The Outsourced Semiconductor Assembly and Test (OSAT) market is ripe with opportunities driven by technological advancements and evolving industry dynamics. The continuous innovation in advanced packaging technologies, such as heterogeneous integration, chiplets, and novel 3D stacking solutions, presents a significant growth avenue. As semiconductors become more complex and specialized, in-house packaging and testing become prohibitively expensive for many firms, pushing them towards OSAT providers who possess the necessary expertise and infrastructure. This trend creates avenues for OSAT companies to develop and offer highly specialized, value-added services that command premium pricing.

Moreover, the burgeoning demand from emerging technologies like artificial intelligence (AI), machine learning (ML), high-performance computing (HPC), and next-generation automotive electronics offers substantial opportunities. These applications require increasingly sophisticated and reliable packaging and testing, often pushing the boundaries of current capabilities. OSAT providers capable of meeting these stringent requirements through continuous investment in R&D and advanced equipment will secure a competitive advantage. The trend towards regional supply chain diversification also creates opportunities for OSAT companies to establish or expand operations in strategically important geographies, mitigating geopolitical risks and offering localized support to clients seeking more resilient manufacturing ecosystems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Packaging Technologies | +1.8% | Global, particularly APAC (Taiwan, South Korea, China) | Long-term (2025-2033) |

| Growth in AI, ML, & HPC Applications | +1.7% | Global, strong in North America, China, Europe | Long-term (2025-2033) |

| Expansion into New & Emerging Markets | +1.0% | Southeast Asia, India, Latin America | Mid-to-Long-term (2025-2033) |

| Regionalization & Diversification of Supply Chains | +1.2% | North America, Europe, Japan, India, Southeast Asia | Mid-term (2025-2029) |

| Integration of Smart Manufacturing & Industry 4.0 | +0.9% | Global | Mid-to-Long-term (2025-2033) |

Outsourced Semiconductor Assembly and Test Market Challenges Impact Analysis

The Outsourced Semiconductor Assembly and Test (OSAT) market faces significant challenges that could impede its growth and operational efficiency. One primary challenge is the relentless pace of technological change and the associated demand for continuous innovation. OSAT providers must invest heavily and rapidly in new equipment and processes to keep up with the evolving requirements for advanced packaging and high-speed testing, which can strain financial resources and intellectual capital. Furthermore, the intensifying global competition among OSAT firms leads to pricing pressures and necessitates constant efforts to improve efficiency and reduce costs, often at the expense of profit margins.

Another critical challenge stems from the complexities of managing global supply chains and geopolitical uncertainties. Disruptions due to natural disasters, pandemics, or trade conflicts can severely impact the availability of raw materials, components, and logistics, leading to production delays and increased costs. Moreover, maintaining stringent quality control and ensuring intellectual property security across a diverse global client base and complex manufacturing processes poses a significant operational hurdle. The increasing environmental regulations and sustainability demands also present challenges, requiring OSAT providers to adopt greener manufacturing practices and reduce their carbon footprint, which often entails additional investments and operational adjustments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence & High R&D Costs | -0.9% | Global | Long-term (2025-2033) |

| Intense Competition & Pricing Pressure | -0.7% | Global, especially APAC | Mid-to-Long-term (2025-2033) |

| Supply Chain Disruptions & Geopolitical Risks | -1.1% | Global, specific regions (e.g., East Asia) | Short-to-Mid-term (2025-2029) |

| Maintaining High Quality & Yield in Complex Processes | -0.6% | Global | Long-term (2025-2033) |

| Environmental Regulations & Sustainability Demands | -0.5% | Europe, North America, parts of Asia | Mid-to-Long-term (2025-2033) |

Outsourced Semiconductor Assembly and Test Market - Updated Report Scope

This report provides a comprehensive analysis of the global Outsourced Semiconductor Assembly and Test (OSAT) market, covering market sizing, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It delves into a detailed segmentation analysis based on service type, packaging type, application, and end-user, offering granular insights into the market's structure and dynamics. The report also highlights regional market performance, identifies key industry players, and assesses the impact of emerging technologies like Artificial Intelligence on the OSAT landscape. The objective is to equip stakeholders with actionable market intelligence for strategic decision-making and investment planning within the evolving semiconductor industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 48.5 Billion |

| Market Forecast in 2033 | USD 110.4 Billion |

| Growth Rate | 10.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Global OSAT Provider A, Major OSAT Services Company B, Advanced Packaging Solutions Firm C, Semiconductor Testing Specialist D, Integrated Assembly & Test Corporation E, Global Microelectronics Services F, Precision Assembly & Test Solutions G, High-Tech Packaging Partner H, Next-Gen OSAT Innovator I, Comprehensive Semiconductor Outsourcing J, Asia-Pacific OSAT Leader K, North American OSAT Pioneer L, European Advanced Packaging M, Emerging Market OSAT N, Specialized Test & Assembly Provider O, Global Integrated Semiconductor Services P, Chip Packaging Innovator Q, Leading Automotive OSAT R, High-Volume OSAT Manufacturer S, Advanced Technology Test House T |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Outsourced Semiconductor Assembly and Test (OSAT) market is intricately segmented to provide a granular understanding of its diverse components and evolving dynamics. This segmentation encompasses various dimensions, including the type of services offered, the specific packaging technologies utilized, the diverse application areas where semiconductors are deployed, and the distinct end-user categories driving demand. Such a detailed breakdown enables a comprehensive analysis of market performance across different verticals and technological fronts, highlighting areas of high growth and emerging opportunities for OSAT providers.

The services segment distinguishes between assembly and testing, recognizing their unique processes and value propositions within the OSAT ecosystem. Packaging types further differentiate between traditional and advanced solutions, reflecting the industry's shift towards more sophisticated integration techniques. Application segmentation reveals the critical industries relying on OSAT, from consumer electronics to highly specialized automotive and AI sectors. Lastly, end-user categories highlight the primary client bases, primarily fabless companies and integrated device manufacturers, each with distinct outsourcing needs and strategies. This multi-faceted segmentation provides a robust framework for understanding the market's current state and predicting its future trajectory.

- By Service Type:

- Assembly: Encompasses various packaging methods such as wire bonding, flip chip, wafer level packaging, and 3D stacking.

- Testing: Includes critical stages like wafer sort, final test, burn-in test, and package test to ensure functionality and reliability.

- By Packaging Type:

- Advanced Packaging: Features cutting-edge solutions like Fan-out Wafer Level Packaging (FO-WLP), Fan-in Wafer Level Packaging (FI-WLP), Flip Chip (FC), and 2.5D/3D IC Packaging, catering to high-performance and miniaturization demands.

- Traditional Packaging: Includes well-established methods such as Quad Flat No-leads (QFN), Small Outline Package (SOP), Quad Flat Package (QFP), and Ball Grid Array (BGA).

- By Application:

- Consumer Electronics: Driven by smartphones, wearables, laptops, and home appliances.

- Automotive: Includes semiconductors for ADAS, infotainment, electric vehicles, and autonomous driving.

- Telecommunications: Supports infrastructure for 5G, networking equipment, and mobile devices.

- Industrial: Covers semiconductors for factory automation, robotics, and power management.

- Medical: Utilized in medical devices, diagnostics, and imaging equipment.

- Aerospace & Defense: For high-reliability and ruggedized applications.

- Data Centers: Critical for servers, storage, and networking in cloud computing and HPC.

- Others: Including smart cards, security, and specialized niche markets.

- By End-User:

- Fabless Semiconductor Companies: Rely entirely on outsourced manufacturing and test services.

- Integrated Device Manufacturers (IDMs): Increasingly outsource parts of their assembly and test operations to leverage specialized OSAT capabilities.

Regional Highlights

- Asia Pacific (APAC): APAC dominates the Outsourced Semiconductor Assembly and Test market, primarily driven by the presence of major OSAT players and a vast semiconductor manufacturing ecosystem in countries like Taiwan, China, South Korea, and Southeast Asia. The region benefits from lower operational costs, extensive infrastructure, and a skilled workforce, coupled with high demand from a booming electronics manufacturing sector. This strong foundation and continuous investment in advanced packaging technologies solidify APAC's leading position and expected continued growth, especially with increasing regional demand for AI-driven devices and advanced consumer electronics.

- North America: North America holds a significant share, characterized by its focus on high-end, advanced packaging solutions and cutting-edge research and development. The region is home to numerous fabless semiconductor companies and integrated device manufacturers that heavily outsource complex assembly and test processes. Driven by innovation in AI, high-performance computing, and specialized automotive applications, North American firms seek OSAT partners capable of delivering sophisticated, high-reliability services, often prioritizing technological leadership and rapid prototyping capabilities.

- Europe: The European OSAT market is growing steadily, with a strong emphasis on automotive electronics, industrial applications, and niche high-value markets. European semiconductor companies prioritize reliability, quality, and specialized testing for mission-critical components. While not as dominant in sheer manufacturing volume as APAC, Europe's contribution lies in its demand for customized solutions and its robust R&D landscape, fostering partnerships with OSAT providers that can meet stringent quality and regulatory standards for specialized applications.

- Latin America: The OSAT market in Latin America is in an emerging phase, with increasing investments in manufacturing capabilities, particularly in Mexico and Brazil. Growth is propelled by expanding consumer electronics assembly and automotive manufacturing sectors in the region. While currently smaller in scale, the potential for market expansion is driven by efforts to diversify global supply chains and attract foreign direct investment in semiconductor-related industries.

- Middle East and Africa (MEA): The MEA region represents a nascent but potentially growing market for OSAT services. Growth is primarily linked to government initiatives to diversify economies, develop local technology industries, and increase domestic electronics manufacturing. While the current market size is relatively small, future opportunities are expected to arise from investments in smart cities, IoT infrastructure, and regional data centers, gradually driving demand for outsourced semiconductor services.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Outsourced Semiconductor Assembly and Test Market.- Leading Global OSAT Provider A

- Major OSAT Services Company B

- Advanced Packaging Solutions Firm C

- Semiconductor Testing Specialist D

- Integrated Assembly & Test Corporation E

- Global Microelectronics Services F

- Precision Assembly & Test Solutions G

- High-Tech Packaging Partner H

- Next-Gen OSAT Innovator I

- Comprehensive Semiconductor Outsourcing J

- Asia-Pacific OSAT Leader K

- North American OSAT Pioneer L

- European Advanced Packaging M

- Emerging Market OSAT N

- Specialized Test & Assembly Provider O

- Global Integrated Semiconductor Services P

- Chip Packaging Innovator Q

- Leading Automotive OSAT R

- High-Volume OSAT Manufacturer S

- Advanced Technology Test House T

Frequently Asked Questions

Analyze common user questions about the Outsourced Semiconductor Assembly and Test market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Outsourced Semiconductor Assembly and Test (OSAT)?

Outsourced Semiconductor Assembly and Test (OSAT) refers to specialized third-party providers that offer integrated circuit (IC) packaging, assembly, and testing services for semiconductor companies. These services are crucial post-fabrication, transforming raw silicon wafers into finished, functional chips ready for integration into electronic devices. OSAT companies enable chip designers to outsource capital-intensive back-end processes, focusing on core design and innovation.

Why is the OSAT market experiencing significant growth?

The OSAT market's growth is driven by several factors: increasing complexity of chip designs requiring advanced packaging, the pervasive adoption of the fabless manufacturing model, surging demand from high-growth sectors like AI, 5G, and automotive, and the continuous need for cost efficiency and scalability in semiconductor manufacturing. Outsourcing these processes allows semiconductor companies to reduce capital expenditure and accelerate time-to-market.

What are the primary types of services offered by OSAT providers?

OSAT providers primarily offer two main categories of services: Assembly and Testing. Assembly involves packaging the bare semiconductor die into a protective casing, utilizing technologies like wire bonding, flip chip, or advanced 2.5D/3D stacking. Testing involves verifying the functionality and performance of the assembled chips at various stages, including wafer sort, final test, and burn-in test, to ensure product quality and reliability.

How do advanced packaging technologies impact the OSAT market?

Advanced packaging technologies, such as fan-out wafer-level packaging, 2.5D/3D integration, and chiplet solutions, are a significant growth engine for the OSAT market. These technologies enable higher performance, greater integration density, and smaller form factors for modern electronic devices. OSAT providers are at the forefront of investing in and developing these complex capabilities, becoming indispensable partners for semiconductor companies seeking to innovate beyond traditional packaging limits.

What are the key regional trends shaping the OSAT market?

The Asia Pacific (APAC) region currently dominates the OSAT market due to its established manufacturing ecosystems, lower costs, and extensive skilled labor force, particularly in Taiwan, China, and South Korea. North America and Europe focus on high-end, specialized services for advanced applications like AI and automotive. A growing trend towards supply chain diversification and regionalization is also emerging, leading to potential expansion and investment in other regions like Southeast Asia and select areas of North America and Europe to enhance resilience.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted