Onboard Marine Genset Market

Onboard Marine Genset Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703390 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

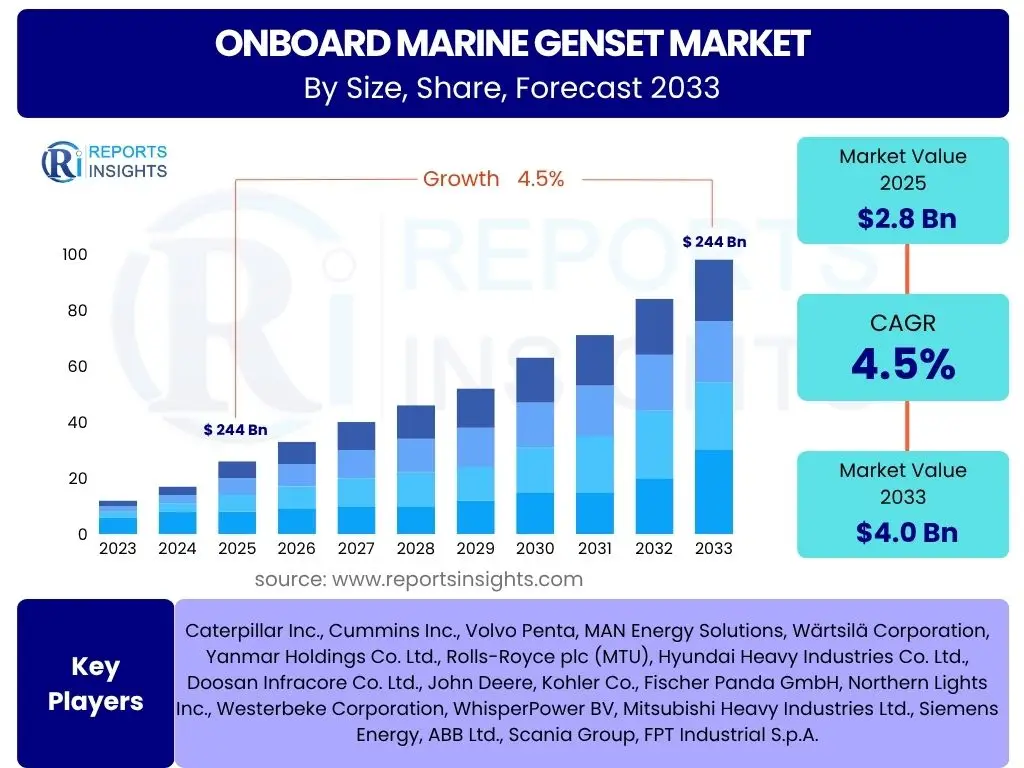

Onboard Marine Genset Market Size

According to Reports Insights Consulting Pvt Ltd, The Onboard Marine Genset Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 2.8 Billion in 2025 and is projected to reach USD 4.0 Billion by the end of the forecast period in 2033.

Key Onboard Marine Genset Market Trends & Insights

User queries regarding trends in the Onboard Marine Genset market frequently center on technological advancements, environmental compliance, and the shifting landscape of marine propulsion. There is significant interest in understanding how hybrid and electric propulsion systems are influencing genset design and demand, as well as the adoption of cleaner fuel alternatives. Furthermore, questions often arise about the integration of smart technologies for enhanced operational efficiency and predictive maintenance capabilities.

The market is witnessing a notable pivot towards solutions that offer reduced emissions and improved fuel efficiency, driven by stringent international maritime regulations. This includes the development of gensets compatible with alternative fuels such as LNG, methanol, and hydrogen, alongside the increasing integration of battery storage systems to create hybrid power solutions. Digitalization and connectivity are also becoming paramount, enabling advanced monitoring and remote diagnostics.

- Shift towards hybrid and electric propulsion systems for reduced emissions and fuel consumption.

- Increasing adoption of alternative fuels, including LNG, methanol, and hydrogen, for marine gensets.

- Integration of advanced digital technologies for remote monitoring, predictive maintenance, and optimized performance.

- Focus on modular and compact genset designs to maximize space utilization on board.

- Development of quieter and more vibration-dampened gensets for enhanced passenger comfort and crew well-being.

AI Impact Analysis on Onboard Marine Genset

Common user questions related to the impact of AI on Onboard Marine Genset technology revolve around its potential for optimizing fuel efficiency, enabling predictive maintenance, and facilitating autonomous operation. Users are keen to understand how AI algorithms can analyze real-time operational data to anticipate failures, schedule maintenance proactively, and fine-tune engine performance for optimal energy consumption. There is also interest in AI's role in the broader context of smart vessel management systems and decision-making processes.

AI's influence on marine gensets is primarily concentrated on enhancing operational intelligence and reliability. Through machine learning, AI can process vast amounts of sensor data from gensets, including temperature, pressure, vibration, and fuel flow, to identify anomalies and predict potential component failures long before they occur. This transition from reactive to proactive maintenance significantly reduces downtime and operational costs. Moreover, AI-driven optimization algorithms can dynamically adjust genset loads and operating parameters based on real-time power demand and environmental conditions, leading to substantial improvements in fuel efficiency and reduced emissions.

- Predictive maintenance: AI analyzes sensor data to forecast equipment failures, reducing unplanned downtime.

- Fuel efficiency optimization: AI algorithms dynamically adjust genset operations based on load, optimizing fuel consumption.

- Autonomous operation integration: AI facilitates seamless integration with autonomous vessel systems for power management.

- Real-time diagnostics: AI provides immediate insights into genset health and performance.

- Lifecycle management: AI supports optimization of genset operation and maintenance throughout its lifespan.

Key Takeaways Onboard Marine Genset Market Size & Forecast

Analysis of common user questions regarding key takeaways from the Onboard Marine Genset market size and forecast reveals a strong interest in understanding the primary drivers of market expansion, the influence of regulatory frameworks, and the geographic distribution of growth opportunities. Users frequently inquire about the relative importance of commercial versus recreational marine sectors and the long-term viability of different fuel types in the context of global decarbonization efforts. The emphasis is on identifying the most impactful factors shaping the market's trajectory through the forecast period.

The market is poised for steady growth, primarily propelled by increasing global maritime trade, a growing demand for luxury yachts and cruise liners, and the continuous modernization of naval fleets. Regulatory mandates for lower emissions, particularly from organizations like the International Maritime Organization (IMO), are compelling manufacturers to innovate cleaner and more efficient genset solutions, fostering a robust demand for advanced technologies. While diesel gensets continue to dominate, there is a clear trend towards hybrid and alternative fuel systems, reflecting a broader industry commitment to sustainability.

- Sustainable growth is anticipated, driven by global trade expansion and increasing demand across diverse marine applications.

- Regulatory pressure for emission reduction is a primary catalyst for technological innovation and market evolution.

- Hybrid and alternative fuel gensets represent a significant future growth segment, alongside conventional diesel solutions.

- Asia Pacific is expected to remain a dominant region due to robust shipbuilding and maritime activity.

- Investments in digitalization and smart genset technologies are crucial for competitive advantage and operational efficiency.

Onboard Marine Genset Market Drivers Analysis

The Onboard Marine Genset market is significantly propelled by several macro and microeconomic factors. A primary driver is the steady expansion of the global maritime trade, which necessitates a larger and more modern fleet of cargo, container, and special purpose vessels, all requiring reliable onboard power generation. Concurrently, the burgeoning tourism sector, particularly the cruise and luxury yacht segments, continues to demand high-performance, quiet, and efficient gensets to ensure passenger comfort and meet stringent environmental standards. The global emphasis on decarbonization and stricter emission regulations from bodies like the IMO also acts as a powerful driver, pushing manufacturers towards cleaner, more efficient, and alternative-fuel compatible genset technologies.

Furthermore, the increasing demand for specialized vessels in sectors such as offshore wind, oil and gas, and scientific research contributes to market growth. These vessels often operate in remote or harsh environments, requiring highly reliable and robust power systems. Advancements in power electronics and battery technology are also enabling the adoption of hybrid propulsion systems, where gensets play a crucial role in charging batteries and providing peak power, thereby enhancing overall system efficiency and reducing fuel consumption. This technological evolution aligns with the industry's drive towards greater sustainability and operational flexibility.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Maritime Trade & Shipbuilding | +1.5% | Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Increasing Demand for Luxury Yachts & Cruise Ships | +1.0% | North America, Europe, Caribbean | Medium-term (2025-2030) |

| Stricter Environmental Regulations (IMO Tier III) | +1.2% | Global, particularly Europe, North America | Ongoing (2025-2033) |

| Technological Advancements in Hybrid/Electric Propulsion | +0.8% | Europe, North America, East Asia | Medium-to-Long-term (2026-2033) |

| Growth in Offshore Support & Specialized Vessels | +0.5% | Europe, North America, Southeast Asia | Long-term (2025-2033) |

Onboard Marine Genset Market Restraints Analysis

Despite robust growth drivers, the Onboard Marine Genset market faces several significant restraints. One primary challenge is the high initial capital expenditure associated with purchasing and installing advanced genset systems, particularly those incorporating alternative fuel technologies or complex hybrid configurations. This cost can be a deterrent for smaller vessel operators or those with limited budgets, leading to slower adoption rates of newer, more efficient technologies. Additionally, the operational costs, including fluctuating fuel prices and the need for specialized maintenance, further contribute to the financial burden on vessel owners.

Another crucial restraint is the ongoing global economic uncertainties, which can lead to volatility in new vessel orders and shipbuilding activities. Any downturn in global trade or recreational boating can directly impact the demand for new gensets. Furthermore, the complexity of integrating sophisticated genset systems with existing vessel infrastructure, particularly in retrofit scenarios, poses technical challenges. The availability of bunkering infrastructure for alternative fuels like LNG or hydrogen remains limited in many ports worldwide, hindering the widespread adoption of these cleaner technologies. Lastly, the availability of skilled personnel for installation, operation, and maintenance of these increasingly complex systems can be a bottleneck in certain regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -0.8% | Global, especially developing economies | Long-term (2025-2033) |

| Volatility in Fuel Prices & Operating Costs | -0.6% | Global | Ongoing (2025-2033) |

| Limited Bunkering Infrastructure for Alternative Fuels | -0.7% | Global, particularly less developed ports | Medium-term (2025-2030) |

| Complex Integration & Retrofit Challenges | -0.4% | Global | Medium-term (2025-2030) |

| Economic Downturns & Geopolitical Instability | -0.5% | Global, varying by region | Short-to-Medium-term (2025-2028) |

Onboard Marine Genset Market Opportunities Analysis

Significant opportunities exist within the Onboard Marine Genset market, driven by the ongoing pursuit of sustainable maritime solutions and technological innovation. The increasing global focus on decarbonization and the shipping industry's commitment to achieving net-zero emissions present a substantial opportunity for manufacturers of gensets compatible with hydrogen, ammonia, and other zero-emission fuels. While these technologies are still nascent, early movers stand to gain a significant competitive advantage as infrastructure develops and regulatory frameworks solidify. The development of more efficient and compact genset designs, potentially leveraging micro-gas turbines or advanced fuel cells, could unlock new markets and applications, especially in space-constrained vessels.

Furthermore, the growth of the offshore energy sector, including offshore wind farms and aquaculture, presents a robust demand for specialized support vessels that require highly reliable and efficient onboard power systems. These vessels often operate continuously for extended periods, necessitating robust gensets with long service intervals and advanced monitoring capabilities. The retrofit market also offers a substantial opportunity, as older vessels seek to upgrade their power systems to comply with new emission regulations or to improve fuel efficiency and operational flexibility. Digitalization and the integration of smart technologies, such as IoT-enabled monitoring and predictive analytics, represent another key area for value creation and differentiation within the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Zero-Emission Fuels (Hydrogen, Ammonia) | +1.0% | Europe, Asia Pacific, North America | Long-term (2028-2033) |

| Growth in Offshore Wind & Aquaculture Support Vessels | +0.9% | Europe, Asia Pacific, North America | Long-term (2025-2033) |

| Increasing Demand for Retrofitting Existing Fleets | +0.7% | Global, especially Europe, North America | Medium-to-Long-term (2026-2033) |

| Advancements in Fuel Cell Technology for Marine Use | +0.6% | Europe, East Asia | Long-term (2029-2033) |

| Integration of Advanced Digital & AI Solutions | +0.5% | Global | Medium-term (2025-2030) |

Onboard Marine Genset Market Challenges Impact Analysis

The Onboard Marine Genset market is confronted with several significant challenges that could impede its growth trajectory. One pervasive challenge is the increasing complexity of international maritime regulations concerning emissions, particularly the IMO's carbon intensity indicator (CII) and existing NOx/SOx limits. While these regulations drive innovation, they also impose significant compliance burdens on manufacturers and operators, requiring constant R&D investment and potentially increasing the cost of genset solutions. Adapting to diverse regional and national regulations further complicates market entry and product development.

Another substantial challenge is the fluctuating costs of raw materials and global supply chain disruptions. The manufacturing of gensets relies on a variety of components, and volatility in prices or availability of materials like steel, copper, and specialized electronic components can directly impact production costs and lead times. Furthermore, the integration of new, more sophisticated genset technologies, especially hybrid and alternative fuel systems, requires specialized expertise for installation, commissioning, and ongoing maintenance. A shortage of skilled technicians capable of handling these advanced systems across various global ports poses a significant operational challenge for the industry, potentially affecting service quality and vessel uptime.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent & Evolving Emission Regulations | -0.9% | Global | Ongoing (2025-2033) |

| Supply Chain Disruptions & Raw Material Volatility | -0.7% | Global | Short-to-Medium-term (2025-2027) |

| Shortage of Skilled Workforce for New Technologies | -0.6% | Global, particularly specialized segments | Long-term (2025-2033) |

| Cybersecurity Risks for Connected Systems | -0.3% | Global | Medium-to-Long-term (2026-2033) |

| High Research & Development Costs for Innovation | -0.4% | Global | Long-term (2025-2033) |

Onboard Marine Genset Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Onboard Marine Genset market, offering crucial insights into its size, growth trajectory, key trends, and influencing factors from 2019 to 2033. It encompasses a detailed segmentation analysis by power output, fuel type, application, and end-user, along with a thorough regional breakdown to highlight opportunities and challenges across major geographies. The report further profiles leading market players, assesses the impact of emerging technologies like AI, and provides a strategic outlook to assist stakeholders in informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 4.0 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Caterpillar Inc., Cummins Inc., Volvo Penta, MAN Energy Solutions, Wärtsilä Corporation, Yanmar Holdings Co. Ltd., Rolls-Royce plc (MTU), Hyundai Heavy Industries Co. Ltd., Doosan Infracore Co. Ltd., John Deere, Kohler Co., Fischer Panda GmbH, Northern Lights Inc., Westerbeke Corporation, WhisperPower BV, Mitsubishi Heavy Industries Ltd., Siemens Energy, ABB Ltd., Scania Group, FPT Industrial S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Onboard Marine Genset market is comprehensively segmented based on several critical parameters to provide a granular view of its dynamics and opportunities. These segmentations allow for a detailed analysis of specific market niches, enabling stakeholders to identify high-growth areas and tailor their strategies effectively. The primary segmentation criteria include power output, fuel type, application, and end-user, each providing unique insights into demand patterns and technological preferences within the maritime industry.

The power output segmentation categorizes gensets by their capacity, reflecting varying energy requirements across different vessel types, from small recreational boats to large commercial ships. Fuel type segmentation highlights the shift towards cleaner energy sources, encompassing traditional diesel alongside emerging hybrid, LNG, and other alternative fuel solutions. Application-based segmentation provides clarity on demand from distinct marine sectors such as commercial shipping, leisure, offshore, and naval operations, each with unique operational demands and regulatory landscapes. Finally, the end-user segmentation differentiates between original equipment manufacturers (OEMs) for new vessel builds and the aftermarket segment, which covers replacements, upgrades, and maintenance.

- By Power Output:

- Below 100 kW: Typically used in smaller recreational vessels, auxiliary power for yachts, or backup power in compact commercial boats.

- 100 kW - 500 kW: Common for medium-sized commercial vessels, larger yachts, and offshore support vessels requiring substantial continuous power.

- Above 500 kW: Primarily for large commercial ships, cruise liners, naval vessels, and specialized offshore platforms demanding high power generation capabilities.

- By Fuel Type:

- Diesel: Remains the most prevalent fuel type due to its high energy density and established infrastructure, particularly in existing fleets.

- Hybrid (Diesel-Electric): Growing in popularity, combining diesel gensets with battery banks to optimize fuel efficiency, reduce emissions, and enhance operational flexibility.

- LNG (Liquefied Natural Gas): Gaining traction as a cleaner burning fuel, offering significant reductions in NOx, SOx, and particulate matter emissions.

- Other (Methanol, Hydrogen, etc.): Emerging as future-proof solutions, driven by long-term decarbonization goals, though infrastructure and technological maturity are still developing.

- By Application:

- Commercial Vessels: Includes cargo ships, container vessels, tankers, bulk carriers, and ferries, requiring robust and reliable power for continuous operation.

- Recreational Vessels: Comprises luxury yachts, cruise ships, and smaller pleasure boats, prioritizing quiet operation, compactness, and high-quality power for onboard amenities.

- Offshore Vessels: Encompasses offshore support vessels (OSVs), drilling rigs, and floating production storage and offloading (FPSO) units, demanding highly resilient and powerful gensets for demanding operations.

- Naval & Defense Vessels: Requires specialized gensets meeting stringent military specifications for reliability, shock resistance, stealth, and electromagnetic compatibility.

- By End-User:

- Original Equipment Manufacturers (OEMs): Purchases gensets for integration into new vessel builds, driven by new shipbuilding orders and design specifications.

- Aftermarket: Involves the replacement, repair, and upgrade of existing gensets on operational vessels, driven by maintenance cycles, regulatory compliance, and performance enhancement needs.

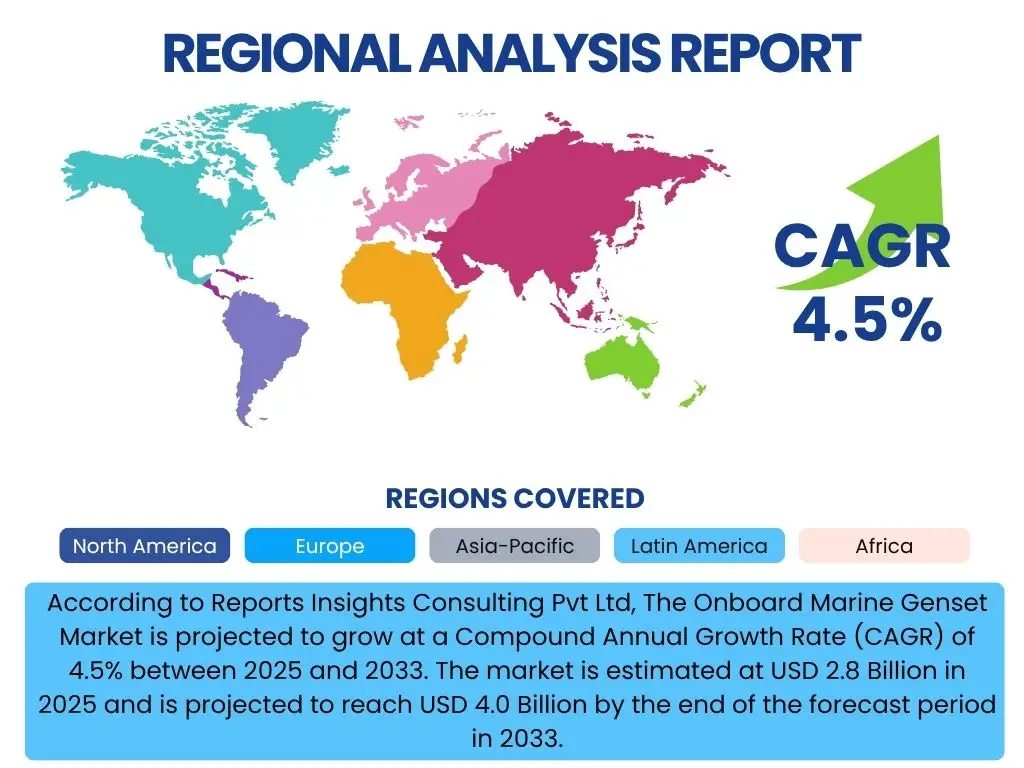

Regional Highlights

- North America: This region demonstrates a steady demand, particularly from the recreational boating sector and specialized vessel markets such as offshore support and coastal trade. Strict environmental regulations and a preference for advanced, quieter, and more efficient gensets are key drivers. The U.S. and Canada are significant contributors to market revenue due to robust maritime activities and technological adoption.

- Europe: A leading region in marine genset innovation and adoption, driven by stringent environmental regulations (e.g., EU sulfur directive), a strong shipbuilding industry, and a high concentration of luxury yacht manufacturers. Countries like Germany, Norway, Finland, and the Netherlands are at the forefront of developing and implementing hybrid and alternative fuel genset technologies.

- Asia Pacific (APAC): Dominates the market share due to its preeminent position in global shipbuilding, particularly in countries like China, South Korea, and Japan. Rapid expansion of maritime trade, increasing port activities, and growing investments in naval fleets are significant factors. The region is also a key market for both commercial and, increasingly, recreational marine applications.

- Latin America: Expected to show moderate growth, influenced by regional economic development, expansion of commercial fleets, and some activity in the offshore oil and gas sector. Countries like Brazil and Mexico are notable for their maritime industries.

- Middle East and Africa (MEA): This region is characterized by demand from the oil and gas sector, particularly offshore exploration and production, and growing investment in port infrastructure. The expansion of maritime trade routes also contributes to a steady demand for marine gensets, though market growth might be slower compared to other regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Onboard Marine Genset Market.- Caterpillar Inc.

- Cummins Inc.

- Volvo Penta

- MAN Energy Solutions

- Wärtsilä Corporation

- Yanmar Holdings Co. Ltd.

- Rolls-Royce plc (MTU)

- Hyundai Heavy Industries Co. Ltd.

- Doosan Infracore Co. Ltd.

- John Deere

- Kohler Co.

- Fischer Panda GmbH

- Northern Lights Inc.

- Westerbeke Corporation

- WhisperPower BV

- Mitsubishi Heavy Industries Ltd.

- Siemens Energy

- ABB Ltd.

- Scania Group

- FPT Industrial S.p.A.

Frequently Asked Questions

Analyze common user questions about the Onboard Marine Genset market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Onboard Marine Genset market?

The Onboard Marine Genset market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, reaching an estimated USD 4.0 Billion by the end of the forecast period.

What are the primary drivers for the Onboard Marine Genset market?

Key drivers include increasing global maritime trade, rising demand for luxury yachts and cruise ships, and stricter environmental regulations compelling the adoption of cleaner and more efficient genset solutions.

How is AI impacting the marine genset industry?

AI is significantly impacting the industry by enabling advanced predictive maintenance, optimizing fuel efficiency through dynamic load adjustments, and facilitating integration with smart, autonomous vessel power management systems.

Which regions are leading in the Onboard Marine Genset market?

Asia Pacific is expected to lead due to robust shipbuilding, while Europe and North America are also significant regions driven by regulatory advancements and strong recreational marine sectors.

What types of alternative fuels are gaining traction for marine gensets?

While diesel remains dominant, there is a growing trend towards hybrid (diesel-electric) systems, Liquefied Natural Gas (LNG), and emerging fuels like methanol and hydrogen, driven by global decarbonization efforts.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted