Ophthalmic Device Market

Ophthalmic Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705955 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

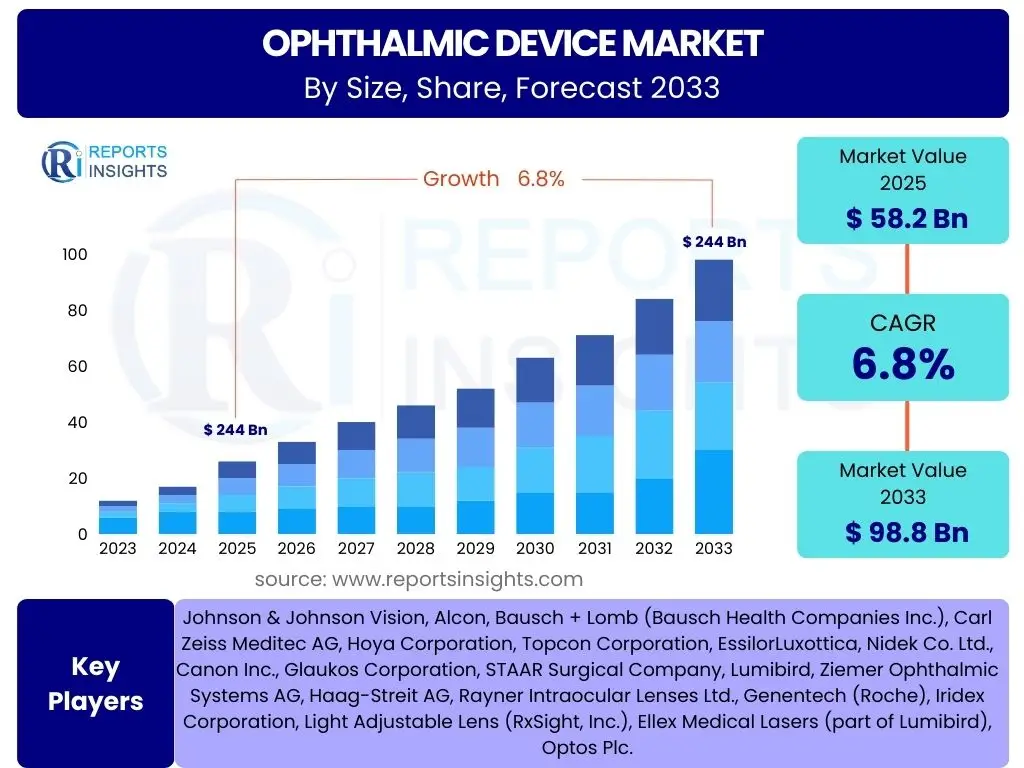

Ophthalmic Device Market Size

According to Reports Insights Consulting Pvt Ltd, The Ophthalmic Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 58.2 Billion in 2025 and is projected to reach USD 98.8 Billion by the end of the forecast period in 2033.

The sustained growth in the ophthalmic device market is primarily attributed to the escalating global prevalence of chronic eye conditions such as cataracts, glaucoma, diabetic retinopathy, and macular degeneration. These conditions are increasingly common among the aging population, a demographic segment experiencing significant growth worldwide. Furthermore, advancements in diagnostic and surgical technologies, coupled with rising healthcare expenditure in both developed and emerging economies, are fueling market expansion by enabling earlier detection and more effective treatment options.

Investments in research and development by key market players are leading to the introduction of innovative products, including advanced intraocular lenses, sophisticated diagnostic imaging systems, and minimally invasive surgical instruments. These innovations are not only improving patient outcomes but also expanding the addressable market by offering solutions for previously untreatable or poorly managed conditions. The increasing adoption of digital health solutions, such as telemedicine for remote eye care, further contributes to market growth by enhancing accessibility and convenience of ophthalmic services, especially in underserved areas.

Key Ophthalmic Device Market Trends & Insights

The ophthalmic device market is currently undergoing transformative changes, driven by a confluence of technological advancements, evolving patient demographics, and shifts in healthcare delivery models. Users frequently inquire about the integration of artificial intelligence and machine learning in diagnostics, the rise of personalized ophthalmology, and the impact of minimally invasive surgical techniques. There is also significant interest in how increasing awareness about eye health and the expansion of digital health platforms are shaping the market landscape. These inquiries highlight a collective focus on innovations that promise improved accuracy, efficiency, and patient outcomes in eye care.

Another prominent area of interest revolves around the increasing demand for refractive error correction devices and premium intraocular lenses, reflecting a growing consumer willingness to invest in vision enhancement. Furthermore, the market is witnessing a trend towards combination therapies and multifunctional devices that offer comprehensive solutions for various ophthalmic conditions, aiming to simplify procedures and reduce recovery times. The push for cost-effective solutions and the expansion of eye care infrastructure in developing regions are also critical trends that will significantly influence market dynamics over the forecast period.

- Technological integration: AI and machine learning for enhanced diagnostics and personalized treatment.

- Minimally invasive surgical techniques: Growing preference for procedures offering faster recovery and reduced trauma.

- Premium intraocular lenses (IOLs): Increased adoption for improved visual outcomes post-cataract surgery.

- Telemedicine and remote eye care: Expansion of digital platforms for consultations and monitoring, especially in remote areas.

- Personalized ophthalmology: Tailored treatment approaches based on individual patient characteristics.

- Focus on early detection: Development of advanced diagnostic tools for conditions like glaucoma and diabetic retinopathy.

- Consolidation and strategic partnerships: Mergers and acquisitions to strengthen market positions and expand product portfolios.

AI Impact Analysis on Ophthalmic Device

The integration of Artificial Intelligence (AI) is profoundly transforming the ophthalmic device market, addressing common user questions related to diagnostic accuracy, predictive analytics, and operational efficiency. Users are keenly interested in how AI can enhance the detection of subtle pathological changes, leading to earlier and more precise diagnoses of conditions such as diabetic retinopathy, glaucoma, and age-related macular degeneration. The expectation is that AI-powered algorithms will significantly reduce diagnostic errors and reduce the burden on ophthalmologists, enabling them to handle a larger patient volume with greater accuracy. This technological shift is also viewed as a crucial step towards proactive eye health management, moving beyond reactive treatment paradigms.

Furthermore, AI's influence extends to surgical planning and execution, with queries focusing on AI-assisted robotic surgeries and image-guided interventions that promise enhanced precision and reduced procedural risks. Concerns often revolve around data privacy, the validation of AI models, and the potential impact on the role of human clinicians. However, the overarching expectation is that AI will augment, rather than replace, human expertise, fostering a new era of personalized and highly effective ophthalmic care. The ability of AI to analyze vast datasets also presents opportunities for drug discovery and the development of novel therapeutic strategies, promising a future where eye diseases are managed with unprecedented efficacy.

- Enhanced Diagnostic Accuracy: AI algorithms analyze retinal scans (OCT, fundus photos) for early detection of diseases like glaucoma, diabetic retinopathy, and AMD, often surpassing human capabilities in subtle anomaly identification.

- Predictive Analytics: AI models can predict disease progression and treatment response, allowing for personalized treatment plans and proactive interventions.

- Optimized Surgical Planning: AI assists in pre-operative planning for cataract and refractive surgeries, ensuring precise lens placement and optimizing surgical parameters.

- Robotics in Surgery: AI-powered robotic systems offer superior precision in delicate ophthalmic procedures, minimizing invasiveness and improving outcomes.

- Teleophthalmology Expansion: AI facilitates remote screening and monitoring by automating image analysis, making eye care more accessible, especially in underserved regions.

- Drug Discovery and Development: AI accelerates the identification of potential drug candidates and optimizes clinical trial designs for ophthalmic pharmaceuticals.

- Operational Efficiency: AI streamlines clinic workflows, from appointment scheduling to inventory management, improving overall productivity.

Key Takeaways Ophthalmic Device Market Size & Forecast

The ophthalmic device market is poised for robust expansion, driven by an aging global population and the increasing incidence of chronic eye diseases, representing a significant opportunity for stakeholders. Users often inquire about the primary drivers sustaining this growth, the most lucrative segments, and the potential impact of disruptive technologies. The market's upward trajectory is firmly supported by continuous innovation in diagnostic and surgical technologies, which are improving treatment efficacy and accessibility, thereby expanding the patient base seeking advanced eye care solutions. The forecast indicates that investing in R&D for next-generation devices will be paramount for market leadership.

Another key takeaway is the increasing importance of emerging economies as growth engines, fueled by improving healthcare infrastructure and rising disposable incomes. While established markets continue to innovate and adopt advanced therapies, regions such as Asia Pacific and Latin America offer significant untapped potential. The market also highlights the critical role of digital health solutions, including telemedicine and AI-powered diagnostics, in revolutionizing service delivery and reaching a broader demographic. Companies prioritizing patient-centric solutions, technological integration, and strategic market penetration in these high-growth areas are best positioned to capitalize on the forecast growth.

- Strong Growth Trajectory: Market projected to reach USD 98.8 Billion by 2033, driven by demographic shifts and disease prevalence.

- Innovation as a Core Driver: Continuous R&D in diagnostics, surgical tools, and premium IOLs is fueling market expansion and improving patient outcomes.

- Aging Population Impact: The global increase in elderly individuals is a primary factor behind the rising demand for cataract, glaucoma, and AMD treatments.

- Emerging Market Potential: Asia Pacific and Latin America are expected to be key growth regions due to improving healthcare access and economic development.

- Digital Transformation: Telemedicine, AI, and connected devices are reshaping eye care delivery, enhancing accessibility and efficiency.

- Shift to Minimally Invasive Procedures: Growing preference for advanced surgical techniques that offer faster recovery and reduced complications.

- Strategic Partnerships: Collaborations and M&A activities are crucial for consolidating market share and expanding product portfolios.

Ophthalmic Device Market Drivers Analysis

The ophthalmic device market is primarily driven by the escalating global prevalence of chronic eye conditions. As populations age, the incidence of diseases such as cataracts, glaucoma, and age-related macular degeneration (AMD) significantly increases, directly driving the demand for diagnostic tools, surgical instruments, and vision correction devices. This demographic shift represents a foundational and sustained impetus for market growth, requiring continuous innovation in treatment modalities and accessible diagnostic solutions worldwide. The focus on early detection and intervention for these prevalent conditions is further accelerating the adoption of advanced ophthalmic technologies.

Technological advancements also serve as a crucial driver, with continuous innovation leading to more precise, less invasive, and more effective diagnostic and therapeutic devices. The development of advanced intraocular lenses, high-resolution imaging systems, and sophisticated laser-assisted surgical tools is enhancing patient outcomes and expanding the scope of treatable conditions. These innovations not only improve the quality of care but also create new market segments and drive upgrades in existing ophthalmic practices. Furthermore, increasing healthcare expenditure and growing awareness regarding eye health are contributing factors, empowering more individuals to seek professional eye care and adopt preventive measures.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Eye Diseases | +2.5% | Global (Aging Populations, Diabetic Epidemics) | 2025-2033 (Long-term) |

| Aging Global Population | +2.0% | North America, Europe, Asia Pacific (e.g., Japan, China) | 2025-2033 (Sustained) |

| Technological Advancements in Devices | +1.5% | Global (Key innovation hubs: US, Germany, Japan) | 2025-2033 (Continuous) |

| Rising Healthcare Expenditure & Awareness | +0.8% | Emerging Economies (e.g., China, India, Brazil), Developed Markets | 2025-2033 (Medium-term) |

| Growing Demand for Refractive Error Correction | +0.5% | North America, Europe, Asia Pacific | 2025-2033 (Medium-term) |

Ophthalmic Device Market Restraints Analysis

Despite the robust growth potential, the ophthalmic device market faces several significant restraints. One major challenge is the high cost associated with advanced ophthalmic devices and surgical procedures. This often limits access to state-of-the-art treatments, particularly in low-income and developing regions, where healthcare budgets are constrained and reimbursement policies may be inadequate. The high initial investment required for sophisticated equipment and the ongoing maintenance costs can deter smaller clinics and hospitals from adopting the latest technologies, thereby slowing market penetration and widespread access.

Furthermore, stringent regulatory approval processes impose considerable hurdles for market entry and product innovation. Devices must undergo rigorous testing and clinical trials to ensure safety and efficacy, leading to lengthy approval timelines and substantial R&D expenses. This regulatory complexity can delay the introduction of new products to the market, stifling innovation and increasing the financial burden on manufacturers. Additionally, the shortage of skilled ophthalmologists and trained technicians, particularly in rural and underserved areas, presents a significant restraint as it directly impacts the capacity for diagnosis and treatment delivery, irrespective of device availability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Devices & Procedures | -1.2% | Emerging Markets, Public Healthcare Systems Globally | 2025-2033 (Sustained) |

| Stringent Regulatory Approval Processes | -0.8% | North America (FDA), Europe (MDR), Japan | 2025-2030 (Medium-term) |

| Lack of Skilled Ophthalmologists & Technicians | -0.7% | Developing Regions, Rural Areas Globally | 2025-2033 (Long-term) |

| Product Recalls & Safety Concerns | -0.5% | Global (Affecting consumer trust) | 2025-2028 (Short-term, Event-driven) |

Ophthalmic Device Market Opportunities Analysis

Significant opportunities in the ophthalmic device market stem from the vast untapped potential in emerging economies. Regions like Asia Pacific, Latin America, and parts of Africa are witnessing rapid economic development, improving healthcare infrastructure, and a growing middle class with increasing disposable incomes. These factors are translating into a greater demand for advanced medical care, including ophthalmic treatments. Manufacturers focusing on cost-effective, yet high-quality, solutions tailored to the specific needs and economic realities of these regions can unlock substantial market expansion. Initiatives to expand access to eye care through government programs and public-private partnerships further amplify these opportunities.

Another major opportunity lies in the continued integration of digital health and Artificial Intelligence (AI) into ophthalmic practices. The proliferation of telemedicine platforms for remote consultations and diagnostic screenings, coupled with AI-powered analytics for early disease detection and personalized treatment, presents avenues for significantly enhancing accessibility and efficiency in eye care. Furthermore, the increasing focus on personalized medicine and customized ophthalmic solutions, particularly in the premium intraocular lens segment, offers a lucrative opportunity for innovation. Developing devices that cater to individual patient needs and optimize visual outcomes will drive adoption and command higher market value. The rise of multi-modal diagnostic devices that combine several imaging technologies into a single unit also represents a significant opportunity by streamlining workflows and improving diagnostic accuracy.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Markets | +1.5% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 (Long-term) |

| Integration of AI & Digital Health Solutions | +1.2% | Global (particularly developed nations for R&D) | 2025-2033 (Continuous) |

| Personalized Medicine & Premium IOLs | +0.9% | North America, Europe, Asia Pacific (High-income segments) | 2025-2033 (Medium-term) |

| Development of Home-Use Diagnostic Devices | +0.6% | Global (Post-pandemic shift to remote care) | 2025-2030 (Medium-term) |

Ophthalmic Device Market Challenges Impact Analysis

The ophthalmic device market, while experiencing significant growth, is not immune to a range of challenges that could impede its progress. Intense market competition among established players and emerging innovators leads to pricing pressures and necessitates continuous investment in research and development to maintain a competitive edge. This competitive landscape can make it difficult for new entrants to gain traction and for smaller companies to sustain profitability, fostering an environment of consolidation and strategic alliances.

Furthermore, disruptions in global supply chains, exemplified by recent events, pose a significant challenge. Reliance on specific raw materials, electronic components, and manufacturing hubs can make the production and distribution of ophthalmic devices vulnerable to geopolitical tensions, natural disasters, and pandemics. Such disruptions can lead to delays in product delivery, increased manufacturing costs, and ultimately, higher prices for end-users. Additionally, ensuring data security and privacy in an increasingly digitized healthcare landscape presents an ongoing challenge, as ophthalmic devices collect sensitive patient information that must be protected against cyber threats and unauthorized access, demanding robust cybersecurity measures and compliance with evolving regulations like GDPR and HIPAA.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Pricing Pressures | -0.9% | Global (Especially in mature markets) | 2025-2033 (Sustained) |

| Supply Chain Disruptions & Raw Material Volatility | -0.7% | Global (Impact on manufacturing and distribution) | 2025-2028 (Short-to-medium term) |

| Data Security & Privacy Concerns | -0.6% | Global (Especially in regions with strict data regulations) | 2025-2033 (Continuous) |

| Reimbursement Uncertainties & Policy Changes | -0.5% | North America, Europe (Influences adoption rates) | 2025-2030 (Medium-term) |

Ophthalmic Device Market - Updated Report Scope

This comprehensive market research report on the Ophthalmic Device Market offers an in-depth analysis of market size, trends, drivers, restraints, and opportunities, providing a strategic overview for stakeholders. The scope encompasses detailed segmentation across various product types, applications, and end-users, reflecting the diverse landscape of the ophthalmic industry. It leverages historical data to provide accurate forecasts, enabling businesses to make informed decisions and identify high-growth areas. The report also highlights key competitive dynamics and profiles leading players, offering insights into their strategies and market positioning, critical for understanding the evolving competitive environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 58.2 Billion |

| Market Forecast in 2033 | USD 98.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Johnson & Johnson Vision, Alcon, Bausch + Lomb (Bausch Health Companies Inc.), Carl Zeiss Meditec AG, Hoya Corporation, Topcon Corporation, EssilorLuxottica, Nidek Co. Ltd., Canon Inc., Glaukos Corporation, STAAR Surgical Company, Lumibird, Ziemer Ophthalmic Systems AG, Haag-Streit AG, Rayner Intraocular Lenses Ltd., Genentech (Roche), Iridex Corporation, Light Adjustable Lens (RxSight, Inc.), Ellex Medical Lasers (part of Lumibird), Optos Plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ophthalmic device market is meticulously segmented to provide a granular understanding of its diverse components and growth avenues. This segmentation by product type, application, and end-user allows for a detailed analysis of specific market dynamics, technological preferences, and demand patterns across different therapeutic areas and care settings. Understanding these segments is crucial for identifying key growth drivers, niche opportunities, and strategic investment areas within the broader ophthalmic industry. For instance, the surgical devices segment, driven by the increasing volume of cataract and refractive surgeries, continues to dominate due to constant innovation and the rising prevalence of age-related eye conditions, whereas the diagnostic and monitoring devices segment is experiencing rapid growth fueled by advancements in early detection technologies like OCT and AI-powered diagnostic platforms.

Within product types, vision care devices, including contact lenses and spectacles, represent a significant consumer-driven segment, while surgical and diagnostic devices are largely propelled by clinical demand and technological breakthroughs. Application-based segmentation highlights the impact of specific eye diseases on device demand, with cataract and glaucoma treatments consistently driving a substantial portion of the market. The end-user analysis provides insights into where these devices are primarily utilized, with hospitals and specialized ophthalmic clinics being major consumers, reflecting the infrastructure required for complex procedures and diagnostics. This multi-faceted segmentation helps to delineate the most promising avenues for market penetration and product development, enabling manufacturers to tailor their strategies to specific market needs and optimize resource allocation for maximum impact.

- By Product Type:

- Vision Care Devices

- Surgical Devices

- Diagnostic and Monitoring Devices

- By Application:

- Cataract Treatment

- Glaucoma Treatment

- Refractive Error Correction

- Diabetic Retinopathy Treatment

- Age-related Macular Degeneration (AMD) Treatment

- Dry Eye Syndrome

- Others

- By End User:

- Hospitals

- Ophthalmic Clinics

- Ambulatory Surgical Centers

- Optical Shops

- Research & Academic Institutes

Regional Highlights

The global ophthalmic device market exhibits distinct regional dynamics, influenced by varying demographic trends, healthcare expenditures, technological adoption rates, and regulatory landscapes. North America and Europe represent mature markets characterized by advanced healthcare infrastructure, high awareness of eye health, and significant R&D investments, driving the adoption of premium and innovative devices. These regions are also early adopters of AI and telemedicine in ophthalmology, shaping global trends. Asia Pacific, on the other hand, is rapidly emerging as the fastest-growing market, propelled by its large and aging population, increasing prevalence of eye diseases, improving economic conditions, and expanding access to healthcare services, particularly in countries like China and India. Latin America, the Middle East, and Africa are also expected to witness substantial growth, albeit from a lower base, as healthcare infrastructure develops and awareness campaigns gain traction.

- North America: Dominates the market share due to high healthcare expenditure, significant R&D activities, early adoption of advanced technologies, and a large aging population. The U.S. remains a key market.

- Europe: A mature market characterized by robust healthcare systems, favorable reimbursement policies, and a strong presence of key market players. Germany, France, and the UK are leading contributors.

- Asia Pacific (APAC): Expected to be the fastest-growing region, driven by its vast population, increasing disposable incomes, improving healthcare infrastructure, and rising prevalence of eye disorders, particularly in China and India.

- Latin America: Showing promising growth due to increasing healthcare investments, rising awareness of eye health, and expanding medical tourism. Brazil and Mexico are key markets.

- Middle East and Africa (MEA): Growth is fueled by increasing government initiatives to improve healthcare facilities, rising prevalence of chronic diseases, and growing medical tourism in certain countries like UAE and Saudi Arabia.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ophthalmic Device Market.- Johnson & Johnson Vision

- Alcon

- Bausch + Lomb (Bausch Health Companies Inc.)

- Carl Zeiss Meditec AG

- Hoya Corporation

- Topcon Corporation

- EssilorLuxottica

- Nidek Co. Ltd.

- Canon Inc.

- Glaukos Corporation

- STAAR Surgical Company

- Lumibird

- Ziemer Ophthalmic Systems AG

- Haag-Streit AG

- Rayner Intraocular Lenses Ltd.

- Genentech (Roche)

- Iridex Corporation

- Light Adjustable Lens (RxSight, Inc.)

- Ellex Medical Lasers (part of Lumibird)

- Optos Plc.

Frequently Asked Questions

What is the projected growth rate of the Ophthalmic Device Market?

The Ophthalmic Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This growth is primarily driven by an aging global population and the increasing prevalence of various eye conditions.

How is AI impacting the Ophthalmic Device Market?

AI is significantly impacting the ophthalmic device market by enhancing diagnostic accuracy for conditions like diabetic retinopathy and glaucoma, enabling more precise surgical planning, and expanding remote eye care through telemedicine platforms. AI also aids in predictive analytics for disease progression and personalized treatment.

Which product types are driving market growth?

Surgical devices, particularly those for cataract and refractive surgeries, along with advanced diagnostic and monitoring devices such as Optical Coherence Tomography (OCT) systems, are key drivers of market growth due to continuous technological advancements and increasing adoption rates.

What are the main opportunities in the Ophthalmic Device Market?

Key opportunities include expansion into emerging markets, further integration of AI and digital health solutions, the growing demand for personalized medicine and premium intraocular lenses, and the development of innovative home-use diagnostic devices for increased accessibility.

What are the primary challenges facing the market?

The market faces challenges such as the high cost of advanced devices, stringent regulatory approval processes, intense market competition leading to pricing pressures, and the ongoing need to address data security and privacy concerns in digital health solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted