Mobile Edge Computing Market

Mobile Edge Computing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703983 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Mobile Edge Computing Market Size

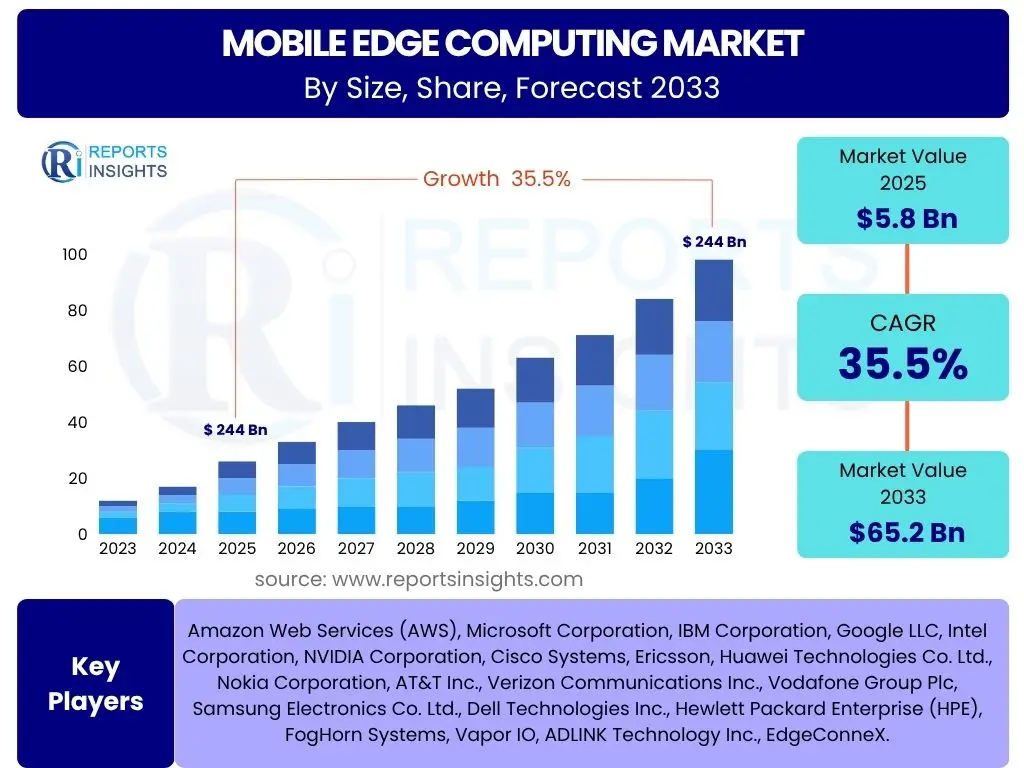

According to Reports Insights Consulting Pvt Ltd, The Mobile Edge Computing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 35.5% between 2025 and 2033. This impressive growth is indicative of the increasing demand for ultra-low latency, high bandwidth, and real-time data processing capabilities at the network edge. The fundamental shift towards decentralized computing infrastructure, driven by the proliferation of IoT devices and data-intensive applications, is a primary catalyst for this market expansion.

The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 65.2 Billion by the end of the forecast period in 2033. This significant valuation increase underscores the transformative potential of Mobile Edge Computing (MEC) across various industries. Investments in 5G infrastructure, coupled with the rising adoption of Artificial Intelligence (AI) and Machine Learning (ML) at the edge, are expected to fuel substantial market acceleration.

The rapid digital transformation initiatives globally, particularly within smart cities, industrial automation, and augmented reality/virtual reality (AR/VR) applications, are creating robust opportunities for MEC deployment. As enterprises seek to enhance operational efficiency, reduce data transfer costs, and improve application responsiveness, MEC emerges as a critical enabler, solidifying its position as a pivotal technology for the next generation of connected services.

Key Mobile Edge Computing Market Trends & Insights

Analysis of common user questions reveals a strong interest in how Mobile Edge Computing (MEC) is evolving and its practical implications for various sectors. Users frequently inquire about the symbiotic relationship between MEC and 5G technology, the role of MEC in enabling advanced IoT applications, and its contribution to real-time data processing needs. There is also significant curiosity regarding the adoption patterns across industries and the emergence of new business models facilitated by edge infrastructure.

A prominent trend observed is the deep integration of MEC with 5G networks, which provides the necessary high bandwidth and ultra-low latency connectivity crucial for edge applications. This synergy is unlocking new possibilities for real-time analytics, critical communications, and enhanced user experiences. Another key insight is the increasing demand for MEC solutions in industrial settings, where it supports Industry 4.0 initiatives by enabling localized data processing for automation, predictive maintenance, and quality control.

Furthermore, the market is witnessing a surge in interest from content delivery networks (CDNs) and gaming platforms seeking to reduce latency and improve content streaming performance. The trend towards deploying Artificial Intelligence workloads directly at the edge for immediate insights and decision-making, rather than relying solely on centralized cloud resources, is also gaining significant momentum. This distributed AI approach addresses data privacy concerns and reduces network backhaul, offering a more efficient and secure computing paradigm.

- Enhanced 5G and MEC Synergy: Accelerating deployment of edge nodes alongside 5G rollout for ultra-low latency services.

- Proliferation of IoT Devices: Driving the need for localized data processing and real-time analytics at the edge.

- Rise of Edge AI and Machine Learning: Shifting AI/ML model inference and training closer to data sources for immediate insights.

- Demand for Real-time Applications: Increasing adoption in autonomous vehicles, AR/VR, and critical infrastructure monitoring.

- Industry 4.0 and Smart Manufacturing: MEC facilitating localized control, data processing, and predictive maintenance in factories.

- Decentralized Content Delivery: Optimizing content streaming and gaming experiences through edge caching and processing.

- Focus on Data Privacy and Security: Edge computing minimizing data transit, enhancing control over sensitive information.

- Development of Open-Source Edge Platforms: Fostering innovation and interoperability within the MEC ecosystem.

AI Impact Analysis on Mobile Edge Computing

User inquiries regarding the impact of Artificial Intelligence (AI) on Mobile Edge Computing (MEC) frequently center on how AI can optimize edge infrastructure, enable intelligent applications at the edge, and address data processing challenges. Common concerns include the complexity of deploying AI models on resource-constrained edge devices, the need for robust data governance, and the potential for AI to enhance MEC's capabilities in areas like security and network management. There is also significant interest in the emerging use cases where the combination of AI and MEC delivers transformative value.

The integration of AI fundamentally transforms MEC by enabling more intelligent, autonomous, and efficient edge operations. AI algorithms can optimize resource allocation, predict network congestion, and automate maintenance tasks within MEC environments, leading to improved performance and reduced operational costs. Furthermore, running AI inferences at the edge significantly reduces latency for applications requiring real-time decision-making, such as autonomous vehicles, smart surveillance, and industrial automation. This localized AI processing minimizes data transfer to the cloud, enhancing privacy and security, and reducing bandwidth consumption.

Beyond operational efficiencies, AI at the edge is a critical enabler for advanced applications that leverage distributed intelligence. For instance, AI-powered computer vision systems deployed on edge devices can perform real-time anomaly detection in manufacturing plants or public spaces without sending vast amounts of video data to a central cloud. Similarly, machine learning models running on MEC infrastructure can personalize user experiences in retail or gaming, adapting in real-time based on local data. This symbiotic relationship between AI and MEC is poised to drive innovation across numerous industries, making edge intelligence a cornerstone of future digital ecosystems.

- Intelligent Resource Management: AI algorithms optimize computing, storage, and network resources at the edge for peak efficiency.

- Enhanced Data Processing and Analytics: AI enables real-time insights from raw edge data, supporting immediate decision-making.

- Autonomous Edge Applications: Facilitating self-driving vehicles, smart robots, and intelligent drones with localized AI processing.

- Predictive Maintenance: AI models at the edge analyze sensor data to predict equipment failures, reducing downtime and costs.

- Improved Network Optimization: AI assists in dynamic traffic management and routing at the edge for better network performance.

- Advanced Security Capabilities: AI-powered threat detection and anomaly identification directly at the edge to prevent cyberattacks.

- Personalized User Experiences: Edge AI supports real-time adaptation and customization for retail, gaming, and entertainment applications.

Key Takeaways Mobile Edge Computing Market Size & Forecast

Common user questions about the key takeaways from the Mobile Edge Computing (MEC) market size and forecast consistently highlight a focus on understanding the market's growth drivers, its long-term viability, and its impact across different industries. Users are keen to identify the most promising investment areas, the critical technological advancements shaping the market, and the overall strategic importance of MEC in the evolving digital landscape. The queries often reflect a desire for concise, actionable insights into where the market is headed.

A primary takeaway from the market size and forecast data is the explosive growth trajectory anticipated for Mobile Edge Computing, indicating its transition from an emerging technology to a foundational infrastructure component. This rapid expansion is not merely speculative but is underpinned by concrete technological advancements like 5G deployment, the proliferation of IoT devices, and the increasing sophistication of AI applications that demand ultra-low latency processing. The market's significant Compound Annual Growth Rate (CAGR) underscores its compelling potential for stakeholders across the technology ecosystem.

Furthermore, the analysis reveals MEC as a pivotal technology for enabling next-generation digital services and applications that require real-time processing and localized intelligence. Its ability to reduce bandwidth consumption, enhance data security, and improve application responsiveness positions it as an indispensable element for sectors ranging from manufacturing and healthcare to smart cities and autonomous systems. This makes MEC a strategic investment area for enterprises seeking to future-proof their operations and capitalize on the burgeoning opportunities presented by decentralized computing paradigms.

- Exceptional Market Growth: Mobile Edge Computing is poised for exponential growth, driven by increasing demand for low-latency processing.

- Fundamental Enabler for 5G and IoT: MEC is critical for realizing the full potential of 5G networks and scaling IoT deployments.

- Strategic Investment Opportunity: The market presents lucrative prospects for technology providers, infrastructure developers, and service integrators.

- Transformative Impact Across Industries: MEC is set to revolutionize operations in manufacturing, healthcare, smart cities, and autonomous systems.

- Decentralized Computing Imperative: A clear shift towards processing data closer to the source to enhance efficiency, security, and responsiveness.

Mobile Edge Computing Market Drivers Analysis

The Mobile Edge Computing market is propelled by a confluence of technological advancements and evolving business requirements that necessitate faster, more efficient data processing capabilities. These drivers collectively create a compelling need for edge infrastructure, pushing enterprises and service providers to invest in distributed computing solutions. The demand for immediate insights from data generated at the source, coupled with the limitations of traditional cloud-centric models for certain applications, is accelerating MEC adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of IoT Devices and Data | +5.5% | Global (APAC, North America) | Medium-term (3-5 years) |

| Increasing Demand for Ultra-Low Latency | +4.8% | Global (North America, Europe, China) | Short-term (1-3 years) |

| Rollout of 5G Networks | +6.2% | Global (All Regions, with varied pace) | Medium-term (3-5 years) |

| Growth of Data-Intensive Applications (AR/VR, AI) | +4.5% | Global (Developed Economies) | Medium-term (3-5 years) |

| Enhanced Data Security and Privacy Requirements | +3.9% | Global (Europe - GDPR, North America) | Short-term (1-3 years) |

| Shift Towards Industry 4.0 and Smart Manufacturing | +4.1% | Europe, North America, APAC (Japan, South Korea) | Long-term (5-8 years) |

Mobile Edge Computing Market Restraints Analysis

Despite its significant growth potential, the Mobile Edge Computing market faces several formidable restraints that could impede its widespread adoption and dampen its projected growth. These challenges often relate to the inherent complexities of deploying and managing distributed infrastructure, alongside concerns about security, standardization, and the economic viability of certain deployments. Addressing these restraints is crucial for the market to realize its full potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Deployment and Operational Costs | -2.8% | Global (SMEs, Developing Regions) | Medium-term (3-5 years) |

| Security and Data Governance Concerns | -3.5% | Global (Highly Regulated Industries) | Short-term (1-3 years) |

| Interoperability and Standardization Issues | -2.1% | Global (Multi-vendor Environments) | Long-term (5-8 years) |

| Lack of Skilled Professionals | -1.9% | Global (All Regions) | Medium-term (3-5 years) |

| Complexities of Edge Infrastructure Management | -2.3% | Global (Large-scale Deployments) | Short-term (1-3 years) |

Mobile Edge Computing Market Opportunities Analysis

The Mobile Edge Computing market presents a myriad of opportunities driven by technological innovation, the emergence of new use cases, and the increasing need for localized computing across diverse sectors. These opportunities often stem from the current limitations of centralized cloud computing for latency-sensitive or bandwidth-intensive applications, positioning MEC as a vital enabler for the next wave of digital transformation. Strategic alliances and the development of specialized solutions are key avenues for market participants to capitalize on these emerging trends.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Use Cases (e.g., Autonomous Vehicles, AR/VR) | +5.1% | Global (North America, Europe, APAC) | Long-term (5-8 years) |

| Expansion into New Industry Verticals (e.g., Healthcare, Retail) | +4.3% | Global (All Regions) | Medium-term (3-5 years) |

| Development of Open-Source Edge Platforms and Ecosystems | +3.8% | Global (Technology Hubs) | Medium-term (3-5 years) |

| Strategic Partnerships and Collaborations among Key Players | +4.0% | Global (Cross-Industry) | Short-term (1-3 years) |

| Growth in Private 5G Networks and On-Premise Edge Deployments | +4.6% | Europe, North America, APAC (Industrial Sector) | Medium-term (3-5 years) |

Mobile Edge Computing Market Challenges Impact Analysis

While the Mobile Edge Computing market holds immense promise, it is not without its significant challenges that could hinder its full potential and slow down adoption. These challenges range from technical complexities in deploying and managing distributed infrastructure to regulatory hurdles and concerns about data sovereignty. Overcoming these obstacles requires concerted efforts from technology providers, policymakers, and industry consortiums to develop robust solutions, establish common standards, and foster a more mature ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Privacy and Sovereignty Concerns | -2.5% | Global (Europe - GDPR, China) | Short-term (1-3 years) |

| Network Congestion and Bandwidth Management at the Edge | -1.8% | Global (Dense Urban Areas) | Short-term (1-3 years) |

| Vendor Lock-in and Proprietary Solutions | -2.0% | Global (Enterprise Sector) | Medium-term (3-5 years) |

| Power Consumption and Environmental Impact | -1.5% | Global (Hyperscale Deployments) | Long-term (5-8 years) |

| Integration Complexities with Existing Infrastructure | -2.2% | Global (Legacy Systems) | Medium-term (3-5 years) |

Mobile Edge Computing Market - Updated Report Scope

This updated report provides an in-depth analysis of the global Mobile Edge Computing (MEC) market, encompassing its current landscape, historical performance, and future projections. It delves into the market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report aims to offer comprehensive insights for stakeholders to make informed strategic decisions within this rapidly evolving technological domain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 65.2 Billion |

| Growth Rate | 35.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Corporation, IBM Corporation, Google LLC, Intel Corporation, NVIDIA Corporation, Cisco Systems, Ericsson, Huawei Technologies Co. Ltd., Nokia Corporation, AT&T Inc., Verizon Communications Inc., Vodafone Group Plc, Samsung Electronics Co. Ltd., Dell Technologies Inc., Hewlett Packard Enterprise (HPE), FogHorn Systems, Vapor IO, ADLINK Technology Inc., EdgeConneX. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Mobile Edge Computing market is segmented across various dimensions to provide a granular understanding of its diverse landscape and growth drivers. These segmentations by component, application, and end-user illuminate how different facets of the MEC ecosystem contribute to market expansion and address specific industry needs. Analyzing these segments helps identify key areas of investment and innovation, offering a comprehensive view of the market's structure and operational dynamics.

The component segment differentiates between the hardware infrastructure, software platforms, and professional services required for MEC deployment. Each component plays a critical role, from the physical edge devices and servers to the sophisticated software that manages and orchestrates workloads, and the specialized services that facilitate successful integration and ongoing operation. Understanding the growth within each component provides insights into the technological building blocks driving MEC adoption.

Furthermore, the application and end-user segmentations highlight the diverse industries and specific use cases benefiting from MEC capabilities. This ranges from enabling ultra-low latency applications in autonomous vehicles and immersive AR/VR experiences, to optimizing industrial operations and enhancing smart city initiatives. The varied adoption across sectors like manufacturing, healthcare, and retail underscores MEC's versatility and its potential to revolutionize business processes by bringing computation closer to the source of data generation.

- By Component:

- Hardware: Servers, Routers, Gateways, Edge Devices (Sensors, Cameras, IoT endpoints)

- Software: Cloud RAN Software, Analytics Software, Security Software, Orchestration and Management Platforms, Edge AI Software

- Services: Consulting Services, Integration and Deployment Services, Managed Services, Support and Maintenance Services

- By Application:

- Smart Cities (Traffic Management, Public Safety, Smart Grid)

- Industrial IoT (Predictive Maintenance, Quality Control, Asset Tracking)

- Healthcare (Remote Patient Monitoring, Medical Imaging, Hospital Operations)

- Gaming & Entertainment (Cloud Gaming, Immersive Experiences)

- Augmented Reality/Virtual Reality (AR/VR)

- Content Delivery Networks (CDNs)

- Autonomous Vehicles (V2X Communication, Real-time Navigation)

- Drones & Robotics

- By End-User:

- Manufacturing

- Energy & Utilities

- Government & Public Sector

- Retail & E-commerce

- IT & Telecom

- Healthcare

- Transportation & Logistics

- Media & Entertainment

Regional Highlights

The global Mobile Edge Computing market exhibits distinct regional dynamics, influenced by varying levels of technological infrastructure, regulatory frameworks, industry adoption rates, and economic development. Each region presents unique opportunities and challenges for MEC deployment, reflecting a diverse landscape of innovation, investment, and market maturity. Understanding these regional nuances is essential for market participants to tailor their strategies effectively.

North America, particularly the United States, is a leading region in the MEC market, characterized by early adoption of advanced technologies, significant investments in 5G infrastructure, and a strong presence of key technology providers and cloud service giants. The region's robust innovation ecosystem, coupled with high demand for low-latency applications in areas like autonomous vehicles and enterprise edge, positions it at the forefront of MEC development and deployment.

Asia Pacific (APAC) is projected to be one of the fastest-growing regions, driven by rapid digitalization initiatives, extensive 5G network rollouts, and booming industrial IoT and smart city projects in countries like China, Japan, and South Korea. The region's massive population and increasing mobile data consumption further contribute to the demand for localized computing resources. Europe also demonstrates significant growth, fueled by strong industrial automation trends, favorable regulatory environments for data privacy, and a focus on digital transformation across various sectors.

- North America: Leads in MEC adoption due to early 5G deployment, significant R&D investments, and strong presence of major cloud and telecom providers. High demand from autonomous vehicles, enterprise edge, and media content delivery.

- Europe: Driven by Industry 4.0 initiatives, stringent data privacy regulations (GDPR) encouraging localized processing, and robust telecom infrastructure. Focus on industrial automation, smart manufacturing, and smart city projects.

- Asia Pacific (APAC): Fastest-growing market propelled by rapid 5G expansion, massive IoT deployments, and government-backed smart city projects in countries like China, Japan, South Korea, and India. Large scale digitalization and mobile user base.

- Latin America: Emerging market with increasing investments in digital infrastructure and growing awareness of edge computing benefits. Opportunities exist in telecom and specific industrial applications as 5G adoption progresses.

- Middle East and Africa (MEA): Characterized by nascent but growing digital transformation initiatives, particularly in smart city development and critical infrastructure modernization. Significant potential as 5G networks and IoT adoption expand across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mobile Edge Computing Market.- Amazon Web Services (AWS)

- Microsoft Corporation

- IBM Corporation

- Google LLC

- Intel Corporation

- NVIDIA Corporation

- Cisco Systems, Inc.

- Ericsson

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- AT&T Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- Samsung Electronics Co. Ltd.

- Dell Technologies Inc.

- Hewlett Packard Enterprise (HPE)

- FogHorn Systems

- Vapor IO

- ADLINK Technology Inc.

- EdgeConneX

Frequently Asked Questions

Common user questions about the Mobile Edge Computing market and generate a concise list of summarized FAQs reflecting key topics and concerns.

What is Mobile Edge Computing (MEC)?

Mobile Edge Computing (MEC), also known as Multi-access Edge Computing, is a network architecture concept that enables cloud computing capabilities and an IT service environment at the edge of the cellular network. This brings applications and data processing closer to the mobile user or data source, significantly reducing latency, improving bandwidth efficiency, and enhancing real-time data analysis.

How does MEC differ from traditional cloud computing?

While traditional cloud computing centralizes data processing in remote data centers, MEC decentralizes it, pushing computation and storage to the network's edge, closer to end-users and IoT devices. This proximity minimizes data travel distance, drastically reduces latency, and conserves bandwidth, making it ideal for real-time, mission-critical, and data-intensive applications that traditional cloud models cannot efficiently support.

What are the primary benefits of implementing MEC?

Implementing MEC offers several key benefits: ultra-low latency for critical applications, enhanced bandwidth efficiency by processing data locally, improved data privacy and security through localized processing, greater reliability and resilience due to distributed infrastructure, and the enablement of new real-time applications such as autonomous vehicles, augmented reality, and industrial automation.

Which industries are most impacted by Mobile Edge Computing?

Mobile Edge Computing is poised to significantly impact various industries, including manufacturing (for Industry 4.0 and predictive maintenance), healthcare (for remote monitoring and real-time diagnostics), transportation (for autonomous vehicles and traffic management), gaming and entertainment (for immersive AR/VR experiences and cloud gaming), and smart cities (for public safety, smart grids, and intelligent infrastructure).

What are the main challenges for MEC adoption?

Key challenges for MEC adoption include high initial deployment and operational costs for new infrastructure, ensuring robust security and data governance across distributed nodes, achieving interoperability and standardization among diverse vendor solutions, and addressing the current shortage of skilled professionals required for design and management of edge environments. Overcoming these challenges is crucial for widespread MEC proliferation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted