Offshore Wind Market

Offshore Wind Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701063 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Offshore Wind Market Size

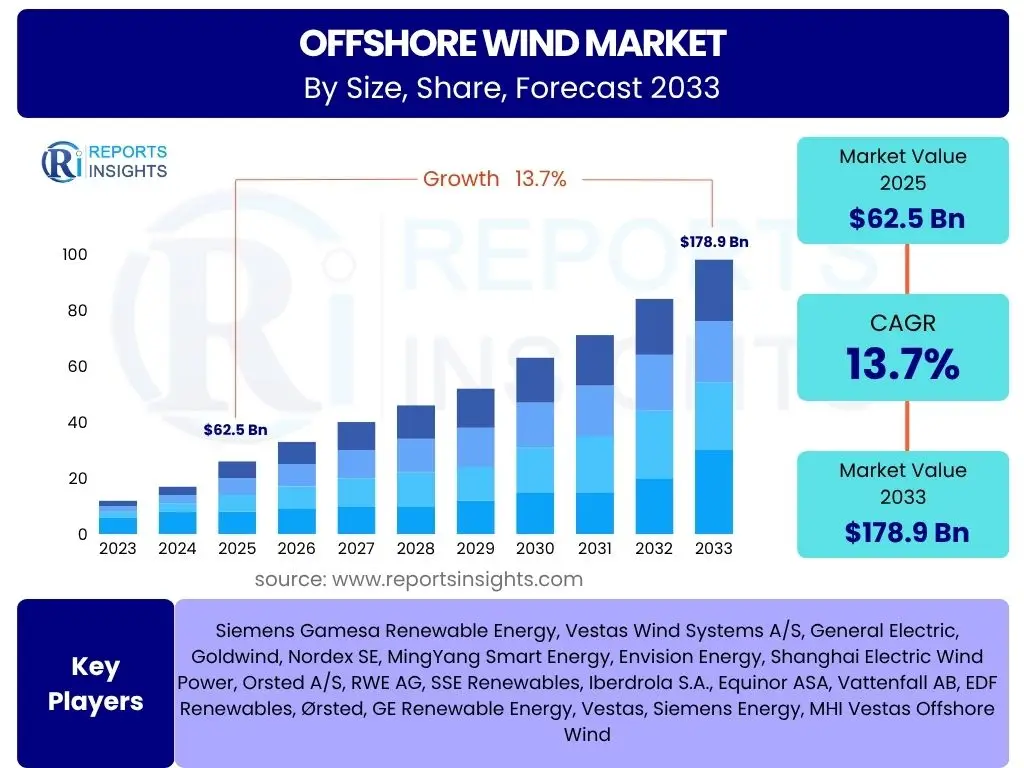

According to Reports Insights Consulting Pvt Ltd, The Offshore Wind Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033. The market is estimated at USD 62.5 Billion in 2025 and is projected to reach USD 178.9 Billion by the end of the forecast period in 2033.

Key Offshore Wind Market Trends & Insights

The offshore wind market is experiencing rapid evolution driven by technological advancements, evolving regulatory frameworks, and increasing global commitments to renewable energy. A primary trend is the substantial increase in turbine size and capacity, with developers increasingly deploying 15MW+ turbines, which significantly enhance power output per project and reduce levelized cost of energy (LCOE). This upscaling enables more efficient energy capture and economies of scale, making offshore wind more competitive with traditional power sources.

Another pivotal trend is the accelerated development and commercialization of floating offshore wind technology. As suitable shallow-water sites become scarce, floating foundations unlock vast deep-water areas for development, particularly in regions like the Mediterranean, parts of Asia, and the U.S. West Coast. This innovation addresses geographical limitations and expands the global potential for offshore wind deployment, attracting significant investment in research, development, and pilot projects.

Furthermore, the market is witnessing a strong emphasis on grid integration and energy storage solutions. As offshore wind projects grow in scale, ensuring stable and reliable power transmission to onshore grids becomes critical. Investments in advanced high-voltage direct current (HVDC) transmission systems, grid hardening, and co-located energy storage solutions, such as battery storage or green hydrogen production, are becoming more prevalent. These efforts aim to enhance grid stability, manage intermittency, and maximize the utility of renewable energy generation.

- Upscaling of turbine technology towards 15MW+ capacity to enhance efficiency and reduce LCOE.

- Rapid advancements and commercialization of floating offshore wind solutions unlocking deep-water development potential.

- Integration of offshore wind with green hydrogen production to decarbonize hard-to-abate sectors.

- Increased focus on hybrid projects combining offshore wind with solar or battery storage for enhanced grid stability.

- Development of advanced digital twins and predictive maintenance systems for operational optimization.

- Growth in cross-border grid connections and energy island concepts to improve energy security and distribution.

AI Impact Analysis on Offshore Wind

Artificial Intelligence (AI) is set to profoundly transform the offshore wind sector, offering unprecedented capabilities for optimizing various aspects of project lifecycle, from design and construction to operations and maintenance. Users frequently inquire about AI's role in improving efficiency and reducing costs. AI-powered analytics can process vast amounts of data from sensors on turbines, weather patterns, and marine conditions to predict equipment failures, optimize maintenance schedules, and enhance energy yield forecasts, thereby minimizing downtime and maximizing operational efficiency.

Concerns often revolve around the complexity of AI implementation, data security, and the need for specialized skills. However, the benefits largely outweigh these challenges. AI-driven solutions are crucial for advanced resource assessment, enabling developers to identify optimal turbine placement and array layouts with higher precision, leading to significantly improved energy capture. Furthermore, AI facilitates predictive modeling for environmental impact assessments, allowing for more sustainable project planning and compliance with stringent regulations.

Expectations for AI's influence include enhanced safety protocols through real-time monitoring and anomaly detection, optimized supply chain logistics, and more efficient grid integration. AI algorithms can manage complex grid demands, balancing intermittent wind power with overall energy supply and demand, contributing to a more stable and resilient energy system. As the industry matures, the integration of AI will become indispensable for achieving ambitious decarbonization goals and maintaining competitive advantage in the global energy market.

- Predictive maintenance and fault detection through AI-driven analytics, minimizing downtime and O&M costs.

- Optimized wind farm design and turbine placement using AI for enhanced energy capture and site assessment.

- Real-time performance monitoring and anomaly detection to improve operational efficiency and safety.

- Enhanced grid integration and stability through AI-powered forecasting and energy management systems.

- Autonomous inspection and repair using AI-enabled robotics and drones, reducing human risk and operational time.

Key Takeaways Offshore Wind Market Size & Forecast

The offshore wind market is poised for robust expansion, driven by aggressive renewable energy targets set by governments worldwide and a significant decline in the Levelized Cost of Energy (LCOE). A primary takeaway is the accelerating pace of project development, with several large-scale projects moving from planning to construction phases, indicating a maturing industry with proven technological and financial viability. The continuous innovation in turbine technology and foundation types, particularly floating offshore wind, is unlocking new geographical areas for development, expanding the addressable market considerably beyond traditional shallow-water sites.

Another crucial insight is the increasing private sector investment and the growing confidence among financial institutions in the long-term profitability of offshore wind projects. This influx of capital is critical for funding the massive infrastructure requirements of large-scale wind farms and associated grid upgrades. Furthermore, the market is benefiting from supportive policy frameworks, including attractive subsidy schemes, Contracts for Difference (CfDs), and streamlined permitting processes in key development regions, which provide a stable investment environment and reduce project risks.

The forecast anticipates sustained growth, fueled by global energy security concerns and the imperative to reduce carbon emissions. The integration of offshore wind with other emerging technologies, such as green hydrogen production and energy storage, is also contributing to its diversified value proposition, enhancing its role in the broader energy transition. The market's resilience against economic fluctuations and its critical contribution to energy independence solidify its position as a cornerstone of future global energy supply.

- Significant growth projected, driven by policy support and decreasing LCOE.

- Technological advancements, especially in floating wind, are unlocking new market segments.

- Increasing private investment and financial confidence are propelling large-scale project development.

- Enhanced grid infrastructure and energy storage integration are critical for market scaling.

- Supply chain development and industrialization are key to achieving cost reduction targets.

Offshore Wind Market Drivers Analysis

The global offshore wind market is experiencing significant growth propelled by a confluence of powerful drivers. Decarbonization mandates and ambitious renewable energy targets set by governments worldwide are perhaps the most influential, creating a strong regulatory push and demand for clean power sources. This is complemented by continuous technological advancements, particularly in turbine design and foundation technologies, which have dramatically improved efficiency, increased capacity, and reduced the Levelized Cost of Energy (LCOE) of offshore wind, making it increasingly competitive with fossil fuels. The growing geopolitical emphasis on energy independence and security also serves as a strong driver, as countries seek to diversify their energy mix and reduce reliance on volatile fossil fuel markets by leveraging abundant domestic wind resources.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Mandates & Renewable Targets | +4.5% | Europe, North America, APAC | 2025-2033 |

| Technological Advancements & Cost Reductions (LCOE) | +3.8% | Global | 2025-2033 |

| Energy Security & Independence Initiatives | +2.7% | Europe, Asia, North America | 2025-2030 |

| Government Incentives & Supportive Policy Frameworks | +2.5% | Europe, U.S., UK, Germany, Taiwan, South Korea | 2025-2033 |

| Increasing Corporate Power Purchase Agreements (PPAs) | +1.9% | Europe, U.S., APAC | 2025-2033 |

Offshore Wind Market Restraints Analysis

Despite its significant growth potential, the offshore wind market faces several notable restraints. High upfront capital expenditure (CAPEX) for developing large-scale offshore wind farms, including specialized vessels, installation equipment, and complex grid connections, remains a significant barrier, requiring substantial financial commitment and long-term investment cycles. Furthermore, the inherent complexities of grid integration and transmission infrastructure pose challenges; existing onshore grids often require extensive upgrades to accommodate large influxes of intermittent offshore wind power, leading to bottlenecks and delays in project commissioning. The lengthy and intricate permitting and consenting processes, which involve numerous regulatory bodies and environmental assessments, also slow down project development, adding to overall costs and project timelines.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Expenditure (CAPEX) | -2.1% | Global | 2025-2030 |

| Grid Integration & Transmission Infrastructure Limitations | -1.8% | Europe, U.S., Japan | 2025-2033 |

| Lengthy Permitting & Consenting Processes | -1.5% | U.S., UK, France, Germany | 2025-2030 |

| Environmental Concerns & Biodiversity Impact | -1.2% | Europe, U.S. East Coast | 2025-2033 |

| Supply Chain Bottlenecks & Raw Material Price Volatility | -1.0% | Global | 2025-2028 |

Offshore Wind Market Opportunities Analysis

The offshore wind market is ripe with substantial opportunities that can further accelerate its growth trajectory. The most significant opportunity lies in the rapid development and commercialization of floating offshore wind technology, which unlocks vast deep-water areas previously inaccessible to conventional fixed-bottom turbines. This innovation allows for deployment in regions with steep continental shelves, such as the Mediterranean Sea, U.S. West Coast, Japan, and South Korea, significantly expanding the global addressable market. Furthermore, the increasing demand for green hydrogen production presents a lucrative synergy, where offshore wind power can be directly used to produce hydrogen through electrolysis, offering a pathway to decarbonize hard-to-abate industrial sectors and providing a flexible energy storage solution.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Commercialization of Floating Offshore Wind Technology | +3.2% | Japan, South Korea, U.S. West Coast, UK, Norway | 2028-2033 |

| Integration with Green Hydrogen Production | +2.8% | Europe, Australia, Middle East | 2027-2033 |

| Emerging Markets in Asia-Pacific and North America | +2.5% | U.S., Japan, South Korea, Vietnam, India, Australia | 2025-2033 |

| Repowering and Life Extension of Existing Assets | +1.9% | Europe (UK, Denmark, Germany) | 2030-2033 |

| Development of Hybrid Projects (Wind + Storage/Solar) | +1.5% | Global | 2025-2033 |

Offshore Wind Market Challenges Impact Analysis

The offshore wind market faces several significant challenges that require strategic solutions to sustain its rapid growth. One primary challenge is the escalating cost of raw materials and ongoing supply chain bottlenecks, particularly for critical components like steel, copper, and specialized vessels, which can lead to project delays and increased development costs. Another key challenge is the shortage of skilled labor across the value chain, from specialized engineers and technicians to construction and installation crews; the rapid expansion of the industry outpaces the current availability of trained personnel, necessitating significant investment in workforce development and training programs. Furthermore, social acceptance and opposition from local communities or fishing industries due to visual impact, navigation interference, or environmental concerns can create significant hurdles in the permitting and development phases of new projects, often leading to protracted disputes and project delays.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Constraints & Raw Material Price Volatility | -1.7% | Global | 2025-2028 |

| Shortage of Skilled Labor & Specialized Vessels | -1.5% | Global | 2025-2033 |

| Social Acceptance & Public Opposition | -1.3% | U.S., France, coastal regions | 2025-2030 |

| Intermittency & Grid Stability Management | -1.0% | Global | 2025-2033 |

| Increasing Cybersecurity Threats to Critical Infrastructure | -0.8% | Global | 2025-2033 |

Offshore Wind Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the global offshore wind market, covering its historical performance, current dynamics, and future projections. The report delves into market sizing, growth drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. It also includes detailed segmentation analysis by foundation type, component, location, and end-use, alongside extensive regional insights, enabling stakeholders to identify key growth pockets and strategic investment areas. The competitive landscape analysis profiles key market players, highlighting their strategies and recent developments to offer a complete understanding of the market's competitive dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 62.5 Billion |

| Market Forecast in 2033 | USD 178.9 Billion |

| Growth Rate | 13.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, General Electric, Goldwind, Nordex SE, MingYang Smart Energy, Envision Energy, Shanghai Electric Wind Power, Orsted A/S, RWE AG, SSE Renewables, Iberdrola S.A., Equinor ASA, Vattenfall AB, EDF Renewables, Ørsted, GE Renewable Energy, Vestas, Siemens Energy, MHI Vestas Offshore Wind |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The offshore wind market is meticulously segmented to provide a granular understanding of its diverse facets and varying dynamics across different technological and application spectra. This segmentation enables stakeholders to identify specific high-growth areas, assess market maturity, and tailor strategies to capture niche opportunities. By understanding the performance of each segment, industry participants can optimize their product offerings, R&D investments, and market entry strategies, ultimately contributing to a more efficient and targeted market approach.

- Foundation Type: This segment differentiates between fixed-bottom and floating foundations, crucial for understanding site suitability and technological maturity.

- Fixed-bottom: Includes established technologies like Monopile, Jacket, Gravity-based, and Tripod foundations, typically deployed in shallower waters.

- Floating: Encompasses innovative solutions such as Semi-Submersible, Spar, Tension-Leg Platform, and Buoy concepts, designed for deeper waters and offering significant potential for market expansion into new geographical areas.

- Component: Analysis of the critical components that make up an offshore wind farm, detailing their individual market sizes and growth rates.

- Turbine: Covers the Blades, Nacelle (housing the generator, gearbox, and control systems), and Tower.

- Substructure: Refers to the foundation structure that supports the turbine.

- Electrical Infrastructure: Includes offshore and onshore Cables for power transmission, and Offshore and Onshore Substations for voltage transformation and grid connection.

- Grid Connection: Specific systems and hardware required to connect the offshore wind farm to the national grid.

- Others: Encompasses ancillary components and services like foundations, scour protection, and installation equipment.

- Location: Categorizes projects based on water depth, impacting technology choice and project complexity.

- Shallow Water: Typically where fixed-bottom foundations are economically viable.

- Deep Water: Areas requiring floating wind technologies, representing future growth opportunities.

- End-Use: Examines the primary application or consumer of the generated offshore wind power.

- Residential: Power supplied to residential consumers.

- Commercial: Power supplied to commercial establishments.

- Industrial: Power supplied to industrial facilities, often through direct Power Purchase Agreements (PPAs).

- Utility-Scale: Power fed directly into the national grid for general public and business consumption.

Regional Highlights

- Europe: Europe remains the undisputed leader in offshore wind development, boasting the largest installed capacity and a robust project pipeline. Countries like the UK, Germany, Denmark, and the Netherlands have established mature markets with supportive policy frameworks, experienced supply chains, and significant investment in R&D, particularly in next-generation turbine technology and grid infrastructure. The region is also at the forefront of floating offshore wind pilot projects and the development of multi-country energy islands aimed at enhancing regional grid integration and energy security.

- North America: The North American offshore wind market, particularly the United States, is poised for significant growth, driven by ambitious state-level mandates and federal support under initiatives like the Inflation Reduction Act. The U.S. East Coast is witnessing the first wave of large-scale project development, while California and other West Coast states are exploring the vast potential of floating offshore wind in deeper waters. Challenges such as lengthy permitting processes and port infrastructure limitations are being actively addressed to accelerate deployment.

- Asia Pacific (APAC): APAC is emerging as a global offshore wind powerhouse, with countries like China, Taiwan, Japan, and South Korea leading the charge. China possesses the largest operational offshore wind capacity globally, while Taiwan and South Korea are rapidly expanding their markets with strong government incentives and a focus on domestic content creation. Japan, with its deep coastal waters, is a key market for floating offshore wind technology. The region's growing energy demand and commitment to decarbonization make it a critical growth engine for the industry.

- Latin America: While still in nascent stages, Latin America holds substantial long-term potential for offshore wind, particularly in countries like Brazil and Colombia with extensive coastlines and favorable wind resources. Early-stage feasibility studies and policy discussions are underway, signaling future development. The region's increasing energy demand and focus on diversifying its energy mix could drive significant investment in offshore wind in the coming decade.

- Middle East and Africa (MEA): The MEA region is beginning to explore its offshore wind potential, with initial interest in countries like South Africa and parts of the Middle East, driven by renewable energy targets and the need for water desalination powered by clean energy. While development is currently limited, increasing awareness of climate change and diversification strategies are expected to stimulate future growth, especially for hybrid projects combining offshore wind with hydrogen production or desalinization plants.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Offshore Wind Market.- Siemens Gamesa Renewable Energy

- Vestas Wind Systems A/S

- General Electric

- Goldwind

- Nordex SE

- MingYang Smart Energy

- Envision Energy

- Shanghai Electric Wind Power

- Orsted A/S

- RWE AG

- SSE Renewables

- Iberdrola S.A.

- Equinor ASA

- Vattenfall AB

- EDF Renewables

- Ocean Winds (Engie & EDPR JV)

- DONG Energy (now Ørsted)

- GE Renewable Energy

- MHI Vestas Offshore Wind (now a part of Vestas)

- CIP (Copenhagen Infrastructure Partners)

Frequently Asked Questions

What is the projected growth rate for the Offshore Wind Market?

The Offshore Wind Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033, reaching an estimated value of USD 178.9 Billion by 2033 from USD 62.5 Billion in 2025. This significant growth is driven by global decarbonization efforts, technological advancements, and supportive government policies.

How is floating offshore wind technology impacting the market?

Floating offshore wind technology is a transformative trend that unlocks vast deep-water areas for development, previously inaccessible to traditional fixed-bottom turbines. This innovation allows for deployment in regions with steep continental shelves, such as Japan, South Korea, and the U.S. West Coast, significantly expanding the global addressable market and driving future growth.

What are the primary drivers of the Offshore Wind Market?

Key drivers include global decarbonization mandates and ambitious renewable energy targets, continuous technological advancements leading to reduced Levelized Cost of Energy (LCOE), increasing emphasis on energy security and independence, and robust government incentives and supportive policy frameworks across major economies. These factors collectively create a conducive environment for sustained market expansion.

What challenges does the Offshore Wind Market face?

The market faces challenges such as high upfront capital expenditure, complexities in grid integration and transmission infrastructure, lengthy permitting and consenting processes, potential supply chain bottlenecks, and a shortage of skilled labor. Addressing these challenges through strategic investments, policy reforms, and workforce development is crucial for sustained growth.

How is Artificial Intelligence (AI) being utilized in offshore wind?

AI is revolutionizing the offshore wind sector by enabling predictive maintenance, optimizing wind farm design and turbine placement, enhancing real-time performance monitoring, and improving grid integration and stability. AI-driven analytics help minimize downtime, reduce operational costs, and maximize energy yield, contributing significantly to the efficiency and profitability of offshore wind projects.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted