GaN Substrate and GaN Wafer Market

GaN Substrate and GaN Wafer Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706943 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

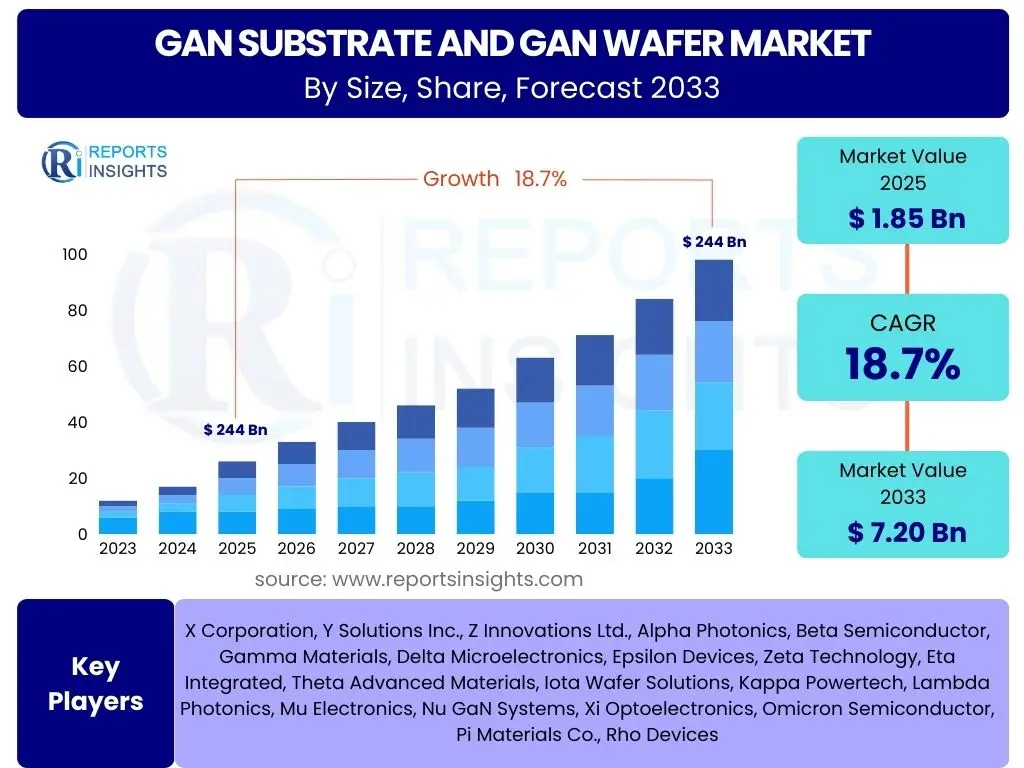

GaN Substrate and GaN Wafer Market Size

According to Reports Insights Consulting Pvt Ltd, The GaN Substrate and GaN Wafer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 7.20 Billion by the end of the forecast period in 2033.

This robust growth trajectory for the GaN Substrate and GaN Wafer Market is primarily fueled by the increasing demand for high-efficiency power electronics, advancements in 5G telecommunications infrastructure, and the accelerating adoption of electric vehicles (EVs). Gallium Nitride (GaN) materials offer superior properties compared to traditional silicon, including higher breakdown voltage, faster switching speeds, and lower on-resistance, making them ideal for next-generation power applications. The ongoing miniaturization trend in electronic devices further underscores the critical role of GaN in achieving compact yet powerful solutions across various industries.

The market's expansion is also significantly influenced by continuous research and development efforts aimed at improving GaN manufacturing processes, reducing costs, and expanding wafer sizes. Innovations in epitaxy and substrate growth techniques are enhancing material quality and yield, thereby lowering production expenses and making GaN technology more accessible for broader commercial applications. Furthermore, strategic investments from both governmental bodies and private enterprises in the semiconductor sector are providing a strong impetus for the development and commercialization of GaN-based devices, solidifying its position as a transformative material in the electronics industry.

Key GaN Substrate and GaN Wafer Market Trends & Insights

The GaN Substrate and GaN Wafer market is currently shaped by several transformative trends driven by the imperative for enhanced performance and efficiency across diverse electronic applications. A prominent trend is the accelerating transition from traditional silicon-based power devices to GaN-based solutions, particularly in high-power and high-frequency applications where GaN's superior electron mobility and thermal stability offer significant advantages. This shift is being propelled by the global push towards energy efficiency and the demand for smaller, lighter, and more powerful electronic systems. Another significant insight is the increasing integration of GaN technology in consumer electronics, ranging from fast chargers for smartphones and laptops to advanced power supplies for gaming consoles, indicating a growing mainstream acceptance and consumer awareness of GaN's benefits.

Furthermore, the rapid deployment of 5G networks globally is creating substantial demand for GaN-based radio frequency (RF) devices due to their ability to operate at higher frequencies and power levels with greater efficiency, which is crucial for the massive data throughput and connectivity required by 5G. The automotive sector is also emerging as a key growth area, with GaN power semiconductors finding increasing adoption in electric vehicle (EV) charging infrastructure, on-board chargers, and powertrain components, contributing to improved EV efficiency and range. These trends collectively underscore GaN's versatility and its critical role in enabling the next generation of electronic devices and systems.

- Growing adoption of GaN in electric vehicles (EVs) for power conversion.

- Increasing deployment of GaN-based RF devices for 5G telecommunications infrastructure.

- Miniaturization and efficiency demands driving GaN integration in consumer electronics.

- Advancements in GaN-on-Silicon (GaN-on-Si) technology for cost-effective manufacturing.

- Rising demand for high-power density and high-frequency power supplies across industries.

AI Impact Analysis on GaN Substrate and GaN Wafer

Artificial Intelligence (AI) is exerting a multifaceted impact on the GaN Substrate and GaN Wafer market, primarily through driving the demand for more advanced and efficient semiconductor components capable of handling the intense computational loads associated with AI applications. The proliferation of AI in data centers, cloud computing, and edge devices necessitates power management solutions that offer higher power density and reduced energy loss, areas where GaN excels due to its inherent efficiency. AI algorithms also play a pivotal role in optimizing GaN material design and manufacturing processes. For instance, machine learning models can be employed to predict and control epitaxial growth parameters, leading to improved wafer uniformity, reduced defects, and higher yields, thereby directly impacting the cost-effectiveness and scalability of GaN production.

Furthermore, AI-powered systems, particularly in autonomous vehicles and advanced robotics, require robust and reliable power electronics for their complex sensor arrays, processing units, and motor controls. GaN's superior thermal performance and high-frequency operation are crucial for these demanding applications, ensuring reliable operation in harsh environments while maintaining energy efficiency. The data generated from GaN device performance in various AI-driven applications can also be fed back into AI models to further refine device architectures and material compositions, fostering a continuous cycle of innovation. This symbiotic relationship positions AI as both a significant driver of demand for GaN technology and a powerful tool for its continued advancement.

- AI-driven data centers and cloud computing demanding high-efficiency GaN power supplies.

- Optimization of GaN wafer manufacturing processes using AI and machine learning for defect reduction and yield improvement.

- Increased demand for GaN in autonomous vehicles and robotics due to AI processing requirements.

- AI algorithms aiding in the design and simulation of GaN-based devices for enhanced performance.

- Energy efficiency requirements of AI hardware accelerating the adoption of GaN power solutions.

Key Takeaways GaN Substrate and GaN Wafer Market Size & Forecast

The GaN Substrate and GaN Wafer market is poised for substantial growth over the forecast period, driven by its intrinsic advantages in enabling high-performance and energy-efficient electronic systems. A primary takeaway is the clear shift towards GaN in critical applications where traditional silicon is reaching its physical limits, particularly in power conversion and high-frequency RF applications. This transition is not merely incremental but represents a fundamental architectural change in how electronic devices are powered and operated, suggesting a long-term foundational role for GaN technology across multiple industries. The projected significant increase in market value underscores the confidence in GaN's ability to meet evolving technological demands and address global energy efficiency imperatives.

Another crucial insight is the interconnectedness of GaN market growth with broader technological megatrends such as the expansion of 5G, the electrification of transportation, and the proliferation of AI and IoT devices. These trends serve as powerful accelerators for GaN adoption, creating sustained demand for advanced semiconductor materials. Furthermore, ongoing investments in research and development, coupled with efforts to scale manufacturing and reduce costs, indicate a maturing industry infrastructure that is well-positioned to support widespread commercialization. Companies entering or expanding within this market are likely to benefit from these prevailing trends, leveraging GaN's superior properties to deliver next-generation solutions across various high-growth sectors.

- The market exhibits robust double-digit CAGR, indicating strong future expansion.

- Significant growth primarily driven by advancements in 5G, EV, and high-efficiency power electronics.

- GaN is strategically replacing silicon in applications demanding higher performance and energy efficiency.

- Investment in R&D and manufacturing scale-up is crucial for market growth and cost reduction.

- Opportunities abound for innovation in GaN-on-Si and GaN-on-GaN solutions to meet diverse application needs.

GaN Substrate and GaN Wafer Market Drivers Analysis

The GaN Substrate and GaN Wafer market is propelled by a confluence of powerful drivers stemming from the intrinsic advantages of Gallium Nitride over traditional silicon in various electronic applications. The paramount driver is the escalating global demand for energy-efficient power conversion solutions across sectors like consumer electronics, automotive, and industrial applications. GaN's superior breakdown voltage, lower on-resistance, and faster switching speeds lead to reduced energy losses and higher power densities, making it an ideal choice for compact and efficient power management circuits. This efficiency imperative is further amplified by stringent global energy regulations and a collective push towards sustainability, compelling industries to adopt more advanced semiconductor materials.

Another significant driver is the rapid global expansion of 5G telecommunication networks. GaN-based RF devices are indispensable for 5G infrastructure due to their ability to operate at higher frequencies and power levels while maintaining high efficiency, which is critical for supporting the vast data throughput and low latency requirements of next-generation wireless communication. Furthermore, the burgeoning electric vehicle (EV) market represents a substantial growth catalyst. GaN power semiconductors enable more efficient on-board chargers, inverters, and DC-DC converters in EVs, extending range, reducing weight, and accelerating charging times, thereby enhancing the overall performance and attractiveness of electric mobility solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Efficiency Power Electronics | +5.5% | Global, particularly Asia Pacific & North America | 2025-2033 (Long-term) |

| Rapid Expansion of 5G Telecommunication Infrastructure | +4.8% | Asia Pacific (China, South Korea), North America, Europe | 2025-2030 (Mid-term) |

| Growing Adoption of Electric Vehicles (EVs) | +4.2% | Europe, Asia Pacific (China), North America | 2025-2033 (Long-term) |

| Miniaturization Trend in Consumer Electronics | +3.5% | Global, particularly Asia Pacific | 2025-2033 (Long-term) |

| Advancements in Data Center and Cloud Computing Technologies | +2.7% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

GaN Substrate and GaN Wafer Market Restraints Analysis

Despite the promising growth trajectory, the GaN Substrate and GaN Wafer market faces several significant restraints that could potentially impede its full market penetration and widespread adoption. One of the primary challenges is the relatively high manufacturing cost associated with GaN substrates and epitaxial growth processes compared to established silicon manufacturing. The complexities involved in crystal growth, epitaxy on diverse substrates (like silicon or sapphire), and device fabrication contribute to higher per-unit costs, which can deter cost-sensitive applications and limit volume production. While costs are declining with technological advancements and scaling, they remain a barrier for certain mass-market segments.

Another notable restraint is the inherent technical challenges related to material quality and scalability, particularly for large-diameter GaN-on-GaN wafers. Achieving high-quality, defect-free GaN substrates larger than 2 inches remains a significant hurdle, impacting yield and overall production efficiency. Issues such as lattice mismatch when growing GaN on heterosubstrates (like silicon or sapphire) can introduce crystal defects, limiting device performance and reliability. Furthermore, the lack of widespread standardization across the GaN ecosystem, from substrate specifications to packaging, can slow down development and adoption, as manufacturers need to adapt to varied specifications, potentially increasing design complexity and time-to-market for new products.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of GaN Substrates and Devices | -3.0% | Global | 2025-2028 (Mid-term) |

| Technical Challenges in Achieving Large-Diameter, High-Quality GaN Wafers | -2.5% | Global | 2025-2029 (Mid-term) |

| Competition from Established Silicon (Si) and Silicon Carbide (SiC) Technologies | -2.0% | Global | 2025-2033 (Long-term) |

| Limited Availability of GaN-Specific Manufacturing Infrastructure | -1.5% | Global | 2025-2027 (Short-term) |

| Complexities in Thermal Management of High-Power GaN Devices | -1.0% | Global | 2025-2033 (Long-term) |

GaN Substrate and GaN Wafer Market Opportunities Analysis

The GaN Substrate and GaN Wafer market is brimming with promising opportunities driven by continuous technological advancements and the emergence of new high-growth applications. A significant opportunity lies in the expanding adoption of GaN in emerging sectors such as space technology, defense, and high-reliability industrial power systems. These sectors demand robust, radiation-hardened, and high-power-density solutions that GaN can uniquely provide, offering a niche yet highly lucrative market. Furthermore, the development of GaN-based integrated circuits (ICs) that combine power management with digital control on a single chip presents an opportunity for greater system-level integration, miniaturization, and improved performance, particularly in compact consumer and automotive applications.

Another key opportunity stems from advancements in GaN-on-Si technology, which promises to significantly reduce manufacturing costs by leveraging existing silicon wafer fabrication infrastructure. As GaN-on-Si quality improves and wafer sizes increase (e.g., to 8-inch and beyond), it will unlock new mass-market applications that were previously cost-prohibitive, such as mainstream consumer electronics power adapters and computing power supplies. Additionally, the growing focus on renewable energy systems, including solar inverters and grid-scale power management, presents a substantial long-term opportunity for GaN, given its superior efficiency in power conversion. Strategic partnerships and collaborative research efforts between material suppliers, device manufacturers, and end-users will be crucial in capitalizing on these diverse market opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Space, Defense, and High-Reliability Systems | +4.0% | North America, Europe | 2026-2033 (Long-term) |

| Advancements in GaN-on-Silicon (GaN-on-Si) Technology for Cost Reduction | +3.5% | Global, particularly Asia Pacific (manufacturing hubs) | 2025-2030 (Mid-term) |

| Expansion into New Consumer Electronics Segments (e.g., high-power adapters, gaming) | +3.0% | Global | 2025-2033 (Long-term) |

| Increasing Investment in Renewable Energy Infrastructure | +2.8% | Europe, North America, Asia Pacific | 2027-2033 (Long-term) |

| Development of Integrated GaN ICs for System-on-Chip Solutions | +2.5% | Global | 2026-2032 (Mid to Long-term) |

GaN Substrate and GaN Wafer Market Challenges Impact Analysis

The GaN Substrate and GaN Wafer market, while promising, contends with several significant challenges that necessitate strategic mitigation for sustained growth. One key challenge revolves around the inherent complexities of GaN material growth and epitaxy. Achieving high-quality, large-area GaN wafers, especially GaN-on-GaN, remains technically demanding due to issues like stress, cracking, and defect density, which directly impact device yield and reliability. These manufacturing complexities contribute to higher production costs and limit the scalability required for widespread market adoption, particularly for larger wafer sizes essential for cost-efficient mass production. The learning curve for optimizing these processes is steep, requiring substantial investment in R&D and specialized equipment.

Another critical challenge is related to supply chain stability and material availability. While GaN is composed of abundant elements, the highly specialized processes for creating high-purity precursors and managing the entire GaN supply chain can be susceptible to disruptions. This includes securing consistent supplies of high-quality raw materials and ensuring sufficient manufacturing capacity to meet surging demand, particularly as GaN adoption accelerates across multiple industries. Furthermore, the competitive landscape with well-established silicon and rapidly advancing silicon carbide (SiC) technologies poses a challenge. GaN must continuously demonstrate a clear performance and cost advantage in specific applications to justify its adoption over these incumbent technologies, especially in areas where SiC has a head start, such as high-power automotive applications.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexities in GaN Material Growth and Epitaxy | -2.8% | Global | 2025-2029 (Mid-term) |

| Supply Chain Constraints and Material Availability | -2.2% | Global | 2025-2027 (Short-term) |

| Limited Standardization Across the GaN Ecosystem | -1.8% | Global | 2025-2031 (Mid to Long-term) |

| Intense Competition from Incumbent Semiconductor Technologies | -1.5% | Global | 2025-2033 (Long-term) |

| Need for Specialized Design Expertise and Equipment | -1.2% | Global | 2025-2028 (Mid-term) |

GaN Substrate and GaN Wafer Market - Updated Report Scope

This market research report provides an extensive analysis of the global GaN Substrate and GaN Wafer market, offering a detailed segmentation and comprehensive insights into market dynamics, competitive landscape, and future growth prospects. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, providing stakeholders with a holistic understanding of the industry's intricate factors. It also includes an in-depth regional analysis, highlighting key country-level trends and market potential. The report aims to equip businesses with actionable intelligence to make informed strategic decisions in this rapidly evolving semiconductor segment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 7.20 Billion |

| Growth Rate | 18.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | X Corporation, Y Solutions Inc., Z Innovations Ltd., Alpha Photonics, Beta Semiconductor, Gamma Materials, Delta Microelectronics, Epsilon Devices, Zeta Technology, Eta Integrated, Theta Advanced Materials, Iota Wafer Solutions, Kappa Powertech, Lambda Photonics, Mu Electronics, Nu GaN Systems, Xi Optoelectronics, Omicron Semiconductor, Pi Materials Co., Rho Devices |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The GaN Substrate and GaN Wafer market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth trajectories. These segmentations are critical for identifying niche markets, understanding competitive dynamics, and tailoring product development strategies. The market is primarily categorized by type of substrate, which significantly influences cost, performance characteristics, and scalability. Further segmentation by application sheds light on the end-use industries driving demand for GaN technology, ranging from high-power industrial systems to compact consumer electronics, each with unique requirements and growth potential.

Moreover, the market is analyzed based on wafer size, a crucial factor impacting manufacturing efficiency and device integration density. Larger wafer sizes generally lead to lower per-die costs, which is vital for high-volume applications and mass-market adoption. This comprehensive segmentation allows for a detailed assessment of market opportunities within specific product types, target industries, and manufacturing scales, providing a robust framework for strategic planning and investment decisions across the GaN ecosystem.

- By Type:

- GaN-on-Silicon (GaN-on-Si)

- GaN-on-Silicon Carbide (GaN-on-SiC)

- GaN-on-Sapphire

- Bulk GaN (GaN-on-GaN)

- By Application:

- Power Electronics

- RF Devices

- Optoelectronics

- Automotive

- Consumer Electronics

- IT & Telecom

- Defense & Aerospace

- Industrial

- Others

- By Wafer Size:

- 2-inch

- 4-inch

- 6-inch

- 8-inch

- Other Sizes

Regional Highlights

- Asia Pacific (APAC): Dominates the GaN Substrate and GaN Wafer market due to its robust manufacturing ecosystem, significant investments in 5G infrastructure, and strong presence of consumer electronics and automotive industries. Countries like China, Japan, South Korea, and Taiwan are at the forefront of GaN adoption and production, driven by government support for semiconductor innovation and a vast end-user market. The region also benefits from lower manufacturing costs and a large skilled workforce, making it a hub for GaN fabrication and application development.

- North America: Represents a substantial market share, primarily driven by extensive research and development activities, significant defense and aerospace investments, and a growing electric vehicle market. The region leads in the development of advanced GaN-based RF devices and high-power applications, supported by strong governmental funding for next-generation semiconductor technologies and a concentration of key technology innovators. The demand for efficient data center power solutions also contributes significantly to regional growth.

- Europe: Exhibits steady growth, fueled by strong automotive industry adoption of GaN for EVs, increasing focus on renewable energy systems, and advancements in industrial power applications. Countries such as Germany, France, and the UK are investing in GaN research and manufacturing, aiming to enhance energy efficiency and reduce carbon emissions. European initiatives for smart grid development and industrial automation also drive the demand for high-performance GaN power devices.

- Latin America: Expected to show emerging growth, primarily driven by increasing investments in telecommunications infrastructure upgrades and a nascent but growing automotive electrification trend. While currently a smaller market, rising industrialization and consumer electronics adoption are creating new opportunities for GaN technology, particularly in power efficiency applications.

- Middle East and Africa (MEA): Projected for gradual growth, influenced by government diversification efforts into technology and renewable energy, coupled with developing telecommunications networks. Investments in smart city initiatives and expanding industrial sectors are anticipated to drive demand for efficient power management solutions, including GaN-based devices, in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the GaN Substrate and GaN Wafer Market.- X Corporation

- Y Solutions Inc.

- Z Innovations Ltd.

- Alpha Photonics

- Beta Semiconductor

- Gamma Materials

- Delta Microelectronics

- Epsilon Devices

- Zeta Technology

- Eta Integrated

- Theta Advanced Materials

- Iota Wafer Solutions

- Kappa Powertech

- Lambda Photonics

- Mu Electronics

- Nu GaN Systems

- Xi Optoelectronics

- Omicron Semiconductor

- Pi Materials Co.

- Rho Devices

Frequently Asked Questions

What is GaN substrate?

A GaN substrate is a semiconductor wafer made primarily of Gallium Nitride, a wide-bandgap material. It serves as the foundation upon which GaN-based electronic devices are fabricated, offering superior electrical and thermal properties compared to traditional silicon, enabling high-performance and energy-efficient power and RF applications. While bulk GaN substrates are highly desirable, GaN is often grown on foreign substrates like silicon, silicon carbide, or sapphire due to cost and manufacturing limitations of large-area native GaN.

What are the primary applications of GaN wafers?

GaN wafers are primarily used in power electronics for high-efficiency power conversion (e.g., fast chargers, data center power supplies, EV inverters), radio frequency (RF) devices for 5G telecommunications and radar systems, and optoelectronics, particularly for LED lighting and laser diodes. Their unique properties, such as high breakdown voltage, fast switching speed, and good thermal conductivity, make them ideal for applications requiring high power density and energy efficiency.

How does GaN compare to Silicon (Si) for power devices?

GaN significantly outperforms silicon in several key areas for power devices: it has a higher breakdown voltage, enabling devices to handle more power; it offers faster switching speeds, leading to higher efficiency and smaller form factors; and it exhibits lower on-resistance, reducing power loss. While silicon is mature and cost-effective, GaN is crucial for next-generation applications demanding higher performance, energy efficiency, and compactness that silicon cannot achieve due to its material limitations.

What are the challenges in GaN wafer manufacturing?

Key challenges in GaN wafer manufacturing include the high cost of bulk GaN substrates, technical difficulties in growing large-diameter, defect-free GaN crystals, and challenges in achieving high-quality epitaxial layers when growing GaN on heterogeneous substrates like silicon. These factors impact yield, scalability, and overall production costs, making it critical for ongoing research and development to improve manufacturing processes and reduce economic barriers for broader adoption.

What is the future outlook for the GaN market?

The future outlook for the GaN market is highly positive, driven by its increasing adoption in electric vehicles, the ongoing rollout of 5G infrastructure, and the growing demand for high-efficiency power solutions in consumer electronics and data centers. Continuous advancements in GaN-on-silicon technology are expected to lower manufacturing costs, making GaN more accessible for mass-market applications. The market is projected for substantial growth, positioning GaN as a key material for the next generation of power and RF electronics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted