Data Centre Equipment Market

Data Centre Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705142 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

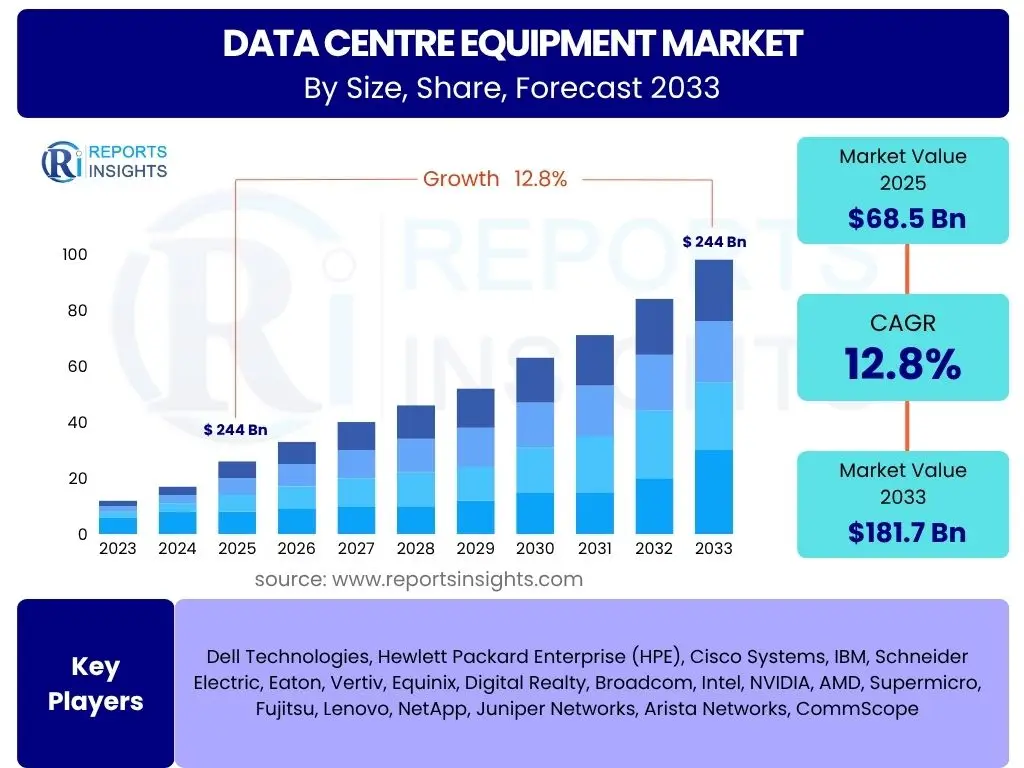

Data Centre Equipment Market Size

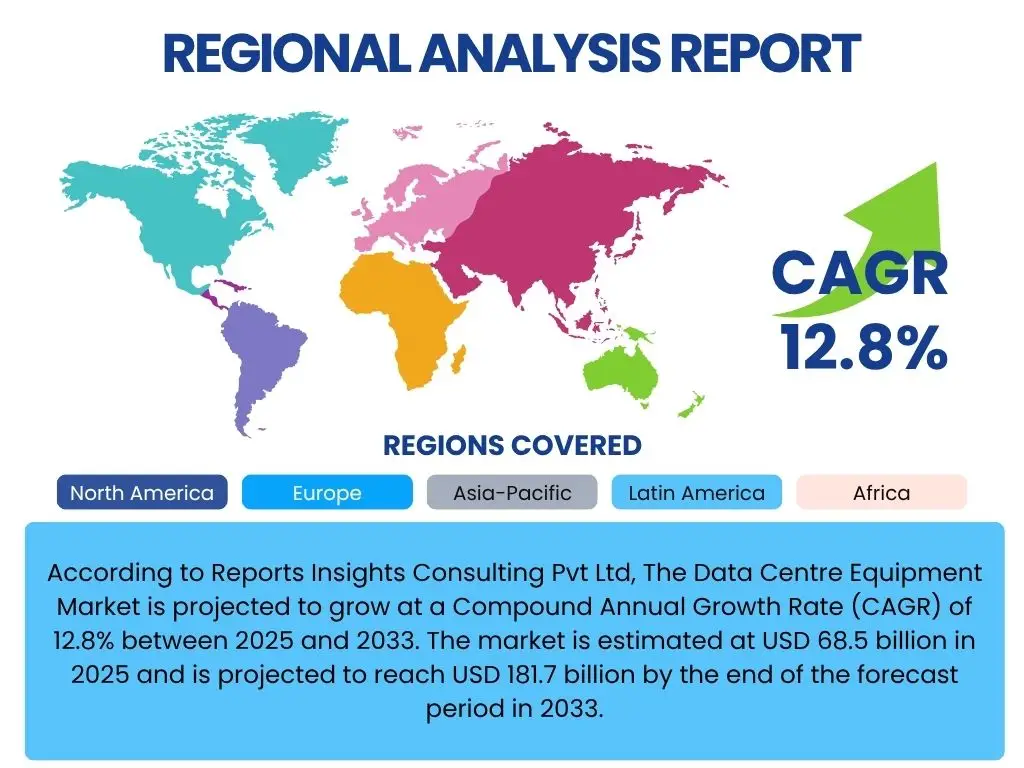

According to Reports Insights Consulting Pvt Ltd, The Data Centre Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 68.5 billion in 2025 and is projected to reach USD 181.7 billion by the end of the forecast period in 2033.

Key Data Centre Equipment Market Trends & Insights

User inquiries frequently highlight the rapid evolution of data center infrastructure, driven by escalating data volumes and the increasing complexity of modern workloads. A prominent theme revolves around the necessity for greater efficiency, scalability, and sustainability in data center operations. Users are keen to understand how emerging technologies like advanced cooling, modular designs, and software-defined everything are reshaping traditional data center architectures and operational paradigms. There is also a significant interest in solutions that address the energy demands of high-density computing and the drive towards net-zero emissions, indicating a strong market emphasis on environmentally responsible practices.

Another area of consistent interest concerns the strategic shift towards edge computing and hybrid cloud environments. Users are seeking insights into how these distributed architectures impact the demand for specific data center equipment, such as smaller, more ruggedized servers and networking gear, as well as the integration challenges between on-premise, cloud, and edge infrastructure. The imperative for enhanced security and robust disaster recovery capabilities across these varied environments also features prominently in user discussions, reflecting the critical nature of data protection and business continuity.

- Increased adoption of liquid cooling solutions for high-density racks.

- Proliferation of modular and prefabricated data center units for rapid deployment.

- Growing emphasis on sustainable and energy-efficient equipment.

- Widespread implementation of AI/ML for Data Center Infrastructure Management (DCIM).

- Expansion of edge computing deployments driving demand for smaller, distributed infrastructure.

- Continued shift towards composable infrastructure architectures.

- Enhanced focus on cybersecurity solutions integrated within data center hardware and software.

AI Impact Analysis on Data Centre Equipment

Common user questions regarding AI's impact on data center equipment predominantly focus on the extraordinary demands placed on infrastructure by AI workloads. Users are concerned about the necessity for specialized hardware, particularly Graphics Processing Units (GPUs) and other AI accelerators, and how this affects server architectures and procurement strategies. The significant power consumption and heat generation associated with AI training and inference are also major points of inquiry, prompting interest in advanced cooling technologies and more robust power delivery systems. There is an expectation that AI will not only consume resources but also enhance data center operations, leading to questions about AI-powered DCIM solutions for predictive maintenance, resource optimization, and automation.

Furthermore, the growth of AI at the edge and in distributed environments is a recurring theme, leading to discussions about how equipment needs to adapt for smaller footprints, lower latency, and enhanced autonomy. Users are exploring the implications of AI on storage solutions, specifically the demand for high-performance, low-latency storage to feed AI models. The rapid pace of AI innovation also raises questions about future-proofing data center investments and the ability of current infrastructure to support evolving AI models and applications, highlighting a need for flexible and scalable equipment solutions.

- **Increased Demand for High-Performance Hardware:** Drives significant demand for GPU-accelerated servers, specialized AI chips, and high-bandwidth interconnects, necessitating upgrades in server and networking infrastructure.

- **Elevated Power and Cooling Requirements:** AI workloads lead to higher rack power densities, compelling the adoption of advanced cooling solutions (e.g., liquid cooling, immersion cooling) and robust power distribution units.

- **Optimized Data Storage and Management:** Requires high-speed, low-latency storage solutions like NVMe SSDs and parallel file systems to feed AI models efficiently, alongside intelligent data management platforms.

- **AI for Data Center Operations (DCIM):** AI is increasingly used within Data Center Infrastructure Management (DCIM) software for predictive analytics, automation of tasks, energy optimization, and intelligent workload placement, enhancing operational efficiency.

- **Edge AI Infrastructure:** Promotes the development of compact, ruggedized, and energy-efficient data center equipment suitable for deployment at the edge, closer to data sources, reducing latency.

- **Network Bandwidth Demands:** AI model training and inference generate massive data flows, requiring higher network bandwidth and lower latency, driving demand for 400GbE and beyond networking equipment.

Key Takeaways Data Centre Equipment Market Size & Forecast

User inquiries into the key takeaways from the Data Centre Equipment market size and forecast consistently highlight the robust growth trajectory driven by the pervasive digital transformation across industries. The primary insight gleaned is the sustained expansion fueled by increasing data generation, cloud adoption, and the escalating demand for high-performance computing, particularly for AI and IoT applications. Stakeholders are particularly interested in understanding which equipment categories and geographical regions are poised for the most significant growth, indicating a strategic focus on investment allocation and market penetration opportunities. The forecast reinforces the notion that data centers remain critical infrastructure for the global digital economy.

Another significant takeaway for users is the evolving nature of data center infrastructure, moving towards more agile, efficient, and sustainable models. The market forecast indicates a strong shift towards solutions that offer greater scalability, reduced operational costs, and lower environmental impact. This includes a notable emphasis on modularity, advanced cooling technologies, and intelligent management systems. The continued investment in hyperscale and colocation facilities, alongside the burgeoning edge computing segment, also presents a key insight into the diverse deployment strategies shaping the future demand for data center equipment.

- The market is experiencing robust growth, primarily driven by digital transformation and cloud expansion.

- Significant investments are being made in next-generation computing, including AI/ML and IoT infrastructure.

- Hyperscale data centers and colocation facilities remain dominant growth engines.

- Edge computing is emerging as a critical segment, driving demand for distributed equipment.

- Energy efficiency and sustainability are increasingly becoming core considerations in equipment procurement.

- Technological advancements in cooling, power management, and automation are pivotal for market evolution.

Data Centre Equipment Market Drivers Analysis

The global data centre equipment market is propelled by a confluence of powerful drivers, fundamentally rooted in the accelerating pace of digital transformation across all industry verticals. The pervasive adoption of cloud computing models, both public and private, necessitates continuous expansion and upgrading of data center infrastructure. Furthermore, the explosion of data generated from diverse sources such as IoT devices, social media, and digital transactions creates an insatiable demand for robust storage, processing, and networking capabilities within data centers. This data proliferation directly translates into increased requirements for high-performance servers, scalable storage solutions, and advanced networking equipment.

Beyond data volume, the increasing complexity of modern workloads, particularly those related to Artificial Intelligence (AI), Machine Learning (ML), and Big Data analytics, serves as a significant driver. These compute-intensive applications require specialized hardware and higher power densities, pushing the boundaries of existing infrastructure and necessitating investments in advanced cooling, power delivery, and specialized processing units. Additionally, the ongoing global rollout of 5G technology and the strategic shift towards edge computing paradigms are decentralizing data processing, thereby creating new demand for modular, energy-efficient data center equipment closer to the points of data generation and consumption. Regulatory compliance requirements for data residency and security also indirectly drive market growth by encouraging investments in secure and compliant data center infrastructure.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Digital Transformation & Cloud Adoption | +2.1% | Global, particularly North America, Europe, APAC | Mid-term to Long-term |

| Explosive Growth in Data Volume & Big Data Analytics | +1.8% | Global | Short-term to Long-term |

| Increasing Demand for AI, ML, & HPC Workloads | +2.3% | North America, APAC (China, India), Europe | Short-term to Mid-term |

| Proliferation of IoT Devices & Edge Computing | +1.5% | Global, especially urbanized & industrial areas | Mid-term |

| Global Rollout of 5G Networks | +0.9% | Global, focusing on dense population centers | Mid-term |

Data Centre Equipment Market Restraints Analysis

Despite the robust growth trajectory, the data centre equipment market faces several significant restraints that could temper its expansion. One of the primary limiting factors is the substantial capital expenditure required for building and upgrading data centers. The high initial investment in land, construction, and specialized equipment, coupled with ongoing operational costs such as energy consumption and maintenance, can be prohibitive for many organizations, particularly smaller enterprises or those in developing regions. This financial barrier often leads organizations to opt for cloud-based services rather than investing in their own on-premise data center infrastructure, thereby shifting demand away from direct equipment purchases.

Another critical restraint is the increasing concern over energy consumption and environmental impact. Data centers are notorious for their high energy usage, which not only translates to significant operational costs but also contributes to carbon emissions. Growing regulatory pressures and corporate sustainability initiatives are forcing data center operators to invest in more energy-efficient equipment and renewable energy sources, which can add to initial costs or extend ROI periods. Furthermore, complexities associated with supply chain disruptions, particularly for specialized components like semiconductors, can lead to equipment shortages, increased lead times, and higher procurement costs, thereby hindering timely data center expansion and upgrades. The scarcity of skilled professionals required to design, deploy, and manage advanced data center infrastructure also poses a notable challenge.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure & Operational Costs | -1.2% | Global, especially SMBs | Short-term to Long-term |

| Significant Energy Consumption & Environmental Concerns | -0.8% | Global, focusing on regions with strict environmental policies | Mid-term to Long-term |

| Supply Chain Volatility & Component Shortages | -0.7% | Global, particularly critical for high-tech components | Short-term to Mid-term |

| Skilled Workforce Shortage & Talent Gap | -0.5% | North America, Europe, APAC | Long-term |

Data Centre Equipment Market Opportunities Analysis

The data centre equipment market presents numerous opportunities driven by ongoing technological advancements and evolving business needs. One significant opportunity lies in the burgeoning market for advanced cooling solutions. As computing densities soar due to AI and HPC workloads, traditional air-cooling methods become insufficient. This creates substantial demand for liquid cooling technologies, including direct-to-chip, immersion, and rear-door heat exchangers, allowing for greater efficiency and sustainability. The increasing focus on green data centers and corporate social responsibility further accelerates this trend, opening avenues for innovation in energy-efficient power supplies, renewable energy integration, and waste heat recovery systems.

Another lucrative opportunity stems from the expansion of edge computing and the need for localized data processing. This necessitates the development and deployment of smaller, modular, and ruggedized data center units suitable for non-traditional environments like factories, retail stores, and remote locations. The growth of distributed infrastructure creates new market segments for specialized servers, storage, and networking equipment designed for edge deployments. Furthermore, the drive towards hybrid and multi-cloud strategies creates opportunities for vendors offering equipment that seamlessly integrates with public cloud services, such as hyperconverged infrastructure (HCI) and composable infrastructure, enabling greater flexibility and agility for enterprises managing diverse IT environments. Opportunities also exist in providing enhanced cybersecurity solutions integrated directly into hardware and software, addressing rising threat landscapes within data centers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Deployment of Liquid Cooling Technologies | +1.5% | Global, especially regions with high energy costs | Short-term to Mid-term |

| Growth of Edge Computing Infrastructure | +1.3% | Global, particularly developing economies & industrial sectors | Mid-term |

| Demand for Sustainable & Energy-Efficient Solutions | +1.0% | North America, Europe, APAC | Mid-term to Long-term |

| Advancements in Data Center Automation & AI-powered DCIM | +0.9% | Global | Mid-term |

| Hybrid Cloud & Multi-cloud Integration Solutions | +0.7% | Global, particularly large enterprises | Short-term to Mid-term |

Data Centre Equipment Market Challenges Impact Analysis

The data centre equipment market grapples with several formidable challenges that can impede its growth and evolution. One significant challenge is the rapid pace of technological obsolescence. With new generations of processors, memory, and networking technologies emerging frequently, data center operators face constant pressure to upgrade equipment to maintain competitive performance and efficiency. This continuous upgrade cycle can lead to substantial capital expenditures and complex migration processes, making long-term investment planning difficult and potentially affecting ROI calculations. Moreover, integrating disparate systems and ensuring interoperability among various vendors' equipment remains a persistent technical challenge, especially in complex hybrid IT environments.

Another major challenge revolves around managing the escalating power and cooling requirements of modern high-density data centers. As rack densities increase due to powerful CPUs and GPUs, the thermal load becomes immense, pushing the limits of traditional infrastructure. This necessitates significant investments in advanced cooling technologies and robust power delivery systems, which are often costly and require specialized expertise to implement and maintain. Furthermore, cybersecurity threats are a continuous and evolving challenge, with data centers being prime targets. Ensuring the physical and digital security of equipment, data, and networks requires constant vigilance, sophisticated security solutions, and adherence to stringent compliance standards, adding layers of complexity and cost to operations. The global supply chain also remains vulnerable to disruptions, affecting the availability and pricing of critical components.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence & High Upgrade Cycles | -0.9% | Global | Short-term to Long-term |

| Managing Escalating Power & Cooling Demands | -1.1% | Global | Short-term to Mid-term |

| Complex Cybersecurity Threats & Data Breaches | -0.6% | Global | Short-term to Long-term |

| Supply Chain Fragility & Geopolitical Risks | -0.7% | Global, especially for key components | Short-term |

Data Centre Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Data Centre Equipment Market, covering current trends, market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It offers strategic insights into the competitive landscape, profiling major industry players and their strategies to maintain market leadership. The report aims to assist stakeholders in making informed business decisions by providing a holistic view of the market's current state and its potential evolution over the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 68.5 Billion |

| Market Forecast in 2033 | USD 181.7 Billion |

| Growth Rate | 12.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Dell Technologies, Hewlett Packard Enterprise (HPE), Cisco Systems, IBM, Schneider Electric, Eaton, Vertiv, Equinix, Digital Realty, Broadcom, Intel, NVIDIA, AMD, Supermicro, Fujitsu, Lenovo, NetApp, Juniper Networks, Arista Networks, CommScope |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Data Centre Equipment Market is extensively segmented to provide a granular view of its diverse components and applications. This segmentation allows for a precise understanding of demand patterns, technological shifts, and strategic opportunities across various product categories and end-user verticals. The market is primarily segmented by Component, which encompasses critical hardware such as servers, storage, networking equipment, power distribution units, UPS systems, and cooling solutions, along with specialized software like DCIM. This detailed component-level breakdown highlights the specific technological advancements and investment trends driving each part of the data center infrastructure stack.

Further segmentation by Data Center Type (Colocation, Hyperscale, Enterprise, Edge) delineates the varying infrastructure needs and investment profiles of different data center models, reflecting the shift towards more specialized and distributed computing environments. The End-Use Industry segmentation provides insights into vertical-specific demands, demonstrating how sectors like BFSI, IT & Telecom, Healthcare, and Retail leverage data center equipment to support their unique operational requirements and digital transformation initiatives. This multi-dimensional segmentation is crucial for stakeholders to identify high-growth areas and tailor their product offerings and market strategies effectively.

- By Component:

- Servers (Rack Servers, Blade Servers, Tower Servers)

- Storage (DAS, NAS, SAN, Object Storage)

- Networking (Switches, Routers, Gateways, Network Interface Cards, Cables)

- Power Distribution Units (PDUs)

- Uninterruptible Power Supplies (UPS)

- Cooling Systems (Chillers, CRAC/CRAH Units, Cooling Towers, Liquid Cooling Solutions)

- Racks & Enclosures

- Physical Security Systems (CCTV, Access Control)

- DCIM Software

- By Data Center Type:

- Colocation Data Centers

- Hyperscale Data Centers

- Enterprise Data Centers

- Edge Data Centers

- By End-Use Industry:

- BFSI (Banking, Financial Services, and Insurance)

- IT & Telecommunications

- Government & Public Sector

- Healthcare

- Retail & E-commerce

- Manufacturing

- Media & Entertainment

- Energy & Utilities

- Others

Regional Highlights

- North America: Dominates the market due to the early adoption of cloud technologies, presence of major hyperscale cloud providers, and significant investments in AI and advanced computing infrastructure. Strong growth is expected in enterprise and edge data center deployments.

- Europe: Exhibits robust growth driven by stringent data residency regulations (GDPR), increasing demand for sustainable data centers, and digital transformation initiatives across industries. Germany, the UK, and France are key markets.

- Asia Pacific (APAC): Emerging as the fastest-growing region, fueled by rapid digitalization, expanding internet penetration, booming e-commerce, and substantial government investments in digital infrastructure, particularly in China, India, Japan, and Australia.

- Latin America: Showing steady growth, propelled by increasing cloud adoption, expansion of multinational corporations, and improving digital connectivity. Brazil and Mexico are leading the regional market.

- Middle East and Africa (MEA): Experiencing notable growth with significant government-led digital transformation agendas, smart city initiatives, and the emergence of regional cloud hubs, particularly in UAE, Saudi Arabia, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Data Centre Equipment Market.- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems

- IBM

- Schneider Electric

- Eaton

- Vertiv

- Equinix

- Digital Realty

- Broadcom

- Intel

- NVIDIA

- AMD

- Supermicro

- Fujitsu

- Lenovo

- NetApp

- Juniper Networks

- Arista Networks

- CommScope

Frequently Asked Questions

Analyze common user questions about the Data Centre Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary components of data center equipment?

The primary components include servers (rack, blade, tower), storage systems (DAS, NAS, SAN), networking equipment (switches, routers), power infrastructure (UPS, PDUs), cooling systems (CRAC/CRAH, liquid cooling), racks, physical security, and Data Center Infrastructure Management (DCIM) software.

How is AI impacting the demand for data center equipment?

AI significantly drives demand for high-performance servers with GPUs and accelerators, requiring more robust power and advanced cooling solutions. AI also enhances DCIM for operational efficiency and necessitates high-speed, low-latency storage infrastructure.

What are the key drivers of growth in the Data Centre Equipment Market?

Key growth drivers include rapid digital transformation, increasing adoption of cloud computing, the explosion of data volumes, rising demand for AI/ML and HPC workloads, and the expansion of IoT and edge computing.

What role does sustainability play in data center equipment trends?

Sustainability is a critical trend, driving demand for energy-efficient equipment, advanced cooling solutions (like liquid cooling), renewable energy integration, and technologies that reduce the environmental footprint and operational costs of data centers.

Which regions are leading the growth in the Data Centre Equipment Market?

North America currently leads in market share due to early adoption and hyperscale presence, while Asia Pacific (APAC) is projected to be the fastest-growing region driven by rapid digitalization, e-commerce growth, and significant infrastructure investments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted