Investment Casting Market

Investment Casting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706090 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

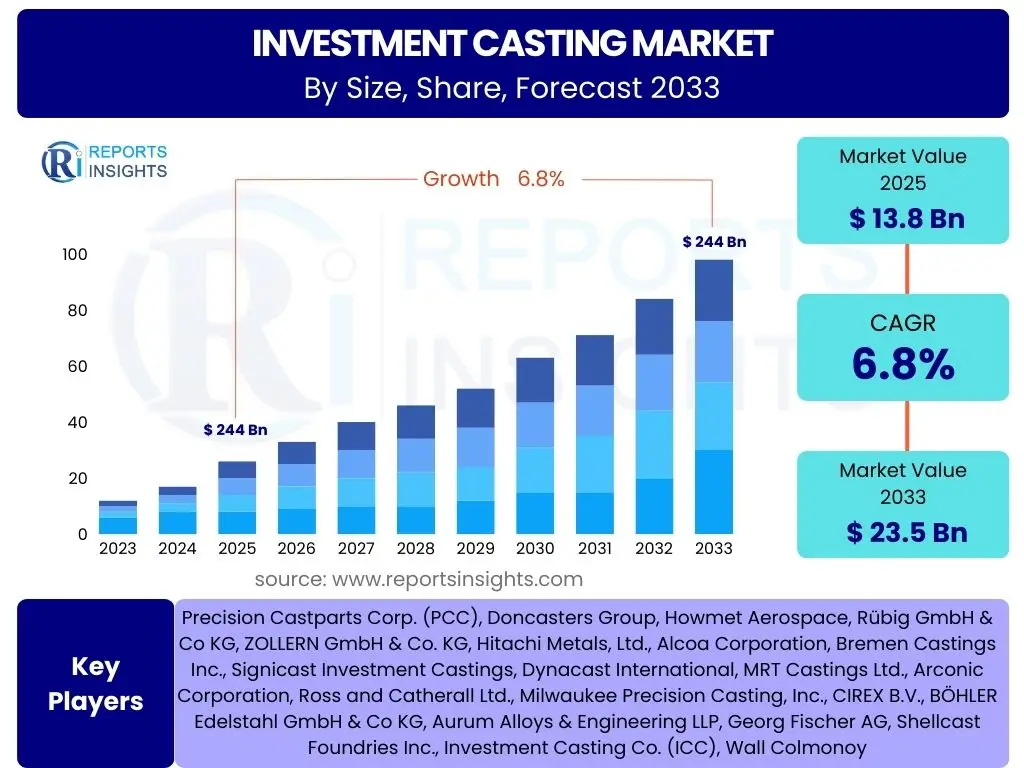

Investment Casting Market Size

According to Reports Insights Consulting Pvt Ltd, The Investment Casting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 13.8 Billion in 2025 and is projected to reach USD 23.5 Billion by the end of the forecast period in 2033.

Key Investment Casting Market Trends & Insights

User queries regarding the Investment Casting market frequently highlight the adoption of advanced manufacturing technologies, the increasing focus on sustainable practices, and the evolving material landscape. Stakeholders are particularly interested in how automation and digitalization are transforming traditional casting processes, leading to improved efficiency and reduced waste. Furthermore, the push for lightweight and high-performance components across various industries is driving innovation in alloy development and process refinement. The market is also witnessing a trend towards supply chain localization and resilience, influenced by geopolitical factors and a desire for greater control over production.

The industry is experiencing a significant shift towards integrating digital tools such as simulation software and IoT for real-time process monitoring and optimization. This digital transformation aims to enhance precision, reduce lead times, and facilitate complex design geometries. Concurrently, there is a growing emphasis on green manufacturing, with companies exploring more energy-efficient processes and recyclable materials to meet environmental regulations and corporate sustainability goals. The demand for near-net-shape components continues to rise, minimizing post-casting machining and material waste, which is a key driver for the adoption of investment casting.

- Advanced Automation and Robotics Integration: Enhancing precision and efficiency in wax pattern assembly, shelling, and pouring.

- Digitalization and Industry 4.0 Adoption: Leveraging IoT, AI, and data analytics for process monitoring, predictive maintenance, and quality control.

- Development of High-Performance Alloys: Focus on superalloys, titanium, and advanced steels for demanding applications in aerospace, energy, and medical sectors.

- Sustainable Manufacturing Practices: Emphasis on energy efficiency, waste reduction, and material recycling to lower environmental impact.

- Near-Net Shape Manufacturing: Driving demand for investment casting due to reduced material waste and post-processing requirements.

- Supply Chain Resilience: Shifting towards regionalized supply chains to mitigate geopolitical risks and ensure consistent material flow.

- Hybrid Manufacturing Approaches: Combining investment casting with additive manufacturing for complex geometries and faster prototyping.

AI Impact Analysis on Investment Casting

Common user questions regarding AI's impact on Investment Casting revolve around its potential to optimize production processes, improve quality control, and enhance material design. Users are keen to understand how AI can reduce defects, predict equipment failures, and streamline complex manufacturing workflows. There is also significant interest in AI's role in accelerating the design and development of new alloys and intricate component geometries, pushing the boundaries of traditional casting capabilities. Concerns often include the initial investment cost, data security, and the need for a skilled workforce capable of implementing and managing AI-driven systems.

AI's influence extends across the entire investment casting value chain, from initial design and simulation to post-production quality assurance. Machine learning algorithms can analyze vast datasets from past production runs to identify patterns indicative of defects, allowing for proactive adjustments and significantly improving yield rates. Furthermore, AI-powered predictive maintenance systems can monitor equipment performance in real-time, forecasting potential breakdowns and scheduling maintenance before costly failures occur. This not only minimizes downtime but also extends the operational life of machinery, contributing to overall operational efficiency and cost savings for foundries.

Beyond operational improvements, AI is revolutionizing design and material science within investment casting. Generative design tools, fueled by AI, can explore a multitude of design iterations that optimize part performance, reduce weight, and simplify manufacturing processes, often achieving geometries impossible with conventional design methods. This capability is particularly valuable for complex components in aerospace and medical industries. AI also aids in the discovery and formulation of novel alloys, predicting material properties based on chemical compositions and processing parameters, thereby accelerating R&D cycles and fostering innovation in high-performance materials.

- Predictive Maintenance: AI algorithms analyze sensor data from casting equipment to predict failures, minimizing downtime and maintenance costs.

- Quality Control and Defect Detection: Machine learning models identify anomalies and defects in real-time, improving yield rates and reducing scrap.

- Process Optimization: AI-driven systems optimize casting parameters (temperature, pressure, pour rate) for enhanced efficiency and consistency.

- Generative Design and Simulation: AI assists in designing complex geometries and simulating casting processes, reducing prototyping cycles.

- Supply Chain Optimization: AI enhances inventory management, demand forecasting, and logistics, ensuring timely material availability.

- Material Development: AI accelerates the discovery and optimization of new alloys by predicting properties based on composition.

- Workforce Augmentation: AI tools empower operators with real-time insights for informed decision-making and operational improvements.

Key Takeaways Investment Casting Market Size & Forecast

User inquiries about key takeaways from the Investment Casting market size and forecast consistently highlight the market's robust growth trajectory and its resilience driven by demanding applications. The insights gleaned suggest a steady expansion, primarily fueled by the aerospace and defense sector's continuous need for lightweight, high-strength components and the automotive industry's push for efficiency and lower emissions through advanced materials. The forecast indicates significant opportunities in emerging economies and through technological advancements that enhance precision and cost-effectiveness.

A critical takeaway is the market's increasing reliance on technological innovation to sustain growth. This includes the integration of automation, digitalization, and advanced material science. Investment casting's ability to produce complex, near-net-shape parts with excellent surface finish and dimensional accuracy continues to be a core competitive advantage. Furthermore, the market is set to benefit from the growing adoption of renewable energy technologies and medical device advancements, both of which require high-precision metal components. The emphasis on sustainability and circular economy principles is also shaping market strategies, influencing material choices and process optimizations.

- Consistent Growth Trajectory: Market poised for steady expansion driven by high-performance component demand.

- Aerospace & Defense Dominance: Continued strong demand from this sector for mission-critical, lightweight parts.

- Automotive Lightweighting Initiatives: Significant market pull from the automotive industry for fuel efficiency and emissions reduction.

- Technological Adoption: Increasing integration of Industry 4.0, automation, and AI for process improvement.

- Emerging Market Opportunities: Untapped potential in developing regions due to industrialization and infrastructure growth.

- Focus on Advanced Materials: Rising demand for superalloys, titanium, and special steels for specialized applications.

- Sustainability as a Driver: Growing emphasis on eco-friendly processes and material efficiency influencing market direction.

Investment Casting Market Drivers Analysis

The Investment Casting Market is significantly propelled by the escalating demand for high-performance and lightweight components across several critical industries. The aerospace and defense sector, in particular, drives substantial growth due to its stringent requirements for parts that can withstand extreme temperatures, pressures, and corrosive environments while maintaining structural integrity and minimal weight. This constant innovation in aircraft engines, structural components, and defense systems necessitates the precision, complex geometries, and superior material properties achievable through investment casting. The push for fuel efficiency and reduced emissions in both commercial aviation and military applications directly translates into a higher demand for advanced, cast components.

Furthermore, the automotive industry's relentless pursuit of vehicle lightweighting and improved fuel economy is a major catalyst for the investment casting market. As manufacturers strive to meet stricter environmental regulations and consumer demands for efficient vehicles, they increasingly turn to investment cast components made from advanced aluminum, steel, and titanium alloys. These components, including turbocharger parts, transmission components, and engine blocks, offer superior strength-to-weight ratios and design flexibility compared to parts produced by other manufacturing methods. The general industrial sector, including industrial machinery, power generation, and oil & gas, also contributes significantly, requiring durable and precise components for various applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Aerospace & Defense | +1.8% | North America, Europe, Asia Pacific (China, India) | Long-term (2025-2033) |

| Automotive Industry Lightweighting Initiatives | +1.5% | Europe, North America, Asia Pacific (Japan, South Korea, China) | Medium-term (2025-2030) |

| Technological Advancements & Automation | +1.2% | Global | Long-term (2025-2033) |

| Growth in Medical and Healthcare Sector | +0.8% | North America, Europe | Medium-term (2025-2030) |

Investment Casting Market Restraints Analysis

Despite its significant advantages, the Investment Casting Market faces notable restraints that can impede its growth. One primary challenge is the high initial capital investment required for establishing and operating an investment casting foundry. The specialized equipment, intricate tooling, and advanced technology necessary for this precision manufacturing process demand substantial financial outlay, making it difficult for new entrants and potentially limiting expansion for existing players. This capital intensiveness often leads to higher per-unit costs compared to less precise casting methods, particularly for high-volume, less complex components, which can sometimes deter potential customers looking for more budget-friendly solutions.

Furthermore, the market is sensitive to the volatility of raw material prices, particularly for critical metals like nickel, cobalt, and titanium, which are essential for producing high-performance alloys. Fluctuations in these commodity prices can directly impact production costs and profit margins for investment casting manufacturers, making long-term financial planning challenging. Environmental regulations, particularly concerning energy consumption, waste management, and emissions, also pose a significant restraint. Compliance with increasingly stringent environmental standards requires continuous investment in cleaner technologies and sustainable practices, adding to operational expenses and potentially slowing down production processes in some regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.9% | Global, particularly emerging economies | Long-term (2025-2033) |

| Raw Material Price Volatility | -0.7% | Global | Short to Medium-term (2025-2028) |

| Stringent Environmental Regulations | -0.5% | Europe, North America, parts of Asia Pacific | Long-term (2025-2033) |

| Competition from Alternative Manufacturing Processes | -0.4% | Global | Long-term (2025-2033) |

Investment Casting Market Opportunities Analysis

Significant opportunities exist within the Investment Casting Market, primarily driven by the expanding adoption of advanced manufacturing technologies and the demand for increasingly specialized components. The integration of additive manufacturing, specifically 3D printing, with traditional investment casting processes offers a lucrative avenue. This hybrid approach allows for the rapid production of complex wax patterns or ceramic molds, significantly reducing lead times and tooling costs for prototyping and small-batch production. It also enables the creation of geometries previously impossible with conventional methods, opening doors to new product designs and applications across various industries, from medical implants to intricate aerospace components.

Moreover, the growing demand for renewable energy infrastructure, particularly wind turbines and hydropower components, presents a substantial opportunity. These sectors require highly durable, precise, and corrosion-resistant parts that can withstand harsh operating conditions, making investment casting an ideal manufacturing method. As global efforts to transition to cleaner energy sources intensify, the need for these specialized cast components will continue to rise. Additionally, the continuous innovation in the medical devices sector, demanding biocompatible and highly precise implants and surgical instruments, further broadens the scope for investment casting applications. The ability to produce intricate, sterile, and custom components efficiently positions investment casting favorably in this expanding market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Additive Manufacturing (3D Printing) | +1.1% | Global | Medium to Long-term (2026-2033) |

| Growth in Renewable Energy Sector | +0.9% | Europe, Asia Pacific (China, India), North America | Long-term (2025-2033) |

| Expansion in Medical Device Manufacturing | +0.7% | North America, Europe | Medium-term (2025-2030) |

| Untapped Markets in Developing Economies | +0.6% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

Investment Casting Market Challenges Impact Analysis

The Investment Casting Market is confronted with several significant challenges that necessitate strategic responses from manufacturers. One pressing issue is the intense competition from alternative manufacturing processes, such as forging, sand casting, and increasingly, direct additive manufacturing. While investment casting offers unparalleled precision and complexity, other methods may be more cost-effective for simpler geometries or higher volume production, forcing investment casting foundries to constantly innovate and emphasize their unique value proposition. Maintaining cost competitiveness while upholding stringent quality standards is a continuous balancing act in a market where customers often seek optimal performance at the lowest possible price.

Another substantial challenge is the increasing complexity of supply chains, exacerbated by global geopolitical tensions, trade disputes, and unforeseen events like pandemics. Disruptions in the supply of critical raw materials, such as specific metal alloys or ceramic binders, can lead to production delays and increased costs. Furthermore, the industry faces a persistent shortage of skilled labor, from experienced mold makers and metallurgists to highly trained machine operators. The specialized nature of investment casting requires a workforce with specific expertise, and the aging workforce combined with a lack of new talent entering the field poses a significant bottleneck for growth and operational efficiency, often leading to higher labor costs and recruitment challenges.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Alternative Manufacturing | -0.8% | Global | Long-term (2025-2033) |

| Skilled Labor Shortage | -0.6% | North America, Europe | Long-term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Risks | -0.5% | Global | Short to Medium-term (2025-2029) |

| Fluctuating Energy Costs | -0.4% | Global | Short to Medium-term (2025-2028) |

Investment Casting Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Investment Casting Market, covering market size estimations, historical data, and future growth projections up to 2033. It offers detailed segmentation analysis by material, end-use industry, and process, alongside a thorough regional breakdown. The scope includes an examination of key market trends, drivers, restraints, opportunities, and challenges influencing the industry's trajectory. Furthermore, the report highlights the impact of AI on investment casting processes and identifies the leading market players, providing a holistic view of the competitive landscape and strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.8 Billion |

| Market Forecast in 2033 | USD 23.5 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Precision Castparts Corp. (PCC), Doncasters Group, Howmet Aerospace, Rübig GmbH & Co KG, ZOLLERN GmbH & Co. KG, Hitachi Metals, Ltd., Alcoa Corporation, Bremen Castings Inc., Signicast Investment Castings, Dynacast International, MRT Castings Ltd., Arconic Corporation, Ross and Catherall Ltd., Milwaukee Precision Casting, Inc., CIREX B.V., BÖHLER Edelstahl GmbH & Co KG, Aurum Alloys & Engineering LLP, Georg Fischer AG, Shellcast Foundries Inc., Investment Casting Co. (ICC), Wall Colmonoy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Investment Casting Market is meticulously segmented across various parameters to provide a granular understanding of its dynamics and opportunities. This comprehensive segmentation allows for a detailed examination of market performance based on the type of materials utilized, the diverse end-use industries that rely on investment casting, and the specific process stages involved in manufacturing. Understanding these segments is crucial for identifying growth pockets, assessing competitive landscapes, and formulating targeted business strategies within the intricate investment casting ecosystem.

The material segmentation highlights the dominance of superalloys and steel alloys due to their superior properties required in high-stress applications, while aluminum and titanium alloys are gaining traction for lightweighting initiatives. The end-use industry breakdown underscores the critical dependence on aerospace & defense and automotive sectors, with emerging contributions from medical and industrial gas turbines. Furthermore, the process segmentation details the various intricate stages of investment casting, from the initial wax pattern creation to the final finishing, providing insights into technological advancements and operational efficiencies at each step.

- By Material:

- Superalloys: Highly resistant to high temperatures and corrosion, critical for aerospace and industrial gas turbines.

- Aluminum Alloys: Preferred for lightweighting in automotive and general industrial applications.

- Steel Alloys: Widely used for strength and versatility across various industrial sectors.

- Titanium Alloys: Essential for high-strength, low-weight components in aerospace and medical implants.

- Others: Includes copper-based alloys, precious metals, and specialized composites for niche applications.

- By End-Use Industry:

- Aerospace & Defense: Largest segment, demanding high-performance engine parts and structural components.

- Automotive: Growing demand for lightweight and complex engine, transmission, and chassis components.

- Medical: Critical for surgical instruments, orthopedic implants, and dental prosthetics requiring high precision and biocompatibility.

- Industrial Gas Turbines (IGT): Key for hot section components requiring extreme temperature resistance.

- General Industrial: Diverse applications including industrial machinery, pumps, valves, and fluid power components.

- Others: Includes marine, consumer goods, oil & gas, and renewable energy sectors.

- By Process:

- Wax Pattern: Involves injecting wax into a die to create an exact replica of the desired part.

- Ceramic Shell: Building layers of ceramic material around the wax pattern to form a mold.

- Melting & Pouring: Melting selected alloys and pouring molten metal into the preheated ceramic shell.

- Finishing: Post-casting processes including cutting, grinding, heat treatment, and surface finishing.

Regional Highlights

- North America: This region is a dominant force in the Investment Casting Market, primarily driven by its robust aerospace and defense sectors. The United States, in particular, has a strong manufacturing base for aircraft components, military hardware, and sophisticated industrial machinery, all of which heavily rely on investment casting for complex, high-performance parts. The region also benefits from significant research and development investments in advanced materials and manufacturing technologies, fostering innovation and adoption of new casting techniques. Demand from the medical device industry for precision implants and surgical tools further contributes to regional market growth.

- Europe: Europe represents a mature and technologically advanced market for investment casting, with a significant presence in the automotive, industrial machinery, and power generation sectors. Countries like Germany, the UK, and France are at the forefront of adopting automation and Industry 4.0 principles in their foundries, leading to enhanced efficiency and product quality. The region's stringent environmental regulations also push for more sustainable casting processes, driving innovation in energy-efficient technologies and waste reduction. Furthermore, the European aerospace industry remains a crucial consumer of investment cast components for both commercial and military aircraft.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate in the Investment Casting Market, fueled by rapid industrialization, burgeoning automotive production, and increasing investments in defense and infrastructure development, particularly in China and India. The growing manufacturing capabilities and expanding middle class in these countries are driving demand for various industrial and consumer goods that utilize cast components. While cost-effectiveness remains a key factor, there is a growing emphasis on quality and precision, leading to the adoption of advanced casting technologies. The region's expanding aerospace and medical sectors also contribute significantly to market expansion.

- Latin America: The Investment Casting Market in Latin America is characterized by emerging industrial growth and increasing foreign investments in manufacturing and infrastructure. Brazil and Mexico are key players in this region, with growing automotive production and expanding general industrial sectors contributing to the demand for cast components. While the market is still developing compared to other regions, there is a steady increase in the adoption of advanced manufacturing techniques to enhance competitiveness and meet international quality standards. The energy sector, particularly oil and gas, also provides consistent demand for durable casting solutions.

- Middle East and Africa (MEA): The MEA region's Investment Casting Market is primarily influenced by investments in the oil and gas industry, power generation, and emerging aerospace and defense initiatives. Countries in the Middle East are investing heavily in diversifying their economies, leading to the development of new industrial capacities that require sophisticated cast components. The growing infrastructure development projects across the region also create opportunities for general industrial castings. While the market is currently smaller in scale compared to others, significant government spending and strategic partnerships are poised to drive future growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Investment Casting Market.- Precision Castparts Corp. (PCC)

- Doncasters Group

- Howmet Aerospace

- Rübig GmbH & Co KG

- ZOLLERN GmbH & Co. KG

- Hitachi Metals, Ltd.

- Alcoa Corporation

- Bremen Castings Inc.

- Signicast Investment Castings

- Dynacast International

- MRT Castings Ltd.

- Arconic Corporation

- Ross and Catherall Ltd.

- Milwaukee Precision Casting, Inc.

- CIREX B.V.

- BÖHLER Edelstahl GmbH & Co KG

- Aurum Alloys & Engineering LLP

- Georg Fischer AG

- Shellcast Foundries Inc.

- Investment Casting Co. (ICC)

- Wall Colmonoy

Frequently Asked Questions

Analyze common user questions about the Investment Casting market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is investment casting?

Investment casting, also known as lost-wax casting, is a precision casting method capable of producing complex near-net-shape components with excellent surface finish and dimensional accuracy. It involves creating a wax pattern, coating it with a ceramic shell, melting out the wax, and then pouring molten metal into the cavity.

What are the primary advantages of investment casting?

Key advantages include the ability to cast intricate geometries and thin walls, achieve excellent surface finish and tight dimensional tolerances, eliminate or minimize machining operations, and produce parts from a wide range of ferrous and non-ferrous alloys, including high-performance superalloys.

Which industries primarily utilize investment casting?

Investment casting is predominantly used in industries requiring high-precision, high-integrity components, such as aerospace and defense (jet engine parts, structural components), automotive (turbochargers, transmission parts), medical (implants, surgical instruments), industrial gas turbines, and general industrial machinery.

How does sustainability impact the investment casting market?

Sustainability is increasingly driving innovation, with foundries focusing on reducing energy consumption, minimizing waste generation, recycling materials, and adopting cleaner melting technologies. This trend responds to stringent environmental regulations and growing corporate social responsibility, influencing material choices and process optimizations.

What future technologies are influencing investment casting?

Future technologies significantly influencing investment casting include advanced automation and robotics for improved efficiency, the integration of Artificial Intelligence (AI) for process optimization and predictive maintenance, and the adoption of additive manufacturing (3D printing) for rapid prototyping of wax patterns and complex tooling.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted