DBC Ceramic Substrate Market

DBC Ceramic Substrate Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707262 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

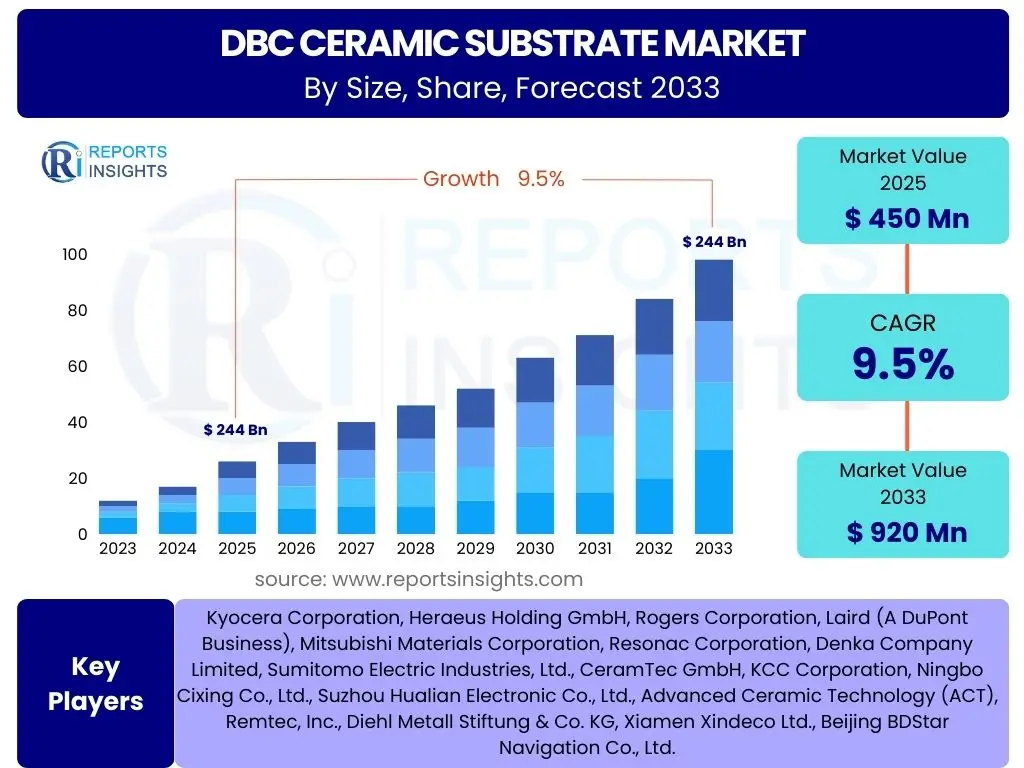

DBC Ceramic Substrate Market Size

According to Reports Insights Consulting Pvt Ltd, The DBC Ceramic Substrate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 920 Million by the end of the forecast period in 2033.

Key DBC Ceramic Substrate Market Trends & Insights

The Direct Bonded Copper (DBC) ceramic substrate market is undergoing significant transformation, driven by advancements in material science and increasing demand from high-power applications. A primary trend involves the continuous innovation in ceramic materials, moving beyond traditional alumina to include advanced ceramics like aluminum nitride (AlN) and silicon nitride (Si3N4). These newer materials offer superior thermal conductivity and mechanical strength, crucial for next-generation power modules and high-frequency devices. The industry is also witnessing a push towards higher integration and miniaturization, enabling more compact and efficient electronic designs across various sectors.

Furthermore, the market is characterized by a growing emphasis on enhanced reliability and performance under extreme operating conditions. This drives the development of DBC substrates with improved adhesion between copper and ceramic layers, as well as optimized surface finishes for better solderability and wire bonding. The increasing adoption of wide bandgap (WBG) semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), is another critical trend. WBG devices operate at higher temperatures and frequencies, necessitating advanced thermal management solutions that DBC substrates are uniquely positioned to provide, thereby expanding their application scope in demanding environments like electric vehicles and renewable energy systems.

- Technological advancements in ceramic materials, including Silicon Nitride (Si3N4) and Aluminum Nitride (AlN), for enhanced thermal conductivity and mechanical robustness.

- Growing demand for higher power density and miniaturization in electronic packaging, driving the need for compact DBC solutions.

- Increased integration of DBC substrates within Electric Vehicle (EV) and Hybrid Electric Vehicle (HEV) power electronics, including inverters, converters, and onboard chargers.

- Expansion of applications in renewable energy systems, specifically solar inverters, wind power converters, and energy storage systems.

- Focus on improved adhesion mechanisms and surface metallization techniques to enhance the long-term reliability and performance of DBC interconnections.

- Synergistic growth with the proliferation of wide bandgap (WBG) semiconductors (SiC and GaN), which benefit significantly from DBC's superior thermal dissipation capabilities.

- Rising demand for customized and application-specific DBC substrate designs to meet unique thermal and electrical requirements.

AI Impact Analysis on DBC Ceramic Substrate

Artificial Intelligence (AI) is poised to significantly influence the DBC ceramic substrate market across its entire value chain, from design and manufacturing to quality control and supply chain management. Common user inquiries often revolve around how AI can optimize production processes, reduce defects, and accelerate material innovation. AI algorithms can analyze vast datasets from manufacturing operations, identifying patterns and anomalies that lead to process inefficiencies or material inconsistencies. This capability enables predictive maintenance, real-time process adjustments, and optimized resource allocation, ultimately leading to higher yields and reduced operational costs for DBC substrate manufacturers.

Moreover, AI's role extends to enhancing the design and development phase of DBC substrates. Machine learning models can be employed to simulate material behaviors, predict thermal performance under varying conditions, and even assist in discovering novel ceramic compositions or bonding techniques. This significantly reduces the need for extensive physical prototyping and experimental iterations, accelerating time-to-market for new products and customized solutions. From a broader perspective, AI-driven demand forecasting and supply chain optimization can improve responsiveness to market fluctuations, ensuring a more stable and efficient supply of raw materials and finished products within the DBC ceramic substrate ecosystem.

- AI-driven optimization of DBC manufacturing processes, leading to increased yield, reduced waste, and improved production efficiency.

- Application of machine learning for predictive maintenance of manufacturing equipment, minimizing downtime and extending asset lifespan.

- AI-assisted material design and simulation, enabling faster discovery of novel ceramic compositions and bonding technologies with enhanced thermal and mechanical properties.

- Implementation of AI for advanced quality inspection, identifying microscopic defects and inconsistencies in DBC substrates with higher accuracy and speed than traditional methods.

- Enhanced supply chain management through AI-powered demand forecasting and logistics optimization, ensuring timely material procurement and product delivery.

- Development of smart factories utilizing AI for real-time monitoring and control of DBC production parameters, leading to consistent product quality.

- AI-facilitated data analysis for understanding customer requirements and market trends, guiding future product development and strategic investments.

Key Takeaways DBC Ceramic Substrate Market Size & Forecast

The DBC ceramic substrate market is on a robust growth trajectory, driven primarily by the escalating demand for high-performance power electronics across various industries. A key takeaway is the pivotal role DBC substrates play in enabling the transition to electric mobility and renewable energy sources, where efficient thermal management is paramount. The market's expansion is intrinsically linked to advancements in semiconductor technology, particularly the wider adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) devices, which necessitate the superior thermal dissipation capabilities offered by DBC substrates. This fundamental relationship underscores the market's resilience and long-term growth potential.

Another significant insight is the increasing differentiation in product offerings, with manufacturers focusing on material innovations and customized solutions to meet diverse application requirements. This includes the development of multi-layer DBC structures and substrates with enhanced mechanical strength for reliability in harsh environments. The geographical distribution of market growth also presents a crucial takeaway, with Asia Pacific expected to remain a dominant force due to its extensive manufacturing base and rapidly expanding automotive and consumer electronics sectors. The collective intelligence gathered indicates a market poised for continued innovation and expansion, offering substantial opportunities for stakeholders capable of addressing the evolving demands for power efficiency and system reliability.

- The DBC ceramic substrate market is projected for substantial growth, driven by increasing adoption in high-power electronic modules.

- Electric Vehicles (EVs) and renewable energy systems are critical growth catalysts, creating sustained demand for advanced thermal management solutions.

- Technological advancements in material science and manufacturing processes are key to unlocking new application areas and improving product performance.

- Asia Pacific is anticipated to maintain its leading position in market share, propelled by robust industrial expansion and electronics manufacturing.

- The market is shifting towards higher-performance materials like Silicon Nitride (Si3N4) and Aluminum Nitride (AlN) to support wide bandgap semiconductors (SiC, GaN).

- Increased investment in research and development for customized and high-reliability DBC substrates is a prominent trend.

- Opportunities exist in niche applications requiring extreme thermal and electrical performance, such as aerospace and advanced medical devices.

DBC Ceramic Substrate Market Drivers Analysis

The DBC ceramic substrate market is significantly propelled by several key drivers, primarily the escalating demand for advanced power electronics across critical industries. The rapid expansion of the electric vehicle (EV) and hybrid electric vehicle (HEV) markets stands out as a paramount driver, as these vehicles heavily rely on efficient power modules for inverters, converters, and battery management systems. DBC substrates provide the necessary thermal management capabilities to handle the high power densities and temperatures generated by these applications, ensuring performance and longevity. Additionally, the global push towards renewable energy sources, such as solar and wind power, creates a substantial need for power converters that utilize DBC substrates to efficiently manage energy flow.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) | +2.5% | Global, particularly China, Europe, North America | Short-to-Mid Term (2025-2029) |

| Increasing Demand for High-Power Electronic Modules | +2.0% | Global | Short-to-Mid Term (2025-2030) |

| Expansion of Renewable Energy Infrastructure (Solar, Wind) | +1.5% | APAC, Europe, North America | Mid-to-Long Term (2027-2033) |

| Adoption of Wide Bandgap (WBG) Semiconductors (SiC, GaN) | +1.0% | Global | Mid-to-Long Term (2028-2033) |

DBC Ceramic Substrate Market Restraints Analysis

Despite its significant growth prospects, the DBC ceramic substrate market faces certain restraints that could impact its expansion. A primary limiting factor is the relatively high manufacturing cost associated with DBC technology, particularly when compared to alternative substrate solutions like insulated metal substrates (IMS) or thick film ceramics. The complex fabrication processes involving high temperatures and specialized materials contribute to this higher cost, which can be a deterrent for cost-sensitive applications. Furthermore, the inherent brittleness of ceramic materials poses handling and processing challenges, increasing the risk of breakage during manufacturing and assembly, which can lead to higher scrap rates and further drive up production expenses.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost and Complex Fabrication Processes | -1.2% | Global | Short-to-Mid Term (2025-2030) |

| Material Brittleness and Handling Challenges | -0.8% | Global | Short-to-Mid Term (2025-2029) |

| Competition from Alternative Substrate Technologies (e.g., AMB, IMS) | -0.5% | Global | Mid-to-Long Term (2028-2033) |

DBC Ceramic Substrate Market Opportunities Analysis

The DBC ceramic substrate market presents several compelling opportunities for growth and innovation. One significant opportunity lies in the continuous advancement of material science and manufacturing techniques. Innovations in ceramic compositions, such as enhanced Silicon Nitride (Si3N4) and composite materials, are enabling the development of DBC substrates with even greater thermal conductivity, mechanical strength, and reliability, thereby expanding their utility in more demanding environments. Furthermore, the burgeoning demand for specialized and customized high-performance solutions across niche applications, including aerospace, defense, and high-frequency telecommunications (5G infrastructure), opens up new revenue streams for manufacturers capable of offering tailored products. The development of new bonding technologies and multi-layer DBC structures also presents avenues for product differentiation and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Materials and Manufacturing Techniques | +1.8% | Global | Mid-to-Long Term (2028-2033) |

| Emerging Applications in 5G Telecommunications and Aerospace | +1.5% | North America, APAC, Europe | Mid-to-Long Term (2027-2033) |

| Growing Demand for Customized and High-Performance Solutions | +1.0% | Europe, North America, Japan | Short-to-Mid Term (2025-2029) |

DBC Ceramic Substrate Market Challenges Impact Analysis

The DBC ceramic substrate market faces several notable challenges that can impede its growth and operational efficiency. One significant challenge pertains to supply chain vulnerabilities and geopolitical risks. The reliance on specific raw materials, such as high-purity ceramics and copper, often sourced from a limited number of regions, makes the supply chain susceptible to disruptions caused by geopolitical tensions, trade disputes, or natural disasters. Such disruptions can lead to material shortages, price volatility, and extended lead times, directly impacting production schedules and profitability. Furthermore, the stringent quality and reliability requirements for power electronics, especially in critical applications like automotive and medical, present a continuous challenge. Ensuring consistent product quality and meeting rigorous industry standards necessitates significant investment in advanced manufacturing processes, quality control measures, and testing protocols.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.9% | Global | Short-to-Mid Term (2025-2030) |

| Stringent Quality and Reliability Requirements | -0.7% | Global | Ongoing |

| Competition from Alternative Cooling and Packaging Technologies | -0.4% | Global | Mid-to-Long Term (2028-2033) |

DBC Ceramic Substrate Market - Updated Report Scope

This comprehensive report offers an in-depth analysis of the global DBC ceramic substrate market, encompassing market size estimations, growth forecasts, key trends, drivers, restraints, and opportunities. It provides a detailed segmentation analysis by material type, application, and end-use industry, alongside a thorough regional assessment. The report also profiles leading market players, offering insights into their strategic initiatives and competitive landscape. The objective is to provide stakeholders with actionable intelligence to navigate market dynamics and identify lucrative investment opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 920 Million |

| Growth Rate | 9.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kyocera Corporation, Heraeus Holding GmbH, Rogers Corporation, Laird (A DuPont Business), Mitsubishi Materials Corporation, Resonac Corporation, Denka Company Limited, Sumitomo Electric Industries, Ltd., CeramTec GmbH, KCC Corporation, Ningbo Cixing Co., Ltd., Suzhou Hualian Electronic Co., Ltd., Advanced Ceramic Technology (ACT), Remtec, Inc., Diehl Metall Stiftung & Co. KG, Xiamen Xindeco Ltd., Beijing BDStar Navigation Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The DBC ceramic substrate market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market landscape. These segments are primarily defined by the type of ceramic material utilized, the specific application areas where DBC substrates are deployed, and the various end-use industries that integrate these critical components into their products and systems. This comprehensive segmentation allows for a detailed analysis of market dynamics, growth drivers, and evolving trends within each category, offering precise insights for strategic planning and investment decisions.

- By Material: This segment includes different types of ceramic materials used for DBC substrates, each offering distinct thermal and mechanical properties.

- Alumina (Al2O3): Traditional and cost-effective, widely used.

- Aluminum Nitride (AlN): Offers superior thermal conductivity compared to alumina, suitable for high-power applications.

- Silicon Nitride (Si3N4): Provides excellent mechanical strength and thermal shock resistance, ideal for automotive and industrial power modules.

- Zirconia (ZrO2): Known for its high fracture toughness.

- Others: Including other advanced ceramics or composite materials.

- By Application: This segmentation focuses on the specific electronic devices and systems where DBC substrates are integrated due to their high thermal dissipation and electrical isolation capabilities.

- Power Modules: Essential for inverters, converters, and rectifiers in various high-power systems.

- LED Lighting: For efficient thermal management in high-brightness LED arrays.

- Automotive Electronics: Including power control units for EVs/HEVs, engine management, and braking systems.

- Industrial Electronics: Used in motor drives, welding equipment, and industrial power supplies.

- Consumer Electronics: Less common, but growing in high-power consumer devices.

- Renewable Energy Systems: Such as solar inverters and wind turbine converters.

- Medical Devices: For high-reliability power applications in medical equipment.

- Aerospace and Defense: In radar systems, power supplies, and control modules requiring extreme reliability.

- Others: Niche applications requiring specific thermal or electrical properties.

- By End-Use Industry: This segment categorizes the market based on the primary industry sectors that are significant consumers of DBC ceramic substrates, reflecting their strategic importance across various economic domains.

- Automotive: The largest and fastest-growing segment, driven by EV/HEV adoption.

- Industrial: Powering heavy machinery, automation, and industrial control systems.

- Consumer Electronics: For higher-power charging and power management units.

- Energy: Critical for renewable energy generation, transmission, and storage.

- Medical: Used in high-reliability diagnostic and therapeutic equipment.

- Telecommunications: Supporting 5G base stations and power infrastructure.

- Aerospace and Defense: For high-performance and robust electronic systems.

Regional Highlights

- Asia Pacific (APAC): APAC is anticipated to dominate the DBC ceramic substrate market throughout the forecast period. This region benefits from a robust manufacturing base, particularly in China, Japan, South Korea, and Taiwan, which are leading producers of power electronics, automotive components, and consumer electronics. Rapid industrialization, increasing investments in renewable energy infrastructure, and the surging production and adoption of electric vehicles further bolster the market growth in this region. Countries like China are also at the forefront of adopting advanced power modules in their expanding industrial and automotive sectors.

- Europe: Europe represents a significant market for DBC ceramic substrates, characterized by a strong emphasis on high-performance industrial applications, automotive innovation, and renewable energy initiatives. Germany, France, and the UK are key contributors, driven by stringent energy efficiency regulations and a proactive approach towards e-mobility. The region's focus on advanced manufacturing and research and development in power electronics continues to fuel demand for reliable and thermally efficient DBC solutions, particularly those utilizing silicon nitride for enhanced durability.

- North America: North America exhibits substantial growth in the DBC ceramic substrate market, largely due to strong demand from the electric vehicle sector, aerospace and defense industries, and the expansion of data centers requiring high-power solutions. The presence of key technology innovators and the continuous investment in advanced power management systems drive the adoption of high-performance DBC substrates. The region also benefits from increasing government support for clean energy initiatives and electric vehicle infrastructure development.

- Latin America, Middle East, and Africa (MEA): While smaller in market share compared to the developed regions, Latin America, the Middle East, and Africa are emerging markets with growing potential. Increasing industrialization, infrastructure development, and nascent adoption of electric vehicles and renewable energy projects are expected to drive demand for DBC substrates in these regions. However, market growth may be slower due to developing technological infrastructure and varying economic conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the DBC Ceramic Substrate Market.- Kyocera Corporation

- Heraeus Holding GmbH

- Rogers Corporation

- Laird (A DuPont Business)

- Mitsubishi Materials Corporation

- Resonac Corporation (formerly Showa Denko Materials)

- Denka Company Limited

- Sumitomo Electric Industries, Ltd.

- CeramTec GmbH (includes Curamik)

- KCC Corporation

- Ningbo Cixing Co., Ltd.

- Suzhou Hualian Electronic Co., Ltd.

- Advanced Ceramic Technology (ACT)

- Remtec, Inc.

- Diehl Metall Stiftung & Co. KG

- Xiamen Xindeco Ltd.

- Beijing BDStar Navigation Co., Ltd.

Frequently Asked Questions

What are DBC ceramic substrates primarily used for?

DBC (Direct Bonded Copper) ceramic substrates are primarily used in high-power electronic applications that require superior thermal management and electrical isolation. Their main applications include power modules for electric vehicles (EVs), renewable energy systems (solar inverters, wind turbines), industrial motor drives, and advanced LED lighting, where they efficiently dissipate heat generated by semiconductor devices.

Why are DBC substrates preferred over other substrate technologies in certain applications?

DBC substrates are preferred due to their excellent thermal conductivity, high electrical insulation, and robust mechanical strength. They offer superior heat dissipation capabilities compared to conventional PCBs or insulated metal substrates (IMS), crucial for high-power density applications. Furthermore, the direct bonding process ensures a strong, reliable interface between copper and ceramic, enhancing overall module longevity and performance under harsh operating conditions.

What materials are commonly used in DBC ceramic substrates?

The most common ceramic materials used for DBC substrates are Alumina (Al2O3), Aluminum Nitride (AlN), and Silicon Nitride (Si3N4). Alumina is widely used due to its cost-effectiveness and good performance. Aluminum Nitride offers higher thermal conductivity, suitable for very high-power applications. Silicon Nitride provides exceptional mechanical strength and thermal shock resistance, making it ideal for automotive and industrial power modules subjected to extreme temperature cycles.

How is the DBC ceramic substrate market expected to grow in the coming years?

The DBC ceramic substrate market is projected to experience robust growth, driven by the escalating demand for power electronics, especially from the electric vehicle and renewable energy sectors. Advances in material science and the increasing adoption of wide bandgap semiconductors (SiC, GaN) are also contributing significantly to this expansion. The market is forecast to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, reaching USD 920 Million by 2033.

What are the main challenges faced by the DBC ceramic substrate market?

Key challenges for the DBC ceramic substrate market include the relatively high manufacturing cost and complex fabrication processes compared to alternative solutions. Additionally, the inherent brittleness of ceramic materials presents handling and processing challenges, increasing the risk of breakage. Supply chain vulnerabilities and stringent quality control requirements for critical applications also pose significant hurdles for manufacturers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted