Micro Data Center Market

Micro Data Center Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705229 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

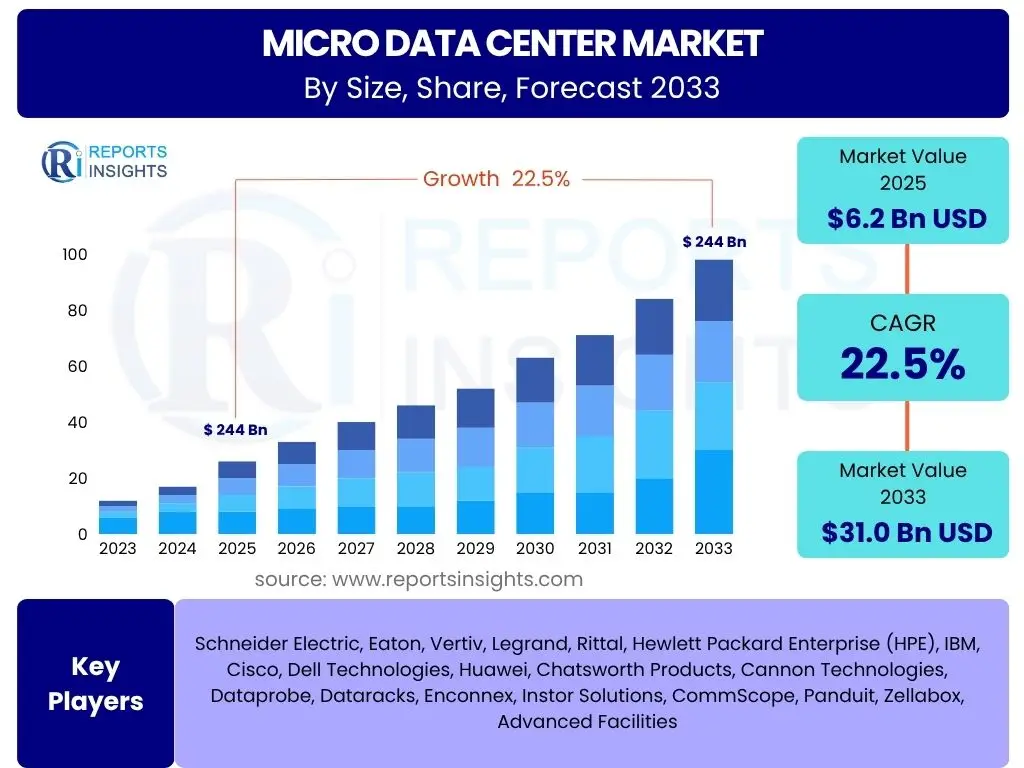

Micro Data Center Market Size

According to Reports Insights Consulting Pvt Ltd, The Micro Data Center Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market is estimated at $6.2 Billion USD in 2025 and is projected to reach $31.0 Billion USD by the end of the forecast period in 2033.

Key Micro Data Center Market Trends & Insights

The Micro Data Center market is currently shaped by several transformative trends, primarily driven by the increasing demand for localized data processing and reduced latency. Key inquiries from stakeholders often revolve around the evolution of edge computing, the integration of IoT devices, and the impact of 5G networks, all of which necessitate a more distributed IT infrastructure. Furthermore, there is a growing emphasis on modularity, scalability, and enhanced physical and cyber security within these compact environments, alongside a rising focus on energy efficiency and sustainability solutions. These trends collectively underscore a shift from centralized data processing to a more decentralized model, bringing computation closer to the source of data generation and consumption.

User interest also highlights the criticality of rapid deployment and ease of management for micro data centers. Businesses are seeking solutions that can be quickly installed in diverse, non-traditional IT environments, from remote industrial sites to retail branches and smart city infrastructure. This necessitates a trend towards pre-integrated, "plug-and-play" units that simplify deployment and reduce setup time. The ability to remotely monitor and manage these distributed assets efficiently is another significant area of inquiry, pointing towards the adoption of advanced Data Center Infrastructure Management (DCIM) tools and automation, ensuring operational continuity and minimizing the need for on-site IT personnel.

- Proliferation of Edge Computing: Driving demand for localized processing capabilities at the network edge.

- Rising IoT Device Adoption: Generating vast data volumes requiring immediate, localized analysis.

- 5G Network Expansion: Enabling ultra-low latency applications that benefit from edge infrastructure.

- Modular and Scalable Designs: Facilitating rapid deployment and flexible expansion based on demand.

- Enhanced Physical and Cyber Security: Addressing unique security challenges of distributed IT environments.

- Focus on Energy Efficiency and Sustainability: Implementing greener technologies and practices in compact footprints.

- Increased Demand for Remote Monitoring and Management: Leveraging DCIM for operational efficiency and reduced human intervention.

- Integration of AI and Machine Learning: Optimizing performance, predictive maintenance, and autonomous operations.

AI Impact Analysis on Micro Data Center

The convergence of Artificial Intelligence (AI) with Micro Data Centers is a critical area of discussion, with common user questions focusing on how AI workloads will influence micro data center design, resource requirements, and operational strategies. The primary driver for this integration is AI's inherent need for low-latency processing, which positions micro data centers as ideal environments for performing AI inference and even localized training at the edge. Users are keen to understand the implications for power consumption, cooling efficiency, and the need for specialized hardware, such as GPUs and ASICs, within these constrained spaces. The ability of micro data centers to bring AI capabilities closer to data sources, reducing the need to transmit vast amounts of data to centralized clouds, is a significant draw, promising faster decision-making and enhanced real-time applications.

Furthermore, the impact of AI extends beyond just hosting AI workloads; it also influences the management and optimization of the micro data centers themselves. There's a growing expectation for AI-powered analytics to improve predictive maintenance, optimize power usage, and enhance security protocols within these distributed units. Users are interested in how AI can facilitate more autonomous operations, reduce operational expenditure, and improve the overall reliability of edge infrastructure. This dual impact—AI as a workload requiring micro data centers and AI as a tool to manage them—is a significant theme, highlighting a synergistic relationship that will shape the future evolution of edge computing architectures and drive innovation in compact data solutions.

- Increased Processing Demand: AI inference and localized training at the edge require high-performance computing.

- Specialized Hardware Needs: Greater integration of GPUs, ASICs, and other AI accelerators within micro data centers.

- Elevated Power Density: AI workloads consume more power, necessitating advanced power distribution and thermal management.

- Enhanced Cooling Requirements: Higher heat generation from AI hardware demands efficient and often liquid cooling solutions.

- Reduced Latency for AI Applications: Enables real-time AI decision-making closer to the data source.

- Automated Operations and Management: AI-powered DCIM for predictive maintenance, resource optimization, and security.

- Data Sovereignty and Compliance: Keeping AI processing local addresses regulatory and privacy concerns.

- New Market Opportunities: Creation of specialized AI-ready micro data center solutions for various industries.

Key Takeaways Micro Data Center Market Size & Forecast

The Micro Data Center market's projected growth indicates a fundamental shift in IT infrastructure deployment, moving computing capabilities closer to the data generation points. Key takeaways from the market size and forecast analysis emphasize the undeniable role of edge computing, IoT proliferation, and 5G network expansion as primary catalysts. Stakeholders are particularly interested in the sustained rapid expansion, driven by the need for ultra-low latency applications, real-time data processing, and localized analytics across diverse sectors. The forecast underscores a strategic pivot from large, centralized data centers to a more distributed and agile architecture, highlighting significant investment opportunities in hardware, software, and services that support these compact, integrated solutions.

Furthermore, the forecast reveals that market expansion is not uniform across all segments or regions. There's a notable surge in demand for modular, scalable, and resilient solutions that can be rapidly deployed in non-traditional environments. The increasing complexity of managing a distributed network of micro data centers also points to a growing need for advanced remote monitoring, automation, and security features. These insights suggest that successful market players will be those who can provide integrated, energy-efficient, and easily manageable solutions that address the specific performance, security, and operational challenges inherent in edge deployments, solidifying micro data centers as a cornerstone of the future digital landscape.

- Significant Growth Trajectory: The market is poised for robust growth, driven by digital transformation initiatives.

- Edge Computing Dominance: Edge applications are the primary growth engine, requiring localized data processing.

- IoT and 5G Synergies: These technologies are foundational to the widespread adoption of micro data centers.

- Strategic Infrastructure Shift: Trend towards decentralized IT infrastructure for improved latency and bandwidth.

- Investment Hotspot: Represents a lucrative segment for technology providers, investors, and service providers.

- Focus on Modularity and Rapid Deployment: Demand for pre-integrated, easily deployable solutions.

- Operational Efficiency Imperative: Growing need for solutions enabling remote management and automation.

- Enhanced Security Requirements: Criticality of robust physical and cyber security for distributed assets.

Micro Data Center Market Drivers Analysis

The rapid proliferation of edge computing is a primary driver for the Micro Data Center market. As more data is generated at the periphery of networks—from IoT devices in smart factories to surveillance cameras in smart cities—the need to process this data closer to its source becomes paramount. This localized processing significantly reduces latency, conserves bandwidth by minimizing data backhauling to central data centers, and enables real-time decision-making for critical applications. Industries like manufacturing, healthcare, and retail are increasingly adopting edge computing to enhance operational efficiency, improve customer experiences, and unlock new insights, thereby fueling the demand for compact, deployable IT infrastructure solutions.

The widespread deployment of 5G networks and the accelerating adoption of IoT devices further amplify the market drivers. 5G's ultra-low latency and high bandwidth capabilities are unlocking new applications that are highly sensitive to network delays, such as autonomous vehicles, augmented reality, and real-time industrial automation. These applications often require computing resources to be situated very close to the end-users or devices, making micro data centers an ideal solution. Concurrently, the exponential growth in IoT endpoints, from smart sensors to connected appliances, is generating unprecedented volumes of data. Micro data centers serve as critical hubs for collecting, filtering, and processing this data locally, enabling immediate insights and reducing the burden on core data center facilities, thus driving continuous market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Edge Computing | +5.0% | Global, especially North America, Europe, Asia Pacific | Short to Long Term (2025-2033) |

| Proliferation of IoT Devices | +4.5% | Global, strong in Asia Pacific, Europe | Short to Medium Term (2025-2029) |

| Deployment of 5G Networks | +4.0% | Global, particularly North America, China, South Korea, Japan | Short to Medium Term (2025-2030) |

| Growth in Real-time Applications | +3.5% | Global, cross-industry | Medium to Long Term (2027-2033) |

| Demand for Data Localization & Sovereignty | +2.5% | Europe (GDPR), India, China | Medium Term (2026-2031) |

Micro Data Center Market Restraints Analysis

Despite the robust growth prospects, the Micro Data Center market faces several significant restraints, primarily revolving around the high initial capital expenditure required for deployment. While micro data centers offer long-term operational efficiencies, the upfront cost of acquiring and integrating robust infrastructure, including advanced power, cooling, security, and monitoring solutions within a compact, resilient enclosure, can be substantial. This initial investment can be a deterrent for smaller enterprises or those with limited IT budgets, particularly in emerging economies where financial resources for infrastructure upgrades may be constrained. Additionally, the perception that smaller footprint solutions may not offer the same level of scalability or power as traditional data centers can also limit adoption by organizations with rapidly expanding or unpredictable IT needs.

Another key restraint involves the challenges associated with managing a geographically dispersed network of micro data centers. While these units offer the benefit of localized processing, their distributed nature can complicate monitoring, maintenance, and security. Ensuring consistent power supply, environmental control, and physical security across numerous remote locations requires sophisticated management tools and potentially skilled personnel, which can add to operational complexities and costs. Furthermore, standardization across different vendor solutions remains a hurdle, leading to potential integration issues and vendor lock-in, which can hinder seamless expansion or migration efforts for organizations seeking a cohesive IT infrastructure strategy. Addressing these management and standardization challenges is crucial for overcoming market adoption barriers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -2.0% | Global, particularly emerging markets | Short to Medium Term (2025-2029) |

| Complexity of Managing Distributed Infrastructure | -1.5% | Global, large enterprises with vast networks | Medium Term (2026-2031) |

| Limited Standardization Across Vendors | -1.0% | Global, cross-industry | Medium to Long Term (2027-2033) |

| Power and Cooling Challenges in Remote Locations | -0.8% | Rural areas, regions with unstable grids | Short to Medium Term (2025-2030) |

| Physical Security Concerns in Unattended Sites | -0.7% | Global, high-value data sectors | Ongoing (2025-2033) |

Micro Data Center Market Opportunities Analysis

The burgeoning adoption of Artificial Intelligence (AI) and Machine Learning (ML) at the edge presents a significant opportunity for the Micro Data Center market. As businesses increasingly deploy AI applications for real-time analytics, predictive maintenance, and autonomous operations, the need for localized processing power capable of handling compute-intensive AI workloads grows exponentially. Micro data centers are uniquely positioned to provide the necessary infrastructure to support AI inference, and in some cases, even localized model training, minimizing latency and bandwidth strain on central networks. This integration allows for faster insights and actions, opening up new use cases in smart manufacturing, retail analytics, and healthcare diagnostics that were previously constrained by network limitations. The demand for "AI-ready" micro data centers, equipped with specialized hardware like GPUs and advanced cooling, will be a major growth driver.

Another substantial opportunity lies in the expanding landscape of smart cities, smart infrastructure, and industrial automation. Smart cities initiatives, for instance, rely heavily on interconnected sensors, cameras, and traffic management systems that generate massive amounts of data requiring immediate local processing for real-time responsiveness. Similarly, in industrial automation, edge computing facilitated by micro data centers is crucial for controlling robotics, monitoring operational technology (OT), and implementing predictive maintenance in factories and remote facilities. These sectors demand robust, secure, and resilient IT infrastructure that can withstand harsh environments and operate autonomously, characteristics inherent in well-designed micro data centers. Partnerships with telecommunication providers, utility companies, and infrastructure developers will be key to unlocking these vast market potentials, providing compact, high-performance computing wherever it is needed to drive digital transformation initiatives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI/ML at the Edge | +4.0% | Global, particularly North America, Europe, Asia Pacific | Medium to Long Term (2026-2033) |

| Growth in Smart City Initiatives | +3.5% | Global, strong in Asia Pacific, Europe | Medium Term (2027-2032) |

| Increased Adoption in Industrial Automation (Industry 4.0) | +3.0% | Germany, Japan, China, USA | Short to Medium Term (2025-2030) |

| Expansion of Cloud-Edge Hybrid Architectures | +2.5% | Global, enterprises of all sizes | Medium to Long Term (2026-2033) |

| Demand for Sustainable & Energy-Efficient Solutions | +2.0% | Europe, North America | Medium Term (2027-2032) |

Micro Data Center Market Challenges Impact Analysis

The integration complexity and interoperability issues pose a significant challenge within the Micro Data Center market. Deploying a micro data center often involves integrating various components from different vendors—including power, cooling, racks, security systems, and monitoring software—into a cohesive, compact unit. Ensuring seamless communication and compatibility among these disparate systems can be technically intricate and time-consuming, leading to deployment delays and potential performance bottlenecks. Moreover, interoperability with existing IT infrastructure, whether on-premises or cloud-based, can be a hurdle, requiring significant customization and expertise. This complexity can deter potential adopters who seek straightforward, "plug-and-play" solutions, thereby impacting market penetration and increasing the total cost of ownership for end-users.

Another notable challenge is the scarcity of skilled personnel capable of deploying, maintaining, and troubleshooting micro data centers, especially in remote or unconventional locations. Unlike traditional data centers with dedicated IT staff, micro data centers often operate in environments with limited or no on-site technical support. This necessitates personnel with a broad range of skills, including expertise in networking, power management, cooling systems, and physical security, coupled with the ability to manage distributed IT assets remotely. The talent gap can lead to operational inefficiencies, increased reliance on third-party service providers, and higher operational costs. Furthermore, maintaining optimal environmental conditions (temperature, humidity, air quality) in diverse deployment settings—ranging from outdoor enclosures to non-IT specific indoor spaces—presents a continuous challenge that requires advanced monitoring and proactive management to ensure the longevity and reliability of the equipment, limiting deployment flexibility.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration Complexity & Interoperability Issues | -1.8% | Global, across all verticals | Short to Medium Term (2025-2029) |

| Scarcity of Skilled Personnel | -1.5% | Global, particularly in remote areas | Ongoing (2025-2033) |

| Maintaining Environmental Control in Diverse Settings | -1.2% | Global, outdoor/unconventional deployments | Short to Medium Term (2025-2030) |

| Ensuring Robust Physical & Cyber Security for Distributed Assets | -1.0% | Global, high-risk industries | Ongoing (2025-2033) |

| Regulatory Compliance in Varied Geographies | -0.9% | Europe, Asia Pacific | Medium Term (2026-2031) |

Micro Data Center Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Micro Data Center Market, meticulously covering its size, growth forecast, key trends, drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis across various types, components, applications, and industry verticals, complemented by a thorough regional assessment. The report also profiles leading market players, offering insights into their strategies and market positioning. Designed to equip stakeholders with actionable intelligence, it serves as an essential guide for strategic planning, investment decisions, and competitive landscape analysis within this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | $6.2 Billion USD |

| Market Forecast in 2033 | $31.0 Billion USD |

| Growth Rate | 22.5% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Schneider Electric, Eaton, Vertiv, Legrand, Rittal, Hewlett Packard Enterprise (HPE), IBM, Cisco, Dell Technologies, Huawei, Chatsworth Products, Cannon Technologies, Dataprobe, Dataracks, Enconnex, Instor Solutions, CommScope, Panduit, Zellabox, Advanced Facilities |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Micro Data Center market is extensively segmented to provide a granular view of its diverse dynamics and identify specific growth avenues. This segmentation allows for a deeper understanding of how different product types, component offerings, application areas, and industry verticals contribute to the overall market landscape. By breaking down the market into these distinct categories, businesses can pinpoint high-potential segments, tailor their offerings to specific customer needs, and develop targeted strategies for market penetration and expansion. Each segment reflects unique requirements and growth drivers, from power and cooling solutions to specific industry applications like healthcare or manufacturing.

Analyzing the market by type (rack units) reveals insights into the prevalent size requirements for edge deployments, while component segmentation (solutions vs. services) highlights the value chain's key offerings. Furthermore, the application and vertical segments underscore the diverse utility of micro data centers across various end-use cases, ranging from supporting IoT ecosystems and 5G networks to enabling digital transformation in retail and government sectors. This comprehensive segmentation is critical for market participants to identify niche opportunities, understand competitive positioning, and forecast future demand patterns effectively, ensuring that product development and marketing efforts are aligned with evolving market needs.

- By Type:

- Up to 25 RU (Rack Units)

- 25 to 40 RU

- More than 40 RU

- By Component:

- Solutions:

- Power (UPS, PDU, Generators)

- Cooling (CRAC/CRAH, Liquid Cooling, In-Row Cooling)

- Racks & Enclosures

- Security (Physical, Monitoring, Access Control)

- Monitoring & Management (DCIM, EMS)

- Services:

- Installation & Integration

- Consulting & Professional Services

- Managed & Support Services

- Solutions:

- By Application:

- Edge Computing

- Remote Office/Branch Office (ROBO)

- Internet of Things (IoT)

- Telecommunications

- Smart Cities

- Industrial Automation

- By Vertical:

- IT & Telecommunications

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

- Retail & Consumer Goods

- Manufacturing

- Government & Public Sector

- Energy & Utilities

- Media & Entertainment

Regional Highlights

- North America: This region is a leading market, driven by early adoption of advanced technologies, significant investments in edge computing infrastructure, and the widespread deployment of 5G networks. The presence of major technology companies and a strong focus on IoT applications across industries like manufacturing, healthcare, and retail contribute significantly to market growth. The United States and Canada are key contributors due to robust digital transformation initiatives and high data generation rates.

- Europe: The European market is characterized by stringent data privacy regulations (like GDPR) driving demand for data localization and a strong emphasis on smart city initiatives and Industry 4.0. Countries such as Germany, the UK, and France are at the forefront, investing in highly localized and energy-efficient micro data center solutions. The region's focus on sustainability also drives the adoption of green technologies within these compact units.

- Asia Pacific (APAC): APAC is projected to exhibit the highest growth rate due to rapid industrialization, booming digital economies, and extensive deployment of 5G infrastructure, particularly in countries like China, India, Japan, and South Korea. The immense population base and increasing internet penetration are fueling the demand for edge computing in various applications, including smart retail, smart manufacturing, and telecommunications. Government initiatives supporting digital transformation also play a crucial role.

- Latin America: This region is an emerging market for micro data centers, primarily driven by increasing internet penetration, cloud adoption, and efforts to modernize IT infrastructure. Countries such as Brazil and Mexico are witnessing growing investments in telecommunications and smart city projects, creating a nascent but promising market for edge solutions. Challenges related to infrastructure development and economic stability remain, but the potential for growth is significant.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, fueled by government-led digital initiatives, smart city projects in the UAE and Saudi Arabia, and increasing demand for data centers to support local digital services. Investments in oil and gas, telecommunications, and smart infrastructure are driving the need for localized computing, though market maturity varies significantly across countries within the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Micro Data Center Market.- Schneider Electric

- Eaton

- Vertiv

- Legrand

- Rittal

- Hewlett Packard Enterprise (HPE)

- IBM

- Cisco

- Dell Technologies

- Huawei

- Chatsworth Products

- Cannon Technologies

- Dataprobe

- Dataracks

- Enconnex

- Instor Solutions

- CommScope

- Panduit

- Zellabox

- Advanced Facilities

Frequently Asked Questions

What is a Micro Data Center?

A Micro Data Center is a compact, modular, and self-contained data center solution designed to house and protect IT equipment in non-traditional IT spaces. It typically integrates all essential infrastructure components, including power, cooling, security, and monitoring, within a single rack or enclosure. These units are deployed close to the data source or end-users, primarily to reduce latency, conserve bandwidth, and enable real-time processing for edge computing applications. They are highly scalable, secure, and often remotely manageable, making them ideal for diverse environments such as remote offices, retail stores, industrial sites, and smart city infrastructure.

Why are Micro Data Centers gaining popularity?

Micro Data Centers are gaining significant popularity primarily due to the explosive growth of edge computing, Internet of Things (IoT) devices, and 5G network deployments. These trends necessitate processing data closer to its source to achieve ultra-low latency, improve application responsiveness, and reduce the strain on centralized networks. Their modular, rapidly deployable, and self-contained nature makes them ideal for environments where traditional data centers are impractical. Furthermore, they offer enhanced physical security, simplified management through remote monitoring, and often improved energy efficiency, aligning with modern business needs for agile, distributed, and resilient IT infrastructure.

What are the primary benefits of deploying Micro Data Centers?

The primary benefits of deploying Micro Data Centers include significantly reduced latency and improved application performance by bringing computing closer to the edge. They offer considerable bandwidth savings by processing data locally, minimizing the need to backhaul large volumes of data to central facilities. Their modular design enables rapid deployment and scalability, allowing businesses to expand IT capacity quickly as needed. Micro Data Centers also provide enhanced physical and cyber security for critical data, offer robust environmental protection for IT equipment in diverse settings, and simplify remote management, reducing operational costs and the need for dedicated on-site IT personnel.

Which industries are major adopters of Micro Data Centers?

Micro Data Centers are being adopted across a wide array of industries that require localized data processing and low-latency computing. Key adopters include Telecommunications, leveraging them for 5G network densification and edge computing nodes. Retail & Consumer Goods utilize them for in-store analytics, inventory management, and personalized customer experiences. Manufacturing sectors adopt them for Industry 4.0 applications, real-time control, and predictive maintenance. Healthcare uses them for localized patient data processing and remote diagnostics. Additionally, Government & Public Sector, BFSI (Banking, Financial Services, and Insurance), and Energy & Utilities are increasingly deploying micro data centers to enhance operational efficiency, security, and data sovereignty.

What is the future outlook for the Micro Data Center market?

The future outlook for the Micro Data Center market is highly positive, projecting sustained strong growth driven by the continuous expansion of edge computing, the proliferation of AI and Machine Learning applications at the edge, and ongoing global 5G rollouts. The market is expected to witness increasing integration of advanced cooling solutions, more intelligent automation capabilities through AI-powered DCIM, and a greater emphasis on energy efficiency and sustainable designs. As organizations continue to decentralize their IT infrastructure to meet demands for real-time processing and data localization, Micro Data Centers will become an increasingly indispensable component of the digital ecosystem, leading to further innovation and broader adoption across diverse industries worldwide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted