Marine Trencher Market

Marine Trencher Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702680 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

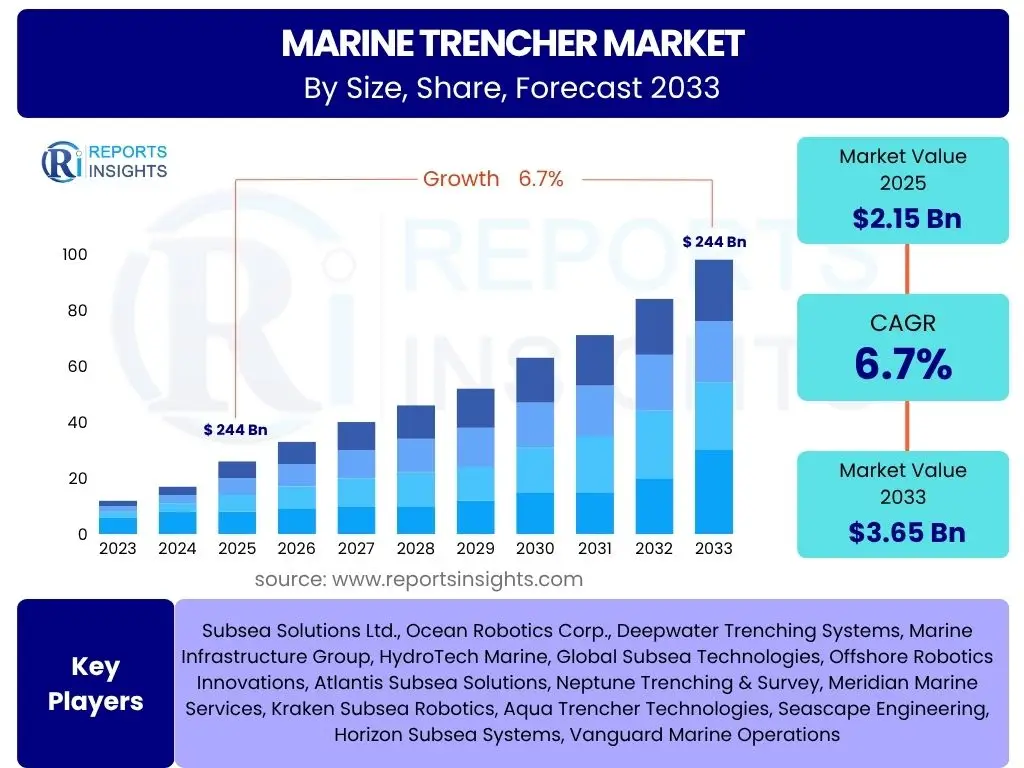

Marine Trencher Market Size

According to Reports Insights Consulting Pvt Ltd, The Marine Trencher Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 2.15 billion in 2025 and is projected to reach USD 3.65 billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the escalating demand for subsea infrastructure development, particularly within the offshore renewable energy sector and telecommunications. The market's expansion reflects a global shift towards deeper water exploration and the need for reliable trenching solutions for cable laying, pipeline burial, and seabed preparation.

The consistent increase in offshore activities, including oil and gas extraction, wind farm installations, and the expansion of global communication networks, underpins the positive market outlook. Innovations in trencher technology, such as enhanced automation, greater operational depths, and improved efficiency, are further contributing to this growth. Companies are investing significantly in research and development to offer advanced solutions that can withstand harsh marine environments and meet stringent industry standards, ensuring the sustained growth and technological evolution of the marine trencher market.

Key Marine Trencher Market Trends & Insights

User inquiries about marine trencher market trends frequently focus on the adoption of autonomous capabilities, the impact of renewable energy projects, and the evolution of subsea infrastructure. The market is witnessing a strong trend towards higher automation and remote operability, driven by the need for increased efficiency, reduced human intervention in hazardous environments, and lower operational costs. This technological shift enables trenching operations in deeper waters and more challenging seabed conditions, expanding the potential scope of subsea projects globally. Furthermore, the burgeoning offshore wind sector is a pivotal driver, creating substantial demand for trenchers capable of burying inter-array and export cables, ensuring their protection and stability.

Another significant trend involves the development of hybrid and electric-powered trenchers, aligning with global efforts towards decarbonization and environmental sustainability. These innovations aim to reduce fuel consumption and emissions, making operations more eco-friendly and economically viable in the long term. Concurrently, there is an increasing emphasis on integrated solutions that combine trenching with other subsea services, such as inspection, repair, and maintenance, offering comprehensive project management capabilities. The market is also seeing a rise in specialized trenchers designed for specific applications, like rock trenching or precise shallow-water operations, addressing diverse project requirements with tailored solutions.

- Increased demand from offshore wind farm development for cable burial.

- Rising adoption of Remotely Operated Vehicle (ROV) and Autonomous Underwater Vehicle (AUV) trenchers for enhanced safety and efficiency.

- Technological advancements in rock trenching capabilities and deep-water operations.

- Focus on environmentally sustainable and energy-efficient trencher designs (e.g., electric/hybrid systems).

- Growing trend towards integrated subsea services including trenching, inspection, and maintenance.

AI Impact Analysis on Marine Trencher

User questions related to AI's impact on marine trenchers often revolve around automation levels, predictive maintenance capabilities, and data-driven operational optimization. Artificial intelligence is poised to significantly transform the marine trencher market by enhancing operational intelligence, safety, and efficiency. AI algorithms can process vast amounts of data from sonar, sensors, and navigational systems to provide real-time insights into seabed conditions, trenching progress, and equipment performance. This capability allows for dynamic adjustments to trencher operations, optimizing trench profiles, minimizing energy consumption, and preventing potential equipment failures. Furthermore, AI-powered vision systems can improve obstacle avoidance and ensure precise cable or pipeline burial, reducing the risk of damage and rework.

The implementation of AI also extends to predictive maintenance, where machine learning models analyze historical operational data to anticipate equipment malfunctions before they occur. This proactive approach significantly reduces downtime, extends the lifespan of expensive components, and optimizes maintenance schedules, leading to substantial cost savings. Moreover, AI can facilitate more autonomous operations, allowing trenchers to execute complex tasks with minimal human intervention, especially in hazardous or deep-water environments. This not only enhances safety for human operators but also enables round-the-clock operations, boosting project timelines and overall productivity. The integration of AI is not merely an incremental improvement but a fundamental shift towards smarter, more resilient, and highly efficient marine trenching solutions, paving the way for fully autonomous subsea construction in the future.

- Enhanced autonomous operation and navigation for trenchers, reducing human error.

- Predictive maintenance analytics for equipment, minimizing downtime and optimizing lifespan.

- Real-time data analysis for optimized trenching parameters and improved precision.

- AI-powered obstacle detection and avoidance systems for safer operations.

- Improved efficiency through adaptive planning and resource allocation based on AI insights.

Key Takeaways Marine Trencher Market Size & Forecast

Common user inquiries regarding marine trencher market size and forecast highlight the industry's sustained growth, driven by global energy transitions and connectivity demands. The market is projected for significant expansion through 2033, largely fueled by the rapid development of offshore wind farms, which require extensive subsea cable installation and protection. The increasing investment in renewable energy infrastructure worldwide creates a consistent and growing demand for specialized trenching services. Additionally, the continuous expansion and upgrade of global telecommunication networks, particularly the laying of new fiber optic cables across oceans, contribute substantially to market vitality. This foundational demand ensures a stable growth trajectory for the marine trencher market.

Technological innovation represents another crucial takeaway, with advancements in trencher capabilities, such as greater operating depths, improved efficiency in diverse seabed conditions, and increased automation, being key drivers. The market is characterized by a shift towards more sophisticated and adaptable trenching solutions that can handle complex projects in challenging environments. Furthermore, the strategic importance of protecting critical subsea assets, like power cables and pipelines, against external damage underscores the ongoing need for effective burial solutions. These combined factors solidify the marine trencher market as a vital component of global offshore infrastructure development, presenting robust opportunities for technology providers and service operators alike.

- Significant market growth driven by offshore renewable energy projects and telecommunications.

- Increasing adoption of advanced and autonomous trencher technologies.

- High demand for subsea cable and pipeline protection in diverse marine environments.

- Market expansion into deeper waters and more challenging seabed conditions.

- Continued investment in R&D to enhance efficiency and reduce operational costs.

Marine Trencher Market Drivers Analysis

The marine trencher market is propelled by several key drivers that reflect global energy shifts, increasing connectivity, and the need for robust subsea infrastructure. A primary driver is the accelerating development of offshore wind energy projects globally. These installations require extensive networks of inter-array and export cables to connect turbines to substations and then to onshore grids, all of which need to be buried for protection from anchors, fishing gear, and natural seabed movements. This surge in offshore wind capacity directly translates into higher demand for specialized trenching services and equipment, making it a critical growth catalyst for the market.

Another significant driver is the continuous expansion and upgrade of subsea telecommunication networks. The global demand for high-speed internet and data transfer necessitates the laying of new intercontinental fiber optic cables, which require precise and secure burial. Additionally, the ongoing exploration and production activities in the oil and gas sector, particularly in deeper waters, also contribute to market growth as new pipelines and umbilicals need to be installed and protected. These factors collectively underscore the indispensable role of marine trenchers in facilitating modern global energy and communication infrastructures.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Offshore Wind Farm Installations | +2.1% | Europe, North America, Asia Pacific (APAC) | 2025-2033 (Long-Term) |

| Expansion of Submarine Cable Networks (Telecom & Power) | +1.8% | Global, particularly Asia Pacific, North America | 2025-2033 (Long-Term) |

| Increased Deepwater Oil & Gas Exploration and Production | +0.9% | North America, Latin America, Middle East | 2025-2030 (Medium-Term) |

| Focus on Subsea Asset Protection and Integrity | +0.7% | Global | 2025-2033 (Long-Term) |

| Technological Advancements in Trenching Equipment | +1.2% | Global | 2025-2033 (Long-Term) |

Marine Trencher Market Restraints Analysis

Despite the robust growth drivers, the marine trencher market faces several significant restraints that could temper its expansion. One major restraint is the high capital investment required for acquiring and maintaining advanced trenching equipment. Marine trenchers, especially those designed for deep-water or rock trenching, are complex, specialized machinery that involves substantial upfront costs, making entry into the market challenging for new players and imposing considerable financial burdens on existing operators. This high expenditure extends to operational costs, including fuel, maintenance, and highly skilled personnel, which can impact project profitability, especially in a competitive bidding environment.

Another critical restraint involves stringent environmental regulations and permitting processes. Offshore operations are subject to strict rules concerning seabed disturbance, noise pollution, and potential impacts on marine ecosystems. Obtaining the necessary permits can be time-consuming and complex, leading to project delays and increased administrative costs. Furthermore, the volatility of commodity prices, particularly in the oil and gas sector, can lead to fluctuations in investment decisions for new offshore projects, thereby indirectly impacting the demand for trenching services. The shortage of highly skilled operators and technical personnel capable of managing sophisticated marine trenching equipment also poses a challenge, potentially limiting operational capacity and efficiency across the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital & Operational Expenditure | -1.5% | Global | 2025-2033 (Long-Term) |

| Stringent Environmental Regulations & Permitting | -1.1% | Europe, North America | 2025-2033 (Long-Term) |

| Volatility in Commodity Prices (Oil & Gas) | -0.8% | Global | 2025-2030 (Medium-Term) |

| Shortage of Skilled Personnel | -0.6% | Global | 2025-2033 (Long-Term) |

| Unfavorable Weather Conditions & Operational Risks | -0.5% | Global, particularly harsh environments | 2025-2033 (Long-Term) |

Marine Trencher Market Opportunities Analysis

The marine trencher market presents several compelling opportunities for growth and innovation. The most significant opportunity lies in the burgeoning offshore renewable energy sector, beyond just wind farms, including emerging technologies like wave and tidal energy. As these nascent industries mature, they will require extensive subsea infrastructure, including power export cables and anchoring systems, creating new and substantial demand for specialized trenching solutions. This diversification within the renewable energy landscape offers a long-term growth avenue for trencher manufacturers and service providers, moving beyond traditional oil and gas applications.

Another key opportunity stems from the increasing global investment in deep-water and ultra-deep-water projects, both for oil and gas and for scientific research and exploration. Operating in these extreme environments necessitates highly advanced and robust trenchers capable of enduring immense pressures and complex seabed conditions. This drives innovation in remotely operated and autonomous trenching technologies, presenting opportunities for companies that can develop cutting-edge solutions for these challenging frontiers. Furthermore, the development of new subsea applications, such as carbon capture and storage infrastructure or advanced sensor networks for ocean monitoring, also opens up niche market segments for customized trenching services, further expanding the market's potential scope.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Offshore Renewable Energy Sources (e.g., Wave, Tidal) | +1.5% | Europe, Asia Pacific | 2028-2033 (Long-Term) |

| Growth in Deepwater & Ultra-Deepwater Projects | +1.3% | Latin America, Africa, North America | 2025-2033 (Long-Term) |

| Technological Innovation in Autonomous & AI-Powered Trenchers | +1.1% | Global | 2025-2033 (Long-Term) |

| Expansion into New Subsea Applications (e.g., Ocean Monitoring, Carbon Storage) | +0.9% | Global | 2028-2033 (Long-Term) |

| Increasing Focus on Subsea Decommissioning Activities | +0.7% | North Sea, Gulf of Mexico | 2025-2033 (Long-Term) |

Marine Trencher Market Challenges Impact Analysis

The marine trencher market faces several significant challenges that operators and manufacturers must navigate. Operating in harsh and unpredictable marine environments poses a constant challenge, as extreme weather conditions, strong currents, and varying seabed compositions can severely impact operational efficiency and safety. These environmental factors necessitate robust and adaptable equipment, leading to higher design and manufacturing costs. Furthermore, the logistical complexities associated with mobilizing, deploying, and maintaining specialized vessels and trenching equipment in remote offshore locations add substantial operational burdens and can lead to project delays.

Another major challenge is the intense competition within the market, which can exert downward pressure on pricing and profit margins. Companies must continuously innovate and optimize their services to remain competitive, often investing heavily in new technologies and fleet upgrades. Regulatory compliance, particularly across diverse international jurisdictions, presents another hurdle, as differing environmental standards and permitting requirements can complicate project planning and execution. Ensuring the safety of personnel during complex subsea operations and mitigating the risks of equipment failure in challenging conditions also remain paramount concerns that demand continuous vigilance and investment in training and advanced safety protocols.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Harsh Marine Operating Environments & Weather Risks | -1.0% | Global, particularly North Sea, Atlantic | 2025-2033 (Long-Term) |

| Technical Complexity & Equipment Reliability in Deepwater | -0.9% | Global | 2025-2033 (Long-Term) |

| Logistical Challenges & High Mobilization Costs | -0.7% | Global | 2025-2033 (Long-Term) |

| Intense Market Competition & Price Pressure | -0.6% | Global | 2025-2030 (Medium-Term) |

| Cybersecurity Risks for Remote & Autonomous Systems | -0.4% | Global | 2025-2033 (Long-Term) |

Marine Trencher Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Marine Trencher Market, covering market sizing, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis by type, application, operating depth, and propulsion, alongside a thorough regional assessment. The report also includes an impact analysis of AI on the market and profiles of leading industry players, providing stakeholders with critical insights for strategic decision-making and market positioning from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.15 billion |

| Market Forecast in 2033 | USD 3.65 billion |

| Growth Rate | 6.7% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Subsea Solutions Ltd., Ocean Robotics Corp., Deepwater Trenching Systems, Marine Infrastructure Group, HydroTech Marine, Global Subsea Technologies, Offshore Robotics Innovations, Atlantis Subsea Solutions, Neptune Trenching & Survey, Meridian Marine Services, Kraken Subsea Robotics, Aqua Trencher Technologies, Seascape Engineering, Horizon Subsea Systems, Vanguard Marine Operations |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Marine Trencher Market is extensively segmented to provide a granular view of its diverse applications and technological variations. This segmentation helps in understanding the specific demands and growth pockets within the industry, enabling targeted strategies for market participants. The primary segments include trenchers categorized by their operational type, their key application areas, the depths at which they can operate, and their method of propulsion, each reflecting distinct technological requirements and market dynamics.

The Type segmentation differentiates between Remotely Operated Vehicle (ROV) trenchers, which offer flexibility and precision, mechanical trenchers used for tougher seabed conditions, and jetting trenchers ideal for softer soils. Application segmentation highlights the dominance of offshore renewable energy and telecommunications, alongside traditional oil and gas. Operating Depth categorizes equipment for shallow, deep, or ultra-deep waters, acknowledging the varying engineering challenges. Finally, propulsion type distinguishes between tracked, skidded, and free-swimming systems, each suited for different operational environments and mobility requirements.

- By Type:

- Remotely Operated Vehicle (ROV) Trenchers

- Mechanical Trenchers

- Jetting Trenchers

- By Application:

- Oil & Gas

- Renewable Energy (Offshore Wind, Wave, Tidal)

- Telecommunications

- Decommissioning

- Others (Scientific Research, Mineral Exploration)

- By Operating Depth:

- Shallow Water (up to 100 meters)

- Deep Water (100 to 1,000 meters)

- Ultra-Deep Water (above 1,000 meters)

- By Propulsion Type:

- Tracked

- Skidded

- Free Swimming (AUV/ROV variants)

Regional Highlights

- Europe: Dominant market share driven by extensive offshore wind farm development in the North Sea and Baltic Sea, coupled with stringent regulations on cable and pipeline protection. Strong focus on technological innovation and sustainable solutions.

- North America: Significant growth in offshore oil and gas pipeline installations, increasing investment in new offshore wind projects (e.g., East Coast USA), and a robust telecommunications infrastructure driving demand for trenching.

- Asia Pacific (APAC): Fastest-growing region due to rapid industrialization, burgeoning offshore wind capacity in China, Taiwan, Japan, and South Korea, and major investments in new submarine communication cables connecting growing economies.

- Latin America: Driven by deepwater oil and gas projects, particularly in Brazil and Mexico, requiring specialized trenching for pipeline installation and maintenance. Emerging opportunities in renewable energy.

- Middle East and Africa (MEA): Growth attributed to new oil and gas field developments and expansion of regional subsea communication networks. Projects often involve challenging seabed conditions, necessitating robust trenching solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Marine Trencher Market.- Subsea Solutions Ltd.

- Ocean Robotics Corp.

- Deepwater Trenching Systems

- Marine Infrastructure Group

- HydroTech Marine

- Global Subsea Technologies

- Offshore Robotics Innovations

- Atlantis Subsea Solutions

- Neptune Trenching & Survey

- Meridian Marine Services

- Kraken Subsea Robotics

- Aqua Trencher Technologies

- Seascape Engineering

- Horizon Subsea Systems

- Vanguard Marine Operations

Frequently Asked Questions

What is a marine trencher?

A marine trencher is a specialized subsea machine designed to excavate trenches on the seabed. These trenches are primarily used to bury and protect subsea cables (power or telecommunications) and pipelines from external damage caused by fishing gear, ship anchors, or natural seabed movements. Trenchers can operate in various water depths and seabed conditions, utilizing different methods like jetting, mechanical cutting, or plowing.

What are the primary applications of marine trenchers?

Marine trenchers are primarily used for burying subsea power cables for offshore wind farms and other renewable energy projects, installing and protecting oil and gas pipelines, and laying fiber optic telecommunication cables across oceans. They are also employed in subsea infrastructure development, maintenance, and decommissioning activities.

What is the projected growth of the Marine Trencher Market?

The Marine Trencher Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. It is estimated at USD 2.15 billion in 2025 and is forecast to reach USD 3.65 billion by 2033, driven by increasing offshore infrastructure demands.

What technological trends are impacting marine trenchers?

Key technological trends include the increased adoption of Remotely Operated Vehicle (ROV) and Autonomous Underwater Vehicle (AUV) trenchers for enhanced safety and efficiency, advancements in deep-water and rock trenching capabilities, and the development of environmentally friendly electric and hybrid-powered trencher systems. Artificial intelligence and automation are also playing a growing role in operational optimization.

Which regions are key contributors to the Marine Trencher Market?

Europe leads the market due to extensive offshore wind development. Asia Pacific is the fastest-growing region driven by new offshore wind capacity and telecommunication cable projects. North America, Latin America, and the Middle East and Africa also contribute significantly due to oil and gas activities and growing renewable energy investments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted