Bus Duct Market

Bus Duct Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703598 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Bus Duct Market Size

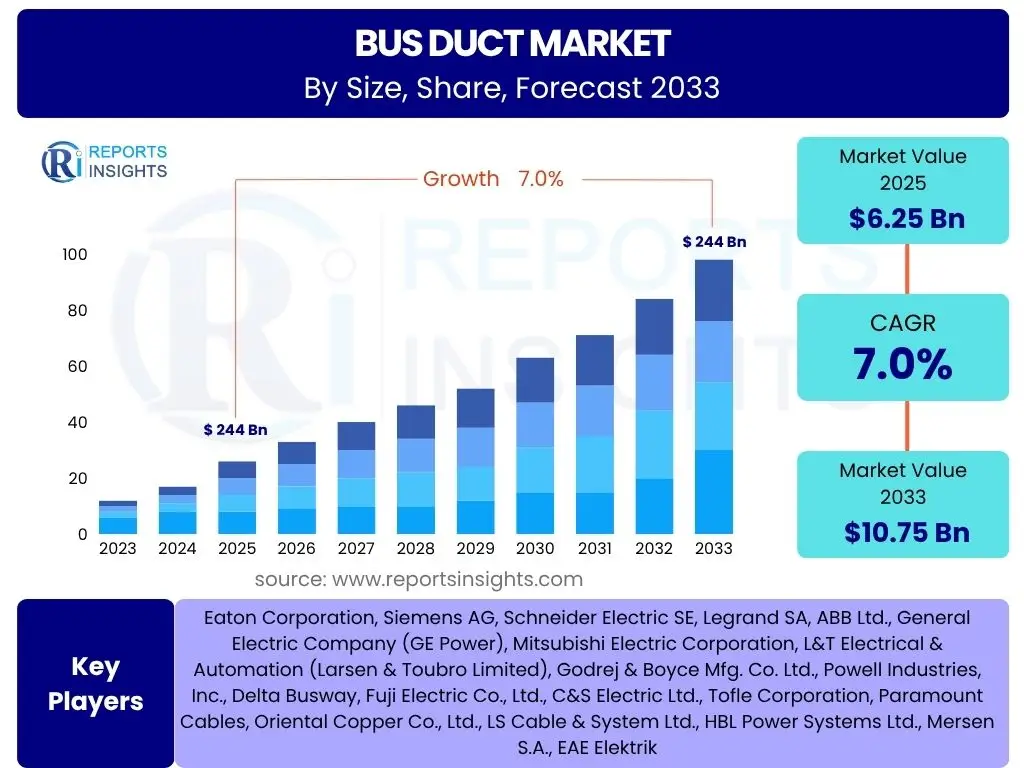

According to Reports Insights Consulting Pvt Ltd, The Bus Duct Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.0% between 2025 and 2033. The market is estimated at USD 6.25 Billion in 2025 and is projected to reach USD 10.75 Billion by the end of the forecast period in 2033.

Key Bus Duct Market Trends & Insights

The global Bus Duct market is experiencing a significant transformation, driven by an increasing emphasis on energy efficiency, space optimization, and enhanced safety in power distribution systems. Industry stakeholders are increasingly investing in modular and customizable bus duct solutions, which facilitate quicker installation and greater flexibility in diverse architectural and industrial settings. This trend is particularly pronounced in urban development projects and the expansion of data centers, where high power density and reliable distribution are paramount. Furthermore, the integration of smart technologies, such as sensors for real-time monitoring and predictive maintenance, is becoming a standard feature, offering enhanced operational efficiency and reducing downtime.

Another prominent trend involves the growing adoption of environmentally friendly materials and manufacturing processes in bus duct production. Companies are responding to stringent environmental regulations and consumer demand for sustainable solutions by developing products with lower carbon footprints and improved recyclability. This includes advancements in insulation materials and conductor technologies that not only improve performance but also align with global sustainability objectives. The market is also witnessing a shift towards higher voltage and current ratings to accommodate the increasing power demands of large-scale industrial complexes and critical infrastructure, thereby expanding the potential applications of bus duct systems beyond traditional uses.

- Emphasis on modular and customizable bus duct designs for flexibility and ease of installation.

- Integration of smart technologies for real-time monitoring and predictive maintenance.

- Development and adoption of eco-friendly materials and sustainable manufacturing processes.

- Increasing demand for higher voltage and current rated bus ducts in large-scale applications.

- Rising demand from data centers and renewable energy projects for efficient power distribution.

AI Impact Analysis on Bus Duct

Artificial intelligence (AI) is poised to significantly impact the Bus Duct market by revolutionizing various aspects from design and manufacturing to operational management and maintenance. AI-driven design tools can optimize bus duct configurations for efficiency, material usage, and thermal performance, leading to more compact and cost-effective solutions. In manufacturing, AI can enhance quality control through automated inspection systems and improve production line efficiency by optimizing resource allocation and predicting equipment failures. This leads to higher precision in fabrication and a reduction in waste, contributing to more sustainable production cycles.

For operational phases, AI facilitates advanced predictive maintenance capabilities for bus duct systems. By analyzing data from integrated sensors regarding temperature, current load, and vibrations, AI algorithms can accurately predict potential failures, allowing for proactive intervention before disruptions occur. This minimizes downtime, extends asset lifespan, and reduces operational costs for end-users. Furthermore, AI can contribute to smart grid integration by optimizing power flow through bus duct networks, enhancing overall energy efficiency and grid stability. The ability of AI to process vast amounts of data and identify patterns that are imperceptible to human analysis will transform how bus duct systems are designed, managed, and maintained throughout their lifecycle.

- AI-driven optimization in bus duct design for enhanced efficiency and material usage.

- Automated quality control and production optimization in manufacturing through AI.

- Predictive maintenance for bus duct systems using AI to prevent failures and minimize downtime.

- AI integration into smart grids for optimized power flow and improved energy efficiency.

- Enhanced thermal management and fault detection capabilities via AI algorithms.

Key Takeaways Bus Duct Market Size & Forecast

The Bus Duct market is on a robust growth trajectory, driven by global urbanization, industrial expansion, and the escalating demand for reliable and efficient power distribution solutions across diverse sectors. The projected compound annual growth rate indicates a strong market expansion, suggesting increasing investments in modern infrastructure, including commercial complexes, data centers, and manufacturing facilities, which critically depend on advanced power transmission systems. This growth highlights the market's resilience and its integral role in supporting the increasing electrical power requirements of a developing global economy. Stakeholders can anticipate sustained demand, particularly from regions undergoing rapid industrialization and urban development.

Furthermore, the market's evolution is characterized by a strong emphasis on technological innovation, with advancements aimed at improving energy efficiency, reducing installation complexity, and enhancing system safety. The shift towards compact, modular, and smart bus duct solutions reflects the industry's response to the need for flexible, high-performance power distribution in constrained spaces. This technological progression is not only expanding the applicability of bus ducts but also creating new market opportunities in sectors like renewable energy integration and electric vehicle charging infrastructure. The forecast underscores a positive outlook for manufacturers and service providers who can adapt to these evolving technological and environmental demands, emphasizing the importance of innovation and strategic partnerships for market leadership.

- The Bus Duct market is expected to experience significant growth, driven by global infrastructure development.

- Increasing demand for efficient and reliable power distribution is a primary market accelerator.

- Technological advancements, including smart and modular designs, are crucial for market expansion.

- Emerging applications in data centers, renewable energy, and smart cities offer substantial growth avenues.

- Market participants must prioritize innovation and sustainability to capitalize on future opportunities.

Bus Duct Market Drivers Analysis

The Bus Duct market is primarily driven by the escalating global demand for electricity, propelled by rapid urbanization and industrialization across developing economies. As cities expand and new manufacturing facilities are established, the need for efficient and safe power distribution systems becomes critical. Bus duct systems offer superior advantages over traditional cabling, such as higher current carrying capacity, reduced installation time, and lower space requirements, making them the preferred choice for modern infrastructure projects. This robust demand from the industrial and commercial sectors significantly contributes to market growth.

Moreover, the continuous development of smart grids and renewable energy infrastructure worldwide is acting as a substantial catalyst for the Bus Duct market. The integration of renewable energy sources like solar and wind power into national grids necessitates reliable and efficient power transfer solutions, for which bus ducts are ideally suited. Additionally, the increasing focus on energy efficiency and fire safety standards in building codes and industrial regulations is further pushing the adoption of bus duct systems, which inherently offer better thermal management and fire resistance properties compared to conventional cabling. This regulatory support coupled with technological advancements ensures sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Industrialization and Urbanization | +2.1% | Asia Pacific (China, India), Africa | Short to Medium Term (2025-2029) |

| Growth in Data Centers & IT Infrastructure | +1.8% | North America, Europe, APAC | Medium to Long Term (2026-2033) |

| Increasing Demand for Reliable Power Distribution | +1.5% | Global | Short to Long Term (2025-2033) |

| Integration of Renewable Energy Sources | +1.3% | Europe, North America, China | Medium to Long Term (2027-2033) |

| Adoption of Smart Grid Technologies | +1.1% | North America, Europe, Japan | Medium to Long Term (2027-2033) |

| Focus on Energy Efficiency and Safety Standards | +0.9% | Global, especially developed regions | Short to Medium Term (2025-2030) |

Bus Duct Market Restraints Analysis

Despite significant growth drivers, the Bus Duct market faces several restraints that could potentially impede its expansion. One primary concern is the relatively high initial capital expenditure associated with bus duct systems compared to traditional cable wiring solutions. While bus ducts offer long-term operational advantages and cost savings through efficiency and reduced maintenance, the upfront investment can be a deterrent for small to medium-sized enterprises or projects with limited budgets. This economic factor often influences procurement decisions, particularly in price-sensitive markets.

Another significant restraint is the technical complexity involved in the design, installation, and maintenance of bus duct systems, requiring specialized skills and labor. The availability of adequately trained professionals for these tasks can be a challenge in certain regions, leading to higher labor costs and potential project delays. Furthermore, the market faces competition from advanced cable technologies that continue to evolve, offering improved fire resistance, flexibility, and insulation properties, albeit often with lower current carrying capacities. Regulatory hurdles and the need for adherence to diverse international and regional standards also add to the complexity and cost for manufacturers operating on a global scale, requiring substantial investment in compliance and certification.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Installation Cost | -1.2% | Developing Regions (SEA, Africa), Small Projects | Short to Medium Term (2025-2029) |

| Competition from Traditional Cable Systems | -0.8% | Global, particularly in smaller applications | Short to Medium Term (2025-2028) |

| Lack of Standardized Regulations Across Regions | -0.6% | Global, Cross-Border Projects | Medium to Long Term (2026-2033) |

| Technical Skill Requirements for Installation & Maintenance | -0.5% | Emerging Markets, Labor-intensive projects | Short to Medium Term (2025-2030) |

Bus Duct Market Opportunities Analysis

The Bus Duct market is poised for significant growth through several emerging opportunities driven by global infrastructure development and technological advancements. One key area is the accelerating development of smart cities and intelligent building initiatives worldwide. These projects demand highly efficient, reliable, and space-saving power distribution systems that can integrate seamlessly with advanced automation and control technologies, making bus ducts an ideal choice. The increasing adoption of Building Management Systems (BMS) and Internet of Things (IoT) technologies within commercial and residential complexes further amplifies the need for sophisticated electrical infrastructure, presenting lucrative opportunities for bus duct manufacturers.

Another substantial opportunity lies in the burgeoning electric vehicle (EV) charging infrastructure and large-scale renewable energy projects. As nations transition towards sustainable energy sources and promote EV adoption, there is a burgeoning requirement for robust and high-capacity power distribution for EV charging stations and grid integration of renewable energy farms. Bus ducts offer the necessary current carrying capacity and modularity to support these large-scale power demands efficiently. Furthermore, the global trend of upgrading and modernizing aging electrical infrastructure in developed economies presents a significant replacement market for bus ducts, replacing outdated and less efficient cabling systems with superior solutions, thereby ensuring long-term market sustainability and growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Smart Cities and Intelligent Buildings | +1.7% | North America, Europe, APAC, Middle East | Medium to Long Term (2026-2033) |

| Expansion of EV Charging Infrastructure | +1.5% | Global, particularly Europe, China, North America | Medium to Long Term (2027-2033) |

| Modernization of Aging Electrical Infrastructure | +1.2% | North America, Europe, Japan | Short to Long Term (2025-2033) |

| Increased Adoption in Healthcare and Pharmaceutical Facilities | +0.9% | Global | Short to Medium Term (2025-2030) |

| Emergence of New Industrial Automation Projects | +0.8% | Asia Pacific (China), Europe, North America | Medium Term (2026-2031) |

Bus Duct Market Challenges Impact Analysis

The Bus Duct market faces several challenges that necessitate strategic responses from industry players to sustain growth. One significant challenge is the volatility in raw material prices, particularly for copper and aluminum, which are primary components of bus duct systems. Fluctuations in these commodity prices directly impact manufacturing costs and profitability, making it difficult for manufacturers to maintain stable pricing and profit margins. Geopolitical factors and supply chain disruptions can exacerbate this challenge, leading to unpredictable production costs and potential delays in project delivery, which can strain customer relationships and overall market stability.

Another critical challenge involves the complex and sometimes fragmented regulatory landscape across different countries and regions. Adherence to diverse local electrical codes, safety standards, and environmental regulations requires significant investment in product development, testing, and certification. This complexity can hinder market entry for new players and increase operational costs for existing ones, particularly for those looking to expand globally. Furthermore, the lack of widespread awareness and understanding of the long-term benefits of bus duct systems compared to conventional wiring, especially in developing markets, poses a marketing and educational challenge. Overcoming these hurdles will require innovative manufacturing processes, robust supply chain management, and comprehensive market education initiatives.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Copper, Aluminum) | -0.9% | Global | Short to Medium Term (2025-2029) |

| Lack of Standardization and Interoperability | -0.7% | Global, particularly cross-regional projects | Medium to Long Term (2026-2033) |

| Intense Competition and Price Pressure | -0.6% | Global, particularly in mature markets | Short to Medium Term (2025-2028) |

| Requirement for Specialized Installation Workforce | -0.5% | Developing Economies, Remote Areas | Short to Medium Term (2025-2030) |

| Limited Awareness in Specific End-User Segments | -0.4% | Emerging Markets | Short to Medium Term (2025-2029) |

Bus Duct Market - Updated Report Scope

This report provides a comprehensive analysis of the global Bus Duct market, offering in-depth insights into market size, growth trends, competitive landscape, and strategic recommendations for stakeholders. It encompasses detailed segmentation analysis by type, current rating, application, and end-user, alongside a thorough regional assessment to provide a holistic view of market dynamics and future growth prospects. The study meticulously examines market drivers, restraints, opportunities, and challenges influencing the industry, employing a robust methodology to forecast market performance through 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.25 Billion |

| Market Forecast in 2033 | USD 10.75 Billion |

| Growth Rate | 7.0% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Eaton Corporation, Siemens AG, Schneider Electric SE, Legrand SA, ABB Ltd., General Electric Company (GE Power), Mitsubishi Electric Corporation, L&T Electrical & Automation (Larsen & Toubro Limited), Godrej & Boyce Mfg. Co. Ltd., Powell Industries, Inc., Delta Busway, Fuji Electric Co., Ltd., C&S Electric Ltd., Tofle Corporation, Paramount Cables, Oriental Copper Co., Ltd., LS Cable & System Ltd., HBL Power Systems Ltd., Mersen S.A., EAE Elektrik |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Bus Duct market is comprehensively segmented based on various critical parameters to provide a granular understanding of its diverse applications and market dynamics. This segmentation facilitates a detailed analysis of market performance across different product types, current ratings, and end-user industries, offering insights into specific growth drivers and technological preferences within each category. Understanding these segments is crucial for market participants to tailor their strategies, identify niche opportunities, and develop products that cater to specific market demands.

The segmentation by type includes key categories such as Sandwich Bus Duct, known for its compact design and high current density; Air Insulated Bus Duct, often preferred for its cost-effectiveness and ease of maintenance; and specialized types like Plug-in, Lighting, Compact, and Resin Insulated Bus Duct, each serving distinct application requirements. Current rating segmentation, encompassing low, medium, and high current, reflects the varying power demands across different sectors, from residential buildings to heavy industrial plants. Further segmentation by application (Industrial, Commercial, Residential, Transportation) and end-user (Data Centers, Manufacturing Plants, Power Generation & Distribution, etc.) highlights the broad utility and expanding adoption of bus duct systems across critical infrastructure and emerging sectors.

- By Type:

- Sandwich Bus Duct

- Air Insulated Bus Duct

- Plug-in Bus Duct

- Lighting Bus Duct

- Compact Bus Duct

- Resin Insulated Bus Duct

- By Current Rating:

- Low Current

- Medium Current

- High Current

- By Application:

- Industrial

- Commercial

- Residential

- Transportation

- By End-User:

- Data Centers

- Manufacturing Plants

- Power Generation & Distribution

- Commercial Buildings

- Residential Complexes

- Transportation Infrastructure

- Renewable Energy (Solar, Wind Farms)

Regional Highlights

- North America: This region is characterized by significant investments in smart grid infrastructure modernization and the expansion of data centers, driving the demand for high-performance bus duct systems. The United States and Canada are leading the adoption of advanced bus duct technologies due to stringent safety regulations and a focus on energy efficiency in commercial and industrial sectors. The market here is mature but shows consistent growth due to infrastructure upgrades and technological advancements.

- Europe: Europe exhibits robust growth, primarily fueled by the strong emphasis on renewable energy integration and the development of sustainable building solutions. Countries like Germany, the UK, and France are heavily investing in upgrading their aging electrical infrastructure and adhering to ambitious decarbonization targets, which necessitate efficient and reliable power distribution systems like bus ducts. The region also benefits from the presence of key industry players and advanced manufacturing capabilities.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for bus ducts, driven by rapid industrialization, urbanization, and massive infrastructure development projects, particularly in China and India. The increasing establishment of manufacturing facilities, commercial hubs, and residential complexes, coupled with government initiatives for smart cities and rural electrification, significantly boosts market demand. Emerging economies in Southeast Asia are also contributing substantially to this growth.

- Latin America: The market in Latin America is witnessing steady growth, influenced by increasing foreign investments in industrial sectors, mining operations, and commercial construction activities. Brazil and Mexico are key contributors, with rising energy demands and a focus on modernizing their power distribution networks. While growth may be slower compared to APAC, the region presents long-term opportunities as infrastructure development continues.

- Middle East and Africa (MEA): The MEA region is experiencing substantial growth, primarily propelled by large-scale construction projects, including commercial buildings, hospitality sectors, and mega-cities like Neom in Saudi Arabia and various developments in the UAE. Significant investments in oil and gas infrastructure and diversification efforts towards non-oil sectors are creating considerable demand for robust power distribution systems. Rapid urbanization and increasing power consumption in African countries are also contributing to market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bus Duct Market.- Eaton Corporation

- Siemens AG

- Schneider Electric SE

- Legrand SA

- ABB Ltd.

- General Electric Company (GE Power)

- Mitsubishi Electric Corporation

- L&T Electrical & Automation (Larsen & Toubro Limited)

- Godrej & Boyce Mfg. Co. Ltd.

- Powell Industries, Inc.

- Delta Busway

- Fuji Electric Co., Ltd.

- C&S Electric Ltd.

- Tofle Corporation

- Paramount Cables

- Oriental Copper Co., Ltd.

- LS Cable & System Ltd.

- HBL Power Systems Ltd.

- Mersen S.A.

- EAE Elektrik

Frequently Asked Questions

What is a bus duct and how does it differ from traditional cabling?

A bus duct, also known as busway, is a system for distributing electrical power using metallic enclosures containing insulated conductors (typically copper or aluminum bars). It differs from traditional cabling by offering higher current carrying capacity, better heat dissipation, modularity, and easier installation in confined spaces, making it ideal for high-power distribution in industrial and commercial settings.

What are the primary applications of bus duct systems?

Bus duct systems are primarily used in industrial facilities, commercial buildings, data centers, power generation and distribution plants, and transportation infrastructure. They are crucial for efficient power distribution in high-rise buildings, manufacturing assembly lines, hospitals, and critical infrastructure requiring reliable and flexible power supply.

What are the key advantages of using bus ducts over conventional wiring?

Key advantages include superior electrical efficiency due to lower voltage drop and heat loss, enhanced safety with fire-resistant enclosures, significant space savings, easier and faster installation, increased flexibility for modifications and expansions, and reduced maintenance requirements, leading to lower total cost of ownership over time.

How does the integration of smart technologies impact bus duct efficiency?

The integration of smart technologies, such as IoT sensors and AI-driven monitoring systems, significantly enhances bus duct efficiency by providing real-time data on temperature, current load, and system health. This enables predictive maintenance, early fault detection, optimized power flow, and improved overall operational reliability, minimizing downtime and energy waste.

What regions are expected to drive the most growth in the Bus Duct market?

Asia Pacific (APAC) is projected to be the leading region for growth in the Bus Duct market, driven by rapid industrialization, urbanization, and significant infrastructure development in countries like China and India. North America and Europe also show substantial growth due to modernization of aging infrastructure and increasing investments in data centers and renewable energy projects.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted