Surgical Stapling Device Market

Surgical Stapling Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704902 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

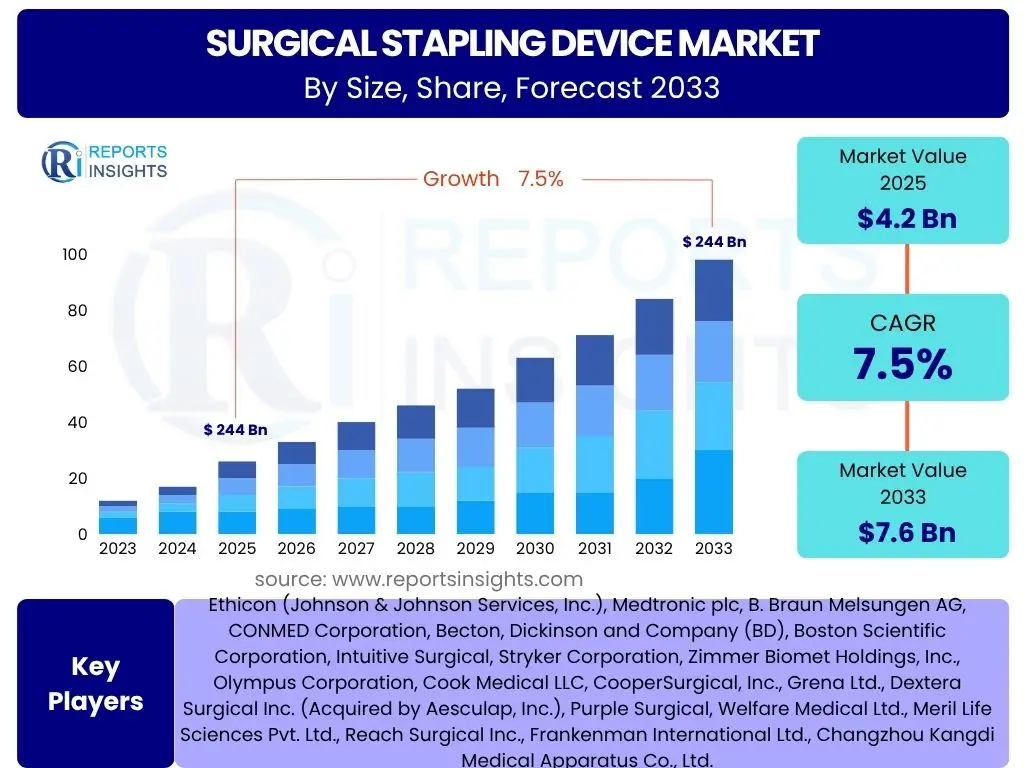

Surgical Stapling Device Market Size

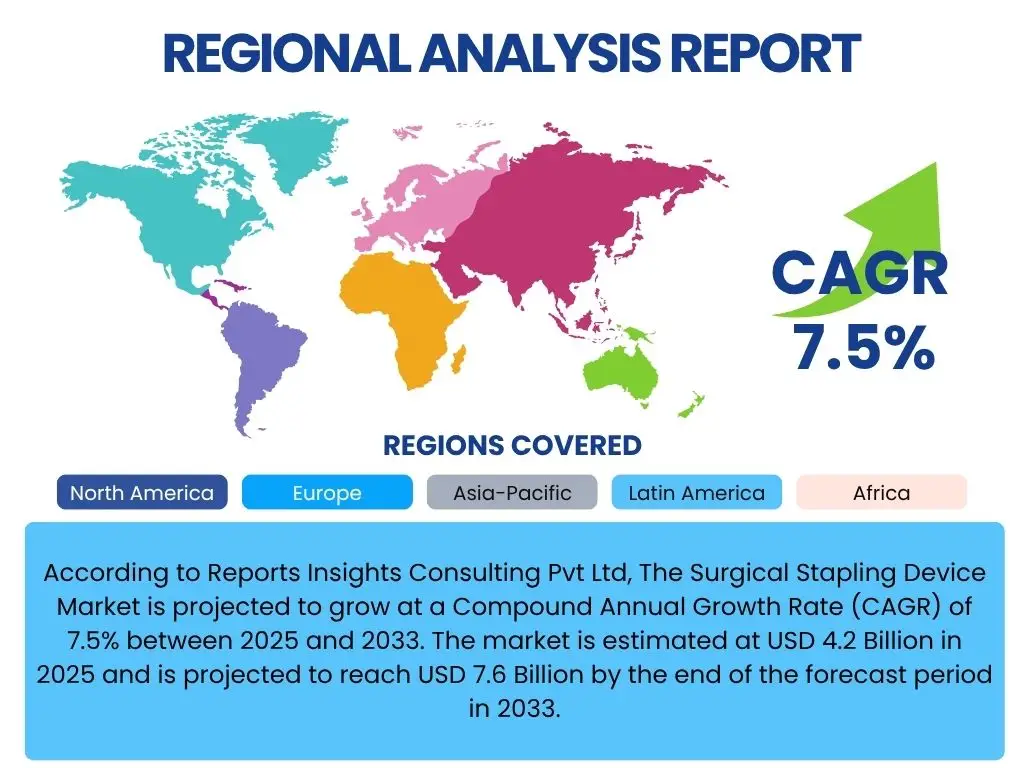

According to Reports Insights Consulting Pvt Ltd, The Surgical Stapling Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 4.2 Billion in 2025 and is projected to reach USD 7.6 Billion by the end of the forecast period in 2033.

Key Surgical Stapling Device Market Trends & Insights

The Surgical Stapling Device market is witnessing dynamic shifts driven by advancements in surgical techniques and a growing emphasis on patient outcomes. Key user inquiries often revolve around the evolution of stapling technology, the impact of minimally invasive procedures, and the demand for enhanced safety features. Insights indicate a strong market pull towards devices that offer greater precision, reduced tissue trauma, and improved ergonomics for surgeons.

Technological innovation continues to be a central theme, with product development focusing on smart features, better visualization, and integration with robotic surgical systems. The market is also experiencing a heightened awareness regarding the cost-effectiveness and efficiency of single-use devices, balanced against environmental sustainability concerns. These trends collectively shape the landscape, pushing manufacturers to innovate while addressing clinical needs and economic pressures.

- Increasing adoption of minimally invasive surgical (MIS) procedures across various specialties.

- Development and integration of powered and smart stapling devices offering enhanced precision and control.

- Growing demand for single-use surgical staplers to reduce infection risks and streamline sterilization processes.

- Emphasis on advanced tissue management capabilities and reduced post-operative complications.

- Expansion of ambulatory surgical centers (ASCs) driving demand for cost-effective and efficient stapling solutions.

- Rising prevalence of chronic diseases necessitating surgical interventions, such as bariatric and colorectal surgeries.

- Focus on improved ergonomics and user-friendliness in stapler design for surgical professionals.

AI Impact Analysis on Surgical Stapling Device

Common user questions regarding AI's impact on surgical stapling devices center on how artificial intelligence can enhance precision, minimize errors, and automate certain aspects of surgical procedures. Users are also keen to understand the potential for AI to integrate with existing robotic platforms, provide real-time feedback, and improve patient safety through data-driven insights. The general expectation is that AI will revolutionize the surgical workflow, making stapling more predictable and efficacious.

The integration of AI into surgical stapling devices is anticipated to lead to more sophisticated instruments capable of performing complex tasks with greater accuracy. This includes predictive analytics for optimal staple line formation, real-time tissue recognition, and adaptive firing mechanisms. While still in nascent stages, the long-term impact of AI is projected to extend to training, procedural planning, and post-operative analysis, thereby optimizing clinical outcomes and standardizing surgical excellence.

- Enhanced precision and consistency through AI-guided staple placement and firing.

- Real-time feedback systems for surgeons, optimizing tissue compression and staple line integrity.

- Integration with robotic surgical platforms for automated or augmented stapling procedures.

- Predictive analytics to identify potential complications during or after stapling based on tissue properties.

- AI-driven training simulations for surgical residents, improving proficiency with stapling devices.

Key Takeaways Surgical Stapling Device Market Size & Forecast

Insights derived from analyzing common user inquiries about the Surgical Stapling Device market size and forecast reveal a strong interest in understanding the core growth drivers and the long-term potential of the sector. Users frequently seek information on the factors contributing to market expansion, such as increasing surgical volumes and technological innovations, as well as critical market indicators like the projected CAGR and estimated market valuation over the forecast period. The emphasis is on identifying the most impactful trends and strategic areas for investment or development.

The market is poised for robust growth, primarily fueled by the global increase in surgical procedures, an aging population, and the escalating demand for minimally invasive techniques. Technological advancements in powered and smart stapling devices are significant contributors to this growth, promising enhanced patient safety and surgical efficiency. Furthermore, the expansion into emerging economies presents substantial untapped opportunities, making the market a dynamic and attractive landscape for innovation and investment.

- The market is set for substantial growth, driven by increasing global surgical procedure volumes and technological advancements.

- Minimally invasive surgery adoption is a primary catalyst, favoring innovative stapling solutions.

- Powered and smart stapling devices are emerging as key product segments, offering superior precision and control.

- Asia Pacific and other developing regions are expected to exhibit the highest growth rates due to improving healthcare infrastructure and patient affordability.

- Product innovation focusing on patient safety, reduced complications, and improved ergonomics will be crucial for competitive advantage.

Surgical Stapling Device Market Drivers Analysis

The Surgical Stapling Device market is significantly propelled by several key factors that collectively contribute to its robust expansion. A major driver is the global increase in the number of surgical procedures performed annually, driven by the rising prevalence of chronic diseases such as obesity, cancer, and cardiovascular conditions. This surge in surgical interventions directly correlates with a higher demand for efficient and reliable wound closure devices like surgical staplers.

Furthermore, the growing preference for minimally invasive surgical (MIS) techniques, which often necessitate specialized stapling devices for precise internal closure, acts as a strong market accelerator. Advancements in stapling technology, including the development of powered, smart, and endoscopic staplers, also play a crucial role by offering enhanced precision, safety, and reduced post-operative complications, thereby encouraging their wider adoption by surgeons and healthcare facilities worldwide.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Surgical Procedures Globally | +1.2% | Global, particularly North America, Europe, Asia Pacific | Short-term (2025-2028) & Mid-term (2028-2031) |

| Growing Adoption of Minimally Invasive Surgery | +1.0% | North America, Europe, Developed Asia Pacific | Short-term (2025-2028) & Long-term (2031-2033) |

| Technological Advancements in Stapling Devices | +0.8% | Global, particularly developed economies | Mid-term (2028-2031) & Long-term (2031-2033) |

| Rising Prevalence of Chronic Diseases | +0.7% | Global | Short-term (2025-2028) |

| Aging Global Population | +0.6% | Europe, North America, Japan, China | Long-term (2031-2033) |

Surgical Stapling Device Market Restraints Analysis

Despite robust growth prospects, the Surgical Stapling Device market faces certain restraints that could impede its full potential. A significant challenge is the high cost associated with advanced and technologically sophisticated surgical staplers, especially powered and smart devices. This high cost can limit adoption in healthcare settings with budget constraints, particularly in developing regions, and may encourage the continued use of traditional methods or reusable instruments despite their potential drawbacks.

Another notable restraint includes the stringent regulatory approval processes for new medical devices, which can lead to lengthy and costly development cycles. Furthermore, concerns regarding product recalls due to manufacturing defects or performance issues can erode surgeon confidence and impact market uptake. The availability of alternative wound closure methods, such as sutures and sealants, also presents a competitive pressure, as these options may be preferred in certain clinical scenarios or due to cost considerations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Devices | -0.9% | Developing Economies, Budget-Constrained Healthcare Systems | Short-term (2025-2028) & Mid-term (2028-2031) |

| Stringent Regulatory Landscape | -0.7% | North America, Europe | Short-term (2025-2028) |

| Product Recalls and Safety Concerns | -0.6% | Global | Short-term (2025-2028) |

| Availability of Alternative Wound Closure Methods | -0.5% | Global | Mid-term (2028-2031) |

Surgical Stapling Device Market Opportunities Analysis

The Surgical Stapling Device market is abundant with opportunities that can fuel significant growth and innovation. One major opportunity lies in the untapped potential of emerging markets, particularly in Asia Pacific, Latin America, and parts of Africa. These regions are witnessing rapid improvements in healthcare infrastructure, increasing healthcare expenditure, and a growing patient base, which collectively create a fertile ground for the adoption of advanced surgical devices.

Another significant opportunity is the continuous innovation in product development, focusing on smart, AI-integrated, and robotic-assisted staplers. The drive towards personalized medicine and patient-specific surgical solutions also opens new avenues for specialized stapling devices tailored to unique anatomical requirements. Furthermore, the expansion of ambulatory surgical centers (ASCs) and outpatient settings presents a demand for efficient, cost-effective, and easy-to-use stapling devices, aligning with the shift towards less invasive and shorter hospital stays.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +1.1% | Asia Pacific, Latin America, Middle East & Africa | Mid-term (2028-2031) & Long-term (2031-2033) |

| Development of Smart & AI-Integrated Staplers | +1.0% | Global, particularly Developed Economies | Mid-term (2028-2031) & Long-term (2031-2033) |

| Growth of Ambulatory Surgical Centers (ASCs) | +0.8% | North America, Europe | Short-term (2025-2028) |

| Focus on Personalized & Procedure-Specific Devices | +0.7% | Global | Long-term (2031-2033) |

Surgical Stapling Device Market Challenges Impact Analysis

The Surgical Stapling Device market faces several challenges that require strategic navigation by market players. Intense competition among a few dominant global manufacturers, coupled with the entry of local players, creates pricing pressures and necessitates continuous innovation to maintain market share. This competitive landscape demands significant investment in research and development, as well as robust marketing and distribution networks.

Another significant challenge involves the complexities of supply chain management, particularly for global operations, which can be vulnerable to disruptions from geopolitical events, natural disasters, or pandemics. Furthermore, the need for extensive training for surgeons and medical staff on the proper use of advanced stapling devices, coupled with the management of potential complications associated with stapler malfunction, remains a persistent concern. Lastly, cybersecurity risks for increasingly connected or smart surgical devices are emerging as a critical challenge requiring robust protective measures.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Pricing Pressure | -0.8% | Global | Short-term (2025-2028) & Mid-term (2028-2031) |

| Supply Chain Vulnerabilities & Disruptions | -0.7% | Global | Short-term (2025-2028) |

| Training Requirements for New Technologies | -0.6% | Global | Mid-term (2028-2031) |

| Management of Post-Operative Complications | -0.5% | Global | Short-term (2025-2028) |

Surgical Stapling Device Market - Updated Report Scope

This market research report provides an in-depth analysis of the Surgical Stapling Device market, offering a comprehensive understanding of its current landscape, historical performance, and future growth trajectory. The scope encompasses detailed market sizing, segmentation analysis by product, application, end-user, and usage, along with regional breakdowns. It also delves into the competitive environment, identifying key players and their strategic initiatives, and assesses the impact of market drivers, restraints, opportunities, and challenges that shape the industry's evolution. The report aims to furnish stakeholders with actionable insights for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.2 Billion |

| Market Forecast in 2033 | USD 7.6 Billion |

| Growth Rate | 7.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ethicon (Johnson & Johnson Services, Inc.), Medtronic plc, B. Braun Melsungen AG, CONMED Corporation, Becton, Dickinson and Company (BD), Boston Scientific Corporation, Intuitive Surgical, Stryker Corporation, Zimmer Biomet Holdings, Inc., Olympus Corporation, Cook Medical LLC, CooperSurgical, Inc., Grena Ltd., Dextera Surgical Inc. (Acquired by Aesculap, Inc.), Purple Surgical, Welfare Medical Ltd., Meril Life Sciences Pvt. Ltd., Reach Surgical Inc., Frankenman International Ltd., Changzhou Kangdi Medical Apparatus Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Surgical Stapling Device market is comprehensively segmented to provide granular insights into its diverse components and dynamics. This segmentation facilitates a deeper understanding of market trends, consumer preferences, and growth opportunities across various product types, surgical applications, end-user categories, and usage models. The detailed breakdown allows stakeholders to identify specific high-growth areas and tailor strategies to meet evolving market demands and clinical needs.

Analyzing the market through these segments reveals that powered staplers and disposable devices are experiencing significant adoption due to their precision and safety advantages. The increasing volume of abdominal and bariatric surgeries represents key application areas driving demand. Hospitals continue to be the largest end-users, though the growing proliferation of ambulatory surgical centers (ASCs) indicates a shift in healthcare delivery models impacting device procurement and utilization.

- By Product Type: Manual Staplers, Powered Staplers (Linear, Circular, Endoscopic, Skin, Ligating, Specialized)

- By Application: Abdominal Surgery, Thoracic Surgery, Bariatric Surgery, Colorectal Surgery, Gynecological Surgery, Cardiac Surgery, Pediatric Surgery, Other Surgical Applications

- By End User: Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics

- By Usage: Reusable Staplers, Disposable Staplers

Regional Highlights

- North America: Dominates the market share due to advanced healthcare infrastructure, high adoption rates of technologically advanced surgical procedures, significant R&D investments, and the presence of key market players. The U.S. remains a primary market due to a large number of bariatric and other complex surgeries.

- Europe: A mature market characterized by increasing healthcare expenditure, a rising geriatric population, and a high prevalence of chronic diseases. Countries like Germany, France, and the UK are key contributors, focusing on product innovation and favorable reimbursement policies.

- Asia Pacific (APAC): Expected to be the fastest-growing region, driven by improving healthcare infrastructure, increasing medical tourism, a large patient pool, and growing awareness of advanced surgical techniques. Countries like China, India, and Japan are experiencing rapid market expansion.

- Latin America: Showing steady growth due to rising healthcare spending, increasing adoption of modern medical technologies, and a growing number of surgical facilities. Brazil and Mexico are significant markets in this region.

- Middle East and Africa (MEA): Emerging as a potential growth region, fueled by rising investments in healthcare, improving economic conditions, and the increasing incidence of lifestyle-related diseases requiring surgical interventions. Saudi Arabia and UAE are leading the regional market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Surgical Stapling Device Market.- Ethicon (Johnson & Johnson Services, Inc.)

- Medtronic plc

- B. Braun Melsungen AG

- CONMED Corporation

- Becton, Dickinson and Company (BD)

- Boston Scientific Corporation

- Intuitive Surgical

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Olympus Corporation

- Cook Medical LLC

- CooperSurgical, Inc.

- Grena Ltd.

- Dextera Surgical Inc. (Acquired by Aesculap, Inc.)

- Purple Surgical

- Welfare Medical Ltd.

- Meril Life Sciences Pvt. Ltd.

- Reach Surgical Inc.

- Frankenman International Ltd.

- Changzhou Kangdi Medical Apparatus Co., Ltd.

Frequently Asked Questions

What is a surgical stapling device and its primary use?

A surgical stapling device is a medical instrument used to close wounds, resect organs, or create anastomoses during surgical procedures. It delivers surgical staples, typically made of titanium or stainless steel, to securely join tissues or blood vessels, offering an efficient and precise alternative to traditional hand suturing. Its primary use lies in providing a fast, consistent, and strong closure, particularly in minimally invasive surgeries where manual suturing can be challenging.

What are the main types of surgical staplers available in the market?

The main types of surgical staplers include manual staplers and powered staplers. Manual staplers require direct manipulation by the surgeon, while powered staplers offer automated firing and controlled compression for consistent results. Further classifications include linear staplers for straight incisions, circular staplers for creating anastomoses, skin staplers for external wound closure, ligating staplers for blood vessels, and specialized staplers for endoscopic or robotic-assisted procedures.

What are the key advantages of using surgical staplers over traditional sutures?

Surgical staplers offer several advantages over traditional sutures, including significantly reduced operating time, enhanced consistency and uniformity in wound closure, and often a stronger, more secure tissue approximation. They are particularly beneficial in minimally invasive surgeries where access is limited, providing precise closure in deep or confined anatomical spaces. Additionally, staplers can minimize tissue trauma and improve surgical efficiency.

What factors are driving the growth of the surgical stapling device market?

The growth of the surgical stapling device market is primarily driven by the increasing global volume of surgical procedures, a rising prevalence of chronic diseases necessitating surgical interventions, and the escalating adoption of minimally invasive surgical techniques. Technological advancements leading to powered, smart, and robotic-assisted staplers also contribute significantly, alongside the expansion of healthcare infrastructure in emerging economies and a growing aging population.

What are the primary challenges faced by the surgical stapling device market?

Key challenges in the surgical stapling device market include the high cost of advanced devices, which can limit adoption in budget-constrained settings, and stringent regulatory approval processes that prolong market entry for new innovations. Intense market competition leading to pricing pressures, product recalls due to manufacturing issues, and the need for continuous surgeon training on complex new technologies also pose significant hurdles for market players.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted