LPG Tanker Market

LPG Tanker Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705840 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

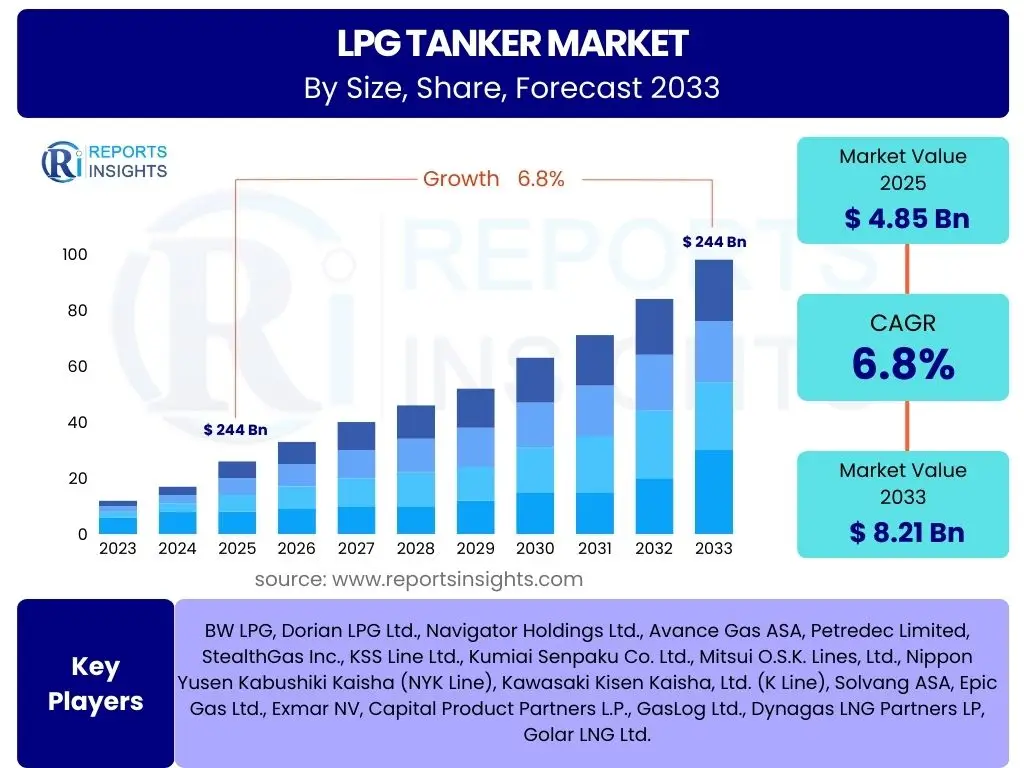

LPG Tanker Market Size

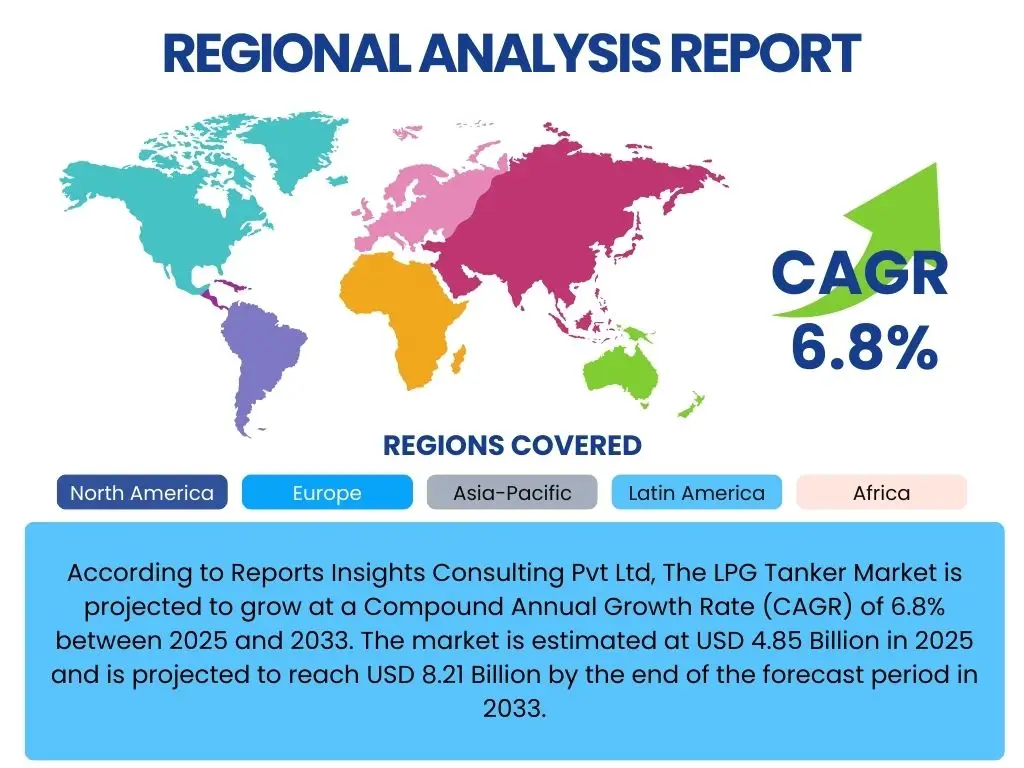

According to Reports Insights Consulting Pvt Ltd, The LPG Tanker Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.85 Billion in 2025 and is projected to reach USD 8.21 Billion by the end of the forecast period in 2033.

Key LPG Tanker Market Trends & Insights

The global LPG tanker market is witnessing transformative trends driven by evolving energy landscapes, stringent environmental regulations, and technological advancements. Users frequently inquire about how the industry is adapting to these shifts, particularly concerning fleet modernization, the adoption of cleaner fuels, and the impact of geopolitical dynamics on trade routes and supply chains. The market's trajectory is increasingly shaped by the imperative for sustainable shipping practices and the demand for efficient, reliable transportation of liquefied petroleum gas across diverse end-use sectors.

A significant trend involves the global push towards decarbonization, prompting shipowners to invest in newbuilds equipped with dual-fuel propulsion systems, including LPG as a marine fuel. This trend aligns with the International Maritime Organization's (IMO) emissions reduction targets, encouraging the retirement of older, less efficient vessels. Furthermore, the expansion of LPG production, especially from the United States and the Middle East, is reshaping trade flows, increasing demand for long-haul very large gas carriers (VLGCs) and influencing regional market dynamics.

- Accelerated fleet modernization with a focus on fuel efficiency and lower emissions.

- Rising adoption of dual-fuel (LPG and conventional) propulsion systems in newbuilds.

- Shifting global LPG trade routes driven by increased production in the US and Middle East.

- Growing demand for LPG as a cleaner marine fuel.

- Integration of advanced digital technologies for operational optimization and safety.

AI Impact Analysis on LPG Tanker

The integration of Artificial Intelligence (AI) across various facets of the LPG tanker industry is a topic of increasing interest, with common user questions revolving around its potential to enhance operational efficiency, safety, and predictive capabilities. AI's application extends from optimizing voyage planning and fuel consumption to facilitating advanced maintenance schedules and improving cargo management. Stakeholders are keen to understand how AI can mitigate risks associated with human error, enhance decision-making in complex maritime environments, and contribute to overall cost reduction.

AI technologies are poised to revolutionize vessel operations by enabling predictive analytics for equipment maintenance, thereby reducing downtime and extending asset lifespans. Machine learning algorithms can analyze vast datasets, including weather patterns, port congestion, and market prices, to recommend optimal routes and loading strategies. This not only minimizes fuel consumption but also ensures timely delivery and enhances supply chain resilience, addressing key concerns about operational reliability and economic viability in the competitive LPG shipping market.

- Predictive maintenance through AI algorithms to prevent equipment failures and reduce operational downtime.

- Optimized route planning and fuel consumption via AI-driven analytics, leading to cost savings and reduced emissions.

- Enhanced safety protocols and risk assessment capabilities through real-time data analysis and anomaly detection.

- Automated cargo management and monitoring systems for efficient loading, discharge, and temperature control.

- Improved fleet management and logistics through data-driven insights and forecasting for better resource allocation.

Key Takeaways LPG Tanker Market Size & Forecast

The LPG tanker market is positioned for substantial growth over the forecast period, reflecting an escalating global demand for LPG across diverse sectors and the ongoing evolution of international energy trade. Key takeaways frequently sought by users include the primary drivers of this growth, the anticipated trajectory of market expansion, and the factors that will most significantly influence its future landscape. The market's resilience and adaptive capacity to global economic shifts and regulatory pressures are central to understanding its long-term outlook.

The market's forecast indicates a robust expansion, largely propelled by the increasing utilization of LPG as a clean-burning fuel, particularly in emerging economies, and its indispensable role in the petrochemical industry. Furthermore, the strategic repositioning of major energy producers and the continued development of export infrastructure contribute significantly to the demand for efficient seaborne transportation. This sustained growth underscores the LPG tanker sector's critical role in global energy logistics and its appeal for strategic investments.

- The LPG tanker market is projected for significant growth, driven by rising global LPG consumption.

- Fleet modernization and the adoption of cleaner technologies are pivotal for market competitiveness.

- Strategic investments in newbuilds and infrastructure are essential to meet future demand.

- Geopolitical stability and trade policies will continue to influence market dynamics and trade routes.

LPG Tanker Market Drivers Analysis

The growth of the LPG tanker market is underpinned by several powerful drivers, primarily stemming from the increasing global demand for liquefied petroleum gas. This demand is multifaceted, originating from residential and commercial heating, industrial processes, chemical feedstock for the petrochemical industry, and increasingly, as an alternative marine fuel. The expanding production capacity, particularly in major exporting regions, necessitates robust transportation infrastructure, directly benefiting the LPG tanker sector.

Furthermore, evolving energy policies and environmental concerns are driving the shift towards cleaner fuels, positioning LPG as a viable alternative to traditional fossil fuels. This transition encourages investment in modern, more efficient, and environmentally compliant LPG tankers. The continuous development of LPG export terminals and import infrastructure globally also plays a crucial role in facilitating larger volumes of seaborne trade, thereby sustaining the demand for specialized transportation vessels.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global LPG Demand | +1.5% | Global | Long-term (2025-2033) |

| Expanding Petrochemical Industry | +0.8% | Asia Pacific | Mid-term (2025-2029) |

| US LPG Export Growth | +1.2% | North America, Asia | Long-term (2025-2033) |

| Fleet Modernization for Efficiency | +0.7% | Global | Mid-term (2025-2030) |

LPG Tanker Market Restraints Analysis

Despite its growth potential, the LPG tanker market faces several significant restraints that could impede its expansion. One primary concern is the inherent volatility of crude oil and LPG prices, which can directly impact trade volumes and freight rates. Sudden fluctuations in energy markets create uncertainty for operators and potential investors, making long-term planning challenging and affecting profitability margins.

Another critical restraint involves increasingly stringent environmental regulations, particularly those imposed by the International Maritime Organization (IMO) regarding sulfur emissions and greenhouse gases. While these regulations promote sustainability, compliance often requires substantial capital expenditure for retrofitting existing vessels or investing in new, more expensive, technologically advanced ships. Geopolitical instabilities and trade disputes can also disrupt established trade routes, leading to rerouting, increased transit times, and heightened operational costs, thereby acting as a significant impediment to market fluidity and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Instability and Trade Disputes | -0.9% | Global | Short-term (2025-2027) |

| Volatile Energy Prices | -0.7% | Global | Mid-term (2025-2029) |

| Stringent Environmental Regulations | -0.6% | Europe, Global | Long-term (2025-2033) |

| Oversupply of Vessels | -0.5% | Global | Short-term (2025-2026) |

LPG Tanker Market Opportunities Analysis

The LPG tanker market presents several promising opportunities for growth and innovation. A significant opportunity lies in the accelerating adoption of dual-fuel vessels capable of running on LPG, which offers a cleaner and often more cost-effective alternative to traditional bunker fuels. This trend is driven by both environmental mandates and economic incentives, positioning LPG as a pivotal transition fuel in the maritime sector and opening new avenues for vessel design and propulsion technology.

Furthermore, the expanding demand for LPG in emerging economies, particularly in Asia and Africa, for residential, commercial, and industrial applications, represents a substantial market opportunity. These regions are actively investing in LPG import infrastructure, creating new trade lanes and increasing the requirement for efficient transportation. The continuous advancements in shipping technologies, including digitalization and automation, also offer opportunities for operators to enhance operational efficiency, safety, and profitability, making the sector more attractive for investment and fostering sustainable development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Dual-Fuel Vessels | +1.0% | Global | Long-term (2026-2033) |

| Emerging Markets Demand Growth | +0.9% | Asia, Africa | Mid-term (2025-2030) |

| Development of LPG Infrastructure | +0.7% | Global | Long-term (2027-2033) |

| Green Shipping Initiatives | +0.6% | Europe, Global | Long-term (2028-2033) |

LPG Tanker Market Challenges Impact Analysis

The LPG tanker market faces a unique set of challenges that require proactive strategies from industry participants. One significant challenge is the substantial capital expenditure required for acquiring new, technologically advanced, and environmentally compliant vessels. This high upfront investment, coupled with volatile freight rates and market uncertainties, can pose financial hurdles, especially for smaller operators or those seeking to modernize their fleets.

Another critical challenge involves maintaining a skilled workforce and addressing potential crew shortages. Operating sophisticated LPG tankers demands highly trained personnel, and recruitment and retention in a globally competitive maritime labor market remain a persistent concern. Additionally, the increasing threat of cybersecurity breaches targeting maritime operational technology and IT systems presents a growing challenge, necessitating robust protective measures to safeguard sensitive data and ensure uninterrupted operations and safety on board. Supply chain disruptions, often triggered by geopolitical events, natural disasters, or pandemics, also continue to pose a challenge by impacting trade flows and vessel scheduling.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Newbuilds | -0.8% | Global | Long-term (2025-2033) |

| Cybersecurity Threats | -0.5% | Global | Ongoing |

| Crew Training and Retention | -0.4% | Global | Ongoing |

| Supply Chain Disruptions | -0.6% | Global | Short-term (2025-2026) |

LPG Tanker Market - Updated Report Scope

This report provides a comprehensive analysis of the global LPG Tanker Market, covering market size estimations, growth forecasts, and detailed segmentation. It examines the key drivers, restraints, opportunities, and challenges influencing market dynamics, along with an in-depth assessment of the competitive landscape. The scope includes an analysis of regional trends and the impact of emerging technologies, offering actionable insights for stakeholders in the maritime and energy sectors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.85 Billion |

| Market Forecast in 2033 | USD 8.21 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BW LPG, Dorian LPG Ltd., Navigator Holdings Ltd., Avance Gas ASA, Petredec Limited, StealthGas Inc., KSS Line Ltd., Kumiai Senpaku Co. Ltd., Mitsui O.S.K. Lines, Ltd., Nippon Yusen Kabushiki Kaisha (NYK Line), Kawasaki Kisen Kaisha, Ltd. (K Line), Solvang ASA, Epic Gas Ltd., Exmar NV, Capital Product Partners L.P., GasLog Ltd., Dynagas LNG Partners LP, Golar LNG Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LPG tanker market is comprehensively segmented to provide a granular view of its various components, enabling a deeper understanding of market dynamics and niche opportunities. This segmentation helps in identifying specific growth areas, competitive landscapes within sub-markets, and the distinct demands of different end-use sectors. Analyzing the market across these dimensions offers valuable insights into regional disparities, technological preferences, and the evolving needs of the global LPG supply chain.

Each segment, from vessel size categories to fleet ownership models and diverse end-use applications, contributes uniquely to the overall market structure. For instance, the demand for Very Large Gas Carriers (VLGCs) is closely tied to long-haul intercontinental trade, while smaller carriers cater to regional distribution. Understanding these distinctions is crucial for market participants to tailor their strategies, optimize fleet deployment, and capitalize on specific market trends. The detailed segmentation also aids in forecasting demand patterns and identifying potential areas for infrastructure development.

- By Vessel Size

- Very Large Gas Carriers (VLGCs)

- Large Gas Carriers (LGCs)

- Mid-size Gas Carriers (MGCs)

- Small Gas Carriers (SGCs)

- Handy Size Gas Carriers

- By Fleet Type

- Chartered

- Owned

- By End-Use

- Residential & Commercial

- Industrial

- Chemical

- Autogas

- Marine Fuel

Regional Highlights

The global LPG tanker market exhibits distinct regional dynamics, influenced by varying levels of LPG production, consumption patterns, regulatory frameworks, and infrastructural development. Asia Pacific stands out as a dominant region, driven by robust industrial growth, a large population demanding LPG for residential use, and significant petrochemical industry expansion, particularly in China, India, and Southeast Asian countries. The region's increasing reliance on LPG imports from major producing nations fuels the demand for a large and efficient tanker fleet, especially VLGCs for long-haul voyages.

North America, primarily the United States, plays a pivotal role as a major LPG exporter, leveraging its shale gas boom. This has profoundly reshaped global trade flows, creating new routes and increasing demand for specialized tankers to transport LPG to lucrative Asian and European markets. Europe, while a mature market, focuses on environmental compliance and fleet modernization, adopting cleaner technologies and exploring LPG as a marine fuel. The Middle East remains a crucial supply hub, with its vast reserves and export capabilities maintaining a steady demand for tanker services. Latin America and Africa represent emerging markets with growing LPG consumption, presenting future growth opportunities for the LPG tanker industry as their energy infrastructures develop.

- Asia Pacific: The largest and fastest-growing market, driven by high LPG consumption for residential, commercial, and industrial sectors, especially in China, India, and Southeast Asia. Significant demand for VLGCs due to increasing imports from the US and Middle East.

- North America: A key exporter, particularly the United States, whose shale gas revolution has transformed global LPG trade dynamics, leading to increased demand for large gas carriers for intercontinental shipments.

- Europe: Characterized by stringent environmental regulations driving fleet modernization and the adoption of greener propulsion technologies; a major importer of LPG for petrochemicals and heating, with a focus on sustainable shipping.

- Middle East: A primary source of LPG exports, with significant production capacities driving consistent demand for tanker services to Asian and European markets.

- Latin America & Africa: Emerging markets with growing LPG consumption, propelled by urbanization and expanding energy access initiatives, offering long-term growth potential for regional and international trade.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LPG Tanker Market.- BW LPG

- Dorian LPG Ltd.

- Navigator Holdings Ltd.

- Avance Gas ASA

- Petredec Limited

- StealthGas Inc.

- KSS Line Ltd.

- Kumiai Senpaku Co. Ltd.

- Mitsui O.S.K. Lines, Ltd.

- Nippon Yusen Kabushiki Kaisha (NYK Line)

- Kawasaki Kisen Kaisha, Ltd. (K Line)

- Solvang ASA

- Epic Gas Ltd.

- Exmar NV

- Capital Product Partners L.P.

- GasLog Ltd.

- Dynagas LNG Partners LP

- Golar LNG Ltd.

Frequently Asked Questions

What factors are driving the growth of the LPG tanker market?

The LPG tanker market's growth is primarily driven by increasing global demand for LPG across residential, industrial, and petrochemical sectors, expanding LPG production in key regions like the US and Middle East, and the growing adoption of LPG as a cleaner marine fuel.

How are environmental regulations impacting the LPG tanker industry?

Environmental regulations, particularly IMO 2020 and future decarbonization targets, are significantly impacting the industry by necessitating fleet modernization, investment in dual-fuel vessels (including LPG as fuel), and the implementation of emission reduction technologies to ensure compliance and promote sustainable shipping practices.

What role does technology, particularly AI, play in modern LPG tanker operations?

AI is increasingly vital in modern LPG tanker operations for predictive maintenance, optimizing voyage routes to enhance fuel efficiency, improving cargo management, and strengthening safety protocols through data analytics, leading to significant cost savings and operational improvements.

Which regions are key contributors to the global LPG tanker market?

Key contributors to the global LPG tanker market include Asia Pacific (driven by high demand and imports), North America (a major exporter), and the Middle East (a primary supply hub). Europe also plays a significant role with its focus on modernizing fleets and adhering to environmental standards.

What are the primary challenges faced by LPG tanker operators?

Primary challenges include high capital expenditure for new and compliant vessels, volatility in energy prices, geopolitical instability affecting trade routes, stringent environmental regulations requiring significant investments, and challenges related to crew training, retention, and cybersecurity threats.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted