Pseudo SRAM Market

Pseudo SRAM Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709703 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

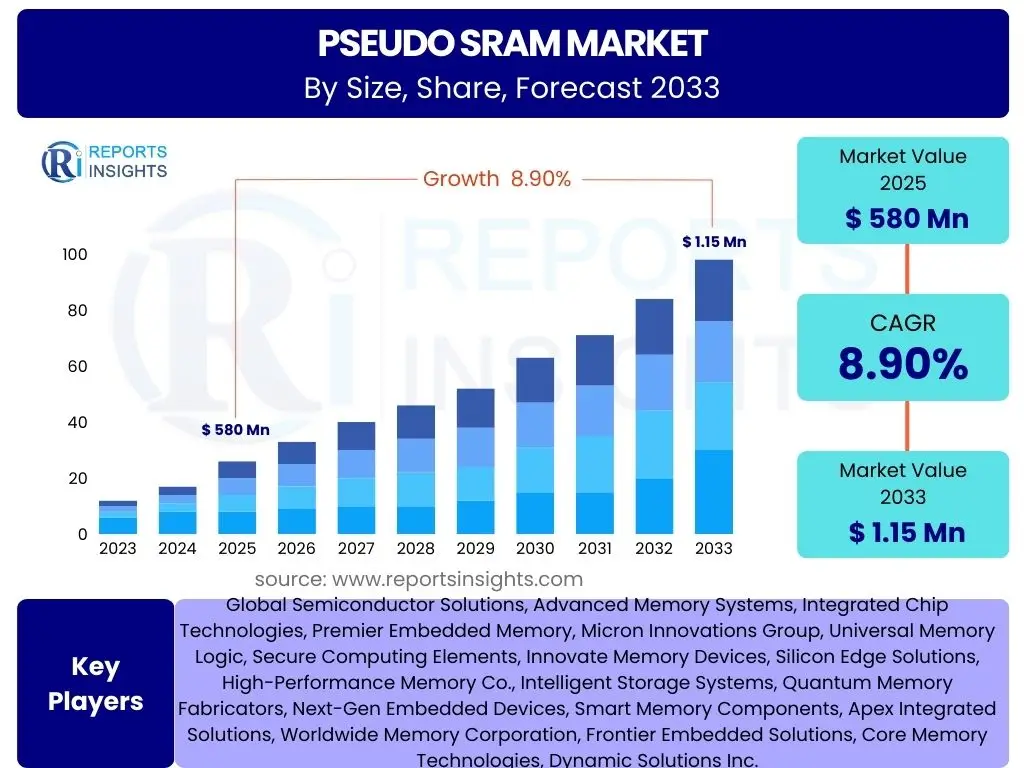

Pseudo SRAM Market Size

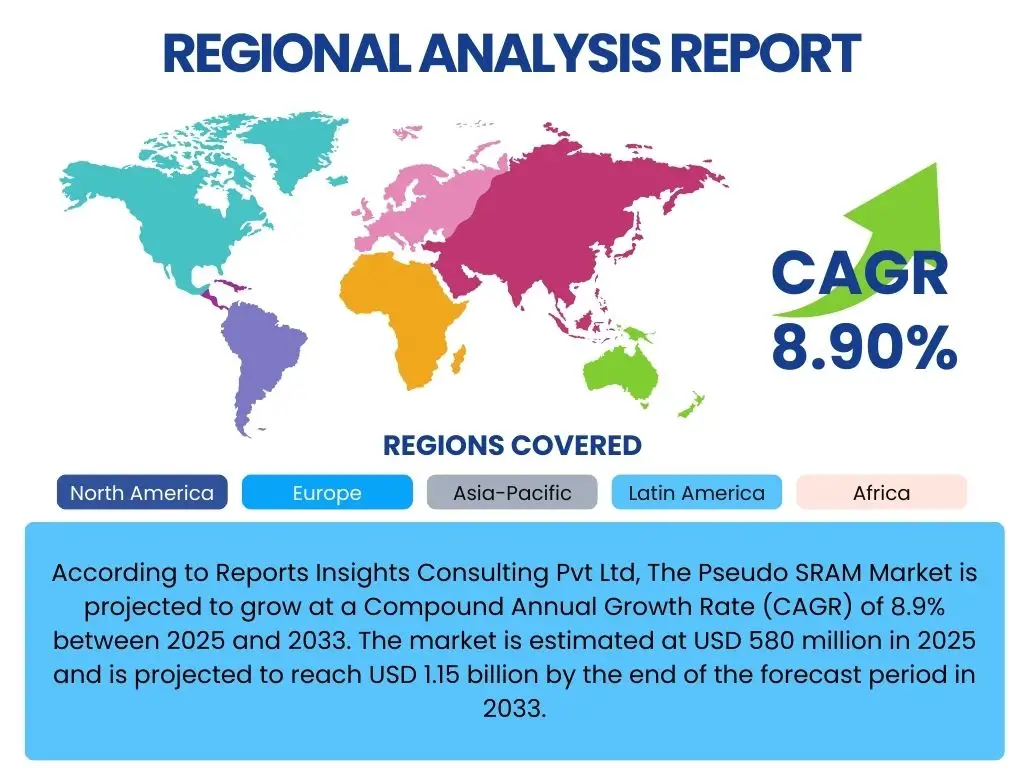

According to Reports Insights Consulting Pvt Ltd, The Pseudo SRAM Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 580 million in 2025 and is projected to reach USD 1.15 billion by the end of the forecast period in 2033.

Key Pseudo SRAM Market Trends & Insights

The Pseudo SRAM market is experiencing robust growth driven by several key trends, primarily the increasing demand for high-performance, low-power memory solutions in a rapidly expanding array of embedded systems. Users frequently inquire about the specific technological advancements and application areas fueling this expansion. Key insights indicate a growing preference for integrated memory solutions that offer a balance of speed, power efficiency, and cost-effectiveness, particularly in portable and IoT devices where battery life is a critical factor. Furthermore, the market is seeing a shift towards higher density Pseudo SRAMs to meet the evolving requirements of sophisticated applications.

Another significant trend is the continuous miniaturization of electronic devices, which necessitates compact memory solutions that can operate efficiently within constrained power envelopes. This miniaturization, coupled with the proliferation of edge computing and artificial intelligence in embedded systems, is driving innovation in Pseudo SRAM technology. The increasing adoption of 5G infrastructure and advanced automotive systems also plays a crucial role, creating new demand for reliable and fast memory that can handle complex data processing tasks without consuming excessive power. These dynamics collectively shape the strategic direction for memory manufacturers and system integrators alike.

- Escalating demand for low-power memory in battery-operated devices.

- Growing integration of Pseudo SRAM in IoT and edge computing applications.

- Increasing adoption of high-density Pseudo SRAM for sophisticated embedded systems.

- Technological advancements in manufacturing processes leading to cost reduction and performance improvement.

- Surging demand from the automotive sector for infotainment and ADAS (Advanced Driver-Assistance Systems).

- Expansion of 5G infrastructure and related networking equipment requiring efficient caching solutions.

- Miniaturization trends in consumer electronics driving compact memory solutions.

AI Impact Analysis on Pseudo SRAM

The advent and rapid proliferation of Artificial Intelligence (AI) are profoundly impacting the Pseudo SRAM market, generating numerous user questions regarding its specific role and future trajectory. Users are keen to understand how AI's demands for efficient data processing, particularly at the edge, translate into opportunities for Pseudo SRAM. AI-powered applications, especially those deployed on edge devices, require rapid access to data for inference while operating within strict power budgets. Pseudo SRAM, with its excellent balance of speed and power efficiency, emerges as a critical component for local caching and buffering of data for AI accelerators and microcontrollers in such scenarios.

The impact extends to the design philosophies of new AI-enabled embedded systems, where the need for quick boot times, responsive user interfaces, and continuous data processing pushes the demand for Pseudo SRAM. Generative AI models, even when optimized for edge deployment, still require efficient memory to handle intermediate computations and feature data. Pseudo SRAM's architecture allows for simpler integration and lower pin counts compared to dynamic RAM, making it suitable for space-constrained AI modules. This symbiotic relationship between AI and Pseudo SRAM is expected to accelerate innovation in memory design, focusing on further improvements in density, speed, and energy consumption tailored for AI workloads.

Furthermore, the growth of TinyML and other ultra-low-power AI initiatives further cements Pseudo SRAM’s position. These applications often run on microcontrollers with limited on-chip memory, necessitating external memory that is both fast enough to support AI inference and power-efficient enough to maintain long battery life. Pseudo SRAM provides a compelling solution by offering a performance level significantly higher than standard NOR flash and a power profile much lower than traditional DRAM, making it an optimal choice for local data storage and buffering in an expanding ecosystem of AI-driven devices, from smart sensors to advanced wearables.

- Enhanced demand for Pseudo SRAM in edge AI devices for efficient data caching.

- Crucial role in providing low-power, high-speed memory for AI accelerators and microcontrollers.

- Facilitates quick boot-up and responsive operation in AI-enabled embedded systems.

- Supports TinyML and ultra-low-power AI applications requiring external memory.

- Drives innovation in Pseudo SRAM design for optimized density, speed, and power for AI workloads.

- Enables localized data buffering for real-time AI inference on portable devices.

- Contributes to reduced system complexity and cost in AI solutions by simplifying memory architecture.

Key Takeaways Pseudo SRAM Market Size & Forecast

User inquiries frequently focus on discerning the most critical aspects of the Pseudo SRAM market’s future trajectory and overall health. The primary takeaway from the market size and forecast data is the consistent and substantial growth expected over the next decade. This growth is not merely incremental but reflective of fundamental shifts in technology and consumer demand. The market’s expansion to USD 1.15 billion by 2033 signifies its increasing indispensability across various industries, underpinning the ongoing digital transformation and the proliferation of smart, connected devices. The robust CAGR of 8.9% confirms a sustained upward trend, indicating strong market confidence and continuous investment in Pseudo SRAM technology.

Another crucial takeaway revolves around the resilience and adaptability of Pseudo SRAM in a highly competitive memory landscape. Despite the emergence of alternative memory technologies, Pseudo SRAM continues to carve out significant niches due to its unique combination of advantages, particularly in applications where power efficiency, cost-effectiveness, and adequate speed are paramount. This sustained relevance highlights its strategic importance for designers balancing performance requirements with energy consumption and overall system cost. The forecast therefore points to a market that is not only growing but also solidifying its position within its core application segments while expanding into new ones.

- The Pseudo SRAM market is set for significant expansion, projecting to nearly double in value by 2033.

- Strong growth is driven by the increasing need for efficient, low-power memory solutions in embedded systems.

- Pseudo SRAM maintains its competitive edge through a compelling balance of cost, performance, and power consumption.

- Emerging technologies like AI and IoT are key growth catalysts for Pseudo SRAM adoption.

- Investment in manufacturing and research & development is expected to continue, driving further innovation.

- The market's stability and growth underscore its critical role in various high-growth industries.

Pseudo SRAM Market Drivers Analysis

The Pseudo SRAM market is propelled by a confluence of factors, each contributing significantly to its growth trajectory. A primary driver is the accelerating proliferation of IoT devices, which inherently require memory solutions that are both power-efficient and cost-effective. These devices, ranging from smart home sensors to industrial monitoring equipment, often operate on battery power for extended periods and need reliable, fast memory for local data storage and processing without the high power overhead of traditional DRAM. Pseudo SRAM’s architecture makes it an ideal choice for these applications, ensuring optimal performance under stringent power constraints.

Furthermore, the robust expansion of the automotive electronics sector serves as another powerful driver. Modern vehicles are increasingly integrating advanced infotainment systems, sophisticated driver-assistance systems (ADAS), and complex engine control units. These systems demand memory with high reliability, low power consumption, and efficient data handling capabilities. Pseudo SRAM fits these requirements perfectly, enabling features like instant-on functionality, quick boot times for navigation and entertainment, and secure data buffering for critical ADAS operations. The transition to electric vehicles and autonomous driving further amplifies this demand, as these platforms incorporate even more embedded intelligence.

The rising adoption of edge computing and artificial intelligence (AI) in embedded applications also significantly fuels the Pseudo SRAM market. Edge devices need to perform real-time data processing and inference locally, minimizing latency and reducing reliance on cloud connectivity. Pseudo SRAM provides the necessary speed for data caching and buffering for AI accelerators while maintaining low power consumption, critical for devices operating away from constant power sources. This synergy with AI and edge computing creates new, high-growth opportunities for Pseudo SRAM manufacturers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of IoT Devices | +2.1% | Global, particularly Asia Pacific & North America | 2025-2033 (Long-term) |

| Growth in Automotive Electronics | +1.8% | Europe, North America, China | 2025-2031 (Medium-term) |

| Increased Adoption of Edge AI | +1.5% | North America, Europe, Asia Pacific | 2026-2033 (Medium to Long-term) |

| Demand for Low-Power Memory | +1.2% | Global | 2025-2033 (Long-term) |

| Miniaturization in Consumer Electronics | +0.8% | Asia Pacific, North America | 2025-2029 (Short to Medium-term) |

| Expansion of 5G Infrastructure | +0.7% | China, North America, Europe | 2025-2030 (Short to Medium-term) |

Pseudo SRAM Market Restraints Analysis

Despite its significant growth potential, the Pseudo SRAM market faces several inherent restraints that could temper its expansion. One major restraint is the intense competition from alternative memory technologies. While Pseudo SRAM offers a unique blend of attributes, other memory types such as Low Power Double Data Rate (LPDDR) DRAM, NOR Flash, and emerging non-volatile memories like MRAM and RRAM, continually improve in performance, density, and cost-effectiveness. In certain applications, these alternatives may offer superior characteristics, compelling designers to opt for different solutions, especially when high density or extreme speeds are prioritized over power efficiency and cost.

Another significant restraint is the relatively limited density of Pseudo SRAM compared to standard DRAM. For applications requiring very large amounts of main memory, Pseudo SRAM often falls short. While it excels in specific niche applications requiring fast, low-power local buffering, it cannot replace DRAM in systems demanding gigabytes of main memory for complex operating systems, large databases, or high-performance computing. This density limitation confines Pseudo SRAM to specific embedded and specialized applications, preventing its wider adoption across all computing platforms. The market faces a continuous challenge to increase density while maintaining its core advantages.

Furthermore, the cost-sensitivity of certain end-use applications acts as a restraint. In highly competitive consumer electronics segments or low-margin industrial devices, every component's cost is scrutinized. While Pseudo SRAM is generally more cost-effective than some specialty SRAMs, it can still be more expensive than certain commodity memory options, particularly in high-volume, cost-optimized designs. Manufacturers must continuously innovate to reduce production costs and offer competitive pricing, especially as the market for embedded solutions becomes increasingly commoditized, putting pressure on profit margins and overall market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Alternative Memory Technologies | -1.5% | Global | 2025-2033 (Long-term) |

| Limited Density Compared to DRAM | -1.0% | Global | 2025-2033 (Long-term) |

| Cost Sensitivity in Volume Applications | -0.8% | Asia Pacific (for manufacturing), Global | 2025-2029 (Short to Medium-term) |

| Supply Chain Volatility and Geopolitical Risks | -0.5% | Global, particularly Asia Pacific | 2025-2028 (Short-term) |

Pseudo SRAM Market Opportunities Analysis

The Pseudo SRAM market is rich with opportunities, driven by technological evolution and the expansion of new application domains. One significant opportunity lies in the continued advancements in Artificial Intelligence and Machine Learning (AI/ML), particularly in edge computing. As AI capabilities are increasingly embedded into devices, from smart home appliances to industrial robots, the need for fast, low-power local memory for AI inference and data buffering escalates. Pseudo SRAM's unique characteristics make it an ideal candidate for supporting these burgeoning AI/ML applications, providing a balance of performance and efficiency that standard memories often cannot match without significant trade-offs. This presents a substantial avenue for market growth and innovation.

Another promising opportunity emerges from the expanding medical and healthcare electronics sector. Wearable health trackers, portable diagnostic devices, and implantable medical instruments require extremely low-power memory solutions with high reliability and compact form factors. Pseudo SRAM is well-suited for these critical applications, ensuring efficient data processing and storage while maximizing battery life and minimizing device size. The stringent requirements of medical devices for longevity and data integrity further underscore Pseudo SRAM’s potential in this high-value market segment, driving demand for specialized, high-quality memory solutions.

Furthermore, the ongoing deployment of 5G infrastructure and the subsequent growth in connected devices and data traffic create ample opportunities. Base stations, network equipment, and specialized industrial controllers within the 5G ecosystem require efficient caching memory to handle high-bandwidth data streams with minimal latency. Pseudo SRAM can serve as an effective buffer memory in these network elements, contributing to overall system performance and energy efficiency. The demand for robust and reliable memory solutions in these critical infrastructure applications offers a stable and growing market for Pseudo SRAM manufacturers, prompting continued innovation in interface speeds and densities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Edge AI/ML Applications | +1.9% | North America, Europe, Asia Pacific | 2026-2033 (Medium to Long-term) |

| Growth in Medical and Healthcare Devices | +1.3% | North America, Europe | 2025-2033 (Long-term) |

| 5G Infrastructure & Network Equipment | +1.0% | China, North America, Europe | 2025-2031 (Medium-term) |

| Development of Advanced Wearable Technology | +0.9% | Global | 2027-2033 (Medium to Long-term) |

| Integration in Specialized Industrial Controllers | +0.7% | Europe, Asia Pacific | 2025-2030 (Short to Medium-term) |

Pseudo SRAM Market Challenges Impact Analysis

The Pseudo SRAM market, while growing, is not immune to significant challenges that could impede its progress. One primary challenge is the risk of technological obsolescence due to the rapid pace of innovation in the broader memory market. New memory technologies, often backed by substantial research and development, continuously emerge with promises of superior performance, lower power, or higher density. While Pseudo SRAM has maintained its niche, any breakthrough in alternative memory solutions that effectively combines its advantages with superior density or lower cost could quickly diminish its market share. Staying competitive requires continuous investment in R&D and strategic adaptation to evolving technological landscapes.

Another critical challenge involves the complexities of intellectual property (IP) and fierce competition among semiconductor manufacturers. The memory market is highly litigious, with numerous patents covering various aspects of memory design, manufacturing processes, and interface technologies. Companies must navigate this intricate IP landscape carefully, ensuring compliance while striving to innovate. Furthermore, intense competition can lead to pricing pressures and reduced profit margins, particularly for less differentiated products. This necessitates robust product development strategies and strong market positioning to sustain profitability and investment in future technologies.

Furthermore, managing the global supply chain for semiconductor components presents ongoing challenges. Geopolitical tensions, natural disasters, and unexpected demand surges can all disrupt the production and delivery of Pseudo SRAM. Manufacturers must maintain resilient supply chains, potentially diversifying production locations and cultivating strong relationships with suppliers and logistics partners. The capital-intensive nature of semiconductor manufacturing also poses a barrier to entry, requiring significant initial investment and continuous upgrades to fabrication facilities, which can be a financial strain, particularly for smaller market players or during economic downturns.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Risk of Technological Obsolescence | -1.2% | Global | 2028-2033 (Long-term) |

| Intense Competition and Pricing Pressures | -0.9% | Asia Pacific (manufacturing hubs), Global | 2025-2029 (Short to Medium-term) |

| Supply Chain Disruptions and Geopolitical Risks | -0.7% | Global | 2025-2028 (Short-term) |

| High R&D Investment Requirements | -0.5% | Global | 2025-2033 (Long-term) |

Pseudo SRAM Market - Updated Report Scope

This report provides a comprehensive analysis of the Pseudo SRAM market, offering detailed insights into its current state, historical performance, and future growth projections. It covers key market dynamics, including drivers, restraints, opportunities, and challenges, along with an in-depth segmentation analysis by type, density, interface, application, and end-use industry across various geographic regions. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making in this evolving memory landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 580 million |

| Market Forecast in 2033 | USD 1.15 billion |

| Growth Rate | 8.9% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Semiconductor Solutions, Advanced Memory Systems, Integrated Chip Technologies, Premier Embedded Memory, Micron Innovations Group, Universal Memory Logic, Secure Computing Elements, Innovate Memory Devices, Silicon Edge Solutions, High-Performance Memory Co., Intelligent Storage Systems, Quantum Memory Fabricators, Next-Gen Embedded Devices, Smart Memory Components, Apex Integrated Solutions, Worldwide Memory Corporation, Frontier Embedded Solutions, Core Memory Technologies, Dynamic Solutions Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Pseudo SRAM market is meticulously segmented to provide a granular view of its diverse landscape and to identify specific growth areas and market dynamics. This comprehensive segmentation allows for a detailed understanding of how different product types, densities, interfaces, applications, and end-use industries contribute to the overall market structure and evolution. By analyzing these segments, stakeholders can pinpoint specific opportunities and tailor strategies to address the nuanced demands of various market verticals, ensuring a targeted approach to product development and market penetration.

- By Type: Asynchronous PSRAM, Synchronous PSRAM, Low-Power PSRAM. Asynchronous PSRAM typically offers simpler integration, while Synchronous PSRAM provides higher speed, and Low-Power PSRAM focuses on energy efficiency, crucial for battery-operated devices.

- By Density: 8Mb, 16Mb, 32Mb, 64Mb, 128Mb, 256Mb, 512Mb, 1Gb and Above. Higher densities are increasingly demanded by advanced applications such as AI edge devices and complex industrial controllers.

- By Interface: Multiplexed Interface (e.g., ADM), Non-Multiplexed Interface (e.g., SRAM-like), Serial Peripheral Interface (SPI), Quad SPI (QSPI). The choice of interface impacts data transfer speed, pin count, and system complexity.

- By Application: Consumer Electronics (Smartphones, Wearables, Tablets), Automotive (Infotainment, ADAS, ECUs), Industrial (Automation, Control Systems), Medical Devices (Portable Diagnostics, Wearables), IoT Devices (Sensors, Gateways), Networking Equipment (Routers, Switches), AI Edge Devices. Each application area leverages Pseudo SRAM's unique attributes differently.

- By End-Use Industry: Telecommunications, Data Processing, Manufacturing, Healthcare, Automotive, Energy & Utilities, Aerospace & Defense. These industries represent the primary consumers of Pseudo SRAM, each with specific requirements regarding reliability, performance, and environmental robustness.

Regional Highlights

- North America: This region is a significant market for Pseudo SRAM, primarily driven by robust investments in research and development, high adoption of advanced technologies like AI, IoT, and edge computing, and a strong presence of key semiconductor manufacturers and innovative tech companies. The automotive sector, particularly for ADAS and in-car infotainment systems, also contributes substantially to demand.

- Europe: Characterized by a strong industrial automation sector and a burgeoning automotive industry, Europe presents a stable market for Pseudo SRAM. Emphasis on sustainable technologies and strict regulatory frameworks drives demand for energy-efficient memory solutions, particularly in industrial control systems, medical devices, and connected vehicles.

- Asia Pacific (APAC): The largest and fastest-growing market, APAC is dominated by major manufacturing hubs in China, Japan, South Korea, and Taiwan. The region benefits from extensive consumer electronics production, rapid adoption of IoT devices, significant government initiatives in 5G infrastructure deployment, and a booming automotive sector, making it a critical area for Pseudo SRAM demand and supply.

- Latin America: This region is an emerging market for Pseudo SRAM, with increasing investments in telecommunications infrastructure, growing adoption of smart devices, and expanding industrial automation. While smaller than other regions, it offers considerable growth potential as digital transformation initiatives gain momentum.

- Middle East and Africa (MEA): The MEA region is witnessing gradual growth, driven by diversification efforts from oil-dependent economies towards technology and smart city initiatives. Increasing adoption of IoT in various sectors and infrastructure development projects contribute to the demand for reliable embedded memory solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pseudo SRAM Market.- Memory Solutions Inc.

- Advanced Embedded Systems

- Global Semiconductor Co.

- Integrated Memory Technologies

- Premier Chip Solutions

- Universal Memory Logic

- Secure Computing Elements

- Innovate Memory Devices

- Silicon Edge Solutions

- High-Performance Memory Co.

- Intelligent Storage Systems

- Quantum Memory Fabricators

- Next-Gen Embedded Devices

- Smart Memory Components

- Apex Integrated Solutions

- Worldwide Memory Corporation

- Frontier Embedded Solutions

- Core Memory Technologies

- Dynamic Solutions Inc.

- Precision Memory Group

Frequently Asked Questions

What is Pseudo SRAM (PSRAM) and how does it function?

Pseudo SRAM (PSRAM) is a type of volatile random-access memory that integrates a DRAM core with an SRAM-like interface, offering a blend of both technologies' advantages. It utilizes a DRAM cell structure for higher density and lower cost than true SRAM, but incorporates a refresh circuit on the chip, making it appear like SRAM to the system controller. This means the host processor does not need to manage refresh cycles, simplifying system design. PSRAM provides higher density than traditional SRAM and consumes significantly less power than DRAM, making it ideal for embedded applications requiring a balance of speed, cost-efficiency, and low power consumption, such as in mobile phones, IoT devices, and automotive systems.

What are the primary applications of Pseudo SRAM?

Pseudo SRAM finds its primary applications in a wide range of embedded systems where a balance of power efficiency, cost-effectiveness, and adequate speed is crucial. Key application areas include consumer electronics such as smartphones (for display buffering and as main memory in feature phones), wearables, and digital cameras. In the automotive sector, it is utilized in infotainment systems, instrument clusters, and Advanced Driver-Assistance Systems (ADAS). Industrial applications involve control systems and automation equipment, while IoT devices like smart sensors, gateways, and edge computing nodes benefit from its low-power characteristics for local data caching and buffering. Its versatility makes it a preferred choice for designs with strict power and space constraints.

How does Pseudo SRAM differ from other memory types like SRAM and DRAM?

Pseudo SRAM (PSRAM) distinguishes itself from Static RAM (SRAM) and Dynamic RAM (DRAM) through its unique architecture and performance characteristics. SRAM is faster and does not require refreshing, but it is expensive and has lower density due to its complex 6-transistor cell structure. DRAM offers the highest density and lowest cost per bit, but it is slower, consumes more power, and requires constant external refreshing by the host processor. PSRAM combines the density and lower cost of DRAM with an SRAM-like interface that includes an on-chip refresh controller, eliminating the need for external refresh. This makes PSRAM denser and more cost-effective than SRAM, while being simpler to integrate and more power-efficient than DRAM, fitting a crucial niche between the two.

What are the key advantages of using Pseudo SRAM in modern electronic designs?

The key advantages of Pseudo SRAM in modern electronic designs stem from its optimized balance of performance, power, and cost. Its primary benefits include lower power consumption compared to DRAM, which is vital for battery-powered devices like smartphones, wearables, and IoT sensors, extending their operational life. PSRAM offers higher density than traditional SRAM at a significantly lower cost, making it an economically viable choice for applications requiring moderate amounts of fast memory without the high price tag of true SRAM. Furthermore, its SRAM-like interface simplifies integration into system designs by offloading the refresh management from the host processor, reducing system complexity and speeding up development cycles. These attributes make it highly suitable for embedded applications where efficiency is paramount.

What is the future outlook for the Pseudo SRAM market?

The future outlook for the Pseudo SRAM market is robust, characterized by sustained growth driven by the ongoing proliferation of embedded systems and the increasing demand for power-efficient memory solutions. The market is expected to expand significantly, fueled by the continuous evolution of IoT, the rapid adoption of edge AI devices requiring efficient local data processing, and the advanced requirements of the automotive electronics sector. While facing competition from alternative memory technologies, PSRAM's unique combination of cost-effectiveness, power efficiency, and adequate speed ensures its continued relevance. Innovations in higher density and faster interfaces will be key to addressing the evolving needs of emerging applications, securing a promising long-term growth trajectory for the market.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted