OLED Encapsulation Adhesive Market

OLED Encapsulation Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700649 | Last Updated : July 26, 2025 |

Format : ![]()

![]()

![]()

![]()

OLED Encapsulation Adhesive Market Size

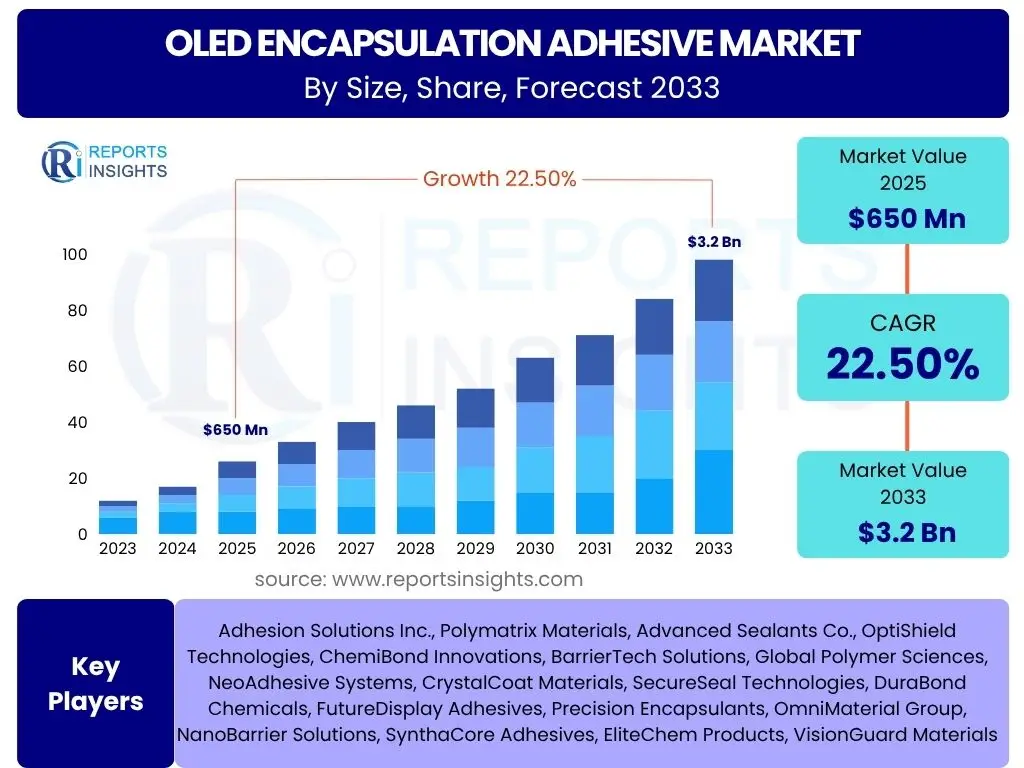

OLED Encapsulation Adhesive Market is projected to grow at a Compound annual growth rate (CAGR) of 22.5% between 2025 and 2033, reaching USD 650 Million in 2025 and is projected to grow by USD 3.2 Billion by 2033 the end of the forecast period.

Key OLED Encapsulation Adhesive Market Trends & Insights

The OLED Encapsulation Adhesive Market is currently experiencing a dynamic phase driven by several influential trends. These trends signify a shift towards more advanced display technologies and a broader range of applications, profoundly impacting the demand and innovation within the encapsulation adhesive sector. The market is increasingly focused on developing materials that can withstand the rigorous demands of next-generation display formats while also addressing environmental considerations. Key insights reveal a clear trajectory towards higher performance, greater flexibility, and enhanced durability in encapsulation solutions.

- Increasing demand for flexible, foldable, and rollable OLED displays.

- Growing integration of OLED technology in diverse consumer electronics.

- Advancements in automotive display and lighting applications utilizing OLEDs.

- Focus on ultra-thin and highly transparent encapsulation materials.

- Rise of micro-LED and mini-LED technologies influencing encapsulation requirements.

- Development of sustainable and eco-friendly adhesive solutions.

- Emphasis on high barrier performance against moisture and oxygen.

- Continuous innovation in UV-curable and hybrid encapsulant formulations.

AI Impact Analysis on OLED Encapsulation Adhesive

Artificial Intelligence (AI) is set to significantly transform various facets of the OLED Encapsulation Adhesive Market, offering unprecedented opportunities for innovation, efficiency, and quality enhancement. AI's capabilities in data processing, pattern recognition, and predictive analytics enable breakthroughs in material science, manufacturing processes, and supply chain management. This technological integration promises to accelerate the development cycle of new adhesives, optimize their performance, and streamline production, ultimately contributing to a more robust and responsive market. The adoption of AI is becoming critical for companies aiming to maintain a competitive edge and address the complex challenges inherent in advanced material development.

- Accelerated discovery and design of novel encapsulation materials through AI-driven simulations.

- Optimized manufacturing processes and quality control using AI for defect detection and real-time adjustments.

- Predictive maintenance for production equipment, minimizing downtime and increasing output efficiency.

- Enhanced supply chain management and logistics optimization, ensuring timely delivery of raw materials and finished products.

- Personalized material formulation and performance prediction based on specific application requirements.

- Improved R&D efficiency by automating data analysis and experimental design.

Key Takeaways OLED Encapsulation Adhesive Market Size & Forecast

- The OLED Encapsulation Adhesive Market is poised for substantial growth, projected at a CAGR of 22.5% from 2025 to 2033.

- Market value is expected to surge from USD 650 Million in 2025 to USD 3.2 Billion by 2033.

- Growth is primarily fueled by the escalating demand for advanced flexible and foldable OLED displays.

- Technological advancements in OLED panels necessitate high-performance, durable encapsulation solutions.

- AI integration is becoming a critical enabler for material innovation and operational efficiency.

- Key challenges include complex manufacturing processes and the need for ultra-high barrier properties.

- Opportunities lie in emerging applications such as AR/VR and smart lighting, alongside new material development.

- Asia Pacific is anticipated to remain the dominant region due to extensive manufacturing capabilities and consumer adoption.

OLED Encapsulation Adhesive Market Drivers Analysis

The OLED Encapsulation Adhesive Market is propelled by several robust drivers that underscore the increasing ubiquity and technological evolution of OLED displays across various sectors. These drivers collectively contribute to a heightened demand for specialized adhesives capable of protecting sensitive OLED components from environmental degradation. As consumer preferences shift towards more advanced, flexible, and immersive display experiences, the need for cutting-edge encapsulation solutions becomes paramount. The continuous innovation in display technology, coupled with the expansion into novel applications, further reinforces the growth trajectory of this market. Understanding these drivers is crucial for stakeholders to capitalize on the burgeoning opportunities and adapt their strategies to market dynamics.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Flexible and Foldable Displays: The rising consumer demand for innovative form factors in smartphones, tablets, and wearables drives the need for highly flexible and durable encapsulation adhesives. | +6.5% | Asia Pacific, North America, Europe | Short to Mid-term (2025-2029) |

| Growing Demand for OLEDs in Consumer Electronics: The widespread integration of OLED panels in high-end televisions, smartphones, and smartwatches necessitates robust encapsulation to extend device lifespan and performance. | +5.8% | Global, particularly Asia Pacific (China, South Korea), North America | Mid to Long-term (2026-2033) |

| Emergence of Automotive OLED Lighting and Displays: The automotive industry's shift towards advanced interior displays and exterior lighting solutions powered by OLEDs creates a new, significant application area for encapsulation adhesives, demanding high reliability and environmental resistance. | +4.2% | Europe, North America, Asia Pacific (Japan, Germany, South Korea) | Mid to Long-term (2027-2033) |

| Technological Advancements in OLED Display Manufacturing: Continuous innovation in OLED panel production, including larger sizes and higher resolutions, requires concomitant improvements in encapsulation adhesive properties for optimal performance and defect prevention. | +3.5% | Global, especially regions with strong R&D capabilities | Continuous |

| Increasing Investment in OLED Production Capacity: Major display manufacturers are expanding their OLED production lines, which directly escalates the demand for essential components like encapsulation adhesives to support increased output. | +2.5% | Asia Pacific (China, South Korea) | Short to Mid-term (2025-2030) |

OLED Encapsulation Adhesive Market Restraints Analysis

While the OLED Encapsulation Adhesive Market exhibits significant growth potential, it is also subject to several restraints that could impede its expansion. These limitations primarily stem from the inherent complexities of OLED technology, the costs associated with high-performance materials, and market competition from established display technologies. Addressing these restraints requires substantial investment in research and development, process optimization, and strategic market positioning. Overcoming these hurdles is essential for manufacturers and suppliers to fully leverage the opportunities present in the burgeoning OLED display market and maintain a sustainable growth trajectory.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost of OLED Panels: The intricate production processes for OLED displays, including the stringent requirements for encapsulation, contribute to higher overall manufacturing costs, potentially limiting broader adoption in cost-sensitive segments. | -4.0% | Global, particularly emerging markets | Mid-term (2025-2030) |

| Complex and Specialized Encapsulation Processes: The need for highly precise and contamination-free encapsulation techniques, such as thin-film encapsulation (TFE), presents significant technical challenges and requires specialized equipment and expertise. | -3.5% | Global, impacting smaller manufacturers | Long-term (2028-2033) |

| Competition from Alternative Display Technologies: While OLEDs are gaining traction, mature LCD technology, and emerging alternatives like MicroLED, continue to offer cost-effective or superior solutions in certain applications, posing a competitive threat. | -2.8% | Global | Short to Mid-term (2025-2028) |

| Material Degradation and Lifespan Concerns: Despite advancements, OLED materials remain susceptible to degradation from moisture and oxygen, necessitating extremely effective encapsulation, and any failure can lead to reduced display lifespan and performance. | -2.0% | Global | Continuous |

OLED Encapsulation Adhesive Market Opportunities Analysis

The OLED Encapsulation Adhesive Market is ripe with promising opportunities driven by technological advancements, market diversification, and evolving consumer demands. These opportunities signify potential areas for growth, innovation, and strategic expansion for market players. As OLED technology continues to mature and penetrate new industry verticals, the demand for specialized, high-performance encapsulation solutions will intensify. Identifying and capitalizing on these emerging avenues will be crucial for companies looking to solidify their market position, diversify their product portfolios, and achieve sustainable long-term growth. The market's dynamic nature encourages continuous research and development to address future encapsulation needs effectively.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Areas: Emerging sectors such as augmented reality (AR) and virtual reality (VR) headsets, smart home appliances, and advanced medical devices are adopting OLED displays, opening new market segments for encapsulation adhesives. | +5.0% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Development of Advanced and Cost-Effective Encapsulation Materials: Innovation in material science leading to new, higher-performing, and more economical adhesive solutions will reduce overall OLED manufacturing costs, fostering broader market adoption. | +4.5% | Global, especially R&D hubs | Continuous |

| Growth in Emerging Markets: Increased disposable income and technological awareness in developing economies are driving the adoption of OLED-equipped devices, presenting significant untapped market potential for encapsulation adhesive suppliers. | +3.8% | Asia Pacific (India, Southeast Asia), Latin America, MEA | Long-term (2029-2033) |

| Focus on Sustainable and Eco-Friendly Encapsulation Solutions: Growing environmental regulations and consumer demand for sustainable products create an opportunity for developing bio-based or recyclable encapsulation adhesives, aligning with global sustainability goals. | +2.7% | Europe, North America, parts of Asia Pacific | Mid to Long-term (2027-2033) |

| Strategic Collaborations and Partnerships: Increased collaboration between material suppliers, display manufacturers, and equipment providers can accelerate innovation, optimize processes, and address complex technical challenges more efficiently. | +2.0% | Global | Continuous |

OLED Encapsulation Adhesive Market Challenges Impact Analysis

Despite the promising outlook, the OLED Encapsulation Adhesive Market faces several significant challenges that could hinder its full growth potential. These challenges are often technical in nature, stemming from the demanding performance requirements of OLED displays and the complexities of advanced material science. Addressing issues such as achieving ultra-thin yet highly effective barriers, ensuring long-term material stability, and navigating a rapidly evolving technological landscape requires substantial R&D investment and continuous innovation. Successfully overcoming these hurdles is crucial for market participants to deliver reliable, high-performance encapsulation solutions that meet the evolving needs of the OLED industry and maintain competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-Thin and Highly Durable Encapsulation: The pursuit of thinner, more flexible, and robust OLED displays necessitates encapsulation layers that are extremely thin yet provide superior barrier properties against moisture and oxygen, posing a significant material and process challenge. | -3.0% | Global, affecting technological leadership | Continuous |

| Ensuring Long-Term Stability and Lifetime of OLED Displays: Encapsulation adhesives must guarantee the long-term stability and operational lifespan of OLED panels, which are highly sensitive to environmental factors, requiring extensive testing and validation. | -2.5% | Global, particularly for premium products | Continuous |

| Rapid Technological Obsolescence: The fast pace of innovation in display technology, including new OLED architectures and emerging display types, means encapsulation materials and processes must constantly evolve, leading to potential obsolescence for existing solutions. | -2.2% | Global, impacting R&D cycles | Short-term (2025-2028) |

| Managing Waste and Recyclability of Advanced Materials: The complex chemical compositions of advanced encapsulation adhesives and OLED panels present challenges in terms of end-of-life recycling and waste management, raising environmental concerns. | -1.8% | Europe, North America, regulatory-focused regions | Mid to Long-term (2027-2033) |

| High R&D Costs and Intellectual Property Barriers: The significant investment required for research and development of novel, high-performance adhesives, coupled with complex intellectual property landscapes, can be a barrier for new market entrants and smaller players. | -1.5% | Global | Continuous |

OLED Encapsulation Adhesive Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the OLED Encapsulation Adhesive Market, providing critical insights into its current landscape, historical performance, and future projections. The report meticulously covers market size, growth drivers, restraints, opportunities, and challenges, segmented across various parameters including material type, application, substrate type, and regional dynamics. It also provides a detailed competitive landscape, profiling key market players and their strategic initiatives. This updated scope ensures a thorough understanding of market trends and forecasts, enabling stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650 Million |

| Market Forecast in 2033 | USD 3.2 Billion |

| Growth Rate | 22.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Adhesion Solutions Inc., Polymatrix Materials, Advanced Sealants Co., OptiShield Technologies, ChemiBond Innovations, BarrierTech Solutions, Global Polymer Sciences, NeoAdhesive Systems, CrystalCoat Materials, SecureSeal Technologies, DuraBond Chemicals, FutureDisplay Adhesives, Precision Encapsulants, OmniMaterial Group, NanoBarrier Solutions, SynthaCore Adhesives, EliteChem Products, VisionGuard Materials |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The OLED Encapsulation Adhesive Market is comprehensively segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market dynamics. This segmentation facilitates a detailed analysis of market trends, growth drivers, and opportunities across various dimensions, enabling stakeholders to identify niche markets and tailor their strategies effectively. Each segment represents a distinct facet of the market, driven by unique material requirements, application demands, and technological advancements. Understanding these specific segments is crucial for accurate market forecasting and strategic planning within the rapidly evolving OLED industry.

- By Material Type: This segment analyzes the market based on the chemical composition and function of the encapsulating material.

- Desiccants: Materials designed to absorb moisture, further categorized into Inorganic Desiccants and Organic Desiccants. Inorganic desiccants typically include molecular sieves or zeolites, while organic desiccants are polymer-based.

- UV Curable Resins: Adhesives that cure rapidly under ultraviolet light, broadly classified into Epoxy-based, Acrylic-based, and Hybrid Resins, each offering distinct properties regarding adhesion, flexibility, and barrier performance.

- Barrier Films: Thin-film materials that create a protective layer, including Thin-film Encapsulation (TFE) layers and Multi-layer Films, which provide superior protection against moisture and oxygen penetration.

- By Application: This segmentation explores the end-use industries and devices where OLED encapsulation adhesives are primarily utilized, highlighting their diverse market penetration.

- Smartphones & Tablets: The largest application segment, driven by the increasing adoption of OLED displays in mobile communication devices, requiring robust and flexible encapsulation.

- Wearable Devices: Including smartwatches and fitness trackers, where compact size and durable, flexible displays necessitate advanced encapsulation.

- Televisions: High-end consumer televisions utilizing large-area OLED panels, demanding high barrier performance for long display life.

- Automotive Displays: Integrating OLED technology into vehicle dashboards, infotainment systems, and exterior lighting, requiring materials with high reliability under varying environmental conditions.

- Smart Lighting: Emerging applications in general and specialized lighting where OLEDs offer unique design flexibility and energy efficiency.

- Others: Encompassing a range of niche and nascent applications such as Augmented Reality (AR) and Virtual Reality (VR) headsets, medical devices, and specialized industrial displays.

- By Substrate Type: This segment differentiates the market based on the type of display substrate being encapsulated, reflecting the growing trend towards flexible electronics.

- Flexible Displays: Encapsulation solutions designed for displays built on flexible substrates like plastic or metal foil, crucial for foldable and rollable devices.

- Rigid Displays: Adhesives for traditional OLED displays manufactured on rigid glass substrates, commonly found in televisions and some smartphone models.

- By Form: This segmentation focuses on the physical state in which the encapsulation adhesive is applied, influencing manufacturing processes and material handling.

- Liquid Encapsulants: Adhesives applied in liquid form, often through dispensing or inkjet printing, which then cure to form a protective layer.

- Film Encapsulants: Pre-formed thin films that are laminated onto the OLED panel, offering precise thickness control and uniform barrier properties.

- Paste Encapsulants: Viscous adhesive formulations applied as a paste, suitable for specific sealing and bonding applications.

Regional Highlights

The global OLED Encapsulation Adhesive Market demonstrates varied growth patterns across different geographical regions, heavily influenced by manufacturing hubs, consumer adoption rates, and technological advancements. Each region contributes distinctly to the market's overall expansion, reflecting unique economic landscapes and strategic priorities.- Asia Pacific (APAC): This region is unequivocally the dominant market for OLED encapsulation adhesives, driven by the presence of major OLED display manufacturing powerhouses, particularly in South Korea and China. Countries like Japan and Taiwan also contribute significantly through their advanced materials science and electronics industries. The high concentration of consumer electronics production, coupled with increasing disposable incomes and a strong demand for innovative display technologies (smartphones, TVs, wearables), fuels robust growth. Extensive investments in new OLED fabrication plants and ongoing research and development initiatives further solidify APAC's leading position, making it a critical hub for both supply and demand.

- North America: North America represents a technologically advanced market characterized by high adoption rates of premium consumer electronics and substantial investments in research and development for emerging technologies like AR/VR. The region's focus on innovative applications and the presence of key technology companies drive the demand for sophisticated OLED encapsulation solutions. While not a primary manufacturing hub for OLED panels on the scale of Asia, North America remains crucial for material innovation, product design, and early adoption of high-value OLED applications, creating a demand for high-performance adhesives.

- Europe: Europe is a significant market, particularly for high-end consumer electronics and the burgeoning automotive display segment. Countries like Germany, France, and the UK are at the forefront of automotive innovation, integrating advanced OLED displays and lighting solutions into vehicles, which necessitates durable and reliable encapsulation. Additionally, strong environmental regulations and a focus on sustainable manufacturing practices in Europe are driving the demand for eco-friendly and energy-efficient encapsulation solutions, influencing material development and adoption patterns within the region.

- Latin America: This region is an emerging market with growing potential, primarily driven by increasing urbanization, rising disposable incomes, and expanding consumer electronics markets. While not a major manufacturing base for OLEDs, Latin America acts as a significant consumer market for OLED-equipped devices, leading to a steady increase in demand for related components. The market growth here is largely influenced by the import of finished OLED products, creating an indirect but consistent demand for encapsulation adhesives.

- Middle East and Africa (MEA): The MEA region is also an emerging market, exhibiting gradual growth primarily due to economic diversification efforts and increasing consumer access to advanced technologies. Investments in infrastructure and smart city initiatives in certain MEA countries are fostering a nascent demand for smart displays, including OLEDs. However, market penetration is slower compared to other regions, and growth is largely dependent on the availability and affordability of OLED-enabled devices.

Top Key Players:

The market research report covers the analysis of key stake holders of the OLED Encapsulation Adhesive Market. Some of the leading players profiled in the report include -- Adhesion Solutions Inc.

- Polymatrix Materials

- Advanced Sealants Co.

- OptiShield Technologies

- ChemiBond Innovations

- BarrierTech Solutions

- Global Polymer Sciences

- NeoAdhesive Systems

- CrystalCoat Materials

- SecureSeal Technologies

- DuraBond Chemicals

- FutureDisplay Adhesives

- Precision Encapsulants

- OmniMaterial Group

- NanoBarrier Solutions

- SynthaCore Adhesives

- EliteChem Products

- VisionGuard Materials

- FlexiBond Technologies

- EcoSeal Solutions

- Luminary Adhesives

Frequently Asked Questions:

What is OLED encapsulation adhesive and why is it crucial?

OLED encapsulation adhesive is a specialized material used to protect Organic Light Emitting Diode (OLED) display components from environmental degradation, particularly from moisture and oxygen. It is crucial because OLED materials are highly susceptible to damage from these elements, which can significantly reduce display lifespan and performance. The adhesive forms a protective barrier, ensuring the longevity and reliability of OLED panels in various electronic devices.What are the primary applications driving the OLED encapsulation adhesive market growth?

The primary applications driving the OLED encapsulation adhesive market growth include smartphones and tablets, which are transitioning rapidly to OLED displays, and high-end televisions. Additionally, the increasing adoption of OLED technology in wearable devices, such as smartwatches, and the emerging use of OLEDs in automotive displays and lighting solutions are significant growth drivers. These applications demand high-performance and durable encapsulation for optimal display function and extended product life.How does flexible display technology impact the demand for these adhesives?

Flexible display technology profoundly impacts the demand for OLED encapsulation adhesives by necessitating materials that can withstand bending, folding, and rolling without compromising barrier integrity. Traditional rigid glass encapsulation is unsuitable for these dynamic applications. This drives demand for advanced flexible and ultra-thin adhesives, such as thin-film encapsulation (TFE) materials and flexible UV-curable resins, which can maintain their protective properties under mechanical stress, enabling the next generation of foldable and rollable devices.What are the key types of materials used in OLED encapsulation adhesives?

The key types of materials used in OLED encapsulation adhesives primarily include desiccants, UV-curable resins, and barrier films. Desiccants, both inorganic and organic, are used to absorb residual moisture. UV-curable resins, such as epoxy-based, acrylic-based, and hybrid formulations, provide a solid, protective layer upon light exposure. Barrier films, often multi-layered or part of thin-film encapsulation (TFE), create a highly effective physical barrier against moisture and oxygen ingress, crucial for long-term OLED performance.What is the forecast for the OLED encapsulation adhesive market size?

The OLED encapsulation adhesive market is projected for robust expansion, with a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market size is estimated to reach USD 650 Million in 2025 and is forecasted to grow substantially to USD 3.2 Billion by the end of 2033. This significant growth is attributed to the widespread adoption of OLED displays across various consumer and industrial applications, coupled with continuous advancements in display technology requiring superior encapsulation solutions.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted