Linear Image Sensor Market

Linear Image Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700739 | Last Updated : July 27, 2025 |

Format : ![]()

![]()

![]()

![]()

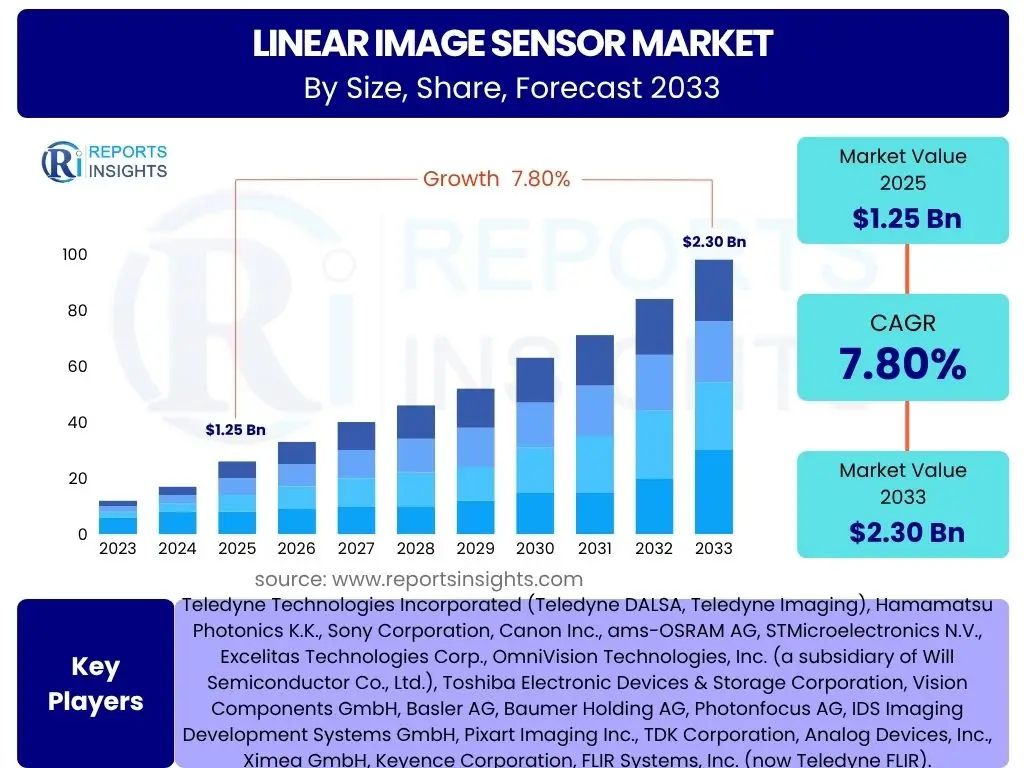

Linear Image Sensor Market Size

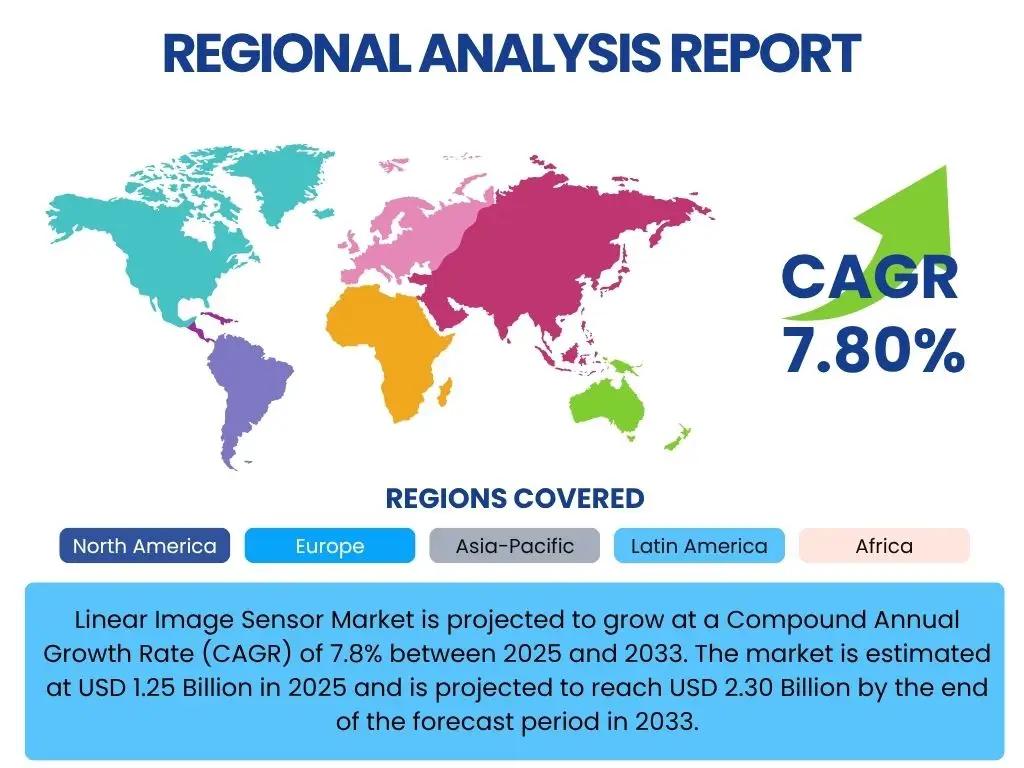

Linear Image Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.30 Billion by the end of the forecast period in 2033.

Key Linear Image Sensor Market Trends & Insights

User inquiries frequently highlight the accelerating pace of technological innovation and diversification of application areas within the linear image sensor market. There is significant interest in how these sensors are evolving beyond traditional industrial machine vision to permeate emerging sectors. Users are keen to understand the impact of miniaturization, increased resolution, and enhanced sensitivity on new product development and market expansion.

Another prominent theme in user questions revolves around the integration of linear image sensors with advanced processing capabilities, including edge AI, to enable real-time data analysis and decision-making at the point of capture. The demand for higher speed and precision in various industrial and medical applications is a consistent area of focus, driving research into faster data readout and more robust sensor designs. The market is also experiencing a shift towards more customized solutions, addressing niche requirements in specialized industries.

- Growing adoption of linear image sensors in industrial automation for high-speed inspection and quality control.

- Increasing demand for high-resolution sensors in medical imaging and scientific instrumentation.

- Advancements in CMOS technology leading to improved performance, lower power consumption, and cost-effectiveness.

- Expansion into new applications such as drone-based inspection, autonomous vehicles, and advanced security systems.

- Rising integration of intelligent features and embedded processing capabilities within sensor modules.

AI Impact Analysis on Linear Image Sensor

Common user questions regarding AI's impact on linear image sensors predominantly center on the enhancement of imaging capabilities and the creation of intelligent inspection systems. Users seek to understand how AI algorithms can improve defect detection accuracy, enable real-time classification, and optimize manufacturing processes through predictive analytics. There is a strong expectation that AI will unlock new levels of efficiency and automation, particularly in complex vision tasks that were previously challenging for traditional rule-based systems.

Furthermore, users are interested in the practical implementation of AI at the edge, where data is processed directly on the sensor or within the camera system, reducing latency and bandwidth requirements. Concerns often include the computational demands of AI, the need for extensive training data, and the integration complexities with existing industrial infrastructure. However, the overarching sentiment is one of anticipation for AI-driven advancements, particularly in applications requiring sophisticated pattern recognition, anomaly detection, and adaptive decision-making.

- AI enhances defect detection and classification accuracy in industrial inspection systems, reducing false positives and negatives.

- Integration of AI at the edge enables real-time processing and faster decision-making, crucial for high-speed manufacturing lines.

- Machine learning algorithms optimize sensor performance by adapting to varying lighting conditions and material properties.

- AI-powered linear image sensors facilitate predictive maintenance and process optimization through data analysis.

- New applications emerge in areas like advanced robotics, autonomous navigation, and sophisticated medical diagnostics, leveraging AI for richer data interpretation.

Key Takeaways Linear Image Sensor Market Size & Forecast

User inquiries frequently seek to distill the most critical insights from the linear image sensor market size and forecast, focusing on the primary growth catalysts and the overarching trajectory of the market. There is a clear interest in identifying which applications are driving the most significant revenue and where future investment opportunities lie. Users often aim to understand the long-term sustainability of growth, considering factors such as technological maturity and market saturation in specific segments.

Another key area of user focus pertains to the competitive landscape and the strategies employed by leading market players to maintain or gain market share. This includes questions about mergers and acquisitions, strategic partnerships, and product innovation pipelines. The discussions also touch upon the regional dynamics, with users keen to pinpoint which geographical areas are expected to exhibit the most robust growth and why, providing a comprehensive view of the market's evolving structure and future potential.

- The market's robust growth is primarily fueled by escalating demand in industrial automation and advanced medical imaging.

- CMOS technology continues to dominate, benefiting from ongoing advancements in resolution, speed, and cost-efficiency.

- Significant expansion opportunities exist in emerging applications such as electric vehicle battery inspection and advanced driver-assistance systems (ADAS).

- Asia Pacific is projected to remain the fastest-growing region, driven by rapid industrialization and manufacturing sector growth.

- Technological convergence, particularly with AI and IoT, is poised to create intelligent vision systems, broadening the market's scope.

Linear Image Sensor Market Drivers Analysis

The global linear image sensor market is experiencing significant growth propelled by several key drivers. A primary factor is the increasing adoption of industrial automation across various manufacturing sectors. Industries are rapidly integrating machine vision systems to enhance product quality, streamline production processes, and reduce operational costs, with linear image sensors being a critical component for high-speed and high-resolution inspection tasks. This trend is particularly evident in quality control, sorting, and dimension verification applications, where precision and speed are paramount.

Another substantial driver is the continuous advancement in medical imaging technologies. Linear image sensors are essential in advanced X-ray systems, dental imaging, and specialized medical diagnostics, where their ability to capture high-resolution images rapidly is invaluable. The growing healthcare expenditure, coupled with the demand for early and accurate disease detection, further fuels the adoption of these sensors in clinical and research settings. Furthermore, the expanding use of document scanning and postal automation, driven by the digitalization trend and the need for efficient data processing, also contributes significantly to market expansion.

The surge in demand for sophisticated security and surveillance systems, particularly those requiring high-performance line scan cameras for perimeter security and object detection, serves as an additional growth catalyst. As security concerns escalate globally, the need for reliable and high-resolution imaging solutions drives innovation and deployment of linear image sensors. Lastly, the ongoing technological improvements in CMOS sensor design, leading to better performance, lower power consumption, and reduced manufacturing costs, make linear image sensors more accessible and attractive for a wider range of applications, stimulating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation and Machine Vision Adoption | +2.1% | Global (APAC, North America, Europe) | Mid-to-Long Term (2025-2033) |

| Advancements in Medical Imaging Technologies | +1.7% | North America, Europe, Asia Pacific | Mid-to-Long Term (2025-2033) |

| Growing Demand for High-Resolution Document Scanning | +1.2% | North America, Europe, Asia Pacific | Short-to-Mid Term (2025-2029) |

| Technological Innovations in CMOS Sensor Design | +1.5% | Global | Ongoing (2025-2033) |

| Rising Need for Advanced Security and Surveillance Systems | +1.3% | Middle East & Africa, Asia Pacific | Mid-to-Long Term (2027-2033) |

Linear Image Sensor Market Restraints Analysis

Despite the promising growth trajectory, the linear image sensor market faces several restraints that could impede its full potential. One significant challenge is the high initial cost associated with implementing advanced linear image sensor systems. This includes not only the cost of the sensors themselves but also the associated specialized lighting, optics, and sophisticated software required for data processing and analysis. Such high upfront investment can deter small and medium-sized enterprises (SMEs) from adopting these technologies, particularly in cost-sensitive industries.

Another restraint stems from the technical complexities involved in integrating linear image sensors into existing industrial and medical setups. These sensors often require precise alignment, calibration, and environmental control (e.g., specific lighting conditions) to function optimally. The need for highly skilled personnel for installation, maintenance, and operation also adds to the operational challenges, limiting broader adoption in regions or industries with a shortage of such expertise.

Furthermore, the market's dependence on certain high-precision manufacturing processes means that supply chain disruptions, especially for critical components or specialized materials, can significantly impact production and lead times. Geopolitical tensions, trade policies, and unexpected global events (such as pandemics) can exacerbate these vulnerabilities, leading to increased costs and delayed market entry for new products. This inherent sensitivity to global supply chain stability poses a persistent risk to market growth and stability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Implementation | -1.5% | Global (SMEs, Emerging Economies) | Mid-to-Long Term (2025-2033) |

| Technical Complexity and Integration Challenges | -1.2% | Global (Industries with legacy systems) | Mid-to-Long Term (2025-2033) |

| Supply Chain Vulnerabilities and Component Shortages | -1.0% | Global (Asia Pacific, Europe) | Short-to-Mid Term (2025-2028) |

| Intense Competition from Area Scan Cameras in Certain Applications | -0.8% | Global | Ongoing (2025-2033) |

Linear Image Sensor Market Opportunities Analysis

The linear image sensor market is poised for significant opportunities driven by emerging technological advancements and expanding application horizons. One key opportunity lies in the burgeoning field of electric vehicle (EV) battery inspection. As the production of EV batteries scales up globally, there is an escalating need for precise, high-speed inspection systems to ensure quality and safety. Linear image sensors, with their ability to capture detailed line-by-line images of battery cells and modules, are ideally suited for this critical manufacturing step, offering substantial growth potential.

Another promising avenue for growth is the integration of linear image sensors into advanced driver-assistance systems (ADAS) and autonomous vehicles. While area scan sensors dominate current ADAS applications, linear sensors are finding niche roles in specific long-range detection, lidar systems, and high-resolution road surface analysis, contributing to enhanced safety and navigation capabilities. The continuous innovation in sensor fusion technologies further amplifies this opportunity, allowing linear sensors to complement other sensing modalities for more robust autonomous solutions.

Furthermore, the increasing adoption of Industry 4.0 principles and the widespread implementation of smart factories present immense opportunities. Linear image sensors are integral to these smart environments, enabling real-time process monitoring, predictive maintenance, and highly automated quality control. The demand for customized, application-specific linear image sensor solutions, coupled with the ongoing development of more compact, energy-efficient, and cost-effective sensors, will open up new markets and facilitate deeper penetration into existing ones, fostering sustained market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for EV Battery Inspection | +1.9% | Asia Pacific, Europe, North America | Mid-to-Long Term (2026-2033) |

| Integration in Advanced Driver-Assistance Systems (ADAS) and Autonomous Vehicles | +1.6% | North America, Europe, Asia Pacific | Long Term (2028-2033) |

| Expansion in Smart Factory and Industry 4.0 Applications | +1.5% | Global (Germany, Japan, USA, China) | Mid-to-Long Term (2025-2033) |

| Emergence of Hyperspectral and Multispectral Imaging | +1.1% | Global (Research & Specialized Industries) | Long Term (2029-2033) |

| Growth in High-Speed Food and Beverage Inspection | +0.9% | Europe, North America | Mid Term (2025-2030) |

Linear Image Sensor Market Challenges Impact Analysis

The linear image sensor market faces several intrinsic and extrinsic challenges that necessitate strategic responses from market participants. One significant challenge is the intense competition from alternative imaging technologies, particularly area scan cameras, which offer advantages in certain applications such as general-purpose machine vision and photography due to their ability to capture a full image in a single frame. While linear sensors excel in high-resolution, high-speed scanning of continuous objects, convincing users of their superior value proposition in specific use cases remains crucial amidst the broader adoption of area scan solutions.

Another key challenge involves the technical complexities and specialized expertise required for optimal integration and operation of linear image sensor systems. These systems demand precise lighting, advanced optics, and sophisticated software for image processing and analysis, which can be daunting for end-users without specialized knowledge. The need for highly trained personnel for installation, calibration, and ongoing maintenance adds to operational costs and can hinder widespread adoption, particularly in regions or industries with a shortage of technical skills.

Furthermore, rapid technological obsolescence poses a challenge, as continuous advancements in sensor design, resolution, and data processing capabilities mean that older sensor models can quickly become outdated. This necessitates significant research and development investment from manufacturers to remain competitive, while end-users face pressure to regularly upgrade their systems to leverage the latest efficiencies and capabilities. Navigating this fast-paced innovation cycle while ensuring cost-effectiveness and backward compatibility is a persistent hurdle for the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Area Scan Cameras | -1.0% | Global | Ongoing (2025-2033) |

| Need for Specialized Expertise and Integration Complexity | -0.9% | Global (Developing Economies) | Mid-to-Long Term (2025-2033) |

| High Development Costs for New Generation Sensors | -0.8% | Global (Manufacturers) | Ongoing (2025-2033) |

| Vulnerability to Economic Downturns Affecting Industrial Spending | -0.7% | Global | Short Term (Event-Dependent) |

Linear Image Sensor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Linear Image Sensor Market, segmenting it across various dimensions including technology type, resolution, application areas, and end-user industries. It offers a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges affecting market growth. The report also includes a thorough competitive landscape analysis, profiling key market players and their strategies, alongside regional market insights, to provide a holistic view of the industry from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.30 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Teledyne Technologies Incorporated (Teledyne DALSA, Teledyne Imaging), Hamamatsu Photonics K.K., Sony Corporation, Canon Inc., ams-OSRAM AG, STMicroelectronics N.V., Excelitas Technologies Corp., OmniVision Technologies, Inc. (a subsidiary of Will Semiconductor Co., Ltd.), Toshiba Electronic Devices & Storage Corporation, Vision Components GmbH, Basler AG, Baumer Holding AG, Photonfocus AG, IDS Imaging Development Systems GmbH, Pixart Imaging Inc., TDK Corporation, Analog Devices, Inc., Ximea GmbH, Keyence Corporation, FLIR Systems, Inc. (now Teledyne FLIR). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The linear image sensor market is meticulously segmented to provide a granular understanding of its diverse components and the unique dynamics within each. This segmentation allows for precise analysis of market trends, adoption patterns, and growth opportunities across different technological approaches, performance specifications, and end-use scenarios. By categorizing the market based on various parameters, stakeholders can identify high-growth niches, assess competitive landscapes, and formulate targeted strategies that align with specific market demands.

Understanding these segments is crucial for manufacturers to tailor their product offerings, for end-users to select the most appropriate sensor technology for their applications, and for investors to identify lucrative opportunities. The report's detailed segmentation illuminates the specific drivers and restraints impacting each category, offering a comprehensive view of the market's complexities. This layered analysis ensures that insights are actionable and highly relevant to the diverse stakeholders operating within or looking to enter the linear image sensor ecosystem.

- By Type:

- CMOS Linear Image Sensors

- CCD Linear Image Sensors

- By Resolution:

- Low Resolution (up to 2K pixels)

- Medium Resolution (2K-8K pixels)

- High Resolution (above 8K pixels)

- By Application:

- Industrial Automation

- Machine Vision

- Quality Control & Inspection

- Material Sorting

- Print Inspection

- Surface Inspection

- Medical Imaging

- X-ray Imaging

- Endoscopy

- Ophthalmic Imaging

- Document Scanning

- High-speed Scanners

- Archival Scanners

- Security & Surveillance

- Perimeter Security

- Object Detection

- Automotive

- ADAS (Advanced Driver-Assistance Systems)

- Lidar

- In-cabin Monitoring

- Consumer Electronics

- Printers

- Scanners

- Barcode Readers

- Scientific & Research

- Industrial Automation

- By End-User Industry:

- Manufacturing

- Healthcare

- Logistics & Retail

- Automotive

- Defense & Aerospace

- Agriculture

- Others (e.g., Textiles, Food & Beverage)

Regional Highlights

The global linear image sensor market exhibits distinct regional dynamics, influenced by varying levels of industrialization, technological adoption, and investment in key end-user sectors. North America and Europe represent mature markets with strong innovation ecosystems, robust manufacturing bases, and significant adoption of automation in industries such as automotive, aerospace, and healthcare. These regions are characterized by a high demand for high-performance, precision linear image sensors for advanced machine vision and medical imaging applications. Investments in Industry 4.0 initiatives and smart factory concepts continue to drive growth, albeit at a relatively steadier pace compared to emerging economies. The presence of key market players and a strong emphasis on R&D contribute to sustained market development.

Asia Pacific (APAC) stands out as the fastest-growing region in the linear image sensor market, primarily driven by rapid industrialization, burgeoning manufacturing sectors, and increasing government initiatives supporting automation and digitalization across countries like China, Japan, South Korea, and India. The region is a global manufacturing hub, leading to high demand for quality control and inspection systems in diverse industries, including electronics, textiles, and automotive. Furthermore, the expanding healthcare infrastructure and rising disposable incomes contribute to the growth of medical imaging applications, solidifying APAC's dominant position in the market. The competitive landscape in this region is also intensifying, with both global and local players vying for market share.

Latin America, the Middle East, and Africa (MEA) are emerging markets for linear image sensors, albeit at an earlier stage of adoption. Growth in these regions is spurred by increasing investments in infrastructure development, industrial diversification, and the nascent adoption of automation technologies. While currently contributing a smaller share to the global market, these regions offer long-term growth potential as their industrial sectors mature and economic development accelerates. Specific opportunities exist in sectors such as oil and gas inspection, mining, and basic manufacturing processes, where the implementation of vision systems is gaining traction to improve efficiency and safety.

- North America: A mature market characterized by high adoption in advanced manufacturing, medical imaging, and defense. Strong R&D investments and a focus on high-precision applications drive demand.

- Europe: A leading region for industrial automation, automotive manufacturing, and scientific research. Strict quality control standards and Industry 4.0 initiatives bolster market growth. Germany and the UK are key contributors.

- Asia Pacific (APAC): The fastest-growing market, propelled by rapid industrialization, large-scale manufacturing operations (especially in China and South Korea), and increasing investments in factory automation and medical facilities. Japan remains a technological powerhouse.

- Latin America: An emerging market with growing industrial sectors, particularly in Brazil and Mexico. Adoption is increasing with a focus on cost-effective automation solutions and agricultural applications.

- Middle East and Africa (MEA): Nascent market with potential driven by diversification efforts from oil-dependent economies into manufacturing, infrastructure development, and security applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Linear Image Sensor Market.- Teledyne Technologies Incorporated

- Hamamatsu Photonics K.K.

- Sony Corporation

- Canon Inc.

- ams-OSRAM AG

- STMicroelectronics N.V.

- Excelitas Technologies Corp.

- OmniVision Technologies, Inc.

- Toshiba Electronic Devices & Storage Corporation

- Vision Components GmbH

- Basler AG

- Baumer Holding AG

- Photonfocus AG

- IDS Imaging Development Systems GmbH

- Pixart Imaging Inc.

- TDK Corporation

- Analog Devices, Inc.

- Ximea GmbH

- Keyence Corporation

- FLIR Systems, Inc.

Frequently Asked Questions

What is a linear image sensor?

A linear image sensor is a specialized electronic device that captures images one line at a time, making it ideal for scanning continuous objects at high speed. Unlike area scan sensors that capture a full frame, linear sensors are composed of a single row of pixels, widely used in applications requiring high resolution and precise dimensional measurements, such as industrial inspection and document scanning.

How does a linear image sensor differ from an area scan sensor?

Linear image sensors capture images as a single line of pixels, requiring relative motion between the sensor and the object to build a complete two-dimensional image. Area scan sensors, conversely, capture an entire two-dimensional area simultaneously. Linear sensors excel in high-resolution, high-speed, continuous scanning, while area scan sensors are preferred for static object capture and general-purpose machine vision.

What are the primary applications of linear image sensors?

Linear image sensors are predominantly used in industrial automation for quality control, surface inspection, and material sorting. Other significant applications include high-resolution medical imaging (e.g., X-ray), document scanning, postal automation, and specialized security systems. Their capability for precise, high-speed line scanning makes them indispensable in these fields.

What technological trends are impacting the linear image sensor market?

Key trends include advancements in CMOS technology, leading to higher resolution, faster readout speeds, and improved low-light performance. Integration with Artificial Intelligence (AI) for enhanced image processing and defect detection, alongside miniaturization and increased customization for niche applications, are also significant technological drivers shaping the market.

What is the growth outlook for the linear image sensor market?

The linear image sensor market is projected for substantial growth, driven by increasing industrial automation, advancements in medical imaging, and the expansion into new applications like EV battery inspection. With a projected Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, the market is set to reach USD 2.30 Billion by 2033, indicating robust demand for precision imaging solutions globally.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted