Marine Diesel Market

Marine Diesel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700666 | Last Updated : July 26, 2025 |

Format : ![]()

![]()

![]()

![]()

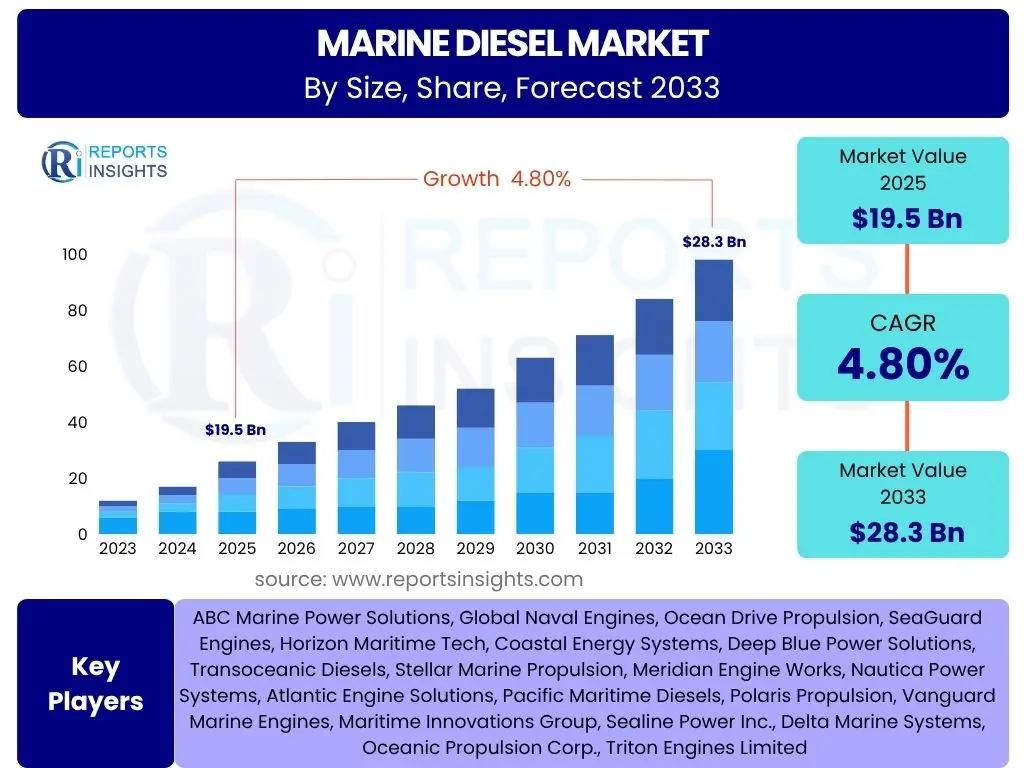

Marine Diesel Market Size

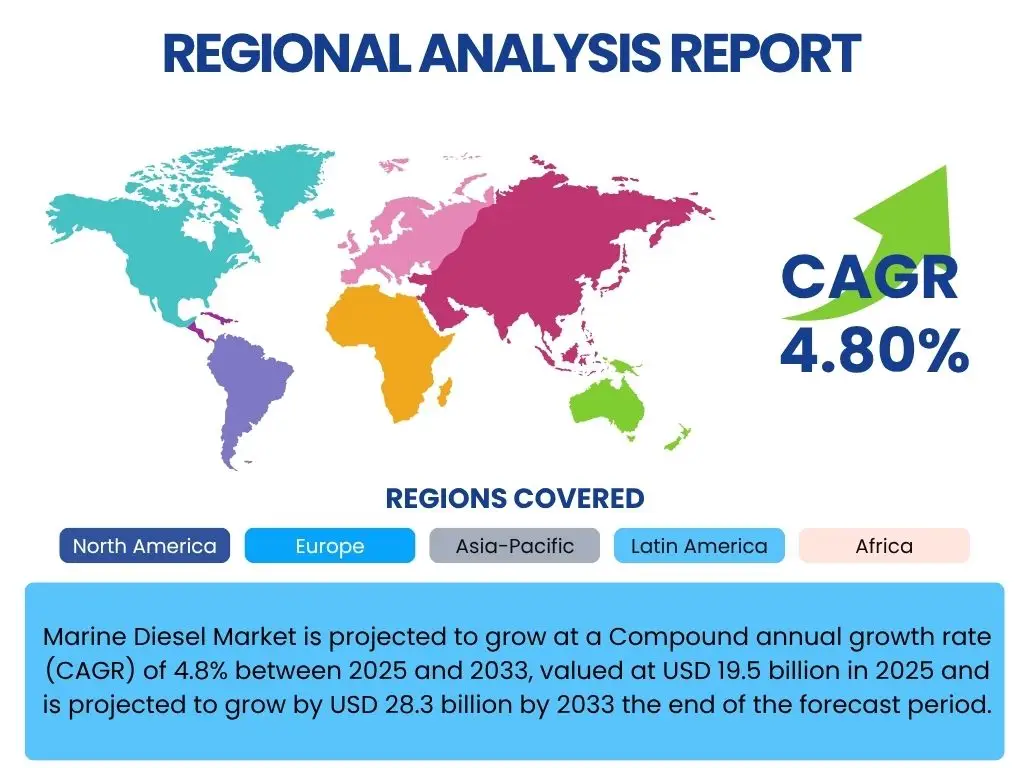

Marine Diesel Market is projected to grow at a Compound annual growth rate (CAGR) of 4.8% between 2025 and 2033, valued at USD 19.5 billion in 2025 and is projected to grow by USD 28.3 billion by 2033 the end of the forecast period.

Key Marine Diesel Market Trends & Insights

The Marine Diesel Market is currently experiencing a dynamic shift driven by stringent environmental regulations, technological advancements in engine efficiency, and a growing emphasis on alternative fuels. Emerging trends include the increasing adoption of dual-fuel engines, the integration of digitalization for predictive maintenance, and a sustained demand from the commercial shipping sector. Furthermore, the market is seeing innovation in propulsion systems aimed at reducing emissions and improving operational costs, signaling a strategic pivot towards sustainable maritime operations while maintaining robust performance standards for marine vessels worldwide.

- Rising demand for fuel-efficient engines.

- Increasing adoption of low-sulfur fuels.

- Growth in dual-fuel engine technology.

- Focus on emissions reduction and IMO regulations.

- Digitalization and predictive maintenance integration.

- Expansion of global trade driving shipping demand.

- Technological advancements in engine design.

- Shifting preference towards cleaner energy solutions.

AI Impact Analysis on Marine Diesel

Artificial Intelligence (AI) is set to revolutionize the Marine Diesel Market by enhancing operational efficiency, optimizing fuel consumption, and improving predictive maintenance capabilities. AI algorithms can analyze vast datasets from engine sensors to forecast potential failures, schedule maintenance proactively, and identify optimal navigation routes to minimize fuel burn. This integration leads to significant cost savings, reduced downtime, and a more sustainable marine ecosystem. While the initial investment in AI infrastructure may be substantial, the long-term benefits in terms of operational reliability and environmental compliance position AI as a transformative force within the sector.

- Optimized fuel consumption through AI-driven route planning.

- Predictive maintenance for marine diesel engines, reducing downtime.

- Enhanced operational efficiency and vessel performance.

- Real-time monitoring and anomaly detection for engine health.

- Improved crew safety through automated alerts and diagnostics.

- Data-driven insights for strategic decision-making in fleet management.

Key Takeaways Marine Diesel Market Size & Forecast

- Market poised for steady growth through 2033.

- CAGR of 4.8% anticipated for the forecast period.

- Significant market value increase from 2025 to 2033.

- Regulatory pressures are a primary growth catalyst.

- Technological innovation drives efficiency and cleaner solutions.

- Global trade expansion underpins market demand.

Marine Diesel Market Drivers Analysis

The Marine Diesel Market is fundamentally propelled by a confluence of factors, primarily the escalating demand for global maritime trade. As international commerce continues to expand, the necessity for efficient and reliable marine transportation grows, directly stimulating the demand for marine diesel engines and associated infrastructure. This global economic activity forms the bedrock of market expansion, ensuring a consistent need for robust propulsion systems across various vessel types.

Furthermore, stringent environmental regulations, particularly those imposed by the International Maritime Organization (IMO) concerning sulfur emissions and greenhouse gases, are acting as significant drivers. These regulations compel shipowners to upgrade or replace existing engines with more efficient and compliant models, often driving investment in advanced diesel technologies or dual-fuel systems. The imperative to reduce the environmental footprint of shipping, coupled with the drive for operational cost efficiency through fuel savings, further reinforces the market's growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Global Maritime Trade | +1.5% | Global, particularly Asia Pacific (China, India), North America, Europe | Long-term (2025-2033) |

| Increasing Demand for New Vessel Construction | +1.2% | Asia Pacific (South Korea, Japan, China), Europe (Germany, Norway) | Medium to Long-term (2025-2030) |

| Stringent Environmental Regulations (IMO 2020, EEXI, CII) | +1.8% | Global, with emphasis on major shipping routes and port states | Medium to Long-term (Ongoing) |

| Technological Advancements in Engine Efficiency | +0.9% | Europe (Germany, Denmark), Asia Pacific (Japan, South Korea) | Medium to Long-term (Ongoing) |

| Rise in Cruise and Leisure Industry | +0.5% | North America, Europe, Asia Pacific (Emerging markets) | Medium-term (2025-2028) |

Marine Diesel Market Restraints Analysis

The Marine Diesel Market faces several significant restraints that could temper its growth trajectory. A primary concern is the escalating volatility of crude oil prices, which directly impacts the cost of marine diesel fuel. Unpredictable fluctuations can severely affect the operational budgets of shipping companies, leading to deferred investments in new vessels or engine upgrades and potentially slowing down market expansion. This price instability creates an environment of uncertainty for long-term planning within the maritime industry.

Moreover, the increasing global push towards decarbonization and the adoption of alternative fuels pose a substantial long-term restraint. While marine diesel remains the dominant propulsion fuel, growing regulatory and societal pressure to reduce emissions is accelerating research and development into fuels like LNG, methanol, ammonia, and hydrogen. This strategic shift could gradually erode the market share of traditional marine diesel, as new vessels are designed for or retrofitted to run on cleaner alternatives, presenting a fundamental challenge to sustained growth in the conventional diesel segment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Crude Oil Prices | -0.8% | Global, impacting all maritime operations | Short to Medium-term (Ongoing) |

| Strict Environmental Regulations on Emissions | -1.2% | Global, particularly developed regions and IMO member states | Long-term (Ongoing push for decarbonization) |

| Emergence of Alternative Fuels (LNG, Methanol, Hydrogen, Ammonia) | -1.5% | Global, with early adoption in technologically advanced regions | Long-term (2028-2033 and beyond) |

| High Capital Investment for New Engine Technologies | -0.6% | Global, affecting smaller and emerging market shipowners | Medium-term (2025-2030) |

| Geopolitical Instability and Trade Disruptions | -0.4% | Specific regions affected by conflicts or trade wars | Short-term (Intermittent) |

Marine Diesel Market Opportunities Analysis

The Marine Diesel Market presents compelling opportunities for growth and innovation, particularly through advancements in engine efficiency and emission reduction technologies. The continuous drive to meet stricter environmental mandates, such as the IMO's decarbonization goals, is creating a strong impetus for manufacturers to develop and integrate cutting-edge diesel engine designs. These include sophisticated fuel injection systems, exhaust gas recirculation (EGR), and selective catalytic reduction (SCR) technologies, all aimed at optimizing fuel consumption and minimizing harmful emissions. Companies that can deliver high-performance, eco-compliant engines stand to capture significant market share.

Furthermore, the expanding global fleet, driven by sustained growth in international trade and the burgeoning cruise and offshore sectors, offers a robust demand pipeline for new marine diesel engines and aftermarket services. Emerging markets in Asia Pacific and Latin America, in particular, are investing heavily in port infrastructure and expanding their maritime capabilities, leading to increased shipbuilding and vessel maintenance activities. This geographical expansion, combined with the lifecycle needs of existing fleets for upgrades and repairs, provides diverse avenues for market players to capitalize on evolving industry requirements and regional developments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Hybrid and Dual-Fuel Propulsion Systems | +1.0% | Global, especially in regions focusing on sustainability (Europe, North America) | Long-term (2025-2033) |

| Increasing Adoption of Digitalization for Predictive Maintenance | +0.7% | Global, with strong potential in developed maritime nations | Medium to Long-term (2025-2030) |

| Expansion of Global Fishing and Offshore Support Vessels | +0.6% | Asia Pacific (Southeast Asia, China), Latin America, Africa | Medium-term (2025-2028) |

| Retrofit Market for Emission Control Systems | +0.8% | Global, targeting older fleets in compliance regions | Short to Medium-term (Ongoing compliance) |

| Growth in Inland Waterway Transportation | +0.4% | Europe (Rhine, Danube), Asia Pacific (Mekong, Yangtze), North America (Mississippi) | Long-term (Sustainable infrastructure development) |

Marine Diesel Market Challenges Impact Analysis

The Marine Diesel Market confronts significant challenges, primarily stemming from the pervasive pressure for decarbonization across the maritime industry. While diesel remains crucial, the long-term vision of zero-emission shipping necessitates a fundamental shift away from fossil fuels. This creates a strategic dilemma for manufacturers and operators, who must balance the need for immediate compliance with current regulations against the future imperative to invest in nascent, often more expensive, alternative fuel technologies. The uncertainty surrounding the timeline and viability of these alternatives complicates investment decisions and could slow down conventional diesel market growth.

Another substantial challenge is the increasing cost and complexity of meeting evolving emission standards. Manufacturers must continually invest in research and development to enhance engine efficiency and integrate advanced emission control technologies, such as exhaust gas cleaning systems (scrubbers) and selective catalytic reduction (SCR) systems. These technologies add significant capital expenditure to new vessel builds and retrofits, impacting the overall cost of ownership for ship operators. For smaller players or those in developing regions, the financial burden of compliance can be prohibitive, potentially leading to slower adoption rates or even market stagnation in certain segments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Costs of Compliance with Emission Regulations | -0.7% | Global, affecting shipowners and operators worldwide | Medium to Long-term (Ongoing) |

| Competition from Alternative Fuel Technologies | -1.0% | Global, particularly in advanced maritime economies | Long-term (2028-2033) |

| Supply Chain Disruptions and Material Shortages | -0.5% | Global, with specific impacts on manufacturing hubs (Asia) | Short to Medium-term (Intermittent) |

| Aging Fleet and High Maintenance Costs | -0.3% | Global, particularly for operators with older vessels | Long-term (Ongoing operational challenge) |

| Lack of Standardized Infrastructure for New Fuels | -0.6% | Global, especially in developing regions without widespread bunkering | Long-term (Hindering widespread adoption of alternatives) |

Marine Diesel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Marine Diesel Market, offering a strategic overview of its size, trends, drivers, restraints, opportunities, and challenges. It is designed to equip stakeholders with critical insights into market dynamics, segmentation, regional performance, and the competitive landscape, facilitating informed decision-making and strategic planning within the global maritime industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.5 billion |

| Market Forecast in 2033 | USD 28.3 billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABC Marine Power Solutions, Global Naval Engines, Ocean Drive Propulsion, SeaGuard Engines, Horizon Maritime Tech, Coastal Energy Systems, Deep Blue Power Solutions, Transoceanic Diesels, Stellar Marine Propulsion, Meridian Engine Works, Nautica Power Systems, Atlantic Engine Solutions, Pacific Maritime Diesels, Polaris Propulsion, Vanguard Marine Engines, Maritime Innovations Group, Sealine Power Inc., Delta Marine Systems, Oceanic Propulsion Corp., Triton Engines Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Marine Diesel Market is meticulously segmented to provide a granular view of its diverse components, aiding stakeholders in pinpointing specific growth areas and market dynamics. This comprehensive segmentation by fuel type, vessel type, application, and power output allows for a detailed understanding of where demand originates and how different market aspects interact. Understanding these segments is crucial for strategic planning, product development, and targeted market penetration, as each segment presents unique characteristics and opportunities influenced by regulatory frameworks, technological advancements, and operational demands.

The categorization by vessel type, for instance, highlights the distinct needs of commercial shipping versus the offshore or passenger sectors, each requiring tailored marine diesel solutions. Similarly, differentiating by power output allows for an analysis of engine performance requirements across various vessel sizes and operational profiles. This multi-faceted approach to segmentation ensures that the report offers actionable insights, enabling market participants to identify lucrative niches and adapt their strategies to evolving industry landscapes effectively.

- Fuel Type: This segment analyzes the market based on the type of marine diesel fuel consumed by vessels.

- Marine Gas Oil (MGO): Characterized by its low sulfur content, primarily used in Emission Control Areas (ECAs) and for auxiliary engines.

- Marine Fuel Oil (MFO): Also known as bunker fuel, it is a residual fuel used by larger vessels outside ECAs.

- Marine Diesel Oil (MDO): A blend of distillate and residual fuels, offering a balance between cost and quality, suitable for various engine types.

- Vessel Type: This segmentation provides insights into the demand across different categories of marine vessels.

- Commercial Vessels: Includes a broad range of cargo ships critical for global trade.

- Container Ships: High-speed vessels for containerized cargo.

- Tankers: Designed for transporting liquids like oil and chemicals.

- Bulk Carriers: Used for carrying unpackaged dry cargo such as grains, coal, and iron ore.

- General Cargo Ships: Versatile vessels for various types of goods.

- Passenger Vessels: Focuses on ships designed for human transport and leisure.

- Cruise Ships: Large vessels for leisure voyages.

- Ferries: Used for short-distance passenger and vehicle transport.

- Offshore Vessels: Supports oil and gas exploration and production activities.

- Supply Vessels: Transport goods and personnel to offshore installations.

- PSVs (Platform Supply Vessels): Specialised vessels for platform support.

- AHTS (Anchor Handling Tug Supply Vessels): Powerful tugs for anchor handling and towing.

- Fishing Vessels: Boats and ships used for commercial fishing.

- Naval Vessels: Military ships and boats used by navies.

- Commercial Vessels: Includes a broad range of cargo ships critical for global trade.

- Application: This segment distinguishes between the primary uses of marine diesel engines on vessels.

- Propulsion: Engines primarily used to drive the vessel forward.

- Auxiliary: Engines used for onboard power generation, lighting, and other systems not directly related to propulsion.

- Power Output: Classifies engines based on their operational speed and power generation capabilities.

- Low Speed (<100 RPM): Typically large, two-stroke engines used in large cargo vessels for maximum efficiency.

- Medium Speed (100-1000 RPM): Four-stroke engines commonly found in a wide range of vessels including ferries, cruise ships, and some cargo ships.

- High Speed (>1000 RPM): Compact and powerful engines often used in smaller vessels, naval ships, and for auxiliary power in larger vessels.

Regional Highlights

The Marine Diesel Market exhibits significant regional variations, with certain geographies playing pivotal roles due to their extensive maritime activities, robust shipbuilding industries, or strategic geopolitical importance. Understanding these regional dynamics is crucial for market participants looking to tailor their strategies and investments to specific local conditions and opportunities. Each region contributes distinctly to the global market, driven by a unique mix of economic growth, regulatory frameworks, and technological adoption rates.

Asia Pacific, for instance, stands out as a dominant force due to its immense shipbuilding capacity and burgeoning international trade. Europe and North America, while having mature maritime sectors, are key drivers of technological innovation and regulatory compliance, influencing global standards. Latin America and the Middle East & Africa represent emerging markets with significant potential, spurred by infrastructure development and increasing demand for maritime transport. A deep dive into these regional performances provides a comprehensive understanding of the market's global footprint and future trajectory.

- Asia Pacific (APAC): Dominates the market due to its robust shipbuilding industry, increasing trade volumes, and growing number of active ports, particularly in countries like China, South Korea, Japan, and India. The region's economic growth fuels higher demand for new vessels and, consequently, marine diesel engines and fuel. Strict environmental regulations are also driving demand for modern, compliant engines in this region.

- Europe: A mature market with a strong emphasis on technological advancements and environmental compliance. Countries such as Germany, Norway, and the Netherlands are at the forefront of developing highly efficient and low-emission marine diesel engines. The region also has a significant market for cruise ships and ferries, driving demand for specific engine types.

- North America: Characterized by strong demand from the commercial shipping, offshore, and recreational boating sectors. The implementation of Emission Control Areas (ECAs) along its coasts has driven the adoption of lower-sulfur fuels and more advanced engine technologies. The region's focus on inland waterways transportation also contributes to market demand.

- Middle East and Africa (MEA): Emerging as a crucial region due to strategic shipping lanes, growing oil and gas activities (offshore vessels), and increasing investment in port infrastructure. The expansion of maritime trade and energy exploration projects is set to fuel demand for marine diesel products and services in the coming years.

- Latin America: Expected to witness steady growth, driven by expanding trade activities, particularly in raw materials and agricultural products, which necessitate robust shipping operations. Investment in naval fleets and coastal transportation also contributes to the demand for marine diesel engines and fuel.

Top Key Players:

The market research report covers the analysis of key stake holders of the Marine Diesel Market. Some of the leading players profiled in the report include -:- Wartsila Corporation

- Caterpillar Inc.

- MAN Energy Solutions

- Yanmar Holdings Co. Ltd.

- Rolls-Royce plc

- Cummins Inc.

- Hyundai Heavy Industries Co. Ltd. (Engine & Machinery Division)

- Mitsubishi Heavy Industries Ltd.

- Deutz AG

- Isuzu Motors Ltd.

- Daihatsu Diesel Mfg. Co. Ltd.

- Kawasaki Heavy Industries Ltd.

- Volvo Penta (Volvo Group)

- ABB Ltd. (Marine & Ports)

- GE Marine (General Electric)

- FPT Industrial (CNH Industrial)

- Anglo Belgian Corporation (ABC)

- Bergen Engines AS

- Niigata Power Systems Co. Ltd.

- JFE Engineering Corporation

Frequently Asked Questions:

What is the current market size of the Marine Diesel Market?

The Marine Diesel Market was valued at USD 19.5 billion in 2025 and is projected to reach USD 28.3 billion by 2033. This growth is driven by increasing global maritime trade and advancements in engine technology.

What are the primary drivers for the growth of the Marine Diesel Market?

Key drivers include the growth in global maritime trade, stringent environmental regulations pushing for cleaner and more efficient engines, and continuous technological advancements aimed at improving fuel efficiency and reducing emissions. The demand for new vessel construction also significantly contributes to market expansion.

How do environmental regulations impact the Marine Diesel Market?

Environmental regulations, particularly those from the IMO concerning sulfur emissions (IMO 2020) and greenhouse gases (EEXI, CII), significantly impact the Marine Diesel Market by mandating the use of low-sulfur fuels and driving the adoption of advanced emission control technologies or dual-fuel engine systems. This pushes innovation and retrofitting, making compliance a major market influencer.

What are the emerging trends in marine diesel engine technology?

Emerging trends include the development and adoption of dual-fuel engines that can run on both diesel and alternative fuels like LNG, the integration of digitalization and AI for predictive maintenance and operational optimization, and continued innovation in engine design for enhanced fuel efficiency and reduced emissions through technologies like exhaust gas recirculation (EGR) and selective catalytic reduction (SCR).

Which regions are key contributors to the Marine Diesel Market?

Asia Pacific is a dominant region due to its significant shipbuilding industry and high trade volumes. Europe and North America are also key contributors, recognized for their technological advancements and strict regulatory frameworks that drive demand for advanced diesel solutions. The Middle East & Africa, and Latin America are emerging as vital regions due to growing maritime activities and infrastructure development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted