Cloud High Performance Computing Market

Cloud High Performance Computing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704184 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

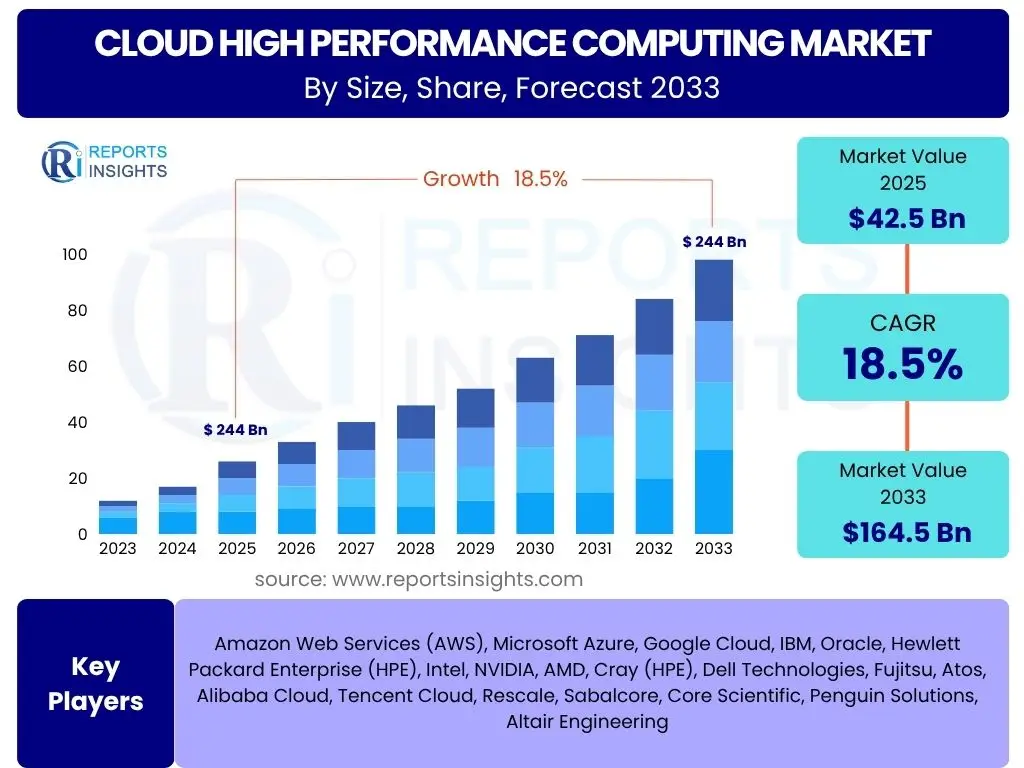

Cloud High Performance Computing Market Size

According to Reports Insights Consulting Pvt Ltd, The Cloud High Performance Computing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 42.5 billion in 2025 and is projected to reach USD 164.5 billion by the end of the forecast period in 2033. This robust growth trajectory is underpinned by the increasing demand for scalable and on-demand computing resources across various industries. The shift from traditional on-premise HPC infrastructure to flexible cloud-based solutions is a primary factor contributing to this expansion, driven by enhanced accessibility, cost-efficiency, and the ability to handle highly complex computational tasks without significant capital expenditure.

Key Cloud High Performance Computing Market Trends & Insights

The Cloud High Performance Computing market is experiencing dynamic shifts, reflecting evolving user needs for advanced computational capabilities. Users frequently inquire about the leading trends shaping market growth, particularly concerning the adoption patterns, technological advancements, and operational efficiencies offered by cloud-based HPC solutions. Key insights reveal a significant migration from traditional on-premise HPC setups to more agile cloud environments, driven by the need for scalability, cost-effectiveness, and faster innovation cycles. The market is also heavily influenced by the increasing complexity of data-intensive workloads and the growing integration of artificial intelligence and machine learning applications, which demand elastic and powerful computing resources.

Furthermore, there is a pronounced trend towards hybrid and multi-cloud strategies, allowing organizations to leverage the best of both worlds by combining on-premise security and control with cloud flexibility for burstable workloads. This approach helps in optimizing resource utilization and managing sensitive data while still benefiting from the vast computational power of the cloud. The continuous development of specialized hardware accelerators like GPUs, FPGAs, and ASICs within cloud infrastructures is another critical trend, catering to the performance demands of specific high-intensity applications such as scientific simulations, genomic analysis, and advanced financial modeling. These developments are directly addressing common user concerns about performance parity with traditional HPC.

- Significant shift from on-premise HPC to cloud-based solutions for enhanced scalability and flexibility.

- Growing adoption of hybrid and multi-cloud strategies to optimize workload management and data security.

- Increasing integration of AI and Machine Learning workloads, necessitating specialized cloud HPC capabilities.

- Rising demand for specialized hardware accelerators (GPUs, FPGAs, ASICs) in cloud environments.

- Emphasis on serverless and containerized HPC solutions for improved agility and resource utilization.

- Focus on sustainability and energy efficiency in cloud HPC infrastructure development.

- Expansion of cloud HPC services to cater to niche applications in manufacturing, healthcare, and finance.

AI Impact Analysis on Cloud High Performance Computing

Artificial intelligence is profoundly reshaping the Cloud High Performance Computing landscape, leading to frequent user inquiries about the synergistic relationship between these two domains. Users commonly seek to understand how AI applications leverage cloud HPC resources, the specific architectural demands placed by AI workloads, and the future implications for both AI development and HPC infrastructure. AI's insatiable demand for computational power, particularly during the training phase of complex machine learning models and deep learning networks, positions cloud HPC as an indispensable backbone. Cloud HPC provides the elastic scalability and specialized hardware (like powerful GPUs and TPUs) necessary to process vast datasets and execute computationally intensive AI algorithms, making advanced AI research and deployment accessible to a broader range of organizations.

The impact extends beyond mere resource provision; AI is also influencing the evolution of cloud HPC architectures itself. There is a growing focus on optimizing cloud environments for AI/ML specific workloads, leading to the development of tailored services, frameworks, and interconnect technologies. This includes advancements in data transfer speeds, specialized AI-optimized virtual machines, and managed services that streamline the AI development lifecycle. As AI becomes more pervasive across industries, the demand for robust, secure, and highly available cloud HPC will continue to accelerate, driving innovation in both software and hardware within the cloud ecosystem to meet the escalating computational requirements of next-generation AI applications.

- AI and Machine Learning workloads are significant drivers for cloud HPC demand, especially for model training and inference.

- Cloud HPC provides the scalable computational resources, including GPUs and TPUs, essential for complex AI algorithm execution.

- AI drives innovation in cloud HPC architecture, fostering development of AI-optimized infrastructure and services.

- The synergy between AI and cloud HPC accelerates research and development in various AI subfields.

- Increased focus on data transfer optimization and low-latency networks within cloud HPC for AI applications.

- AI is enabling more intelligent resource management and automation within cloud HPC platforms.

Key Takeaways Cloud High Performance Computing Market Size & Forecast

User queries regarding the Cloud High Performance Computing market size and forecast consistently aim to distill the most critical insights that can inform strategic decisions. The overarching takeaway is the undeniable trajectory of significant expansion, projecting the market to more than quadruple in value within the next eight years. This robust growth underscores the increasing reliance of enterprises, research institutions, and governments on flexible, scalable, and powerful cloud-based computational resources to drive innovation, accelerate research, and manage complex data workloads. The shift away from capital-intensive on-premise systems towards operational expenditure models in the cloud is a fundamental driver of this forecast.

Furthermore, the forecast highlights the transformative impact of emerging technologies, particularly Artificial Intelligence and Machine Learning, as major catalysts for cloud HPC adoption. The market’s momentum is also strongly influenced by the accessibility it provides to advanced computing capabilities for organizations of all sizes, democratizing high-performance computing. Despite potential challenges related to data security and migration complexities, the inherent benefits of scalability, cost-efficiency, and on-demand access position cloud HPC as a cornerstone for future technological advancements and economic competitiveness across diverse industries globally.

- The Cloud High Performance Computing market is poised for exceptional growth, demonstrating a CAGR of 18.5% through 2033.

- Market valuation is projected to increase from USD 42.5 billion in 2025 to USD 164.5 billion by 2033.

- The expansion is primarily fueled by the increasing demand for scalable and cost-effective computational power across industries.

- Integration of AI and Machine Learning workloads is a significant accelerator for cloud HPC adoption.

- Democratization of advanced computing resources for Small and Medium-sized Enterprises (SMEs) is a key market trend.

- Continued innovation in cloud infrastructure and specialized hardware will sustain market momentum.

Cloud High Performance Computing Market Drivers Analysis

The Cloud High Performance Computing market is propelled by a confluence of powerful drivers stemming from the evolving needs of modern enterprises and research institutions. A primary driver is the escalating demand for high-performance computing capabilities across diverse industries, ranging from scientific research and engineering to financial modeling and media rendering. Organizations are increasingly facing computationally intensive tasks that surpass the capacities of traditional IT infrastructure, making cloud HPC an attractive solution for its on-demand scalability and access to cutting-edge resources. This widespread need for greater processing power to handle complex simulations, data analytics, and modeling is a fundamental growth catalyst.

Another significant driver is the rapid proliferation and integration of Artificial Intelligence and Machine Learning technologies. AI/ML workloads, particularly deep learning model training, require immense computational resources and specialized hardware like GPUs, which cloud HPC providers can offer on a flexible, pay-as-you-go basis. This accessibility enables more organizations to embark on AI initiatives without prohibitive upfront investments. Furthermore, the inherent benefits of cloud infrastructure, such as cost-effectiveness, reduced IT overhead, and the ability to scale resources up or down as needed, provide compelling incentives for businesses to migrate their HPC workloads to the cloud, contributing significantly to market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for high-performance computing in diverse industries | +3.0% | Global | 2025-2033 |

| Growing adoption of AI and Machine Learning workloads | +2.8% | North America, Europe, APAC | 2025-2033 |

| Cost-effectiveness and scalability benefits of cloud infrastructure | +2.5% | Global | 2025-2033 |

| Rise in complex data analytics and big data processing requirements | +2.2% | Global | 2025-2030 |

| Enhanced accessibility to advanced computing resources for SMEs | +1.8% | Emerging Markets | 2025-2033 |

Cloud High Performance Computing Market Restraints Analysis

Despite its significant growth potential, the Cloud High Performance Computing market faces several restraints that could temper its expansion. A primary concern for many organizations is data security and privacy. Migrating sensitive or proprietary data to a public cloud environment raises questions about data sovereignty, compliance with industry regulations, and the potential for unauthorized access. While cloud providers invest heavily in security measures, perception and trust remain significant hurdles, particularly for industries handling highly confidential information like healthcare, finance, or government defense. Addressing these concerns through robust security frameworks and transparent practices is crucial for broader adoption.

Another notable restraint is the high initial investment and perceived operational costs for some users, especially those accustomed to predictable on-premise expenditures. While cloud HPC offers long-term cost efficiencies through reduced hardware procurement and maintenance, the transition itself can be complex and expensive, involving data migration, re-architecting applications, and staff training. Furthermore, latency and network bandwidth limitations can be a significant bottleneck for certain HPC applications that require extremely low-latency communication between compute nodes or rapid transfer of massive datasets. This is particularly relevant for tightly coupled simulations where slight delays can impact performance, making full cloud migration less appealing for specific high-intensity workloads and thus restraining market growth in certain segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data security and privacy concerns | -2.5% | Global | 2025-2030 |

| High initial investment and operational costs for some users | -2.0% | SMEs, Emerging Markets | 2025-2028 |

| Latency and network bandwidth limitations | -1.8% | Remote Geographies | 2025-2030 |

| Complexity in migrating legacy HPC workloads to the cloud | -1.5% | Large Enterprises | 2025-2029 |

| Lack of skilled personnel for cloud HPC management | -1.2% | Global | 2025-2033 |

Cloud High Performance Computing Market Opportunities Analysis

The Cloud High Performance Computing market is ripe with opportunities that promise to accelerate its expansion and diversification. A significant avenue for growth lies in the continuous development of specialized cloud HPC services and platforms tailored to specific industry needs. As cloud providers offer more granular control, optimized software stacks, and pre-configured environments for fields like genomics, automotive design, or weather forecasting, the barrier to entry for specialized HPC users diminishes. This customization reduces the complexity of setting up and managing HPC workloads in the cloud, making it more appealing to a broader range of enterprises and research institutions.

Furthermore, the emergence of and potential integration with cutting-edge technologies like quantum computing and edge computing presents substantial future opportunities. While still nascent, quantum computing, when mature, will demand hybrid architectures where classical HPC complements quantum processors, likely in a cloud environment due to their complex operational requirements. Similarly, edge computing can distribute computational tasks closer to data sources, reducing latency for certain applications, and cloud HPC can serve as the central processing hub for aggregated or intensive workloads. The expansion into new end-use industries, such as broader applications in retail, media, and even gaming, where high-fidelity simulations and rapid data processing are becoming critical, also offers untapped market potential. Lastly, a growing global focus on sustainability is driving demand for "green HPC," where cloud providers with efficient, renewable-energy-powered data centers can offer significant advantages, creating new market segments and competitive differentiation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of specialized cloud HPC services and platforms | +2.0% | Global | 2025-2033 |

| Integration with emerging technologies like quantum computing and edge computing | +1.8% | North America, Europe | 2028-2033 |

| Expansion into new end-use industries such as retail and media | +1.5% | Global | 2025-2030 |

| Growing focus on sustainability and green HPC solutions | +1.2% | Europe, North America | 2025-2033 |

| Hybrid cloud strategies enabling flexible workload distribution | +1.0% | Global | 2025-2033 |

Cloud High Performance Computing Market Challenges Impact Analysis

The Cloud High Performance Computing market, while dynamic, faces several significant challenges that require strategic navigation for sustained growth. One prominent challenge is ensuring data sovereignty and compliance across different regional jurisdictions. As data flows across borders and resides in various cloud data centers, organizations must adhere to diverse and often stringent data protection regulations, such as GDPR in Europe or specific data residency laws in other nations. Navigating this complex regulatory landscape adds layers of complexity and cost, particularly for multinational corporations or those operating in highly regulated sectors.

Another critical challenge is the escalating cost of data transfer, commonly known as "egress fees." While processing and storage in the cloud can be cost-effective, moving large volumes of data out of the cloud back to on-premise systems or to another cloud provider can incur substantial charges, leading to unpredictable operational expenses. This can deter organizations from fully embracing cloud HPC, especially for applications that frequently move massive datasets. Furthermore, concerns about vendor lock-in remain prevalent, as migrating complex HPC workflows and large datasets from one cloud provider to another can be a formidable task, involving significant time, effort, and potential disruption. This creates a reliance on a single provider, limiting an organization's flexibility and bargaining power. Addressing these challenges effectively will be vital for the continued healthy expansion and broader adoption of cloud HPC solutions across all market segments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring data sovereignty and compliance across different regions | -1.5% | Europe, Asia Pacific | 2025-2033 |

| Managing escalating data transfer costs (egress fees) | -1.3% | Global | 2025-2030 |

| Vendor lock-in concerns and interoperability issues | -1.0% | Global | 2025-2033 |

| Optimizing resource utilization and cost-efficiency for burst workloads | -0.8% | Global | 2025-2030 |

| Addressing the talent gap for specialized cloud HPC expertise | -0.7% | Global | 2025-2033 |

Cloud High Performance Computing Market - Updated Report Scope

This comprehensive market insights report meticulously analyzes the Cloud High Performance Computing market, providing an in-depth understanding of its current landscape and future trajectory. The report delineates key market attributes, including historical performance, current market size, and future projections, offering a detailed segmentation breakdown by component, deployment model, organization size, end-use industry, and application. It also covers the geographical spread of the market, identifying key regional contributions and growth pockets. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making, competitive analysis, and identifying emerging opportunities within the cloud HPC domain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 42.5 Billion |

| Market Forecast in 2033 | USD 164.5 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM, Oracle, Hewlett Packard Enterprise (HPE), Intel, NVIDIA, AMD, Cray (HPE), Dell Technologies, Fujitsu, Atos, Alibaba Cloud, Tencent Cloud, Rescale, Sabalcore, Core Scientific, Penguin Solutions, Altair Engineering |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cloud High Performance Computing market is meticulously segmented to provide a granular view of its diverse landscape and to understand the various factors influencing its growth across different dimensions. These segmentations allow for a comprehensive analysis of adoption patterns, technological preferences, and industry-specific demands. Understanding these segments is crucial for stakeholders to identify niche markets, tailor service offerings, and develop targeted strategies that align with specific user requirements and operational models.

The market's segmentation by component differentiates between the core solutions offered, such as Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), and the supporting services like professional and managed services. Deployment models highlight the preference for public, private, or hybrid cloud environments, reflecting varying needs for control, security, and scalability. Organization size distinguishes between the distinct requirements and resource capacities of large enterprises versus Small and Medium-sized Enterprises (SMEs). Furthermore, segmentation by end-use industry provides insights into the vertical applications of cloud HPC, showcasing its utility across a broad spectrum of sectors from scientific research to entertainment. Finally, segmenting by application elucidates the specific computational tasks for which cloud HPC is predominantly utilized, such as AI/ML, genomic analysis, or engineering simulations, offering a detailed perspective on key use cases.

- By Component:

- Solutions: IaaS, PaaS, SaaS

- Services: Professional Services, Managed Services

- By Deployment Model:

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size:

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By End-use Industry:

- Academia & Research

- Government & Defense

- Manufacturing

- Healthcare & Life Sciences

- Financial Services

- Media & Entertainment

- Oil & Gas

- Retail & E-commerce

- Others

- By Application:

- Data Processing & Analytics

- Scientific Research

- Engineering Simulation

- Genomic Analysis

- Weather Modeling

- Financial Modeling

- Drug Discovery

- Artificial Intelligence/Machine Learning

- Deep Learning

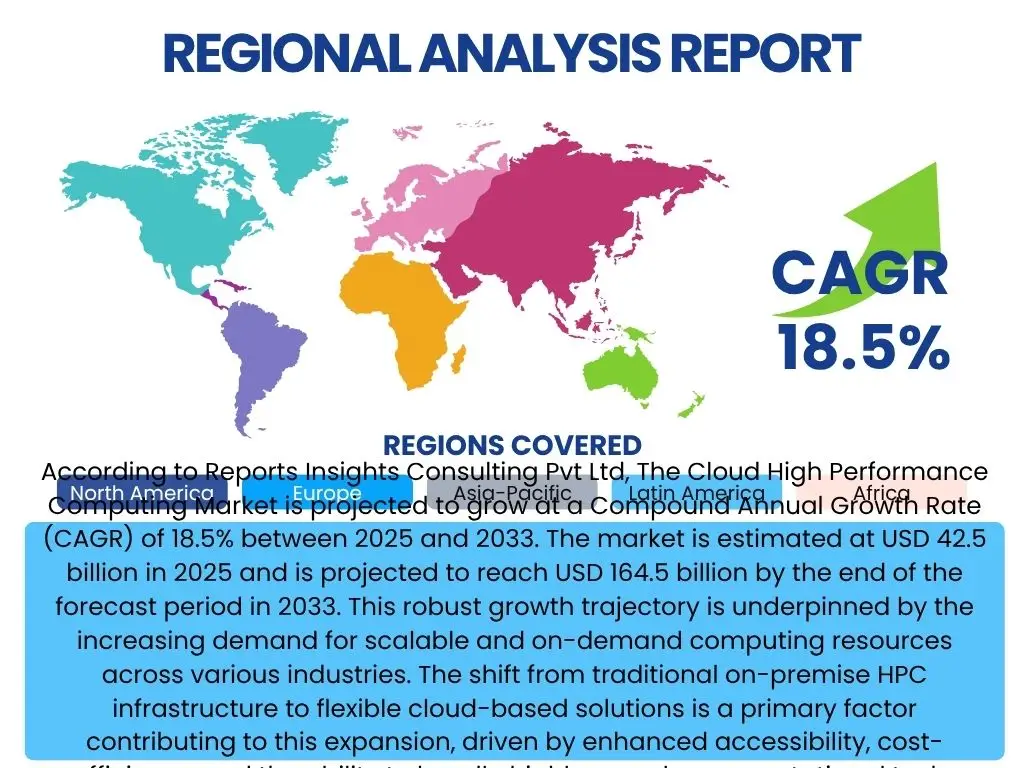

Regional Highlights

Regional analysis provides critical insights into the geographical distribution of Cloud High Performance Computing market growth and adoption trends, highlighting specific drivers and opportunities in different parts of the world. Each region exhibits unique characteristics influenced by technological infrastructure, regulatory environments, economic development, and the prevalence of industries that demand HPC capabilities. Understanding these regional nuances is essential for market participants to tailor their strategies, allocate resources effectively, and capitalize on localized growth opportunities.

North America currently leads the Cloud High Performance Computing market, driven by the presence of major cloud service providers, a robust technology ecosystem, significant R&D investments, and a high concentration of industries requiring advanced computational power, such as technology, healthcare, and financial services. The region benefits from early adoption of cloud technologies and strong government support for scientific research and innovation. Europe follows, with a strong emphasis on data privacy and sovereign cloud solutions, alongside substantial investments in scientific research and automotive manufacturing. Countries like Germany, France, and the UK are key contributors, driven by academic institutions and a growing interest in AI and big data analytics. The European Union's initiatives to foster digital sovereignty also influence the market's trajectory.

Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by rapid digitalization, increasing investments in R&D, and the burgeoning adoption of cloud technologies in countries like China, India, Japan, and South Korea. Emerging economies in this region are rapidly building their digital infrastructure and are keen to leverage cloud HPC for diverse applications in manufacturing, healthcare, and smart city initiatives. Latin America and the Middle East & Africa (MEA) are also emerging markets for cloud HPC, though at an earlier stage of adoption. Growth in these regions is primarily driven by expanding digital economies, increasing government focus on technology infrastructure development, and the need for scalable computing resources in sectors like oil & gas, financial services, and telecommunications. While starting from a smaller base, these regions represent significant long-term potential for market expansion as digital transformation accelerates.

- North America: Dominates the market due to the presence of major cloud providers, advanced technological infrastructure, and high adoption across diverse industries like technology, finance, and healthcare.

- Europe: Exhibits strong growth driven by robust research institutions, automotive and aerospace industries, and increasing investments in AI/ML, with a focus on data sovereignty and secure cloud solutions.

- Asia Pacific (APAC): Expected to be the fastest-growing region, propelled by rapid digitalization, significant R&D investments, and increasing cloud adoption in emerging economies like China, India, and Southeast Asia.

- Latin America: Shows nascent growth, with increasing interest in cloud HPC from financial services and resource extraction industries, driven by a growing digital economy.

- Middle East and Africa (MEA): Emerging market with potential in oil & gas, government, and telecommunications sectors, as regional governments invest in digital transformation and economic diversification.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cloud High Performance Computing Market.- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- IBM

- Oracle

- Hewlett Packard Enterprise (HPE)

- Intel

- NVIDIA

- AMD

- Cray (HPE)

- Dell Technologies

- Fujitsu

- Atos

- Alibaba Cloud

- Tencent Cloud

- Rescale

- Sabalcore

- Core Scientific

- Penguin Solutions

- Altair Engineering

Frequently Asked Questions

Analyze common user questions about the Cloud High Performance Computing market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary benefits of adopting Cloud HPC?

The primary benefits of adopting Cloud High Performance Computing include unparalleled scalability, allowing users to rapidly access vast computational resources on demand without large upfront capital expenditures. It offers cost-effectiveness through a pay-as-you-go model, reducing the need for purchasing and maintaining expensive on-premise hardware. Additionally, cloud HPC provides access to the latest hardware accelerators and diverse software environments, democratizing advanced computing capabilities for organizations of all sizes and accelerating innovation cycles.

How does Cloud HPC ensure data security?

Cloud HPC providers implement robust security measures, including strong encryption for data in transit and at rest, multi-factor authentication, network security (firewalls, VPNs), and stringent access controls. They also adhere to various compliance certifications (e.g., ISO 27001, HIPAA, GDPR) and offer tools for data loss prevention and threat detection. While the cloud provider secures the infrastructure, users are responsible for securing their data within that infrastructure, often referred to as the shared responsibility model.

What industries are major adopters of Cloud HPC?

Major adopters of Cloud High Performance Computing include academia and research institutions for scientific simulations and data analysis, healthcare and life sciences for drug discovery and genomic sequencing, manufacturing for complex engineering simulations and product design, and financial services for risk analysis and algorithmic trading. Additionally, government and defense sectors utilize cloud HPC for intelligence, weather modeling, and national security applications. Media and entertainment industries also leverage it for rendering and content creation.

What is the role of AI in the future of Cloud HPC?

AI is a pivotal force in the future of Cloud HPC. AI workloads, particularly deep learning model training, are inherently compute-intensive and drive the demand for scalable cloud HPC resources, especially specialized hardware like GPUs and TPUs. Cloud HPC provides the flexible infrastructure for AI development, while AI, in turn, can optimize cloud HPC resource management, scheduling, and energy efficiency, leading to more intelligent and automated HPC environments. This synergy will accelerate advancements in both fields.

How can organizations manage costs associated with Cloud HPC?

Organizations can manage Cloud HPC costs by optimizing resource utilization, using spot instances or reserved instances for predictable workloads, and employing auto-scaling to match compute resources with demand. Careful selection of instance types and storage solutions, monitoring usage with cost management tools, and implementing efficient data transfer strategies (minimizing egress fees) are crucial. Furthermore, leveraging hybrid cloud models can help balance workloads and costs, keeping sensitive or high-frequency data on-premise while bursting to the cloud for peak computational needs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted