Non Segregated Phase Bus Duct Market

Non Segregated Phase Bus Duct Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702035 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

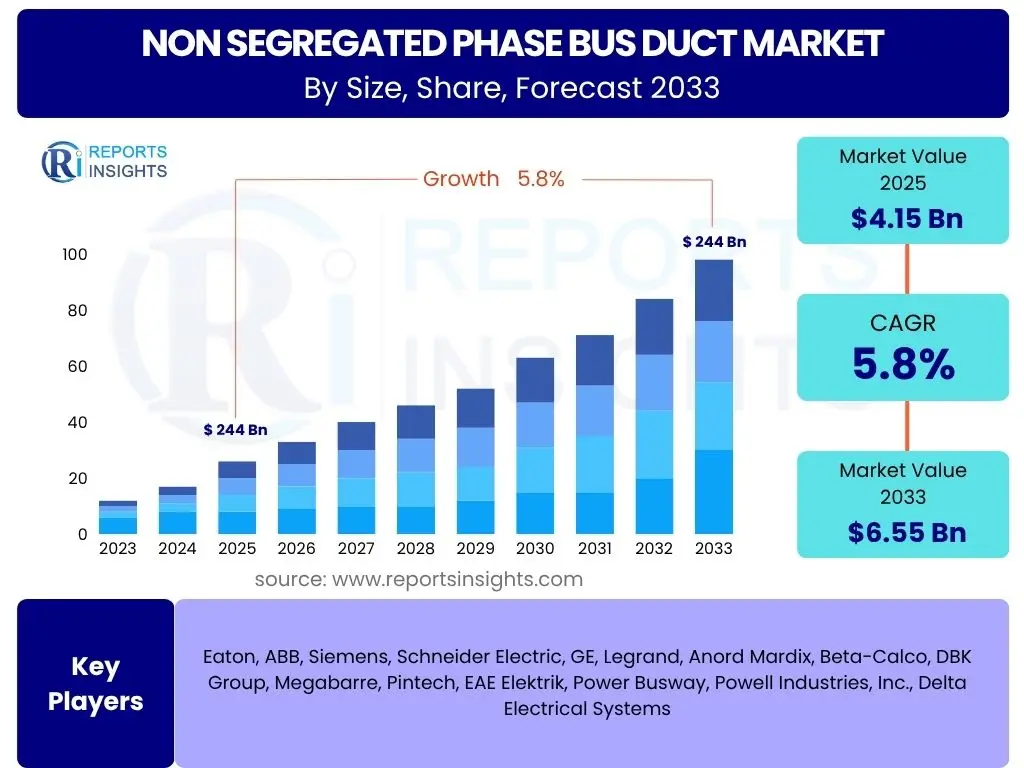

Non Segregated Phase Bus Duct Market Size

According to Reports Insights Consulting Pvt Ltd, The Non Segregated Phase Bus Duct Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 4.15 Billion in 2025 and is projected to reach USD 6.55 Billion by the end of the forecast period in 2033.

The growth trajectory for the Non Segregated Phase Bus Duct (NSPBD) market is underpinned by robust demand stemming from the global expansion of industrial infrastructure, power generation capacities, and modern data centers. NSPBDs, valued for their efficient power transmission capabilities and ease of installation, are becoming increasingly vital in large-scale electrical distribution systems. Their design allows for a compact footprint while ensuring high current carrying capacity, making them suitable for densely populated urban areas and industrial complexes where space optimization is critical.

Furthermore, the ongoing global transition towards renewable energy sources is significantly contributing to market expansion. As new solar farms, wind power plants, and hydroelectric facilities are commissioned, there is a corresponding surge in demand for reliable and efficient power evacuation solutions, which NSPBDs effectively provide. The need for stable and secure power distribution networks in these emerging power landscapes positions NSPBDs as indispensable components, driving their adoption across diverse geographical regions.

Key Non Segregated Phase Bus Duct Market Trends & Insights

Key market trends and insights within the Non Segregated Phase Bus Duct sector reveal a dynamic landscape driven by technological advancements, evolving regulatory frameworks, and increasing sustainability concerns. Stakeholders are keen to understand how current manufacturing processes are adapting, what new materials are being integrated, and how these innovations are improving performance and lifespan. The industry is witnessing a notable shift towards modular and pre-fabricated solutions, aiming to reduce installation time and labor costs on site, while simultaneously enhancing system reliability and operational efficiency. This modular approach also facilitates easier maintenance and upgrades, addressing long-term operational expenditures.

Furthermore, there is a growing emphasis on smart integration, leveraging digital technologies to enhance monitoring, diagnostics, and predictive maintenance capabilities. The incorporation of sensors and communication modules allows for real-time data collection on critical parameters such as temperature, current, and voltage, enabling operators to identify potential issues before they lead to costly downtime. This proactive maintenance strategy not only extends the operational life of the bus duct systems but also significantly improves safety standards and overall grid resilience. The drive for higher energy efficiency and reduced power losses is also a prominent trend, pushing manufacturers to innovate in conductor materials and insulation technologies.

Sustainability is another overarching theme, influencing design and material choices. There is an increasing demand for environmentally friendly materials, reduced waste during manufacturing, and designs that support end-of-life recycling. This aligns with broader corporate social responsibility initiatives and stricter environmental regulations globally, pushing the market towards more eco-conscious solutions. The long-term durability and minimal maintenance requirements of NSPBDs also contribute to their sustainable profile, offering a lower carbon footprint over their operational lifespan compared to traditional cabling solutions in specific applications.

- Increased adoption of modular and pre-fabricated Non Segregated Phase Bus Ducts for quicker installation and reduced on-site labor.

- Integration of smart monitoring systems and IoT sensors for real-time performance tracking, diagnostics, and predictive maintenance.

- Emphasis on enhanced safety features and improved insulation materials to minimize risks and extend operational lifespans.

- Development of Non Segregated Phase Bus Ducts with higher current carrying capacities and lower power losses for increased energy efficiency.

- Growing demand for customizable solutions tailored to specific project requirements in complex industrial and infrastructure developments.

- Focus on sustainable manufacturing practices and the use of eco-friendly materials to align with environmental regulations and corporate responsibility.

AI Impact Analysis on Non Segregated Phase Bus Duct

The impact of Artificial Intelligence (AI) on the Non Segregated Phase Bus Duct market is increasingly becoming a focal point for industry stakeholders, with common user questions revolving around its potential to revolutionize design, manufacturing, operational efficiency, and predictive maintenance. AI's capacity for advanced data processing and pattern recognition can significantly enhance the traditional lifecycle of bus duct systems. For instance, in the design phase, AI algorithms can optimize conductor sizing, insulation thickness, and cooling methodologies, leading to more efficient and cost-effective designs that meet stringent performance requirements and reduce material usage. This optimization can account for various operational parameters and environmental conditions, leading to more resilient and reliable products.

In manufacturing, AI-driven automation and quality control systems can improve production precision, reduce defects, and accelerate throughput. AI-powered vision systems can inspect welds, material integrity, and coating consistency with unparalleled accuracy, ensuring that each component meets the highest quality standards before assembly. Furthermore, AI can optimize supply chain logistics by predicting demand fluctuations and potential material shortages, thereby minimizing disruptions and inventory costs. This integration of AI streamlines the production process, resulting in a more efficient and less wasteful manufacturing footprint, which aligns with industry sustainability goals.

Perhaps the most significant impact of AI lies in its application to operational monitoring and predictive maintenance of installed Non Segregated Phase Bus Duct systems. By analyzing real-time data from sensors (e.g., temperature, vibration, partial discharge), AI algorithms can identify subtle anomalies and predict potential failures long before they occur. This enables proactive maintenance scheduling, minimizing unscheduled downtime, extending equipment lifespan, and reducing operational expenditure. AI can also optimize energy flow within complex electrical networks by dynamically adjusting loads and routing power more efficiently, contributing to overall grid stability and energy savings. This intelligent management capability enhances the reliability and performance of critical power infrastructure.

- AI-driven design optimization for improved efficiency, material usage, and performance characteristics of Non Segregated Phase Bus Ducts.

- Enhanced manufacturing precision and quality control through AI-powered automation and vision inspection systems.

- Predictive maintenance capabilities utilizing AI algorithms to analyze sensor data, forecast failures, and optimize service schedules.

- Real-time operational monitoring and anomaly detection to ensure optimal performance and prevent costly downtime.

- Supply chain optimization through AI for demand forecasting and inventory management, improving material flow and reducing lead times.

- Development of smart bus duct systems with embedded AI for autonomous fault detection and self-healing functionalities in advanced grids.

Key Takeaways Non Segregated Phase Bus Duct Market Size & Forecast

The Non Segregated Phase Bus Duct market is poised for significant expansion, driven by continuous global infrastructure development, increasing power generation capacities, and the modernization of electrical grids. A primary takeaway is the consistent growth projected for the market, indicating strong underlying demand across various industrial and commercial sectors. This expansion is not merely incremental but is being catalyzed by the inherent advantages of NSPBDs, such as their high current carrying capacity, durability, and compact design, which are increasingly favored over traditional cabling solutions in high-power applications. The market's resilience is further supported by investments in smart city initiatives and renewable energy projects, creating new avenues for application.

Another crucial insight is the accelerating pace of technological integration within the bus duct sector. The emphasis on smart features, IoT connectivity, and advanced monitoring systems is transforming NSPBDs from passive power conduits into intelligent components of complex electrical networks. This shift allows for enhanced operational efficiency, proactive maintenance, and improved safety standards, which are critical for maintaining continuous power supply in demanding environments. The drive towards digitalization is not just a trend but a fundamental strategic imperative for manufacturers to stay competitive and meet the evolving needs of their clientele, leading to higher value-added products.

Furthermore, the market forecast highlights the growing importance of regional dynamics, particularly in emerging economies where rapid industrialization and urbanization are fueling massive construction and infrastructure projects. While established markets in North America and Europe continue to invest in grid modernization and data center expansion, regions like Asia Pacific and the Middle East are experiencing explosive growth due to new utility installations and large-scale industrial facility development. These regional disparities create diverse opportunities and challenges, requiring market players to adopt flexible strategies regarding product offerings, distribution networks, and localized support to capture market share effectively and ensure sustained growth throughout the forecast period.

- The Non Segregated Phase Bus Duct market is projected for robust growth, driven by industrialization and infrastructure development.

- Technological advancements, including smart monitoring and digitalization, are enhancing the value and efficiency of NSPBDs.

- Significant growth opportunities exist in emerging economies due to rapid urbanization and increasing power demands.

- The shift towards renewable energy sources and grid modernization projects are key growth catalysts.

- Emphasis on high-performance, modular, and sustainable NSPBD solutions is shaping product development.

- Predictive maintenance and enhanced safety features are becoming standard expectations for new installations.

Non Segregated Phase Bus Duct Market Drivers Analysis

The Non Segregated Phase Bus Duct market is primarily driven by the escalating demand for reliable and efficient power distribution solutions across a multitude of sectors. Rapid industrialization and urbanization globally necessitate robust electrical infrastructure capable of handling high power loads with minimal losses, a requirement precisely met by NSPBDs. Their inherent advantages over traditional cabling, such as better heat dissipation, higher short-circuit withstand capability, and compact design, make them a preferred choice for large-scale industrial facilities, commercial complexes, and data centers. The continuous expansion of manufacturing capabilities and the development of modern urban centers directly translate into increased installation of these essential power conduits.

Moreover, the substantial global investments in modernizing and expanding power generation and transmission infrastructure are significant market drivers. This includes the construction of new power plants, both conventional and renewable, and the upgrade of aging electrical grids to enhance their capacity, stability, and resilience. NSPBDs are integral to these projects, serving as crucial links for power evacuation from generation sources and efficient distribution within substations and industrial facilities. The push towards smart grids and the integration of diverse energy sources further amplify the need for advanced, high-performance bus duct systems that can seamlessly manage complex power flows. This technological evolution within the power sector provides a sustained impetus for market growth.

The burgeoning data center industry also stands as a powerful driver for the Non Segregated Phase Bus Duct market. Data centers require extremely reliable and high-capacity power distribution systems to ensure uninterrupted operation of critical IT equipment. NSPBDs offer a superior solution due to their ability to carry large currents, minimize voltage drops, and provide inherent electromagnetic shielding, which are vital for maintaining data integrity and system stability. As the global demand for cloud computing, big data analytics, and digital services continues to surge, so does the construction of new data centers and the expansion of existing ones, directly translating into increased procurement of Non Segregated Phase Bus Ducts. This specialized demand segment offers a high-growth opportunity for market players.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Industrialization & Urbanization | +1.5% | Asia Pacific, Middle East & Africa, Latin America | 2025-2033 |

| Power Generation & Grid Modernization Investments | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Booming Data Center Industry Expansion | +1.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Increased Focus on Energy Efficiency | +0.8% | Global | 2025-2033 |

Non Segregated Phase Bus Duct Market Restraints Analysis

Despite the positive growth outlook, the Non Segregated Phase Bus Duct market faces several notable restraints that could temper its expansion. One significant challenge is the relatively high initial capital investment required for NSPBD systems compared to conventional cabling solutions. While NSPBDs offer long-term benefits in terms of efficiency and maintenance, the upfront cost can be a deterrent, particularly for smaller projects or in regions with constrained budgets. This cost differential can sometimes lead project developers to opt for less expensive alternatives, even if they are less efficient or require more extensive maintenance over time. Overcoming this perception requires robust cost-benefit analyses and demonstrating the total cost of ownership advantages of NSPBDs.

Another restraint stems from the intense competition posed by alternative power distribution technologies, particularly traditional power cables. In many applications, especially those not requiring very high current capacities or facing space constraints, power cables remain a viable and often more familiar option for engineers and contractors. The entrenched position of cables in established markets and the ease of their installation in certain scenarios can limit the adoption of bus ducts. This necessitates continuous innovation from bus duct manufacturers to highlight their superior performance characteristics, reliability, and safety features that differentiate them from conventional wiring methods, thereby justifying their premium positioning in the market.

Furthermore, the market is susceptible to fluctuations in raw material prices, specifically copper and aluminum, which are primary components in the manufacturing of Non Segregated Phase Bus Ducts. Volatility in commodity markets can directly impact production costs, leading to price instability for end-users and potentially affecting project budgets and timelines. Such unpredictability can make long-term project planning challenging for both manufacturers and purchasers, potentially hindering large-scale investments in new installations. Supply chain disruptions, as experienced in recent global events, can exacerbate these challenges by limiting material availability and increasing lead times, thereby delaying project completions and impacting market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.9% | Global, particularly emerging economies | 2025-2033 |

| Competition from Alternative Cabling Solutions | -0.7% | Global | 2025-2033 |

| Fluctuations in Raw Material Prices | -0.6% | Global | 2025-2030 |

| Stringent Regulatory & Standardization Challenges | -0.5% | Europe, North America | 2025-2028 |

Non Segregated Phase Bus Duct Market Opportunities Analysis

Significant opportunities exist for the Non Segregated Phase Bus Duct market, primarily driven by the burgeoning renewable energy sector and the global push towards smart city infrastructure. The rapid expansion of solar power farms, wind energy projects, and other renewable energy sources necessitates robust and efficient power collection and evacuation systems. NSPBDs, with their high current carrying capacity and low power loss characteristics, are ideally suited for integrating these large-scale renewable generation sites into existing grids. This presents a substantial growth avenue for manufacturers, as they can tailor solutions to meet the specific demands of green energy projects, offering enhanced efficiency and reliability in power transmission from source to grid connection points.

Another major opportunity lies in the increasing global investment in smart grid technologies and the development of resilient urban infrastructure. Smart grids require highly reliable and controllable power distribution systems, where NSPBDs can play a pivotal role. The integration of advanced monitoring, control, and communication capabilities within bus duct systems enables seamless data exchange and contributes to a more stable and efficient power network. As cities worldwide modernize their infrastructure to support sustainable growth, the demand for high-performance power distribution solutions that can accommodate dynamic loads and incorporate advanced digital features will continue to rise, offering considerable prospects for market expansion. This transition also involves retrofitting existing older infrastructure with more efficient and safer solutions.

Furthermore, emerging economies, particularly in Asia Pacific, Latin America, and the Middle East & Africa, present vast untapped market potential. These regions are undergoing rapid industrialization, urbanization, and significant infrastructure development, leading to a substantial increase in electricity demand and the need for modern power distribution systems. Unlike mature markets, these economies often have fewer legacy systems, allowing for the direct adoption of advanced NSPBD technologies in new construction projects. Government initiatives to improve power access, build new manufacturing facilities, and develop commercial hubs in these regions are expected to drive robust demand for Non Segregated Phase Bus Ducts, offering manufacturers opportunities to establish strong market footholds and expand their global presence significantly.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Renewable Energy Projects | +1.1% | Global, particularly Asia Pacific, Europe | 2025-2033 |

| Smart Grid & Smart City Development | +1.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Untapped Markets in Emerging Economies | +0.9% | Asia Pacific, Middle East & Africa, Latin America | 2025-2033 |

| Replacement & Retrofit of Aging Infrastructure | +0.7% | North America, Europe | 2025-2033 |

Non Segregated Phase Bus Duct Market Challenges Impact Analysis

The Non Segregated Phase Bus Duct market faces several significant challenges that could impede its growth trajectory. One primary challenge is the complexity of design and installation, often requiring specialized engineering expertise and meticulous planning. Unlike flexible cables, bus ducts are rigid structures that demand precise measurements and fit, making on-site adjustments difficult and increasing the potential for errors. This complexity translates into higher installation costs and longer project timelines, particularly for custom solutions or retrofitting existing facilities. The availability of skilled labor for both design and installation is also a critical concern, as a shortage of experienced professionals can lead to project delays and quality issues, impacting overall market adoption rates.

Another notable challenge revolves around the increasingly stringent global quality and safety standards. Manufacturers must adhere to a myriad of international and regional regulations, which can vary significantly across different markets. Compliance requires rigorous testing, certification processes, and often, significant investment in research and development to ensure products meet the highest safety and performance benchmarks. Failing to meet these standards can result in product recalls, legal liabilities, and reputational damage. This regulatory landscape demands continuous adaptation and innovation from market players, adding to production complexities and potentially increasing costs, especially for companies seeking to expand their global reach.

Furthermore, the market is vulnerable to supply chain disruptions and volatility in the cost of raw materials. The manufacturing of Non Segregated Phase Bus Ducts relies heavily on key commodities such as copper, aluminum, and various insulation materials. Geopolitical events, trade disputes, and natural disasters can disrupt the supply of these materials, leading to shortages, price spikes, and increased lead times. Such unpredictability makes it challenging for manufacturers to maintain stable pricing and delivery schedules, which can deter potential buyers and impact profitability. Building resilient and diversified supply chains is a constant endeavor for companies in this sector, requiring strategic partnerships and risk mitigation efforts to minimize the impact of external shocks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Design & Installation | -0.8% | Global | 2025-2033 |

| Skilled Labor Shortage | -0.7% | North America, Europe | 2025-2033 |

| Stringent Quality & Safety Standards | -0.6% | Global | 2025-2033 |

| Supply Chain Disruptions & Raw Material Volatility | -0.5% | Global | 2025-2030 |

Non Segregated Phase Bus Duct Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Non Segregated Phase Bus Duct market, offering a detailed forecast from 2025 to 2033. It encompasses a thorough examination of market size, growth drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. The report segments the market by various parameters, including insulation type, voltage level, application, and end-use industry, alongside a meticulous regional analysis covering key geographies. It highlights the competitive landscape by profiling leading market players, offering insights into their strategies and market positioning. The scope also includes an assessment of emerging trends, the impact of technological advancements such as AI, and a discussion of the regulatory environment affecting market dynamics. The objective is to equip stakeholders with actionable intelligence for strategic decision-making and investment planning within the global Non Segregated Phase Bus Duct market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.15 Billion |

| Market Forecast in 2033 | USD 6.55 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Eaton, ABB, Siemens, Schneider Electric, GE, Legrand, Anord Mardix, Beta-Calco, DBK Group, Megabarre, Pintech, EAE Elektrik, Power Busway, Powell Industries, Inc., Delta Electrical Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Non Segregated Phase Bus Duct market is comprehensively segmented to provide granular insights into its diverse components and applications. This segmentation allows for a detailed understanding of specific market dynamics, technological preferences, and demand patterns across various industry verticals and geographical regions. Analyzing the market through these segments helps identify niche opportunities, assess competitive landscapes within specific product categories, and forecast growth trajectories more accurately. Each segment represents a distinct facet of the market, driven by unique requirements and influencing factors, thereby offering a multifaceted perspective on the overall industry structure.

The segmentation by insulation type, including air, solid, and gas insulated NSPBDs, reflects varying performance characteristics, safety considerations, and cost implications, catering to different operational environments and voltage requirements. Voltage level segmentation, spanning low, medium, and high voltage categories, directly correlates with the scale and application of power distribution systems, from building infrastructure to large-scale power plants. Furthermore, the market is broken down by application areas such as power generation, industrial, commercial, and infrastructure, highlighting the diverse end-use sectors where NSPBDs are deployed. This detailed categorization provides a strategic framework for stakeholders to evaluate market potential and devise targeted approaches for product development and market penetration, ensuring their offerings align with specific client needs and industry demands.

- By Insulation Type:

- Air Insulated

- Solid Insulated

- Gas Insulated

- By Voltage Level:

- Low Voltage (Up to 1 kV)

- Medium Voltage (1 kV - 36 kV)

- High Voltage (Above 36 kV)

- By Application:

- Power Generation

- Thermal Power Plants

- Hydroelectric Power Plants

- Nuclear Power Plants

- Renewable Energy (Solar, Wind)

- Industrial

- Manufacturing Plants

- Process Industries (Oil & Gas, Chemicals)

- Metals & Mining

- Automotive

- Commercial

- Data Centers

- Commercial Buildings (Offices, Retail)

- Healthcare Facilities

- Hospitality

- Infrastructure

- Transportation (Airports, Metro, Railways)

- Utilities & Substations

- Telecommunications

- Power Generation

- By End-Use Industry:

- Utilities

- Data Centers

- Manufacturing & Processing

- Transportation

- Commercial & Residential Buildings

Regional Highlights

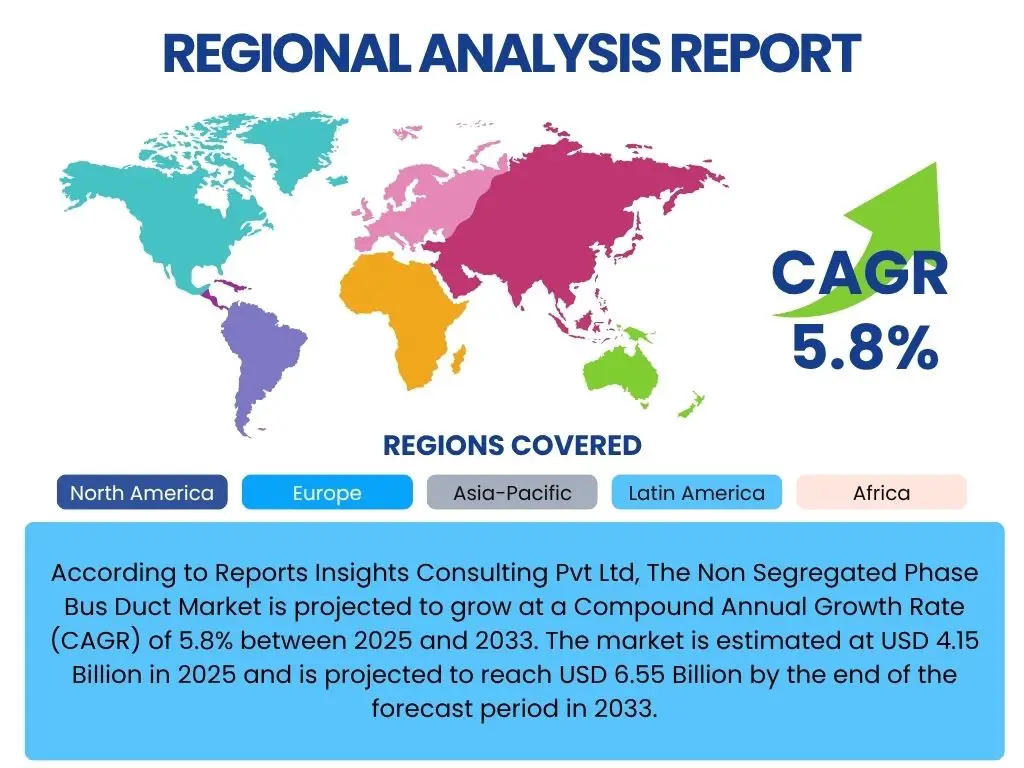

Regional analysis of the Non Segregated Phase Bus Duct market reveals diverse growth trajectories influenced by varying levels of industrialization, infrastructure development, and energy policies across the globe. Each major geographical segment contributes uniquely to the overall market landscape, driven by specific economic conditions and technological adoption rates. Understanding these regional dynamics is critical for market participants to tailor their strategies, allocate resources effectively, and capitalize on localized growth opportunities. The demand for NSPBDs is intrinsically linked to power consumption and the expansion of electrical grids, making regions with high economic activity and energy transition initiatives key areas of focus. This detailed regional breakdown offers insights into the prevailing market conditions and future prospects, facilitating informed decision-making for global expansion.

- North America: This region demonstrates a steady demand driven by extensive investments in data center infrastructure, modernization of aging power grids, and the expansion of commercial and industrial facilities. The United States and Canada lead in adopting advanced bus duct solutions due to stringent safety standards and a focus on energy efficiency. The emphasis on smart grid initiatives and renewable energy integration further fuels market growth, particularly for high-performance and digitally-enabled NSPBDs.

- Europe: Characterized by a strong focus on renewable energy integration, grid stability, and industrial automation, Europe presents a mature but evolving market. Countries like Germany, France, and the UK are investing heavily in upgrading their industrial infrastructure and enhancing grid resilience, driving the demand for reliable and compact power distribution systems. Regulatory frameworks promoting energy efficiency and sustainable practices also play a crucial role in shaping market trends and product development.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market due to rapid industrialization, urbanization, and significant investments in power generation capacity, especially in countries like China, India, Japan, and South Korea. The construction of new manufacturing plants, commercial buildings, and extensive public infrastructure projects creates immense demand for NSPBDs. The burgeoning data center market and the expansion of renewable energy portfolios further accelerate market expansion in APAC.

- Latin America: The market in Latin America is witnessing gradual growth, primarily driven by investments in energy infrastructure development, industrial expansion, and mining activities in countries such as Brazil and Mexico. The need for reliable power distribution in new industrial zones and the upgrade of existing facilities contribute to the demand for Non Segregated Phase Bus Ducts. Economic stability and foreign direct investment are key factors influencing market progression in this region.

- Middle East and Africa (MEA): This region offers substantial growth opportunities, spurred by large-scale infrastructure projects, expansion of power generation capacities, and diversification of economies away from oil. Countries like Saudi Arabia, UAE, and Qatar are investing in mega-projects, including smart cities, industrial zones, and new power plants, creating a robust demand for advanced electrical distribution solutions. The growing focus on renewable energy and data center development also acts as a significant catalyst for the NSPBD market in MEA.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Non Segregated Phase Bus Duct Market.- Eaton

- ABB

- Siemens

- Schneider Electric

- GE

- Legrand

- Anord Mardix

- Beta-Calco

- DBK Group

- Megabarre

- Pintech

- EAE Elektrik

- Power Busway

- Powell Industries, Inc.

- Delta Electrical Systems

- L&T Electrical & Automation

- Godrej & Boyce

- C&S Electric

- Honeywell International Inc.

- Rittal GmbH & Co. KG

Frequently Asked Questions

Analyze common user questions about the Non Segregated Phase Bus Duct market and generate a concise list of summarized FAQs reflecting key topics and concerns.

What is a Non Segregated Phase Bus Duct?

A Non Segregated Phase Bus Duct (NSPBD) is an electrical power distribution system typically used in high-current applications. It consists of conductors for each phase (e.g., A, B, C) that are separated by air and supported by insulators within a common metallic enclosure. Unlike segregated or isolated phase bus ducts, the phases are not individually isolated from each other or the enclosure, though they are kept distinct and supported to prevent short circuits, offering a compact and cost-effective solution for power transmission.

What are the primary benefits of using Non Segregated Phase Bus Ducts?

NSPBDs offer several key advantages, including a compact design that saves space, high current carrying capacity for efficient power transmission, superior short-circuit withstand capability for enhanced safety, and lower voltage drop compared to traditional cables over long distances. They also typically have a longer lifespan, require less maintenance, and are easier to install due to their modular construction, contributing to lower total cost of ownership in industrial and commercial settings.

Where are Non Segregated Phase Bus Ducts commonly applied?

Non Segregated Phase Bus Ducts find extensive applications in various high-power environments. They are widely used in power generation plants (thermal, hydro, nuclear, renewable), industrial facilities (manufacturing, processing plants, metals & mining), data centers requiring reliable and high-capacity power, and large commercial buildings. They are also integral to modernizing urban infrastructure, including transportation hubs and utility substations, for efficient and safe power distribution.

What is the typical lifespan and maintenance requirement for NSPBDs?

Non Segregated Phase Bus Ducts are designed for long operational lifespans, typically ranging from 30 to 50 years, depending on environmental conditions and maintenance practices. Maintenance requirements are generally low compared to complex cabling systems, primarily involving routine inspections, cleaning of insulators, and periodic checks of connections. The integration of smart monitoring systems further reduces maintenance efforts by enabling predictive maintenance, identifying potential issues before they escalate.

How do Non Segregated Phase Bus Ducts contribute to energy efficiency?

NSPBDs contribute to energy efficiency by minimizing power losses during transmission. Their optimized conductor design and efficient heat dissipation capabilities result in lower ohmic losses compared to traditional cable systems, especially at high current loads. This reduction in energy waste translates into significant operational cost savings over the lifespan of the system, aligning with global initiatives for sustainable and energy-efficient power distribution solutions across industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted