LCD Glass Substrate Market

LCD Glass Substrate Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707546 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

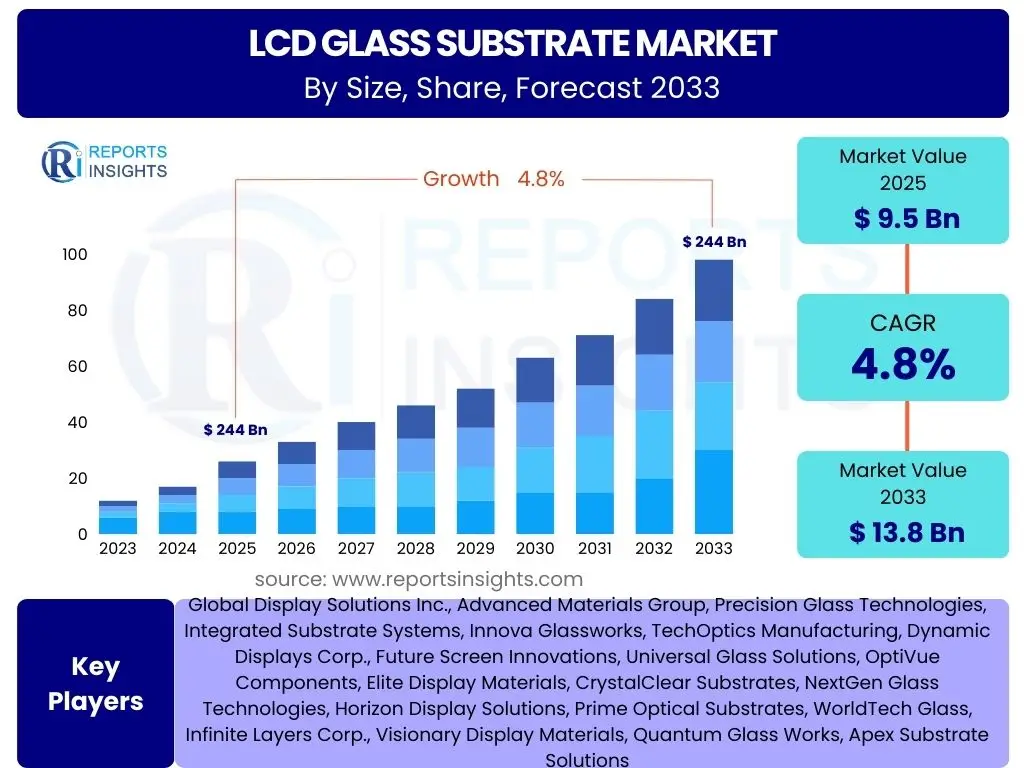

LCD Glass Substrate Market Size

According to Reports Insights Consulting Pvt Ltd, The LCD Glass Substrate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 9.5 Billion in 2025 and is projected to reach USD 13.8 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by the persistent demand for display technologies across various consumer and industrial sectors, despite the evolving landscape of display technologies. The market's resilience is further supported by ongoing innovations in glass manufacturing and processing, which continue to enhance the performance and cost-effectiveness of LCD panels, ensuring their continued relevance in a competitive display market.

The forecasted expansion reflects a stable demand for traditional LCD applications, particularly in large-format televisions, monitors, and select professional displays. While advanced display technologies like OLED and MicroLED are gaining traction, LCDs maintain a strong foothold due to their mature production infrastructure, cost efficiency, and proven performance across a wide range of applications. Furthermore, the expansion into new vertical markets such as automotive infotainment systems, digital signage, and specialized industrial equipment contributes significantly to the sustained demand for high-quality LCD glass substrates, providing a steady growth impetus throughout the forecast period.

Key LCD Glass Substrate Market Trends & Insights

User queries regarding trends in the LCD Glass Substrate market frequently center on technological evolution, market diversification, and the impact of manufacturing efficiencies. Common questions include how display size trends influence substrate demand, the role of material science advancements, and the push for thinner, lighter, and more durable glass. There is also significant interest in the competitive dynamics with emerging display technologies and the industry's response to supply chain complexities. These inquiries highlight a collective focus on the market's adaptability and future trajectory in a rapidly changing technological landscape.

- Shift Towards Larger Display Sizes: The increasing consumer preference for larger televisions and monitors, alongside the proliferation of digital signage and large-format commercial displays, is a primary driver. This trend necessitates the production of larger glass substrates, leading to investments in higher-generation fabrication facilities (Gen 8, Gen 10, Gen 10.5 and beyond) that can efficiently produce multiple large panels from a single sheet.

- Integration into Diverse Applications: Beyond traditional consumer electronics, LCD glass substrates are finding expanding utility in automotive displays, industrial human-machine interfaces (HMIs), medical equipment, and smart home devices. This diversification reduces reliance on any single application segment, providing market stability and opening new avenues for growth.

- Advancements in Substrate Manufacturing Processes: Continuous innovation in glass melting, forming, and cutting technologies aims to improve yield rates, reduce defects, and enhance material properties. Techniques such as fusion draw processes are crucial for producing ultra-flat, smooth, and high-quality glass required for high-resolution displays.

- Emphasis on Thinner and Lighter Glass: The demand for sleeker electronic devices, including ultrathin laptops, tablets, and lightweight televisions, drives the need for thinner and lighter glass substrates. This trend also contributes to reduced shipping costs and material consumption, aligning with sustainability goals.

- Increased Demand for High-Resolution Displays: The proliferation of 4K and 8K resolution content and devices necessitates glass substrates with superior dimensional stability and surface quality to support the higher pixel densities required for crisp, clear images. This pushes manufacturers to achieve tighter tolerances and introduce advanced inspection systems.

AI Impact Analysis on LCD Glass Substrate

Common user questions regarding AI's impact on the LCD Glass Substrate sector often revolve around its potential to revolutionize manufacturing efficiency, quality control, and supply chain management. Users are keen to understand how AI can reduce defects, optimize production yields, and enable more predictive maintenance in highly complex and capital-intensive glass manufacturing environments. There is also curiosity about AI's role in accelerating material science research for next-generation substrates and its implications for workforce dynamics and operational costs within the industry.

- AI in Quality Control and Defect Detection: Artificial intelligence, particularly machine vision systems powered by deep learning, is transforming quality inspection. AI algorithms can analyze vast amounts of data from high-speed cameras to identify microscopic defects, impurities, and structural anomalies on glass substrates with greater accuracy and speed than human inspection, significantly improving outgoing product quality and reducing scrap rates.

- Optimization of Manufacturing Parameters: AI and machine learning models are being deployed to analyze real-time production data from various stages of the glass manufacturing process, including melting, forming, annealing, and cutting. These models can identify optimal operational parameters to minimize energy consumption, maximize throughput, and ensure consistent product quality, leading to substantial operational efficiencies.

- Predictive Maintenance for Production Lines: AI-powered predictive analytics monitor the health of complex manufacturing machinery and equipment, such as furnaces, draw machines, and cutting tools. By analyzing sensor data, AI can anticipate equipment failures before they occur, enabling proactive maintenance schedules. This minimizes unscheduled downtime, extends equipment lifespan, and maintains continuous production flows, crucial for high-volume manufacturing.

- Supply Chain Optimization: AI algorithms can process and analyze global supply chain data, including raw material availability, logistics routes, and demand forecasts. This enables manufacturers to optimize inventory levels, mitigate risks from supply disruptions, and ensure timely delivery of glass substrates, enhancing overall supply chain resilience and responsiveness in a volatile market.

- Enhanced Material Science R&D: AI is increasingly used in research and development to simulate and predict the properties of new glass compositions and processing techniques. By accelerating the discovery of novel materials with enhanced optical, mechanical, or electrical characteristics, AI can significantly shorten the development cycle for next-generation LCD glass substrates, driving innovation and competitive advantage.

Key Takeaways LCD Glass Substrate Market Size & Forecast

User inquiries about key takeaways from the LCD Glass Substrate market size and forecast often focus on understanding the primary growth drivers, the significance of technological advancements, and the future relevance of LCD technology amidst competition. There's a strong interest in identifying the most impactful trends influencing market expansion or contraction, as well as the critical factors that will shape the competitive landscape. Summarily, users seek clear, concise insights into what truly matters for market participants and observers in the coming years.

- Steady Growth Driven by Diversification: The market is projected to experience consistent growth, not solely reliant on traditional consumer electronics, but increasingly supported by the expansion into automotive, industrial, and specialized display applications. This diversification acts as a significant buffer against market fluctuations in any single sector.

- Innovation in Manufacturing is Crucial: Continuous advancements in glass manufacturing processes, particularly those focused on increasing size, reducing thickness, and improving material purity, are vital for maintaining competitive edge and meeting evolving display technology requirements. Companies investing in these areas are likely to lead the market.

- Regional Demand Shifts: While Asia Pacific remains the dominant production and consumption hub, emerging markets in Latin America and the Middle East & Africa are expected to contribute to demand growth, alongside sustained innovation and adoption in North America and Europe for niche, high-value applications.

- Impact of Competing Display Technologies: The rise of OLED, MicroLED, and other next-generation display technologies presents a long-term competitive challenge. The LCD glass substrate market's ability to innovate, remain cost-effective, and integrate into hybrid display solutions will be crucial for its sustained relevance.

- Focus on Cost-Efficiency and Performance: Success in the LCD glass substrate market will increasingly hinge on the ability of manufacturers to deliver high-performance substrates at competitive prices. This involves optimizing production processes, reducing waste, and leveraging economies of scale to meet the demanding requirements of display panel manufacturers globally.

LCD Glass Substrate Market Drivers Analysis

The LCD Glass Substrate market is propelled by a confluence of factors, primarily stemming from the ubiquitous integration of displays into modern life and the continuous evolution of digital technologies. These drivers underscore the foundational role of glass substrates in enabling a vast array of electronic devices and digital interfaces. The sustained demand for visual content and interactive experiences across diverse sectors ensures a resilient and expanding market for these critical components, despite dynamic technological shifts and market forces.

Key drivers include the relentless innovation in consumer electronics, the burgeoning demand for high-resolution displays in professional settings, and the transformative impact of digital signage and automotive applications. Each of these segments contributes uniquely to the market's momentum, driving requirements for larger, thinner, and more sophisticated glass substrates. The ongoing refinement of display technologies, even those that eventually supersede LCDs, often relies on foundational glass substrate manufacturing expertise, further securing its market position.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for consumer electronics | +1.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Expansion of automotive displays | +0.8% | Europe, North America, China | 2026-2033 |

| Proliferation of digital signage | +0.7% | Global, especially urban areas | 2025-2033 |

| Development of new display technologies requiring glass | +0.5% | Global, R&D Hubs | 2027-2033 |

| Urbanization and smart city initiatives | +0.4% | Asia Pacific, Middle East, Europe | 2026-2033 |

LCD Glass Substrate Market Restraints Analysis

While the LCD Glass Substrate market demonstrates robust growth, it is not without significant impediments that could temper its expansion. These restraints primarily stem from intense technological competition, the inherent cost structure of advanced manufacturing, and external market vulnerabilities. The dynamic nature of the display industry means that constant innovation is required, but this also introduces challenges related to the rapid obsolescence of older technologies and the high capital expenditure for new facilities.

Foremost among these restraints is the formidable competition from alternative display technologies, which are continuously improving in performance and reducing in cost, potentially eroding LCD's market share in certain premium segments. Furthermore, the global supply chain for glass substrates is susceptible to geopolitical tensions, trade disputes, and fluctuations in raw material prices, which can directly impact manufacturing costs and product availability. Stringent environmental regulations also impose additional compliance burdens and operational costs, requiring significant investment in sustainable practices and waste management.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from OLED and emerging display technologies | -1.2% | Global, particularly premium segments | 2025-2033 |

| Fluctuations in raw material prices | -0.6% | Global, supply chain dependent | 2025-2033 |

| High capital expenditure for manufacturing facilities | -0.5% | Global, especially new entrants | 2025-2033 |

| Environmental regulations and sustainability concerns | -0.4% | Europe, North America, East Asia | 2026-2033 |

| Geopolitical trade tensions and protectionism | -0.3% | Global, specific trade routes | 2025-2030 |

LCD Glass Substrate Market Opportunities Analysis

Despite existing restraints, the LCD Glass Substrate market is rich with opportunities that can propel its growth and relevance into the future. These opportunities are often tied to innovative applications of display technology, advancements in material science, and the expansion into underserved or emerging market segments. The industry's capacity for adaptation and its foundational role in display manufacturing position it well to capitalize on these new frontiers, ensuring sustained demand for high-quality glass substrates.

Significant opportunities lie in the development and proliferation of flexible and foldable display technologies, which require novel glass substrates capable of extreme bending and durability. The growing demand for high-performance computing displays, particularly in professional and gaming sectors, also creates a niche for advanced, high-resolution LCDs. Furthermore, the expansion into specialized industrial applications, such as medical diagnostics, avionics, and ruggedized outdoor displays, offers high-value segments that prioritize reliability and specific performance characteristics over absolute cost, allowing for premium product offerings.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of flexible and foldable displays | +0.9% | Global, R&D Hubs | 2027-2033 |

| High-performance computing displays | +0.7% | North America, Europe, East Asia | 2025-2033 |

| Expansion into niche industrial applications | +0.6% | Global, developed economies | 2025-2033 |

| Advancements in ultra-thin and lightweight glass | +0.5% | Global | 2025-2033 |

| Miniaturization and increased pixel density | +0.4% | Global, consumer electronics manufacturers | 2026-2033 |

LCD Glass Substrate Market Challenges Impact Analysis

The LCD Glass Substrate market faces several critical challenges that demand continuous innovation and strategic adaptation from manufacturers. These challenges are often multifaceted, encompassing technological hurdles, economic pressures, and environmental considerations. Successfully navigating these complexities is paramount for companies aiming to maintain competitiveness and secure long-term viability in a rapidly evolving display industry, which is characterized by high stakes and significant investment requirements for R&D and manufacturing infrastructure.

One primary challenge is achieving ever-higher levels of transparency and purity in glass substrates, which becomes increasingly difficult as display resolutions and performance demands escalate. Managing supply chain disruptions, whether from natural disasters, geopolitical events, or global health crises, remains a persistent operational challenge, impacting production schedules and material costs. Moreover, the intense competition among existing manufacturers and the continuous emergence of alternative display technologies necessitate constant innovation and cost-optimization strategies to retain market share and profitability, requiring substantial and ongoing capital investment in both facilities and research initiatives.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving higher transparency and purity | -0.8% | Global, R&D centers | 2025-2033 |

| Managing supply chain disruptions | -0.7% | Global | 2025-2030 |

| Intense competition among manufacturers | -0.6% | Global | 2025-2033 |

| Adapting to rapid technological shifts | -0.5% | Global, display industry | 2025-2033 |

| Waste management and recycling | -0.4% | Europe, North America, East Asia | 2026-2033 |

LCD Glass Substrate Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the LCD Glass Substrate market, providing a detailed analysis of its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of key market trends, significant drivers, restraining factors, emerging opportunities, and inherent challenges impacting the industry. It offers granular insights into market segmentation by type, generation, application, and material, alongside a robust regional analysis to identify high-growth areas and market-specific nuances. The report also highlights the competitive landscape by profiling leading market players and provides essential FAQs for quick reference.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.5 Billion |

| Market Forecast in 2033 | USD 13.8 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Display Solutions Inc., Advanced Materials Group, Precision Glass Technologies, Integrated Substrate Systems, Innova Glassworks, TechOptics Manufacturing, Dynamic Displays Corp., Future Screen Innovations, Universal Glass Solutions, OptiVue Components, Elite Display Materials, CrystalClear Substrates, NextGen Glass Technologies, Horizon Display Solutions, Prime Optical Substrates, WorldTech Glass, Infinite Layers Corp., Visionary Display Materials, Quantum Glass Works, Apex Substrate Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LCD Glass Substrate market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for a detailed analysis of specific product types, technological generations, varied applications, and material compositions, each contributing uniquely to the overall market landscape. By breaking down the market into these critical dimensions, stakeholders can gain precise insights into demand patterns, technological preferences, and growth opportunities within different industry verticals and product categories, enabling more targeted strategic planning and investment decisions across the value chain. This comprehensive approach helps to identify niche markets and emerging trends that might otherwise be overlooked in broader analyses.

- By Type:

- TFT LCD Substrate: The dominant type, crucial for high-resolution, color-rich displays found in TVs, smartphones, and monitors due to its advanced transistor technology.

- TN/STN LCD Substrate: Used in simpler, monochrome, or low-resolution displays like calculators, basic industrial instruments, and segment displays, characterized by its cost-effectiveness.

- Others: Includes specialty glass substrates tailored for specific functionalities, such as those with integrated sensors or unique optical properties for niche applications.

- By Generation:

- Gen 6: Commonly used for mid-sized displays like laptop screens and monitors, offering an economical balance between size and efficiency.

- Gen 8: A key generation for producing large TV panels and professional displays, offering significant economies of scale.

- Gen 10: Designed for even larger display production, enabling the manufacturing of multiple 65-inch or 75-inch TV panels from a single sheet, driving down costs.

- Gen 10.5: Represents the cutting edge in large-area substrate production, optimized for ultra-large televisions (e.g., 90+ inches) and high-efficiency manufacturing.

- Others: Encompasses older generations (e.g., Gen 5, Gen 7) still in use for smaller or legacy applications, as well as experimental larger or specialized generations.

- By Application:

- Televisions: The largest segment, driven by global consumer demand for larger and higher-resolution screens.

- Smartphones & Tablets: Requires thinner, more durable, and often alkali-free substrates for compact and portable devices.

- Laptops & Monitors: A stable segment demanding good resolution and color performance for personal and professional computing.

- Automotive Displays: A rapidly growing segment, driven by the integration of infotainment, navigation, and digital dashboards, requiring robust and high-temperature resistant substrates.

- Digital Signage & Professional Displays: Includes large-format screens for advertising, public information, and control rooms, prioritizing durability and brightness.

- Wearable Devices: Demands ultra-thin, lightweight, and sometimes flexible substrates for smartwatches and other personal tech.

- Industrial & Medical Displays: Applications requiring high reliability, specific environmental resistance, and precision, such as in factory automation and diagnostic equipment.

- Others: Diverse applications including smart home appliances, point-of-sale systems, and aerospace displays, each with unique substrate requirements.

- By Material:

- Borosilicate Glass: Known for its thermal resistance and chemical stability, used in various display types.

- Alkali-Free Alumino-Silicate Glass: Preferred for high-performance TFT LCDs due to its excellent dimensional stability, low thermal expansion, and resistance to alkali ion contamination, crucial for high-resolution and advanced displays.

- Others: Includes specialized glass compositions developed for specific performance enhancements, such as ultra-high strength, enhanced optical clarity, or unique electrical properties.

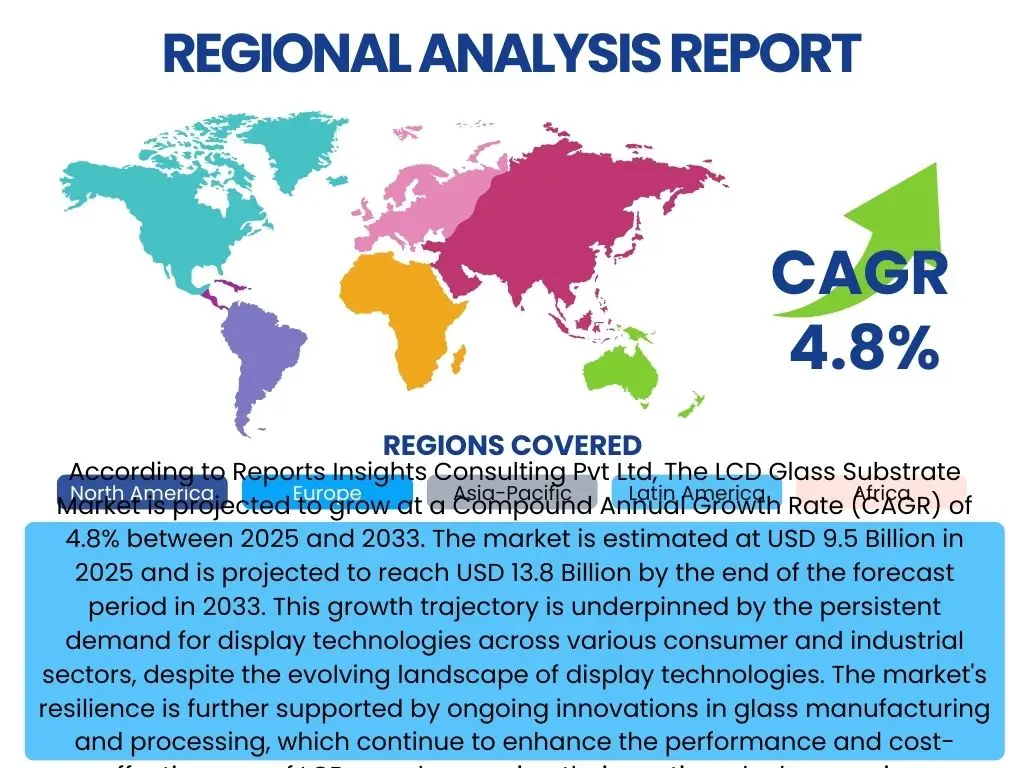

Regional Highlights

Regional dynamics play a pivotal role in shaping the LCD Glass Substrate market, with distinct patterns of manufacturing, consumption, and technological adoption across different geographies. Each region contributes uniquely to the market's global footprint, driven by varying economic conditions, consumer preferences, and industrial developments. Understanding these regional nuances is crucial for market participants to tailor their strategies and investments effectively, leveraging regional strengths and addressing localized challenges within the display manufacturing ecosystem.

- Asia Pacific (APAC): APAC stands as the undisputed powerhouse in the LCD Glass Substrate market, dominating both manufacturing and consumption. Countries like China, South Korea, Japan, and Taiwan host the majority of the world's large-scale display panel fabrication facilities, driving immense demand for substrates. This region benefits from established supply chains, a skilled workforce, and government support for high-tech manufacturing, making it the primary hub for global LCD production and a major consumer of finished display products. The rapid growth of consumer electronics markets in this region further solidifies its leading position.

- North America: North America is characterized by strong research and development capabilities and a high adoption rate of advanced display technologies. While large-scale manufacturing of glass substrates is less prevalent compared to APAC, the region drives demand for high-end, specialized LCD applications such as professional monitors, industrial displays, and rapidly expanding automotive infotainment systems. Innovation in display integration and new application development is a significant regional highlight, fostering demand for premium and specialized glass substrates.

- Europe: Europe exhibits a strong focus on niche industrial, automotive, and medical display applications, often prioritizing reliability, specific certifications, and bespoke solutions over sheer volume. The region is a hub for high-precision engineering and manufacturing, leading to demand for high-quality, durable LCD glass substrates for specialized machinery, smart factory interfaces, and advanced vehicle displays. Environmental regulations and sustainability initiatives also play a significant role, driving demand for more eco-friendly production processes and materials.

- Latin America: The Latin American market for LCD Glass Substrates is primarily driven by the growing consumer electronics sector and increasing penetration of digital infrastructure. While not a major manufacturing hub for substrates, the region's expanding middle class and urbanization contribute to a steady rise in demand for LCD televisions, smartphones, and digital signage. This market represents an area of significant growth potential for imports and localized assembly operations, with increasing opportunities for established display product suppliers.

- Middle East and Africa (MEA): MEA is an emerging market with increasing demand for digital infrastructure, consumer electronics, and smart city developments. The region's growing population and economic diversification efforts are fostering an uptick in demand for LCD panels in public displays, commercial installations, and general consumer use. While still smaller in scale compared to other regions, MEA presents future growth opportunities as investments in smart technologies and digital transformation continue to mature.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LCD Glass Substrate Market.- Global Display Solutions Inc.

- Advanced Materials Group

- Precision Glass Technologies

- Integrated Substrate Systems

- Innova Glassworks

- TechOptics Manufacturing

- Dynamic Displays Corp.

- Future Screen Innovations

- Universal Glass Solutions

- OptiVue Components

- Elite Display Materials

- CrystalClear Substrates

- NextGen Glass Technologies

- Horizon Display Solutions

- Prime Optical Substrates

- WorldTech Glass

- Infinite Layers Corp.

- Visionary Display Materials

- Quantum Glass Works

- Apex Substrate Solutions

Frequently Asked Questions

What is the projected growth rate for the LCD Glass Substrate market?

The LCD Glass Substrate market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, driven by diversified applications and ongoing technological advancements in display manufacturing.

How is AI transforming the manufacturing of LCD Glass Substrates?

AI is significantly impacting LCD Glass Substrate manufacturing by enhancing quality control through machine vision, optimizing production parameters for efficiency, enabling predictive maintenance, and streamlining supply chain management to reduce costs and improve responsiveness.

Which applications are driving the demand for LCD Glass Substrates?

Demand for LCD Glass Substrates is primarily driven by televisions, smartphones, laptops, automotive displays, and the rapidly expanding digital signage and professional display sectors. Niche industrial and medical applications also contribute significantly to market growth.

What are the primary challenges faced by the LCD Glass Substrate market?

Key challenges include intense competition from emerging display technologies like OLED, managing global supply chain disruptions, the high capital expenditure required for advanced manufacturing facilities, and the continuous need to achieve higher material purity and transparency for next-generation displays.

Which regions are expected to be key growth areas in the LCD Glass Substrate market?

Asia Pacific is expected to remain the dominant region for both production and consumption, with strong growth also anticipated in emerging markets within Latin America and the Middle East & Africa due to increasing digital infrastructure and consumer electronics adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted