PID Sensor and Detector Market

PID Sensor and Detector Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703058 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

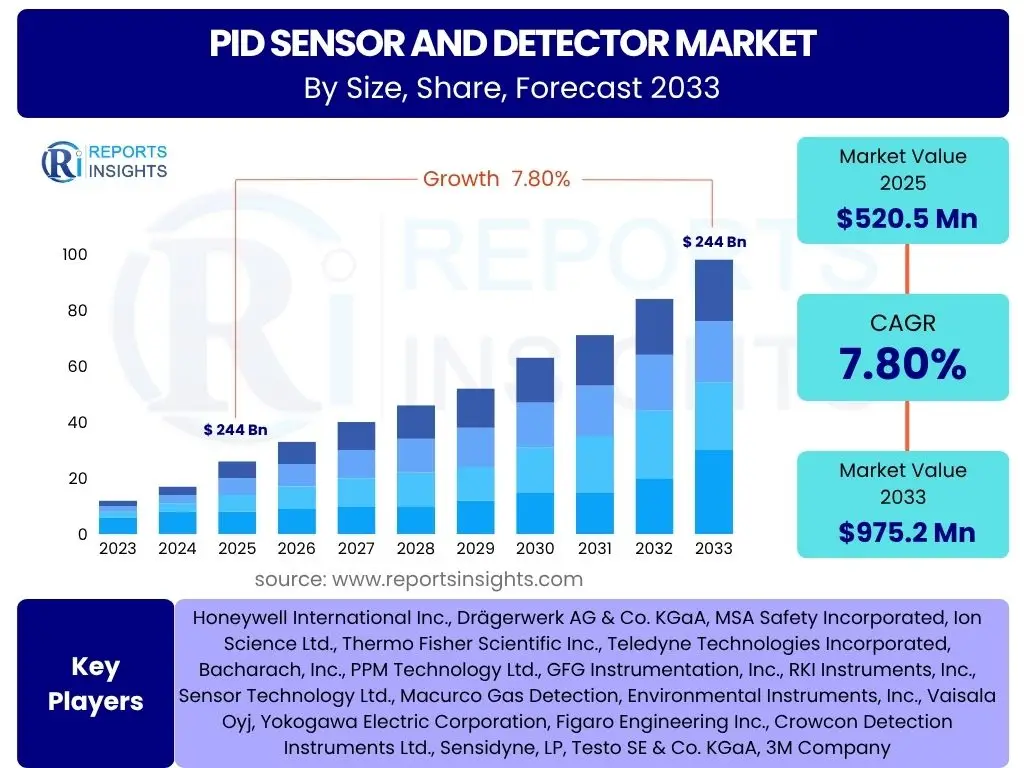

PID Sensor and Detector Market Size

According to Reports Insights Consulting Pvt Ltd, The PID Sensor and Detector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 520.5 Million in 2025 and is projected to reach USD 975.2 Million by the end of the forecast period in 2033.

Key PID Sensor and Detector Market Trends & Insights

The PID Sensor and Detector market is undergoing significant transformation, driven by evolving technological capabilities and increasing awareness of volatile organic compounds (VOCs) and their health impacts. Key trends indicate a shift towards more sophisticated, user-friendly, and interconnected detection solutions. The market is increasingly focused on enhancing sensor sensitivity and selectivity, enabling more precise identification and quantification of specific VOCs even in complex gas mixtures, which is crucial for applications demanding high accuracy, such as environmental compliance and pharmaceutical manufacturing.

Another prominent trend is the integration of PID sensors with broader digital ecosystems, including the Internet of Things (IoT) and Industry 4.0 platforms. This integration facilitates real-time data monitoring, remote access, and predictive maintenance capabilities, moving beyond traditional localized alerts to comprehensive, networked safety and environmental management systems. Such connectivity enhances operational efficiency and safety protocols across various industries, providing immediate insights and enabling proactive hazard mitigation. Furthermore, the push for miniaturization and portability continues, making PID technology more accessible for personal monitoring and rapid deployment in field applications.

- Miniaturization and portability are enhancing the versatility and personal safety applications of PID sensors.

- Increased integration with IoT, cloud platforms, and Industry 4.0 systems enables real-time data analysis and remote monitoring.

- Growing demand for highly sensitive and selective sensors to detect a broader range of VOCs at lower concentrations.

- Expansion of PID technology into new applications such as indoor air quality monitoring, healthcare diagnostics, and smart city initiatives.

- Development of AI and machine learning algorithms for improved data interpretation, false alarm reduction, and predictive maintenance.

AI Impact Analysis on PID Sensor and Detector

Artificial intelligence (AI) is poised to revolutionize the PID Sensor and Detector market by enhancing the accuracy, efficiency, and intelligence of gas detection systems. Users are keenly interested in how AI can minimize false positives and negatives, a long-standing challenge in VOC detection, by analyzing complex sensor data patterns and distinguishing target VOCs from interfering substances. AI algorithms can process vast amounts of data from PID sensors, identifying subtle trends and anomalies that human operators might miss, leading to more reliable and timely hazard alerts. This predictive capability is particularly valuable in dynamic environments where gas compositions can vary significantly.

The integration of AI also promises to transform maintenance and operational aspects of PID sensors. Users anticipate AI-driven predictive maintenance capabilities that can forecast sensor degradation, calibration needs, or component failures, thereby reducing downtime and optimizing operational costs. Furthermore, AI can facilitate autonomous monitoring and decision-making in hazardous environments, reducing human exposure to risks. This includes dynamic adjustment of sensor parameters for optimal performance, adaptive sampling strategies, and intelligent reporting that prioritizes critical information. The ability of AI to learn from historical data and adapt to new environmental conditions ensures that PID detection systems become more robust and responsive over time, addressing key user concerns regarding system reliability and operational longevity.

- AI enhances data interpretation and accuracy, reducing false alarms by identifying complex VOC signatures.

- Predictive maintenance driven by AI optimizes sensor lifespan and ensures timely calibration, minimizing operational downtime.

- Autonomous monitoring and adaptive sampling strategies improve efficiency and safety in hazardous environments.

- Machine learning algorithms enable PID sensors to adapt to changing environmental conditions and improve detection performance over time.

- Integration of AI facilitates seamless communication and actionable insights within broader industrial safety and environmental management systems.

Key Takeaways PID Sensor and Detector Market Size & Forecast

The PID Sensor and Detector market is on a robust growth trajectory, primarily driven by stringent global environmental regulations and an escalating focus on industrial safety. A significant takeaway is the increasing recognition across diverse industries of the critical need for continuous and accurate monitoring of volatile organic compounds (VOCs) to protect human health and ensure regulatory compliance. This heightened awareness, coupled with technological advancements, is fueling widespread adoption of PID solutions. The market forecast indicates sustained expansion, positioning PID technology as an indispensable tool for proactive hazard management and environmental stewardship.

Another crucial insight is the emergence of new application areas beyond traditional industrial safety, particularly in indoor air quality monitoring, healthcare diagnostics, and smart infrastructure. These emerging segments offer substantial growth opportunities, diversifying the market and driving innovation in sensor design and integration. The market's growth will also be significantly influenced by ongoing research and development aimed at improving sensor sensitivity, reducing costs, and enhancing connectivity features, ensuring PID sensors remain competitive and relevant in an evolving technological landscape. Businesses investing in this market should focus on developing versatile, cost-effective, and smart solutions to capture these expanding opportunities.

- The market is poised for significant growth, driven by escalating industrial safety standards and environmental regulations worldwide.

- Increased awareness of VOC health hazards is a primary catalyst for market expansion across multiple sectors.

- Technological advancements, including miniaturization and IoT integration, are enhancing the capabilities and applications of PID sensors.

- Emerging opportunities in indoor air quality, public health, and smart infrastructure are diversifying market revenue streams.

- Strategic focus on developing highly accurate, reliable, and cost-effective PID solutions will be crucial for market leadership.

PID Sensor and Detector Market Drivers Analysis

The market for PID sensors and detectors is primarily propelled by a global increase in industrial safety regulations and environmental protection mandates. Governments and regulatory bodies worldwide are imposing stricter limits on industrial emissions and workplace exposure to hazardous chemicals, particularly Volatile Organic Compounds (VOCs). This regulatory pressure compels industries such as oil and gas, chemical manufacturing, pharmaceuticals, and environmental agencies to implement advanced detection systems, making PID sensors a preferred choice due to their high sensitivity and rapid response times for a wide range of organic compounds. The persistent threat of industrial accidents and the need for continuous monitoring to prevent explosions, leaks, and toxic exposures further reinforce the demand for reliable PID technology.

Beyond regulatory compliance, the market is also significantly driven by growing awareness among industries and the public regarding the adverse health effects of VOC exposure, including respiratory issues, neurological damage, and carcinogenic risks. This heightened health consciousness is expanding the application scope of PID sensors beyond traditional industrial settings to areas like indoor air quality monitoring in commercial buildings, residential spaces, and healthcare facilities. Furthermore, ongoing technological advancements, such as improved sensor sensitivity, enhanced battery life for portable units, and integration with wireless communication and IoT platforms, are making PID solutions more efficient, user-friendly, and accessible, thereby accelerating their adoption across various sectors. The shift towards proactive safety measures and predictive maintenance strategies also contributes to this demand, as companies seek to prevent incidents rather than merely react to them.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental & Safety Regulations | +2.5% | North America, Europe, APAC | Short to Mid-term (2025-2030) |

| Growing Awareness of VOC Hazards | +1.8% | Global | Mid to Long-term (2027-2033) |

| Advancements in Sensor Technology & Miniaturization | +1.5% | Global | Continuous |

| Demand from Oil & Gas and Chemical Industries | +1.2% | MEA, North America, APAC | Short to Mid-term (2025-2030) |

| Integration with IoT & Industry 4.0 | +1.0% | Europe, North America | Mid to Long-term (2027-2033) |

| Rise in Indoor Air Quality Monitoring | +0.8% | North America, Europe, APAC | Mid to Long-term (2027-2033) |

PID Sensor and Detector Market Restraints Analysis

Despite significant growth drivers, the PID Sensor and Detector market faces several notable restraints that could temper its expansion. One primary concern is the relatively high initial cost associated with advanced PID sensors and detector systems. This elevated capital expenditure can be a barrier for small and medium-sized enterprises (SMEs) or organizations in developing regions with limited budgets, leading them to opt for less expensive, albeit potentially less accurate or versatile, alternative gas detection technologies. Furthermore, the cost implications extend beyond initial purchase to include ongoing maintenance, regular calibration requirements, and the periodic replacement of consumable components such as UV lamps and sensor electrodes, which adds to the total cost of ownership and may deter potential adopters.

Another significant restraint involves the technical complexities and calibration challenges inherent in PID technology. While highly sensitive, PID sensors require frequent and precise calibration to maintain their accuracy and reliability, especially when exposed to varying environmental conditions or different types of VOCs. This necessity for specialized calibration gases and trained personnel can be cumbersome and costly for end-users, potentially leading to incorrect readings if not performed diligently. Additionally, PID sensors can sometimes suffer from interferences from other gases like methane or humidity, which can lead to false readings or reduced accuracy, particularly in complex industrial environments. This challenge requires sophisticated algorithms or pre-filters, adding to the system's complexity and potentially limiting its widespread adoption in certain challenging applications. Moreover, fierce competition from alternative detection technologies, such as catalytic bead sensors, infrared sensors, and electrochemical sensors, which might be more cost-effective for specific applications, also poses a significant restraint on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost and Maintenance Expenses | -1.5% | Global, particularly Developing Regions | Short to Mid-term (2025-2030) |

| Technical Complexities and Calibration Requirements | -1.0% | Global | Continuous |

| Interference from Other Gases and Humidity | -0.8% | Specific Industrial Environments | Continuous |

| Competition from Alternative Detection Technologies | -0.7% | Global | Mid-term (2027-2030) |

| Lack of Awareness in Developing Regions | -0.5% | Latin America, MEA, Parts of APAC | Long-term (2030-2033) |

PID Sensor and Detector Market Opportunities Analysis

The PID Sensor and Detector market is ripe with numerous opportunities for growth and innovation. One significant area of opportunity lies in the continuous advancement of sensor technology, particularly in developing more robust, miniature, and highly selective PID sensors. As the push for smaller, more efficient devices intensifies, companies that can deliver compact, long-lasting, and highly sensitive portable PID detectors will find increasing demand, especially for personal safety monitoring and rapid environmental assessments. This miniaturization also facilitates integration into wearable devices and drones, expanding the scope of applications significantly beyond traditional fixed installations.

Another major opportunity stems from the burgeoning demand for indoor air quality (IAQ) monitoring solutions. With growing public awareness about the health impacts of indoor pollutants and an increasing emphasis on creating healthy living and working environments, PID sensors are ideally positioned to detect VOCs in homes, offices, schools, and healthcare facilities. This segment offers a largely untapped market, driving the need for user-friendly, cost-effective, and aesthetically integrated PID solutions. Furthermore, the expansion of smart city initiatives and the widespread adoption of the Internet of Things (IoT) provide a vast landscape for networked PID sensor deployments, enabling real-time, large-scale environmental monitoring and predictive analytics across urban landscapes. The development of lower-cost, high-performance PID solutions for emerging markets and the expansion into niche applications such as automotive cabin air quality and specialized medical diagnostics also represent significant avenues for future market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Indoor Air Quality (IAQ) Monitoring | +2.0% | North America, Europe, APAC | Mid to Long-term (2027-2033) |

| Integration with IoT, AI, and Smart City Initiatives | +1.8% | Global | Mid to Long-term (2027-2033) |

| Miniaturization and Development of Wearable Sensors | +1.5% | Global | Continuous |

| Growth in Emerging Markets (APAC, Latin America, MEA) | +1.3% | APAC, Latin America, MEA | Long-term (2030-2033) |

| Development of Cost-Effective and User-Friendly Solutions | +1.0% | Global | Continuous |

| Niche Applications in Healthcare and Automotive | +0.8% | North America, Europe | Long-term (2030-2033) |

PID Sensor and Detector Market Challenges Impact Analysis

The PID Sensor and Detector market confronts several significant challenges that require innovative solutions to ensure sustained growth. A primary challenge lies in the inherent complexity of accurately detecting and quantifying a vast array of volatile organic compounds (VOCs) in diverse environmental conditions. PID sensors are non-specific detectors, meaning they respond to a broad range of organic compounds, which can make it difficult to identify specific hazardous substances without additional analytical tools. This lack of specificity can lead to ambiguity in readings, particularly in multi-compound environments, and poses a challenge for precise hazard assessment and regulatory compliance that often requires identification of specific chemicals.

Another significant hurdle is ensuring sensor stability and reliability over extended periods, especially in harsh industrial environments characterized by extreme temperatures, humidity, dust, and corrosive gases. PID sensors are susceptible to drift and contamination of their UV lamps and electrodes, which can degrade performance and necessitate frequent maintenance and recalibration. This ongoing maintenance requirement and the potential for reduced accuracy in challenging conditions can increase operational costs and reduce user confidence. Furthermore, market fragmentation, with numerous small and large players offering a variety of PID solutions, presents challenges in terms of standardization, interoperability, and clear product differentiation. The rapid pace of technological change also demands continuous investment in research and development to keep pace with evolving regulatory requirements and competitive landscapes, posing a financial strain on manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sensor Specificity and Interference from Other Gases | -1.2% | Global | Continuous |

| Calibration, Maintenance, and Sensor Drift Issues | -1.0% | Global | Continuous |

| Performance Degradation in Harsh Environments | -0.9% | Industrial Zones (e.g., Oil & Gas, Chemicals) | Continuous |

| High Research and Development Costs | -0.7% | Global | Short to Mid-term (2025-2030) |

| Market Fragmentation and Intense Competition | -0.5% | Global | Continuous |

PID Sensor and Detector Market - Updated Report Scope

The updated report scope for the PID Sensor and Detector Market provides a comprehensive analysis of market dynamics, segmentation, and regional landscapes from 2019 to 2033. It offers crucial insights into market size, growth trends, and forecasts, identifying key drivers, restraints, opportunities, and challenges influencing the industry. The report also details the competitive environment, profiling leading market participants and their strategic initiatives.

This document is designed to assist stakeholders in understanding market potential, making informed business decisions, and identifying high-growth areas within the PID sensor and detector ecosystem. It covers both established and emerging application sectors, emphasizing technological advancements and their impact on market evolution. By presenting a holistic view, the report serves as an invaluable resource for manufacturers, suppliers, investors, and regulatory bodies navigating the complexities of VOC detection solutions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 520.5 Million |

| Market Forecast in 2033 | USD 975.2 Million |

| Growth Rate | 7.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., Drägerwerk AG & Co. KGaA, MSA Safety Incorporated, Ion Science Ltd., Thermo Fisher Scientific Inc., Teledyne Technologies Incorporated, Bacharach, Inc., PPM Technology Ltd., GFG Instrumentation, Inc., RKI Instruments, Inc., Sensor Technology Ltd., Macurco Gas Detection, Environmental Instruments, Inc., Vaisala Oyj, Yokogawa Electric Corporation, Figaro Engineering Inc., Crowcon Detection Instruments Ltd., Sensidyne, LP, Testo SE & Co. KGaA, 3M Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The PID Sensor and Detector market is comprehensively segmented to provide a detailed understanding of its diverse applications and product types, facilitating targeted analysis and strategic planning. This segmentation allows for a nuanced examination of how different sensor types cater to specific industrial needs and environmental challenges. By distinguishing between portable, fixed, and handheld detectors, the report highlights the varying demands across industrial safety, environmental monitoring, and personal protection applications, reflecting distinct user requirements for mobility, continuous operation, and ease of use.

Further segmentation by application and end-use industry illuminates the primary verticals driving market demand. Applications range from critical industrial safety in chemical plants and oil refineries to essential environmental monitoring for air quality and hazardous waste sites. The end-use industry segmentation provides insight into where PID technology is most critical, including oil & gas, chemicals, pharmaceuticals, and environmental agencies. This granular approach underscores the versatility of PID sensors and their indispensable role in ensuring compliance, worker safety, and environmental stewardship across a broad spectrum of economic activities. The detailed breakdown supports stakeholders in identifying growth pockets and tailoring product development to specific market needs.

- By Type

- Portable PID Sensors: Offers flexibility and ease of use for personal monitoring and rapid assessments in various field operations.

- Fixed PID Sensors: Designed for continuous, long-term monitoring in specific industrial locations or critical areas, often integrated into larger safety systems.

- Handheld PID Detectors: Provides immediate, on-the-spot readings for quick surveys, leak detection, and confined space entry checks.

- By Application

- Industrial Safety: Critical for protecting workers from toxic VOC exposures in manufacturing, chemical, and refining facilities.

- Environmental Monitoring: Used for air quality assessment, soil contamination detection, and compliance with environmental regulations.

- Homeland Security & Emergency Response: Deployed for rapid detection of hazardous materials during incidents or threats.

- Public Health & Indoor Air Quality: Monitors VOC levels in residential, commercial, and public buildings to ensure healthy indoor environments.

- Research & Development: Utilized in laboratories for experimental analysis of VOCs and gas phase reactions.

- Automotive: Employed for monitoring cabin air quality and emissions.

- Semiconductor Manufacturing: Essential for detecting trace VOCs that could impact product quality and worker safety.

- By End-Use Industry

- Oil & Gas: Vital for detecting flammable and toxic VOCs in exploration, production, and refining processes.

- Chemicals and Petrochemicals: Ensures safety from a wide range of hazardous organic compounds used in manufacturing.

- Pharmaceuticals and Healthcare: Monitors air quality in cleanrooms, laboratories, and patient environments.

- Food and Beverage: Detects VOCs that can indicate spoilage or contamination, and ensures compliance with hygiene standards.

- Manufacturing and Construction: Protects workers from solvent vapors, adhesives, and other VOCs released during processes.

- Environmental Agencies and Consultants: Uses PID sensors for site assessments, remediation monitoring, and regulatory enforcement.

- Mining: Detects hazardous gases in underground and surface mining operations.

- Government and Military: Utilizes PID technology for defense applications, hazmat response, and public safety.

Regional Highlights

- North America: This region is a dominant market for PID sensors and detectors, primarily driven by stringent occupational safety regulations, well-established industrial sectors such as oil & gas, chemical, and manufacturing, and a high level of environmental awareness. The presence of key market players and significant investments in research and development further bolster market growth. Demand is robust for both fixed and portable solutions, with increasing adoption in indoor air quality monitoring and homeland security applications.

- Europe: Europe represents a mature and highly regulated market, with strong emphasis on environmental protection and industrial hygiene standards. Countries like Germany, the UK, and France are leading in adopting advanced PID technologies due to strict EU directives concerning air quality and chemical exposure. Innovations in sensor technology and integration with smart factory initiatives are key drivers. The region also exhibits significant growth in the pharmaceutical and food & beverage sectors' demand for VOC monitoring.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, propelled by rapid industrialization, expanding manufacturing bases, and increasing environmental concerns in countries like China, India, Japan, and South Korea. While regulatory frameworks are still evolving in some areas, the growing awareness of pollution impacts and worker safety, coupled with government initiatives for environmental protection, is fueling substantial demand. Opportunities abound for cost-effective and rugged PID solutions suited for diverse industrial conditions.

- Latin America: This region is experiencing steady growth, largely driven by the expansion of the oil & gas and mining sectors, particularly in countries like Brazil and Mexico. Increasing foreign investments in industrial infrastructure and a gradual strengthening of environmental and safety regulations are contributing to the adoption of PID technology. The market is developing, with a growing need for both basic and advanced gas detection solutions to meet emerging safety standards.

- Middle East and Africa (MEA): The MEA market for PID sensors is primarily influenced by the extensive oil & gas industry in the Middle East and the growing industrial and infrastructure development across parts of Africa. Investments in petrochemical complexes and manufacturing facilities necessitate advanced safety equipment, including PID detectors. While awareness and regulatory enforcement vary, the region's resource-rich economy and large-scale industrial projects offer significant long-term growth potential for specialized VOC detection solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the PID Sensor and Detector Market.- Honeywell International Inc.

- Drägerwerk AG & Co. KGaA

- MSA Safety Incorporated

- Ion Science Ltd.

- Thermo Fisher Scientific Inc.

- Teledyne Technologies Incorporated

- Bacharach, Inc.

- PPM Technology Ltd.

- GFG Instrumentation, Inc.

- RKI Instruments, Inc.

- Sensor Technology Ltd.

- Macurco Gas Detection

- Environmental Instruments, Inc.

- Vaisala Oyj

- Yokogawa Electric Corporation

- Figaro Engineering Inc.

- Crowcon Detection Instruments Ltd.

- Sensidyne, LP

- Testo SE & Co. KGaA

- 3M Company

Frequently Asked Questions

What is a PID Sensor and how does it work?

A Photoionization Detector (PID) sensor is a highly sensitive gas detection device used to measure volatile organic compounds (VOCs) and other hazardous gases. It works by exposing gas molecules to high-energy ultraviolet (UV) light, which ionizes the molecules. The ionized particles then create a measurable electrical current proportional to the concentration of the gas, allowing for rapid and accurate detection of various compounds at low parts per billion (ppb) to parts per million (ppm) levels. PID sensors are non-destructive and offer a broad range of detection for compounds with ionization potentials lower than the UV lamp's energy.

What are the primary applications of PID Sensors?

PID sensors are widely utilized across numerous applications due to their versatility and sensitivity to VOCs. Key applications include industrial safety for protecting workers from hazardous chemical exposures in oil and gas, chemical, and manufacturing facilities; environmental monitoring for assessing air quality and detecting contamination in soil and water; homeland security and emergency response for identifying unknown substances during hazardous incidents; and indoor air quality (IAQ) monitoring in commercial and residential buildings to ensure healthy environments. They are also crucial in research and development for analytical studies of organic compounds.

What are the benefits of using PID Sensors for VOC detection?

PID sensors offer several significant benefits for detecting volatile organic compounds. Their high sensitivity allows for the detection of VOCs at very low concentrations, often in the parts per billion range, which is crucial for early warning of hazards. They provide a rapid response time, enabling immediate alerts to personnel in dangerous situations. PIDs are also non-destructive, meaning they do not consume or alter the gas sample, allowing for further analysis. Their broad range of detection covers a vast spectrum of organic compounds, making them a versatile tool for various industrial and environmental monitoring needs. Additionally, modern PID sensors are increasingly portable and user-friendly, enhancing their practicality for field applications.

How frequently should PID Sensors be calibrated?

The frequency of PID sensor calibration depends on several factors, including manufacturer recommendations, the sensor's usage intensity, and the environmental conditions it operates in. Generally, PID sensors require regular calibration to maintain accuracy and reliability. For critical industrial safety applications, daily bump tests and weekly or bi-weekly full calibrations are often recommended. For less frequent use or stable environments, monthly or quarterly calibrations might suffice. Exposure to high concentrations of target gases, extreme temperatures, high humidity, or dusty conditions can necessitate more frequent calibration. Following the manufacturer's guidelines and industry best practices is essential to ensure optimal performance and compliance with safety standards.

What are the key factors driving the growth of the PID Sensor market?

The PID Sensor market's growth is primarily driven by escalating global awareness and stringent regulations concerning occupational safety and environmental protection. Increasing regulatory pressure from government bodies to limit exposure to hazardous VOCs in industrial settings and to monitor ambient air quality compels industries to adopt advanced detection technologies. The growing understanding of the adverse health effects associated with VOC exposure further fuels demand. Additionally, technological advancements such as sensor miniaturization, enhanced sensitivity, and integration with IoT and AI platforms are expanding the applications and improving the efficiency of PID solutions, making them more appealing across diverse end-use industries worldwide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted