LNG Tanker Market

LNG Tanker Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705216 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

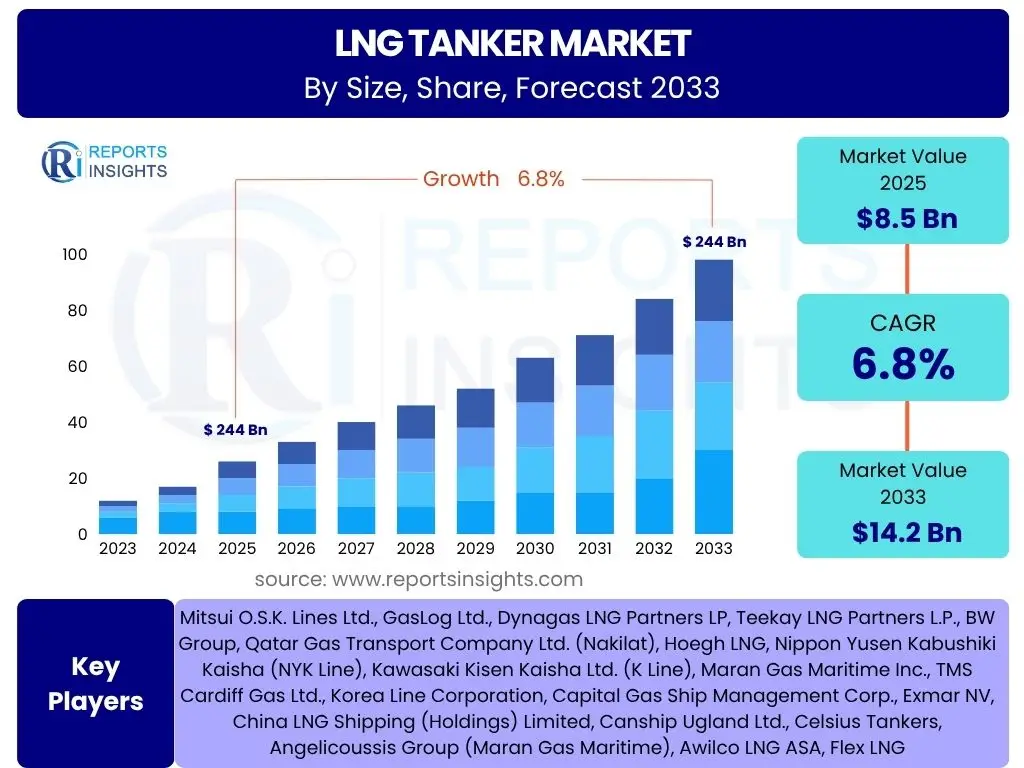

LNG Tanker Market Size

According to Reports Insights Consulting Pvt Ltd, The LNG Tanker Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 14.2 Billion by the end of the forecast period in 2033.

Key LNG Tanker Market Trends & Insights

The LNG tanker market is experiencing significant transformation driven by evolving global energy dynamics and technological advancements. Key trends indicate a robust demand for more efficient and environmentally friendly vessels, as the world increasingly turns to natural gas as a transitional fuel in the shift towards decarbonization. This demand is further fueled by the expansion of liquefaction and regasification terminals worldwide, necessitating a larger and more capable fleet to facilitate international trade routes. The industry is also witnessing a push towards larger vessel capacities and advanced propulsion systems to enhance operational efficiency and reduce emissions.

Another prominent trend is the growing emphasis on digitalization and automation within the LNG tanker fleet. Shipowners and operators are investing in smart technologies, including advanced navigation systems, predictive maintenance tools, and real-time monitoring solutions, to optimize vessel performance, ensure safety, and minimize operational costs. Furthermore, the push for cleaner energy is accelerating the adoption of alternative fuels for the tankers themselves, such as LNG as a marine fuel, creating a self-reinforcing cycle of sustainability within the shipping sector. The geopolitical landscape also plays a crucial role, influencing trade routes and necessitating flexibility in fleet deployment.

- Increased demand for natural gas as a transition fuel drives new vessel orders.

- Focus on larger, more efficient, and eco-friendly vessel designs.

- Rising adoption of dual-fuel and tri-fuel propulsion systems.

- Digitalization and automation for optimized operations and safety.

- Expansion of global LNG liquefaction and regasification infrastructure.

- Development of new trade routes and bunkering hubs.

- Stringent environmental regulations pushing for emissions reduction.

AI Impact Analysis on LNG Tanker

Artificial Intelligence (AI) is set to revolutionize various aspects of the LNG tanker market, offering substantial improvements in operational efficiency, safety, and environmental performance. Common inquiries about AI's role often revolve around its application in optimizing vessel routing, predicting maintenance needs, and enhancing crew training. AI algorithms can analyze vast datasets, including weather patterns, sea conditions, and port congestion, to determine the most fuel-efficient and safest routes, thereby reducing voyage times and carbon emissions. Predictive maintenance, another critical AI application, uses sensor data from vessel machinery to anticipate equipment failures, enabling proactive repairs and significantly minimizing downtime and associated costs.

Beyond operational enhancements, AI is expected to play a pivotal role in refining supply chain logistics and improving risk management within the LNG tanker sector. AI-powered platforms can integrate data from various stakeholders, optimizing the entire LNG value chain from production to delivery. This includes better inventory management, demand forecasting, and scheduling, which can lead to more reliable and cost-effective transportation. Furthermore, AI contributes to enhanced safety protocols through advanced anomaly detection and autonomous navigation systems, although human oversight remains paramount. Concerns primarily focus on data security, the ethical implications of autonomous decision-making, and the need for upskilling the workforce to manage these new technologies effectively.

- Route optimization: AI analyzes real-time data for fuel-efficient and safer voyages.

- Predictive maintenance: AI identifies potential equipment failures before they occur, reducing downtime.

- Enhanced safety: AI supports collision avoidance, navigation, and anomaly detection.

- Supply chain optimization: AI streamlines logistics from liquefaction to regasification.

- Emissions monitoring and reduction: AI helps identify areas for energy efficiency improvements.

- Crew training and simulation: AI-driven simulations enhance crew preparedness and response.

- Autonomous operations: Gradual integration of AI for increased automation in vessel control.

Key Takeaways LNG Tanker Market Size & Forecast

The LNG tanker market is poised for significant expansion, driven by the global energy transition and the increasing importance of natural gas in the world's energy mix. The forecasted growth rate underscores a robust investment climate, as energy companies and maritime operators commit to expanding and modernizing their fleets to meet rising demand. This growth is not merely in the number of vessels but also in their technological sophistication, with a strong emphasis on larger capacities and greener propulsion systems to align with global environmental mandates. The market's upward trajectory reflects confidence in LNG as a crucial bridge fuel for decades to come, especially in regions transitioning away from more carbon-intensive energy sources.

A primary takeaway is the interconnectedness of market growth with infrastructure development. The expansion of LNG export and import terminals globally directly correlates with the need for more tankers. Furthermore, the market outlook is shaped by regional energy policies, geopolitical stability, and the ongoing push for decarbonization within the shipping industry itself. Investors and stakeholders should note the increasing importance of ESG (Environmental, Social, and Governance) factors, which are influencing vessel design, operational practices, and financing decisions. The market is dynamic, necessitating continuous innovation and adaptability from all participants to capitalize on the growth opportunities while mitigating associated risks.

- Sustained strong demand for LNG transport driven by global energy transition.

- Significant fleet expansion and modernization expected through 2033.

- Technological advancements, particularly in propulsion and efficiency, are critical for competitiveness.

- Market growth is highly dependent on global LNG infrastructure development.

- Increasing pressure from environmental regulations will shape future tanker designs and operations.

- ESG considerations are becoming central to investment and operational strategies.

LNG Tanker Market Drivers Analysis

The global shift towards cleaner energy sources is a primary driver for the LNG tanker market. As countries seek to reduce reliance on coal and oil, natural gas, particularly in its liquefied form, serves as a crucial transitional fuel due to its lower carbon emissions compared to other fossil fuels. This increased demand for natural gas necessitates a robust transportation infrastructure, directly fueling the growth of the LNG tanker fleet. Furthermore, the expansion of new liquefaction plants in major gas-producing regions and new regasification terminals in importing nations creates new trade routes and volumes, requiring more specialized vessels to transport LNG across oceans.

Technological advancements and the aging fleet are also significant drivers. Many older LNG tankers are reaching the end of their operational lifespan, necessitating replacement orders that often involve more efficient and environmentally compliant designs. Innovations in propulsion systems, such as dual-fuel engines capable of running on LNG, and improvements in cargo containment systems, enhance the economic viability and environmental footprint of new vessels. Additionally, the increasing global gas trade, driven by geopolitical energy security considerations and competitive pricing, continues to stimulate investment in new and advanced LNG carriers to maintain supply chain resilience and efficiency.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Energy Transition & LNG Demand | +2.1% | Global, particularly Europe, Asia Pacific | 2025-2033 |

| Expansion of LNG Infrastructure (Liquefaction/Regasification) | +1.8% | North America, Qatar, Australia, Europe, Asia | 2025-2033 |

| Fleet Modernization & Replacement Needs | +1.5% | Global | 2025-2030 |

| Technological Advancements in Vessel Design & Propulsion | +0.9% | Global, especially shipbuilding hubs (South Korea, China, Japan) | 2025-2033 |

LNG Tanker Market Restraints Analysis

The LNG tanker market faces several significant restraints that could temper its growth trajectory. High capital investment is a primary barrier; the construction of a single LNG tanker involves substantial financial outlay, making entry for new players challenging and posing a considerable financial burden even for established operators. This high upfront cost is compounded by the long construction times, which can lead to delays in fleet expansion and an inability to quickly respond to sudden shifts in market demand. Furthermore, the specialized nature of LNG transport necessitates highly skilled crews, and a global shortage of such expertise can impact operational efficiency and increase labor costs.

Another critical restraint is the volatility of natural gas prices and geopolitical uncertainties. Fluctuations in gas prices directly affect the economic viability of LNG projects, which in turn impacts demand for transportation services. Geopolitical tensions, trade disputes, and sanctions can disrupt established trade routes, leading to stranded assets or forcing costly rerouting. While LNG is a cleaner fuel, the industry also faces increasing pressure from stringent environmental regulations, particularly concerning methane slip and greenhouse gas emissions, which may necessitate costly modifications or investment in unproven technologies, adding to operational complexities and expenses. The current global economic slowdown and inflationary pressures also contribute to reduced investment appetite.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Costs & Long Construction Timelines | -1.2% | Global | 2025-2033 |

| Volatile Natural Gas Prices & Geopolitical Instability | -0.8% | Global, specific conflict zones | 2025-2030 |

| Stringent Environmental Regulations & Emission Targets | -0.5% | Europe, North America, IMO regulated waters | 2025-2033 |

LNG Tanker Market Opportunities Analysis

Despite existing restraints, the LNG tanker market is replete with significant growth opportunities. The burgeoning small-scale LNG market presents a substantial avenue for expansion, catering to isolated communities, industrial consumers, and remote power generation units that are not connected to traditional pipeline networks. This segment drives demand for smaller, more flexible LNG carriers, opening up new niche markets and trade routes. Furthermore, the increasing adoption of LNG as a marine fuel for other vessel types, known as LNG bunkering, creates a burgeoning demand for specialized bunkering vessels, thus diversifying the tanker fleet's revenue streams and applications.

Technological innovation also offers considerable opportunities, particularly in the realm of digitalization and green shipbuilding. Investment in advanced digital solutions, including AI-powered navigation, predictive analytics, and smart logistics, can enhance operational efficiency, reduce fuel consumption, and improve safety across the fleet. The global push for decarbonization within the maritime sector itself provides an impetus for developing and deploying zero-emission or near-zero-emission LNG carriers, such as those powered by ammonia or hydrogen, though these are still in early stages. Exploring new Arctic shipping routes, made more accessible by climate change, could also significantly reduce transit times between Asia and Europe, creating demand for ice-class LNG carriers and specialized polar operations.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Small-Scale LNG Market | +1.5% | Emerging markets, island nations, remote areas | 2025-2033 |

| LNG Bunkering Expansion for Marine Fuel | +1.3% | Major port hubs globally | 2025-2033 |

| Digitalization & Automation Adoption | +1.0% | Global | 2025-2033 |

| Development of New Trade Routes (e.g., Arctic) | +0.7% | Arctic region, Asia-Europe trade | 2030-2033 |

LNG Tanker Market Challenges Impact Analysis

The LNG tanker market faces several complex challenges that require strategic navigation. Compliance with evolving environmental regulations, particularly those aimed at reducing greenhouse gas emissions and methane slip, poses a significant hurdle. Meeting these increasingly stringent standards often requires substantial investment in new technologies, vessel retrofits, and operational changes, which can impact profitability and require continuous innovation from shipowners. The global supply chain for shipbuilding components and specialized equipment can also be prone to disruptions, influenced by geopolitical events, natural disasters, or pandemic-related factory closures, leading to delays in new vessel deliveries and increased costs.

Another critical challenge is the acute shortage of skilled maritime personnel, particularly engineers and officers experienced in operating highly complex LNG carriers. The specialized nature of these vessels demands extensive training and certification, and the aging workforce combined with limited new talent entering the field creates a talent gap that can affect operational safety and efficiency. Cybersecurity threats are also a growing concern; as vessels become more integrated with digital systems and remote operations, they become vulnerable to cyberattacks that could compromise navigation, cargo management, or even safety systems. Navigating these challenges effectively will be crucial for sustainable growth in the LNG tanker market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with Evolving Environmental Regulations | -1.0% | Global, IMO regulatory framework | 2025-2033 |

| Skilled Crew Shortages | -0.7% | Global | 2025-2033 |

| Supply Chain Disruptions for Shipbuilding | -0.6% | Asia Pacific (shipbuilding hubs), Global | 2025-2028 |

| Increasing Cybersecurity Risks | -0.4% | Global | 2025-2033 |

LNG Tanker Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the global LNG Tanker Market, providing a detailed analysis of market size, growth drivers, restraints, opportunities, and challenges. It offers a strategic outlook from 2025 to 2033, incorporating historical data from 2019 to 2023 for robust trend analysis. The report segments the market extensively by various vessel types, propulsion technologies, cargo capacities, and applications, providing granular insights into each sub-segment's performance and future potential. Furthermore, it includes a thorough regional analysis covering major geographies, identifying key growth pockets and strategic initiatives within each. The scope also extends to profiling leading industry players, offering an understanding of the competitive landscape and their strategic positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 14.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mitsui O.S.K. Lines Ltd., GasLog Ltd., Dynagas LNG Partners LP, Teekay LNG Partners L.P., BW Group, Qatar Gas Transport Company Ltd. (Nakilat), Hoegh LNG, Nippon Yusen Kabushiki Kaisha (NYK Line), Kawasaki Kisen Kaisha Ltd. (K Line), Maran Gas Maritime Inc., TMS Cardiff Gas Ltd., Korea Line Corporation, Capital Gas Ship Management Corp., Exmar NV, China LNG Shipping (Holdings) Limited, Canship Ugland Ltd., Celsius Tankers, Angelicoussis Group (Maran Gas Maritime), Awilco LNG ASA, Flex LNG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LNG tanker market is comprehensively segmented to provide a detailed understanding of its diverse components and drivers. These segmentations allow for a granular analysis of market trends, identifying which vessel types, propulsion technologies, and capacities are gaining traction, and how different applications are contributing to overall market growth. Understanding these segments is crucial for stakeholders to pinpoint specific areas of investment, technological focus, and operational strategy, ensuring that fleet expansion and modernization align with evolving market demands and regulatory requirements across the global LNG value chain.

- By Vessel Type:

- Conventional LNG Tankers

- Q-Max LNG Tankers

- Q-Flex LNG Tankers

- Floating Storage and Regasification Units (FSRUs)

- Small-Scale LNG Carriers

- By Propulsion Type:

- Steam Turbine

- Dual Fuel Diesel-Electric (DFDE)

- Tri-Fuel Diesel-Electric (TFDE)

- X-DF / ME-GI

- Other Advanced Propulsion Systems (e.g., Ammonia-ready)

- By Cargo Capacity:

- Below 100,000 cbm

- 100,000-170,000 cbm

- 170,000-200,000 cbm (e.g., Q-Flex)

- Above 200,000 cbm (e.g., Q-Max)

- By Application:

- Inter-regional Trade

- Intra-regional Trade

- LNG Bunkering

- Floating Production, Storage, and Offloading (FPSO)

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to robust energy demand, expansion of regasification terminals in China, India, Japan, and South Korea, and significant shipbuilding capabilities. Increased intra-regional trade and growing reliance on LNG imports drive fleet growth.

- Europe: Witnessing a surge in LNG imports to diversify energy supplies, particularly after geopolitical shifts. Investments in new FSRUs and increased demand for efficient carriers characterize this region's market.

- North America: A major LNG exporter, particularly the United States, driving demand for long-haul LNG carriers. Ongoing expansion of liquefaction capacity continues to fuel new shipbuilding orders.

- Middle East & Africa (MEA): Key LNG exporting region (e.g., Qatar) with substantial existing and planned liquefaction capacity, leading to significant investment in large-capacity tankers for global distribution.

- Latin America: Growing interest in LNG for power generation and industrial use, leading to increased imports and development of small-scale LNG projects, driving demand for specialized vessels.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LNG Tanker Market.- Mitsui O.S.K. Lines Ltd.

- GasLog Ltd.

- Dynagas LNG Partners LP

- Teekay LNG Partners L.P.

- BW Group

- Qatar Gas Transport Company Ltd. (Nakilat)

- Hoegh LNG

- Nippon Yusen Kabushiki Kaisha (NYK Line)

- Kawasaki Kisen Kaisha Ltd. (K Line)

- Maran Gas Maritime Inc.

- TMS Cardiff Gas Ltd.

- Korea Line Corporation

- Capital Gas Ship Management Corp.

- Exmar NV

- China LNG Shipping (Holdings) Limited

- Canship Ugland Ltd.

- Celsius Tankers

- Angelicoussis Group (Maran Gas Maritime)

- Awilco LNG ASA

- Flex LNG

Frequently Asked Questions

What is the projected growth rate for the LNG Tanker Market?

The LNG Tanker Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing global demand for natural gas and expanding trade routes.

What are the primary drivers of growth in the LNG Tanker Market?

Key drivers include the global energy transition favoring cleaner natural gas, significant expansion of LNG liquefaction and regasification infrastructure, and the continuous need for fleet modernization with more efficient and environmentally compliant vessels.

How is AI impacting the LNG Tanker industry?

AI is transforming the industry through optimized vessel routing, predictive maintenance for reduced downtime, enhanced safety features, and improved supply chain efficiency, leading to more cost-effective and sustainable operations.

What are the main challenges facing the LNG Tanker Market?

Major challenges include high capital costs for new builds, compliance with stringent and evolving environmental regulations, geopolitical uncertainties affecting trade routes, and a global shortage of skilled maritime professionals.

Which regions are key contributors to the LNG Tanker Market?

Asia Pacific, Europe, and North America are leading regions due to strong import/export demands, expanding infrastructure, and strategic energy policies, while the Middle East and Africa also play a crucial role as major LNG exporters.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted