Offshore Pipeline Infrastructure Market

Offshore Pipeline Infrastructure Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705652 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Offshore Pipeline Infrastructure Market Size

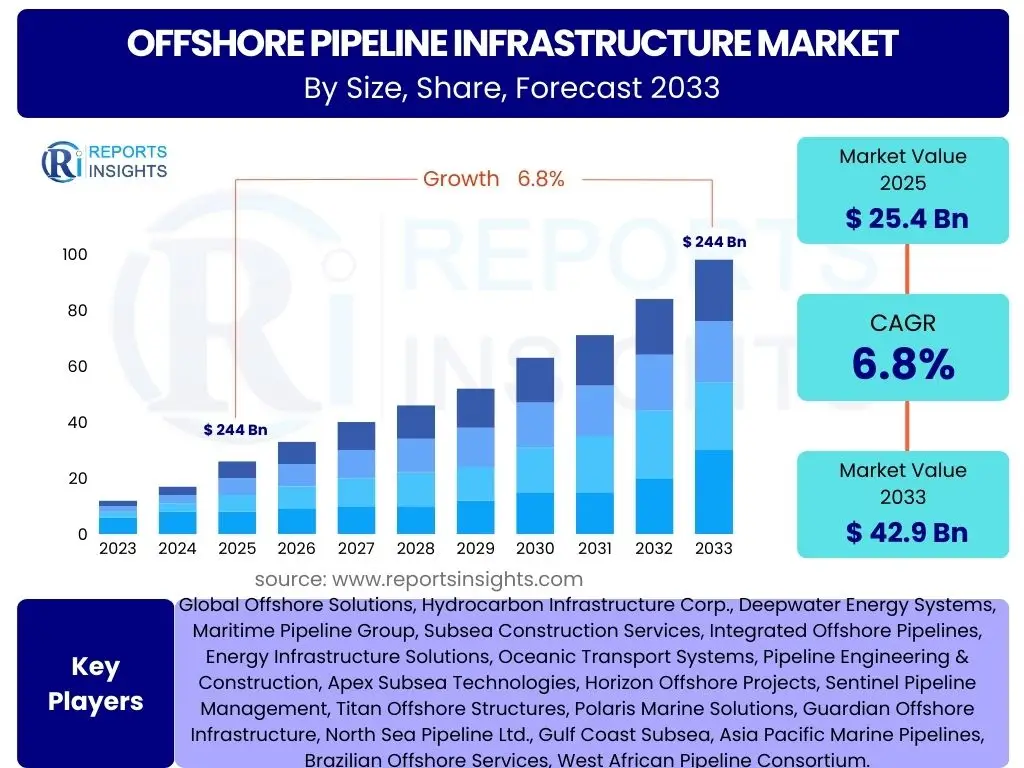

According to Reports Insights Consulting Pvt Ltd, The Offshore Pipeline Infrastructure Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 25.4 Billion in 2025 and is projected to reach USD 42.9 Billion by the end of the forecast period in 2033.

Key Offshore Pipeline Infrastructure Market Trends & Insights

User inquiries frequently revolve around the evolving technological landscape and sustainability initiatives within the offshore pipeline sector. There is significant interest in how digitalization, automation, and advanced materials are shaping future projects. Stakeholders are also keen to understand the shift towards deeper water exploration and the increasing emphasis on environmental compliance and decarbonization efforts. The market is experiencing a notable pivot towards integrating renewable energy transportation and carbon capture solutions, which introduces new pipeline requirements.

Furthermore, discussions highlight the importance of asset integrity management and the adoption of predictive maintenance strategies to enhance operational efficiency and safety. The ongoing need to replace aging infrastructure, particularly in mature basins, presents a continuous demand for new installations and refurbishment projects. Geopolitical shifts and energy security concerns are also driving strategic investments in new inter-regional pipeline connections, ensuring diversified supply routes.

- Growing adoption of digital twin technology and AI-powered predictive maintenance for enhanced asset management and operational efficiency.

- Increased focus on ultra-deepwater and Arctic region exploration and production, requiring advanced pipeline materials and installation techniques.

- Rising investment in gas pipelines, including LNG export/import infrastructure, driven by global energy transition strategies and demand for cleaner fossil fuels.

- Integration of hydrogen and carbon capture, utilization, and storage (CCUS) pipeline infrastructure as part of decarbonization efforts.

- Emphasis on environmental regulations and sustainable practices, leading to innovations in pipeline design, construction, and decommissioning to minimize ecological impact.

- Technological advancements in subsea robotics and autonomous underwater vehicles (AUVs) for inspection, repair, and maintenance (IRM) operations, reducing human intervention and operational costs.

AI Impact Analysis on Offshore Pipeline Infrastructure

Common user questions regarding AI's influence in the offshore pipeline domain typically focus on its practical applications, such as improving operational efficiency, enhancing safety, and optimizing asset management. There is a strong curiosity about how AI can mitigate risks, reduce costs, and extend the lifespan of critical infrastructure. Users are keen to understand specific use cases, ranging from predictive maintenance and integrity monitoring to autonomous inspection and construction planning.

The sentiment is largely positive, recognizing AI's potential to transform traditional labor-intensive processes into data-driven, automated workflows. However, concerns are also raised regarding data security, the need for skilled personnel to manage AI systems, and the initial investment required for implementation. Despite these challenges, the overarching expectation is that AI will play a pivotal role in creating more resilient, efficient, and environmentally sustainable offshore pipeline networks, by enabling proactive decision-making and continuous optimization across the entire lifecycle of infrastructure assets.

- AI-driven predictive maintenance: Enhances asset reliability and extends operational lifespan by forecasting equipment failures.

- Real-time integrity monitoring: Utilizes AI algorithms to analyze sensor data for immediate detection of anomalies and potential leaks.

- Route optimization and planning: AI assists in identifying optimal pipeline routes, considering environmental, geological, and economic factors.

- Autonomous inspection and repair: Powers AUVs and robotics for self-guided inspections and targeted repairs, reducing human exposure to hazardous environments.

- Enhanced safety protocols: AI systems analyze operational data to identify potential safety hazards and recommend preventative measures.

- Supply chain optimization: AI streamlines logistics and procurement for pipeline construction and maintenance projects, improving efficiency.

Key Takeaways Offshore Pipeline Infrastructure Market Size & Forecast

Analysis of common user questions regarding the Offshore Pipeline Infrastructure market size and forecast reveals a predominant interest in future growth trajectories, investment hotspots, and the driving forces behind market expansion. Users are particularly keen on understanding how global energy demand, geopolitical stability, and technological advancements will influence market valuation and regional opportunities. The focus is on identifying areas of significant growth and anticipating potential market shifts that could impact long-term investment strategies.

The insights indicate that while traditional oil and gas transportation remains a core component, the market's future growth is increasingly tied to the energy transition, including infrastructure for natural gas, hydrogen, and carbon capture. Stakeholders are seeking clarity on the scale of investments required for these new ventures and the projected timelines for their maturity. Furthermore, there's a strong emphasis on the role of digitalization and automation in enhancing project viability and economic returns, underscoring the shift towards more efficient and sustainable operational models.

- Significant market growth anticipated, driven by sustained global energy demand and strategic infrastructure development.

- Natural gas pipelines and liquefied natural gas (LNG) export/import facilities are expected to be key growth segments.

- Increasing investments in deepwater and ultra-deepwater projects are propelling demand for advanced pipeline technologies.

- Emergence of new market segments such as hydrogen and carbon capture pipelines will contribute substantially to future expansion.

- Technological advancements, including digitalization and automation, are critical enablers for market efficiency and safety.

- Market stability is influenced by geopolitical factors, regulatory frameworks, and global economic conditions, requiring adaptive strategies.

Offshore Pipeline Infrastructure Market Drivers Analysis

The offshore pipeline infrastructure market is significantly driven by a confluence of factors, primarily the persistent global demand for energy resources, particularly hydrocarbons, which necessitates efficient transportation from offshore fields to processing facilities. As easily accessible onshore reserves deplete, exploration and production activities are increasingly moving into deeper waters and more challenging offshore environments, thereby creating continuous demand for robust and specialized pipeline networks. Furthermore, the growing global trade in natural gas, particularly in its liquefied form (LNG), fuels the need for extensive subsea gas pipelines and associated infrastructure to connect production hubs with consumption centers across continents.

Another crucial driver is the ongoing energy transition and the strategic shift towards natural gas as a cleaner bridging fuel, which necessitates expanded gas transmission infrastructure. Additionally, the development of new energy projects, including offshore wind farms and nascent carbon capture and storage (CCS) initiatives, presents new avenues for pipeline construction. These factors, combined with the imperative to replace aging infrastructure and ensure asset integrity in existing networks, collectively contribute to the sustained growth and investment in the offshore pipeline sector.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Energy Demand | +1.8% | Global (Asia Pacific, North America, Europe) | 2025-2033 |

| New Offshore Discoveries & Deepwater Exploration | +1.5% | Brazil, West Africa, Gulf of Mexico, North Sea, Southeast Asia | 2025-2033 |

| Growth in Natural Gas Consumption & Trade | +1.3% | Europe, Asia Pacific (China, India, Japan), North America | 2025-2033 |

| Replacement & Modernization of Aging Infrastructure | +1.0% | North Sea, Gulf of Mexico, Persian Gulf | 2025-2030 |

Offshore Pipeline Infrastructure Market Restraints Analysis

The offshore pipeline infrastructure market faces several significant restraints that can impede its growth and increase project complexity. One primary challenge is the stringent and evolving environmental regulations governing offshore activities. Concerns over marine ecosystem protection, oil spill prevention, and carbon emissions necessitate rigorous compliance and often lead to lengthy approval processes, increasing project timelines and costs. The escalating capital expenditure associated with complex offshore projects, including specialized vessels, advanced materials, and deepwater installation techniques, also poses a substantial barrier, making funding more challenging to secure and potentially delaying or canceling projects.

Furthermore, geopolitical instability in key energy-producing regions can introduce significant uncertainties, affecting investment decisions and project viability. Fluctuations in crude oil and natural gas prices directly impact the profitability of offshore exploration and production, subsequently influencing the demand for new pipeline infrastructure. Supply chain disruptions, often exacerbated by global events or trade tensions, can also lead to delays and increased costs for materials and equipment. These multifaceted restraints collectively demand careful risk assessment and innovative mitigation strategies from market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations & Compliance Costs | -1.2% | Global (Europe, North America particularly) | 2025-2033 |

| High Capital Expenditure & Project Financing Challenges | -1.0% | Global | 2025-2033 |

| Volatility in Crude Oil & Gas Prices | -0.8% | Global | 2025-2033 |

| Geopolitical Risks & Regional Instability | -0.7% | Middle East, Eastern Europe, South China Sea | 2025-2033 |

Offshore Pipeline Infrastructure Market Opportunities Analysis

Significant opportunities are emerging within the offshore pipeline infrastructure market, driven by global energy transition efforts and technological advancements. One key area is the development of infrastructure for transporting new energy carriers such as hydrogen and for carbon capture, utilization, and storage (CCUS) projects. As nations commit to decarbonization, there will be increasing demand for pipelines capable of handling these specialized substances, potentially repurposing existing gas pipelines or requiring entirely new build-outs. This presents a substantial long-term growth avenue for pipeline operators and constructors.

Furthermore, advancements in digital technologies, including remote sensing, robotics, and advanced analytics, offer opportunities to enhance the efficiency, safety, and cost-effectiveness of pipeline operations and maintenance. The ability to conduct more precise inspections, predict failures, and automate repair processes can reduce operational expenditures and extend asset life. Lastly, the strategic expansion into frontier regions with undeveloped offshore reserves, coupled with the ongoing need for robust inter-regional energy connectivity, provides further avenues for new pipeline installations and upgrades, especially in areas previously considered economically or technically challenging.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Hydrogen & CCUS Pipelines | +1.5% | Europe, North America, Australia, Middle East | 2028-2033 |

| Technological Advancements (AI, Robotics, Digitalization) | +1.2% | Global | 2025-2033 |

| Expansion into Underexplored Frontier Basins | +1.0% | Arctic, East Africa, Eastern Mediterranean, South America | 2027-2033 |

| Strategic Inter-Regional Energy Connectivity Projects | +0.9% | Europe-Africa, Asia-Europe, South Asia | 2025-2033 |

Offshore Pipeline Infrastructure Market Challenges Impact Analysis

The offshore pipeline infrastructure market grapples with several formidable challenges that influence project feasibility, cost, and timelines. One significant hurdle is the increasing complexity of operating in extreme environments, such as ultra-deep waters, high-pressure/high-temperature (HPHT) conditions, and Arctic regions. These conditions demand highly specialized engineering, advanced materials, and sophisticated installation techniques, significantly driving up project costs and technical risks. The aging infrastructure in mature offshore basins also presents a dual challenge: the need for extensive maintenance, repair, and potential replacement, alongside the complexities of decommissioning and ensuring environmental compliance for end-of-life assets.

Furthermore, climate change impacts, including more severe weather events and rising sea levels, pose direct threats to the physical integrity and operational continuity of offshore pipelines, requiring enhanced resilience measures. The industry also faces a persistent shortage of skilled labor, particularly specialized engineers, technicians, and vessel crew, which can lead to project delays and increased labor costs. Navigating the intricate web of international and national regulations, coupled with public and environmental group opposition to new fossil fuel infrastructure, adds layers of complexity to project development and execution. Addressing these challenges requires continuous innovation, strategic partnerships, and robust risk management frameworks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Operating in Extreme & Harsh Environments | -1.0% | Global (Deepwater, Arctic) | 2025-2033 |

| Aging Infrastructure & Decommissioning Complexities | -0.9% | North Sea, Gulf of Mexico, Southeast Asia | 2025-2030 |

| Increasing Regulatory & Permitting Burdens | -0.8% | Global | 2025-2033 |

| Skilled Labor Shortages & Talent Retention | -0.7% | Global | 2025-2033 |

Offshore Pipeline Infrastructure Market - Updated Report Scope

This report provides a comprehensive analysis of the Offshore Pipeline Infrastructure Market, encompassing detailed market sizing, forecast projections, and a thorough examination of key growth drivers, significant restraints, emerging opportunities, and prevailing challenges. It segments the market by various criteria, including material, product type, depth, application, and region, offering granular insights into specific market dynamics. The report also profiles leading industry players, assessing their strategies, market positioning, and recent developments to provide a holistic view of the competitive landscape. Its scope extends to analyzing the impact of technological advancements and geopolitical factors on market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.4 Billion |

| Market Forecast in 2033 | USD 42.9 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Offshore Solutions, Hydrocarbon Infrastructure Corp., Deepwater Energy Systems, Maritime Pipeline Group, Subsea Construction Services, Integrated Offshore Pipelines, Energy Infrastructure Solutions, Oceanic Transport Systems, Pipeline Engineering & Construction, Apex Subsea Technologies, Horizon Offshore Projects, Sentinel Pipeline Management, Titan Offshore Structures, Polaris Marine Solutions, Guardian Offshore Infrastructure, North Sea Pipeline Ltd., Gulf Coast Subsea, Asia Pacific Marine Pipelines, Brazilian Offshore Services, West African Pipeline Consortium. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The offshore pipeline infrastructure market is segmented comprehensively to provide granular insights into its diverse components and applications. This segmentation allows for a detailed understanding of specific industry dynamics, technology adoption rates, and regional demand patterns across various operational parameters. Analyzing the market through these distinct lenses helps stakeholders identify niche opportunities, assess competitive landscapes within specific categories, and tailor strategies to address the unique requirements of different sub-sectors. The segmentation also highlights the industry's evolution, showcasing the increasing complexity and specialization required for modern offshore projects.

- By Type: This segment differentiates pipelines based on the fluid they transport, primarily oil and gas, but also includes other fluids such as water for injection or chemicals. The demand for each type is influenced by global energy mix shifts and specific regional resource development.

- By Material: This segmentation explores the types of materials used for pipeline construction, predominantly steel variants (carbon, stainless, alloy) known for their strength and durability, as well as emerging composite materials offering enhanced corrosion resistance and flexibility.

- By Diameter: Pipelines are categorized by their internal diameter, which directly impacts their capacity and suitability for various transportation volumes. This includes small, medium, and large diameter pipelines catering to different project scales.

- By Depth: This critical segment classifies pipelines based on the water depth at which they are installed: shallow water, deepwater, and ultra-deepwater. Each depth category presents unique engineering challenges, technological requirements, and cost structures.

- By Application: This segment defines the primary function of the pipeline within the offshore energy value chain, including transportation (long-distance), gathering (from wellheads to processing units), distribution (to onshore facilities), and activities related to decommissioning and abandonment.

- By Component: This detailed segmentation breaks down the pipeline system into its constituent parts, such as the pipes themselves, various fittings and connectors, control valves and actuators, essential pumps and compressors, and advanced monitoring and control systems critical for operational integrity.

Regional Highlights

- North America: Driven by sustained activity in the Gulf of Mexico, with significant investments in deepwater oil and gas fields and a growing focus on pipeline integrity management and modernization projects. Canada's East Coast also contributes to demand.

- Europe: Characterized by mature basin activity in the North Sea, necessitating extensive repair, maintenance, and decommissioning of aging infrastructure. Growth is increasingly propelled by gas import pipelines and pioneering projects in hydrogen and CCUS.

- Asia Pacific (APAC): Represents a rapidly expanding market due to escalating energy demand, new discoveries in Southeast Asia (e.g., Malaysia, Indonesia, Vietnam), Australia, and ongoing infrastructure development in China and India, particularly for gas.

- Latin America: Dominated by Brazil's prolific pre-salt deepwater discoveries, driving substantial investment in complex subsea infrastructure. Mexico and Guyana are also emerging as key contributors to regional pipeline demand.

- Middle East and Africa (MEA): Features robust growth fueled by vast offshore oil and gas reserves, significant state-backed investments in new production facilities, and strategic pipeline projects aimed at enhancing export capabilities and regional energy security, particularly in the Persian Gulf and West Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Offshore Pipeline Infrastructure Market.- Global Offshore Solutions

- Hydrocarbon Infrastructure Corp.

- Deepwater Energy Systems

- Maritime Pipeline Group

- Subsea Construction Services

- Integrated Offshore Pipelines

- Energy Infrastructure Solutions

- Oceanic Transport Systems

- Pipeline Engineering & Construction

- Apex Subsea Technologies

- Horizon Offshore Projects

- Sentinel Pipeline Management

- Titan Offshore Structures

- Polaris Marine Solutions

- Guardian Offshore Infrastructure

- North Sea Pipeline Ltd.

- Gulf Coast Subsea

- Asia Pacific Marine Pipelines

- Brazilian Offshore Services

- West African Pipeline Consortium

Frequently Asked Questions

Analyze common user questions about the Offshore Pipeline Infrastructure market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is offshore pipeline infrastructure?

Offshore pipeline infrastructure refers to the network of pipes, associated components, and support systems used to transport oil, natural gas, and other fluids from offshore production facilities to onshore processing plants or other offshore installations. It includes pipelines, risers, manifolds, pumps, valves, and monitoring systems.

Why is offshore pipeline infrastructure important?

It is crucial for global energy supply, enabling the efficient and safe transportation of resources from remote offshore fields to consumers. It supports energy security, facilitates international trade, and is essential for developing new energy sources like offshore wind and emerging technologies such as carbon capture and hydrogen transport.

What are the key types of offshore pipelines?

Offshore pipelines are primarily categorized by the type of fluid transported (oil, gas, or other fluids like water injection), material used (steel, composites), diameter, and the water depth at which they are installed (shallow, deep, or ultra-deepwater).

What are the main challenges in offshore pipeline construction?

Key challenges include operating in harsh marine environments, managing high capital costs, adhering to stringent environmental regulations, ensuring structural integrity under extreme pressures and temperatures, and mitigating geopolitical risks or supply chain disruptions.

How is technology impacting the offshore pipeline market?

Technological advancements, particularly in digitalization, AI, robotics, and advanced materials, are significantly impacting the market by enhancing operational efficiency, improving safety, enabling predictive maintenance, optimizing route planning, and reducing environmental footprints. These innovations are critical for navigating complex offshore projects and extending asset lifespan.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted