Non evaporable Getter Pump Market

Non evaporable Getter Pump Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701335 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

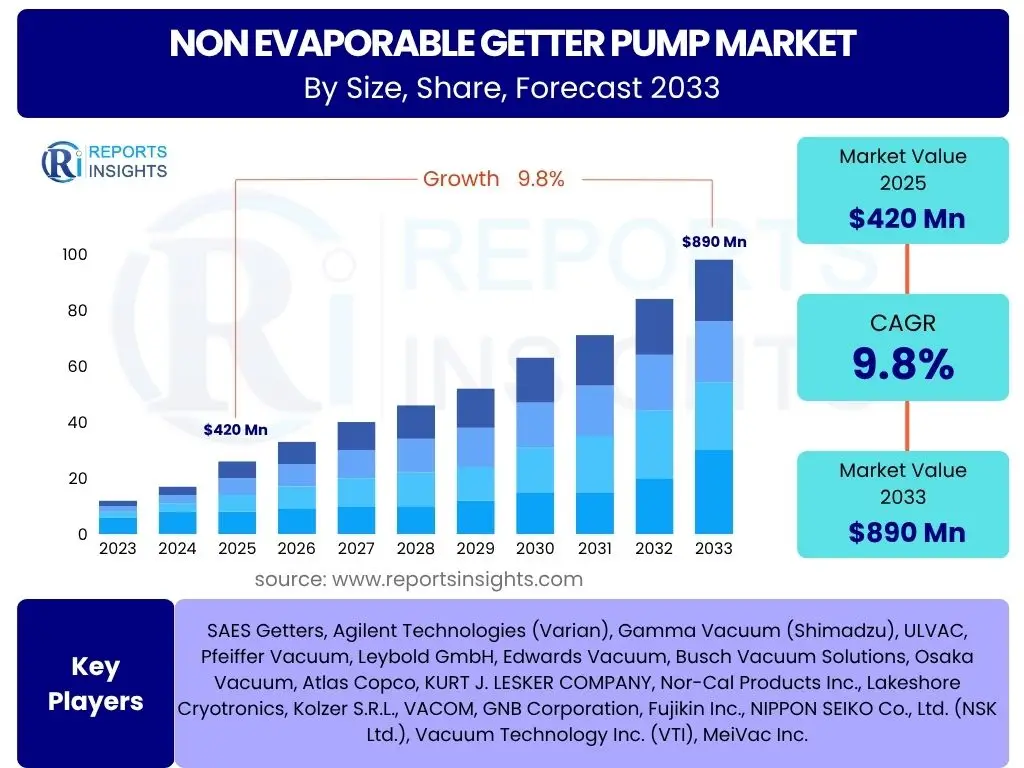

Non evaporable Getter Pump Market Size

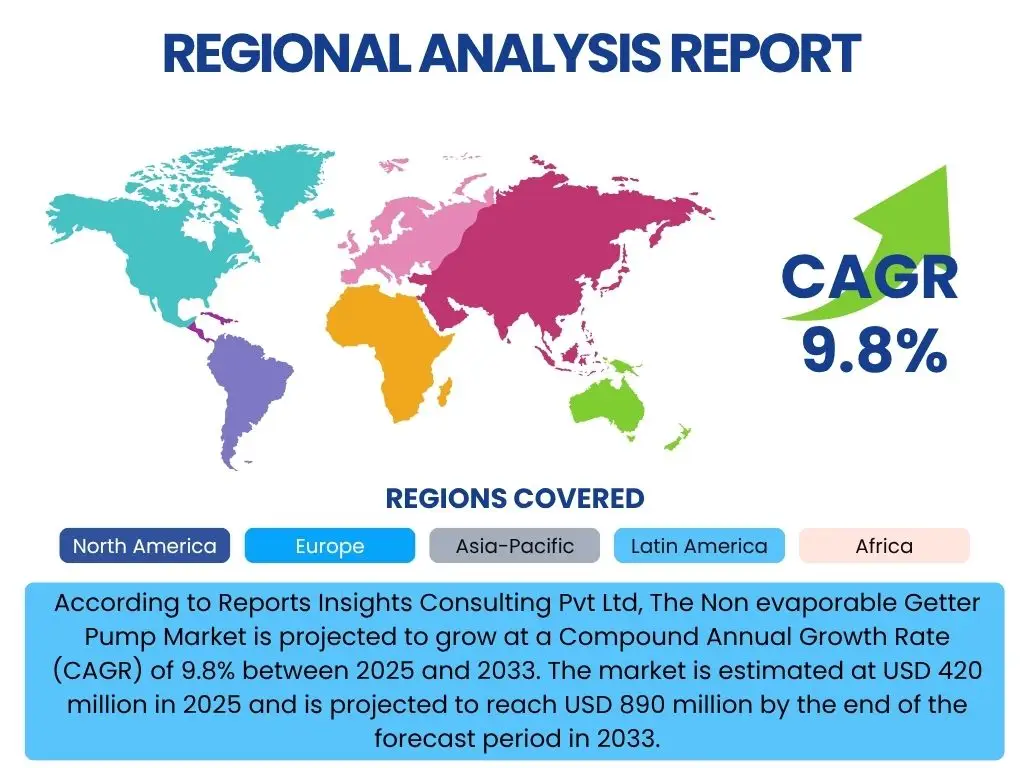

According to Reports Insights Consulting Pvt Ltd, The Non evaporable Getter Pump Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 420 million in 2025 and is projected to reach USD 890 million by the end of the forecast period in 2033.

Key Non evaporable Getter Pump Market Trends & Insights

Common user questions regarding market trends for Non-evaporable Getter Pumps often revolve around their evolving applications, technological advancements, and integration into new high-tech industries. The market is witnessing a significant shift towards ultra-high vacuum (UHV) and extreme-high vacuum (XHV) requirements, driven by miniaturization in electronics and the need for pristine environments in advanced research. This demand fuels innovation in getter material composition and design, enhancing pumping efficiency and lifespan.

Another prominent trend is the increasing adoption of non-evaporable getter pumps in emerging fields such as quantum computing, advanced scientific instruments, and specialized medical device manufacturing. These applications demand highly stable and contaminant-free vacuum environments, which traditional pumping methods may struggle to achieve cost-effectively or efficiently. The market is also experiencing a push towards more energy-efficient and compact pump designs, aligning with broader industry goals of sustainability and reduced operational footprint. Furthermore, the integration of smart monitoring and predictive maintenance capabilities is becoming more prevalent, offering users enhanced control and reliability.

- Growing demand for Ultra-High Vacuum (UHV) and Extreme-High Vacuum (XHV) environments in critical applications.

- Miniaturization and integration of getter technology into compact vacuum systems.

- Development of advanced getter materials with enhanced pumping speeds and capacity.

- Increasing application in emerging sectors such as quantum computing, space simulation, and advanced research.

- Focus on energy efficiency and longer operational lifespan for getter pumps.

AI Impact Analysis on Non evaporable Getter Pump

User inquiries concerning AI's influence on the Non-evaporable Getter Pump market frequently address its potential to optimize performance, enhance manufacturing processes, and enable new applications. AI-driven predictive maintenance is a key area, where algorithms analyze sensor data from vacuum systems to forecast pump degradation, allowing for proactive maintenance and minimizing downtime. This capability extends the operational lifespan of getter pumps and reduces total cost of ownership, addressing common concerns about maintenance complexities and unexpected failures.

Furthermore, AI and machine learning are increasingly utilized in the R&D phase of getter materials and pump designs. Computational models can simulate various material compositions and structural configurations, predicting their getter properties and adsorption capacities under different vacuum conditions. This accelerates the discovery of novel, high-performance getter alloys and optimizes manufacturing parameters, leading to more efficient and durable products. Users anticipate that AI integration will lead to smarter, more autonomous vacuum systems that can self-regulate and adapt to changing process demands, ensuring optimal vacuum levels with minimal human intervention.

- Predictive maintenance and fault detection, optimizing pump lifespan and reducing downtime.

- AI-driven material science research for novel getter alloys and improved performance.

- Enhanced process control and automation in manufacturing, ensuring consistent product quality.

- Real-time monitoring and adaptive vacuum system management for optimal efficiency.

- Data analytics for performance optimization and identifying new application areas.

Key Takeaways Non evaporable Getter Pump Market Size & Forecast

Common user questions regarding key takeaways from the Non-evaporable Getter Pump market size and forecast highlight the significant growth potential and strategic importance of this niche technology. The market's projected growth trajectory underscores the escalating global demand for ultra-high and extreme-high vacuum solutions across various high-tech industries. A primary insight is that technological advancements, particularly in semiconductor manufacturing and advanced research, are the core drivers of this expansion, emphasizing the getter pump's role as a critical enabler of next-generation technologies.

Another crucial takeaway is the increasing geographical diversification of demand, with significant growth anticipated in APAC due to its burgeoning electronics manufacturing sector, alongside sustained demand from established markets in North America and Europe for R&D and specialized industrial applications. The market's resilience is also notable, driven by its indispensable nature in preventing contamination and maintaining pristine environments, which are non-negotiable requirements in industries like microelectronics, analytical instrumentation, and particle physics. This ensures a stable and continuously expanding market, less susceptible to broader economic fluctuations due to its specific high-value applications.

- Substantial growth expected, primarily driven by UHV/XHV requirements in semiconductors and research.

- Asia-Pacific is poised for significant expansion due to manufacturing prowess.

- Technological innovation in getter materials and compact designs is crucial for market penetration.

- The indispensable nature of getter pumps in contamination-sensitive environments ensures stable demand.

- Strategic investments in R&D and expanding application scope are key for market players.

Non evaporable Getter Pump Market Drivers Analysis

The Non-evaporable Getter Pump market is propelled by several robust drivers, primarily the escalating demand for ultra-high vacuum (UHV) and extreme-high vacuum (XHV) environments across diverse high-technology sectors. Industries such as semiconductor manufacturing, flat-panel display production, and advanced scientific research inherently require pristine, contaminant-free vacuum conditions to ensure product integrity, process efficiency, and accurate experimental results. Getter pumps offer a highly effective solution for maintaining these demanding vacuum levels by irreversibly adsorbing residual gases, significantly reducing background pressure and extending the lifespan of vacuum systems.

Furthermore, the continuous advancements in materials science and nanotechnology necessitate increasingly stringent vacuum conditions for deposition, etching, and analysis processes. Non-evaporable getter pumps, with their ability to handle a wide range of gases and their compact footprint, are becoming indispensable components in these evolving technological landscapes. The global push for miniaturization in electronics and the expansion of specialized fields like quantum computing and space simulation also contribute significantly, as these areas critically rely on stable and high-purity vacuum environments that getter pumps can reliably provide.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Semiconductor & Electronics Manufacturing | +2.5% | Asia Pacific (China, Taiwan, South Korea), North America | Short to Long-term (2025-2033) |

| Increasing Demand for Ultra-High Vacuum (UHV) and Extreme-High Vacuum (XHV) | +2.0% | Global, particularly Research & Academia centers | Short to Long-term (2025-2033) |

| Advancements in Scientific Research and Particle Accelerators | +1.5% | Europe, North America, Japan | Medium to Long-term (2027-2033) |

| Expansion of Flat Panel Display and Solar Panel Production | +1.0% | Asia Pacific (China, South Korea, Japan) | Short to Medium-term (2025-2030) |

| Development of New Materials and Nanotechnology Applications | +0.8% | Global | Medium to Long-term (2027-2033) |

Non evaporable Getter Pump Market Restraints Analysis

Despite the robust growth drivers, the Non-evaporable Getter Pump market faces certain restraints that could temper its expansion. One significant challenge is the relatively high upfront cost associated with these specialized pumps compared to some alternative vacuum technologies. While getter pumps offer superior performance in specific UHV/XHV applications, the initial investment can be a deterrent for budget-conscious organizations or those with less stringent vacuum requirements, leading them to opt for more conventional, albeit less efficient, pumping solutions. This cost sensitivity can particularly impact smaller research facilities or industrial operations.

Another restraint lies in the niche application of non-evaporable getter pumps. Their primary utility is confined to environments demanding extremely pure vacuum, which limits their broad adoption across all vacuum-dependent industries. This specificity means the market size is inherently smaller than that for general-purpose vacuum pumps. Furthermore, the limited lifespan of getter materials, which eventually become saturated with adsorbed gases and require replacement, contributes to ongoing operational costs and maintenance complexities. The need for periodic replacement and specialized installation procedures can add to the total cost of ownership, influencing procurement decisions and potentially slowing market penetration in certain segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost and Installation Complexity | -1.2% | Global, particularly smaller enterprises | Short to Medium-term (2025-2030) |

| Limited Lifespan and Need for Replacement | -0.9% | Global, all end-use industries | Medium to Long-term (2027-2033) |

| Competition from Alternative Vacuum Technologies (e.g., Ion Pumps, Cryopumps) | -0.7% | Global, specific industrial segments | Short to Long-term (2025-2033) |

| Dependency on High-Tech Manufacturing Cycles | -0.5% | Global, especially APAC, North America | Short-term (2025-2026) |

Non evaporable Getter Pump Market Opportunities Analysis

Significant opportunities exist for the Non-evaporable Getter Pump market, primarily driven by the continuous emergence of new high-tech applications that demand exceptionally clean and stable vacuum environments. Fields such as quantum computing, advanced space simulation chambers, and next-generation analytical instruments are rapidly evolving, each requiring sophisticated vacuum solutions to function optimally. Non-evaporable getter pumps are uniquely positioned to meet these stringent requirements due to their ability to achieve very low base pressures and efficiently handle residual gases, offering a distinct advantage over other pumping technologies in these specific, high-value applications.

Furthermore, there is a growing opportunity in developing more integrated and compact getter solutions. As various technologies undergo miniaturization, the demand for smaller, more efficient vacuum components that can be seamlessly incorporated into complex systems increases. This pushes manufacturers to innovate in terms of material efficiency, design, and integration capabilities, opening avenues for partnerships with OEMs in specialized equipment manufacturing. The expansion into new geographic markets, particularly in developing economies that are rapidly building their semiconductor and research infrastructure, also presents a substantial growth avenue for market players seeking to diversify their revenue streams and capture new demand centers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New High-Tech Applications (e.g., Quantum Computing, Space Simulation) | +1.8% | North America, Europe, Asia Pacific | Medium to Long-term (2027-2033) |

| Technological Integration and Miniaturization of Vacuum Systems | +1.5% | Global, especially Electronics & Photonics sectors | Short to Long-term (2025-2033) |

| Expansion into New Geographic Markets (e.g., Emerging Economies) | +1.0% | Asia Pacific (Southeast Asia), Latin America, MEA | Medium-term (2027-2031) |

| R&D in Advanced Getter Materials for Enhanced Performance | +0.8% | Global, R&D focused regions | Long-term (2029-2033) |

Non evaporable Getter Pump Market Challenges Impact Analysis

The Non-evaporable Getter Pump market faces several critical challenges that require strategic navigation for sustained growth. One primary challenge is the significant capital investment required for research and development (R&D) into novel getter materials and advanced pump designs. Developing materials that offer higher pumping speeds, greater capacity, and extended lifespans under diverse operating conditions demands extensive scientific expertise and substantial financial resources. This high R&D cost can be a barrier to entry for new players and can strain the resources of existing companies, potentially slowing down innovation cycles or increasing product costs.

Another significant challenge is the intense competition from established alternative vacuum technologies, such as ion pumps and cryopumps, which have their own specific advantages and well-entrenched market positions. While non-evaporable getter pumps offer unique benefits in specific UHV/XHV applications, convincing end-users to switch from familiar and often less expensive alternatives requires strong technical justification and demonstration of superior long-term value. Furthermore, the market's reliance on highly skilled personnel for installation, maintenance, and troubleshooting poses a challenge, particularly in regions where such expertise is scarce. Training and retaining this specialized workforce adds to operational costs and can limit scalability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D Investment for Material Science and Design | -1.0% | Global, particularly leading technology hubs | Short to Long-term (2025-2033) |

| Competition from Established Alternative Vacuum Technologies | -0.8% | Global, all industrial segments | Short to Medium-term (2025-2030) |

| Stringent Quality and Performance Requirements | -0.6% | Global, particularly highly regulated industries | Short to Long-term (2025-2033) |

| Market Awareness and Education for Niche Applications | -0.4% | Emerging markets, less specialized industries | Medium-term (2027-2031) |

Non evaporable Getter Pump Market - Updated Report Scope

This market insights report on Non-evaporable Getter Pumps provides a comprehensive analysis of the current market landscape, historical performance, and future growth projections. It delves into the underlying market dynamics, including key drivers, restraints, opportunities, and challenges, offering a holistic view for stakeholders. The report segments the market extensively by type, material, application, and end-use industry, providing granular insights into demand patterns across different verticals. Furthermore, it offers a detailed regional analysis, highlighting growth hotspots and market specifics across major geographies. The competitive landscape section profiles key players, their strategies, and recent developments, delivering actionable intelligence for strategic decision-making in this specialized vacuum technology sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 420 Million |

| Market Forecast in 2033 | USD 890 Million |

| Growth Rate | 9.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SAES Getters, Agilent Technologies (Varian), Gamma Vacuum (Shimadzu), ULVAC, Pfeiffer Vacuum, Leybold GmbH, Edwards Vacuum, Busch Vacuum Solutions, Osaka Vacuum, Atlas Copco, KURT J. LESKER COMPANY, Nor-Cal Products Inc., Lakeshore Cryotronics, Kolzer S.R.L., VACOM, GNB Corporation, Fujikin Inc., NIPPON SEIKO Co., Ltd. (NSK Ltd.), Vacuum Technology Inc. (VTI), MeiVac Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Non-evaporable Getter Pump market is meticulously segmented to provide a detailed understanding of its diverse facets and varying demand dynamics across different product types, materials, applications, and end-use industries. This granular segmentation allows for a precise analysis of specific market niches, enabling stakeholders to identify key growth areas and tailor their strategies accordingly. By understanding the preferences and requirements within each segment, companies can optimize their product offerings, sales channels, and marketing efforts to achieve maximum market penetration and profitability.

The segmentation by type, for instance, distinguishes between Bulk Getters, Thin Film Getters, and Flash Getters, each with unique characteristics and suitability for different vacuum applications. Similarly, the material segmentation highlights the importance of specific alloys like Zirconium-Aluminum and Titanium-Zirconium-Vanadium, which are crucial for their getter properties. Application-based segmentation provides insights into which industries are driving demand, from semiconductor manufacturing to advanced scientific research, while end-use industry segmentation categorizes the market by broader sectors such as electronics, healthcare, and aerospace, offering a comprehensive view of the market's reach and impact.

- By Type: This segment includes Bulk Getters, characterized by their significant capacity and long lifespan, often used in large-scale vacuum systems. Thin Film Getters offer a compact solution, suitable for miniaturized devices and integrated systems. Flash Getters provide rapid pumping capabilities for specific short-burst applications.

- By Material: Key materials comprise Zirconium-Aluminum Alloys (e.g., St 101, St 707), widely used for their excellent hydrogen and active gas adsorption. Titanium-Zirconium-Vanadium (Ti-Zr-V) Alloys are prominent for their broad spectrum of gas adsorption, including inert gases when activated. Barium Alloys and other specialized compositions cater to unique vacuum requirements and temperature ranges.

- By Application:

- Semiconductor Manufacturing: Critical for producing integrated circuits and microchips under ultra-high vacuum conditions.

- Flat Panel Displays: Essential for processes like sputtering and deposition in LCD and OLED production.

- Scientific Instruments: Utilized in particle accelerators, electron microscopes, and mass spectrometers for pristine vacuum environments.

- Research & Development: Employed in material science, fundamental physics, and advanced chemistry experiments requiring UHV/XHV.

- Solar Panels: Used in the manufacturing of thin-film solar cells.

- Medical Devices: For creating sterile vacuum conditions in medical equipment and analytical instruments.

- Vacuum Insulation Panels (VIPs): Enhancing insulation performance in various applications.

- Others: Including applications in aerospace, defense, and specialized industrial processes.

- By End-Use Industry:

- Electronics: Encompassing semiconductors, displays, and other electronic components.

- Aerospace & Defense: For space simulation chambers and advanced optical systems.

- Healthcare: Used in medical imaging, analytical diagnostics, and pharmaceutical production.

- Automotive: For specialized coatings and component manufacturing.

- Energy: In fusion research, solar energy, and battery production.

- Research & Academia: Across universities and national laboratories for fundamental and applied research.

Regional Highlights

The global Non-evaporable Getter Pump market exhibits distinct regional dynamics, influenced by varying levels of industrialization, technological adoption, and research investments. Asia Pacific (APAC) is projected to emerge as the dominant and fastest-growing region, primarily driven by the colossal expansion of its semiconductor manufacturing base, particularly in countries like China, Taiwan, and South Korea. These nations are at the forefront of global electronics production, necessitating a continuous demand for advanced vacuum solutions to meet increasingly stringent process requirements and accelerate miniaturization. Furthermore, investments in flat-panel display manufacturing and R&D facilities across APAC contribute significantly to market growth.

North America and Europe represent mature yet robust markets for non-evaporable getter pumps, characterized by strong innovation ecosystems and significant investments in scientific research, aerospace, and advanced materials development. Countries such as the United States, Germany, and the United Kingdom are hubs for particle accelerators, electron microscopy, and quantum computing research, all of which critically rely on UHV/XHV environments maintained by getter pumps. While their growth rates may be more modest compared to APAC, these regions continue to drive demand for highly specialized and customized getter solutions, emphasizing performance, reliability, and integration capabilities. Latin America, the Middle East, and Africa (MEA) are emerging regions, with nascent but growing demand stemming from expanding industrialization, educational infrastructure development, and nascent high-tech initiatives.

- Asia Pacific (APAC): Dominant market share and highest growth, fueled by semiconductor manufacturing (China, Taiwan, South Korea, Japan), flat panel display production, and increasing government investments in R&D and advanced materials.

- North America: Strong demand driven by advanced scientific research (e.g., particle physics, nanotechnology), aerospace & defense, and a robust semiconductor industry. Key countries include the United States and Canada.

- Europe: Significant market presence due to major scientific research facilities (e.g., CERN), leading academic institutions, and strong industrial sectors in Germany, France, and the UK, focusing on precision manufacturing and analytical instrumentation.

- Latin America: Emerging market with growing investments in industrial and research sectors, though currently smaller in scale. Countries like Brazil and Mexico are showing increasing potential.

- Middle East and Africa (MEA): Developing market with nascent high-tech initiatives and increasing industrial diversification, particularly in countries like Saudi Arabia and UAE, leading to gradual adoption of advanced vacuum technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Non evaporable Getter Pump Market.- SAES Getters S.p.A.

- Agilent Technologies (Varian)

- Gamma Vacuum (Shimadzu Corporation)

- ULVAC, Inc.

- Pfeiffer Vacuum GmbH

- Leybold GmbH

- Edwards Vacuum (Atlas Copco)

- Busch Vacuum Solutions

- Osaka Vacuum, Ltd.

- KURT J. LESKER COMPANY

- Nor-Cal Products Inc.

- Lakeshore Cryotronics, Inc.

- Kolzer S.R.L.

- VACOM GmbH

- GNB Corporation

- Fujikin Inc.

- NIPPON SEIKO Co., Ltd. (NSK Ltd.)

- Vacuum Technology Inc. (VTI)

- MeiVac Inc.

Frequently Asked Questions

Analyze common user questions about the Non evaporable Getter Pump market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Non-evaporable Getter Pump and how does it work?

A Non-evaporable Getter (NEG) pump is a type of vacuum pump that uses a reactive material, typically an alloy, to chemically adsorb active gas molecules from a vacuum system, creating and maintaining ultra-high vacuum (UHV) or extreme-high vacuum (XHV) conditions. Unlike evaporable getters, NEGs do not require heating to evaporate the getter material onto a surface; instead, they operate by forming stable chemical bonds with gas molecules on their surface, making the adsorption process irreversible without re-release.

What are the primary applications of Non-evaporable Getter Pumps?

NEG pumps are primarily used in applications requiring extremely clean and contaminant-free vacuum environments. Key applications include semiconductor manufacturing (e.g., thin-film deposition, etching), flat panel display production, scientific instruments (e.g., particle accelerators, electron microscopes, mass spectrometers), advanced research and development (e.g., material science, surface analysis), and specialized medical devices or space simulation chambers. They are indispensable where residual gases must be minimized to ensure performance and integrity.

What are the advantages of using Non-evaporable Getter Pumps over other vacuum technologies?

Non-evaporable Getter Pumps offer several advantages, including high pumping speeds for active gases (like hydrogen, carbon monoxide, water vapor), very low ultimate pressures (reaching into the XHV range), no moving parts (leading to vibration-free operation), and relatively compact designs. They also produce no contamination and require no power for continuous pumping once activated, making them highly reliable and energy-efficient for long-term UHV maintenance. Their ability to irreversibly trap gases is crucial for sensitive processes.

What materials are commonly used in Non-evaporable Getter Pumps?

The most common materials used in Non-evaporable Getter Pumps are alloys containing elements like Zirconium (Zr), Titanium (Ti), Vanadium (V), Aluminum (Al), and Barium (Ba). Zirconium-Aluminum alloys (e.g., St 101, St 707) are widely utilized for their excellent hydrogen adsorption. Titanium-Zirconium-Vanadium alloys (e.g., CapaciTorr) are known for broad gas sorption capabilities. These materials are chosen for their high chemical reactivity with residual gases, stability, and ability to be activated at specific temperatures.

What is the future outlook for the Non-evaporable Getter Pump Market?

The future outlook for the Non-evaporable Getter Pump market is highly positive, driven by the increasing demand for ultra-high and extreme-high vacuum environments across various high-tech sectors. Growth will be fueled by continued innovation in semiconductor manufacturing, the expansion of flat panel display production, and the emergence of new applications in quantum computing, advanced scientific research, and space simulation. Technological advancements, including AI integration for predictive maintenance and the development of more efficient getter materials, will further propel market expansion globally, particularly in Asia-Pacific.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted