Industrial Valve in Oil and Gas Market

Industrial Valve in Oil and Gas Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704562 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Industrial Valve in Oil and Gas Market Size

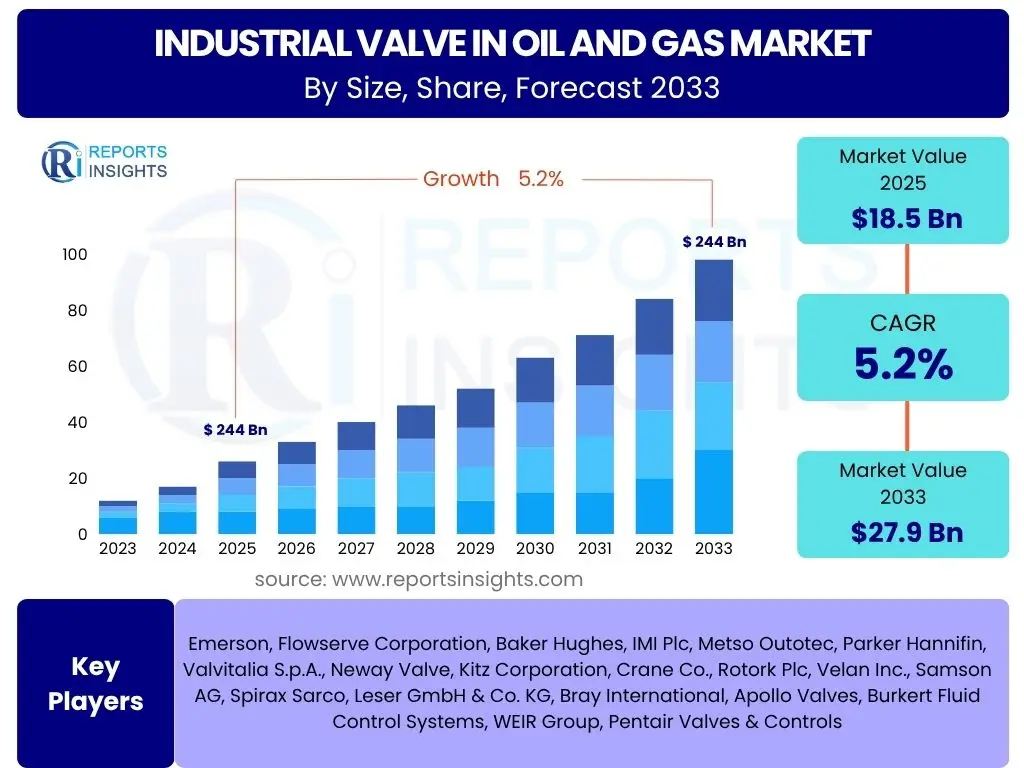

According to Reports Insights Consulting Pvt Ltd, The Industrial Valve in Oil and Gas Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 27.9 Billion by the end of the forecast period in 2033.

Key Industrial Valve in Oil and Gas Market Trends & Insights

User inquiries frequently highlight the increasing adoption of advanced technologies and the industry's evolving response to sustainability mandates as pivotal trends. The drive for operational efficiency and safety, coupled with the need to modernize aging infrastructure, is leading to a significant shift towards intelligent and automated valve systems. Furthermore, market participants are keenly observing the impact of fluctuating energy prices and geopolitical shifts on investment patterns within the oil and gas sector.

A key insight derived from these observations is the growing emphasis on predictive maintenance capabilities and remote monitoring. This technological integration not only enhances operational reliability and reduces downtime but also addresses the demand for more agile and responsive industrial processes. The convergence of digital solutions with traditional valve technology is poised to redefine industry standards and operational paradigms in the coming years.

- Digitalization and Industry 4.0 integration, including IIoT-enabled valves.

- Increased adoption of smart valves for remote monitoring and control.

- Growing focus on predictive maintenance to reduce operational downtime.

- Emphasis on sustainable and emission-reducing valve technologies.

- Development of advanced materials for enhanced durability and performance.

- Modular valve designs for easier installation, maintenance, and scalability.

AI Impact Analysis on Industrial Valve in Oil and Gas

Common user questions regarding AI's influence in the industrial valve domain primarily focus on how artificial intelligence can enhance operational efficiency, predictive capabilities, and safety protocols. Users are keen to understand AI's role in automating complex processes, optimizing asset performance, and deriving actionable insights from vast amounts of operational data. Concerns often revolve around data security, integration challenges, and the need for a skilled workforce capable of managing AI-driven systems.

The core expectation is that AI will revolutionize valve lifecycle management, from design and manufacturing to operation and maintenance. Specifically, AI is anticipated to enable more precise control, facilitate anomaly detection, and allow for a proactive approach to maintenance, thereby minimizing unexpected failures and extending equipment lifespan. This technological evolution promises to deliver significant cost savings and improve overall operational safety in the demanding oil and gas environment.

- Enhanced predictive maintenance capabilities for valves, forecasting potential failures.

- Optimization of valve operation through real-time data analysis and adaptive control.

- Improved safety by autonomously detecting and responding to abnormal conditions.

- Automated inspection and diagnostics, reducing manual intervention.

- Better resource allocation and inventory management for valve components.

- Facilitation of remote and autonomous operations, especially in hazardous environments.

Key Takeaways Industrial Valve in Oil and Gas Market Size & Forecast

User queries about the industrial valve market's size and forecast frequently center on identifying core growth catalysts and understanding market resilience amidst fluctuating global energy dynamics. The market's consistent growth trajectory, despite various economic and geopolitical volatilities, is a central theme. Stakeholders are particularly interested in how technological advancements and evolving regulatory landscapes contribute to this projected expansion, especially in terms of demand for specialized valve types and materials.

A significant takeaway is the dual importance of new infrastructure development and the ongoing need for maintenance, repair, and overhaul (MRO) activities in driving market demand. The forecast indicates that both upstream and midstream segments will be crucial contributors, propelled by global energy consumption trends and the expansion of natural gas and LNG facilities. Additionally, the increasing emphasis on environmental compliance and operational efficiency will continue to steer technological innovation and market direction.

- The market exhibits resilient growth, driven by essential infrastructure development and maintenance needs.

- Technological innovation, particularly in smart and automated valves, is crucial for market expansion.

- Demand for industrial valves is influenced by global energy consumption patterns and geopolitical stability.

- Aging oil and gas infrastructure necessitates significant replacement and upgrade investments.

- The shift towards natural gas and LNG infrastructure is creating new demand avenues for specialized valves.

- Regulatory compliance and safety standards remain paramount, influencing valve design and material selection.

Industrial Valve in Oil and Gas Market Drivers Analysis

The industrial valve market in oil and gas is fundamentally driven by the continuous global demand for energy, which necessitates ongoing exploration, production, and processing activities. This demand fuels investment in new projects and the expansion of existing infrastructure, directly increasing the need for a wide range of industrial valves. Furthermore, the aging nature of much of the world's oil and gas infrastructure requires constant replacement and upgrades, providing a stable base for valve demand even in periods of lower new project activity.

Strict safety and environmental regulations globally also play a pivotal role in driving market growth. These regulations mandate the use of high-integrity, reliable, and often specialized valves to prevent leaks, control emissions, and ensure operational safety, thereby compelling industries to invest in advanced valve technologies. Additionally, the expansion of midstream infrastructure, such as pipelines for crude oil and natural gas, and the proliferation of liquefied natural gas (LNG) terminals, represent significant growth avenues for valve manufacturers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Global Energy Demand | +1.5% | Asia Pacific, Middle East, North America | Long-term (2025-2033) |

| Expansion of Midstream Infrastructure | +1.2% | North America, Europe, Asia Pacific | Mid-term (2026-2030) |

| Replacement of Aging Infrastructure | +1.0% | North America, Europe | Ongoing (2025-2033) |

| Growing Investments in E&P Activities | +0.8% | Middle East, Africa, Latin America | Mid-term (2027-2032) |

| Strict Safety and Environmental Regulations | +0.7% | Global, particularly Europe and North America | Ongoing (2025-2033) |

Industrial Valve in Oil and Gas Market Restraints Analysis

The industrial valve market in oil and gas faces significant restraints, primarily stemming from the inherent volatility of crude oil and natural gas prices. Fluctuations in these commodity prices directly impact investment decisions in new oil and gas projects, leading to project delays or cancellations that reduce demand for new valves. This unpredictability creates an unstable investment environment for both energy companies and their suppliers, including valve manufacturers.

Another prominent restraint is the accelerating global shift towards renewable energy sources and away from fossil fuels. As nations commit to decarbonization targets and invest heavily in solar, wind, and other green technologies, the long-term outlook for new oil and gas developments becomes less certain, potentially capping growth in the industrial valve sector. Additionally, the high capital expenditure required for advanced and specialized valve systems can deter some companies, particularly smaller operators, from upgrading their existing infrastructure, opting instead for less costly maintenance solutions or delayed replacements.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Crude Oil and Natural Gas Prices | -1.3% | Global | Short to Mid-term (2025-2028) |

| Growing Adoption of Renewable Energy Sources | -1.0% | Europe, North America, Asia Pacific | Long-term (2027-2033) |

| High Capital Expenditure for Advanced Valve Systems | -0.8% | Global | Ongoing (2025-2033) |

| Geopolitical Uncertainties and Trade Disputes | -0.6% | Global, particularly Europe, Middle East | Short-term (2025-2027) |

| Environmental Concerns and Project Delays | -0.5% | North America, Europe, Australia | Ongoing (2025-2033) |

Industrial Valve in Oil and Gas Market Opportunities Analysis

Significant opportunities in the industrial valve market for oil and gas are emerging from the ongoing digital transformation within the energy sector. The integration of Industry 4.0 technologies, such as the Industrial Internet of Things (IIoT), AI, and advanced analytics, presents a vast potential for developing smart valves capable of real-time monitoring, predictive maintenance, and autonomous operation. This shift allows valve manufacturers to offer higher-value solutions that enhance operational efficiency and safety, moving beyond traditional product sales.

Furthermore, the increasing focus on unconventional oil and gas resources, including shale gas, tight oil, and deepwater exploration, opens new specialized niches for valve technology. These challenging environments demand valves designed for extreme pressures, temperatures, and corrosive media, driving innovation in material science and engineering. The expansion of liquefied natural gas (LNG) infrastructure, encompassing liquefaction plants, regasification terminals, and export facilities, also represents a substantial growth area, requiring specialized cryogenic and high-performance valves.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation and Industry 4.0 Integration | +1.4% | Global | Long-term (2025-2033) |

| Growth in Unconventional Oil and Gas Resources | +1.1% | North America, Latin America, Asia Pacific | Mid-term (2026-2031) |

| Increasing Demand for Smart and Intelligent Valves | +1.0% | Global | Long-term (2025-2033) |

| Expansion in Liquefied Natural Gas (LNG) Infrastructure | +0.9% | Asia Pacific, North America, Europe | Mid-term (2027-2032) |

| Maintenance, Repair, and Overhaul (MRO) Activities | +0.7% | Global | Ongoing (2025-2033) |

Industrial Valve in Oil and Gas Market Challenges Impact Analysis

The industrial valve market in oil and gas faces several pressing challenges, notably cybersecurity threats to increasingly connected valve systems. As more smart and IIoT-enabled valves are deployed, they become potential entry points for cyberattacks, risking operational disruptions, data breaches, and safety incidents. Ensuring robust cybersecurity measures for these critical infrastructure components is a significant hurdle that requires continuous investment and vigilance from manufacturers and operators alike.

Another substantial challenge is the persistent shortage of skilled labor required for the installation, maintenance, and complex troubleshooting of advanced valve technologies. The aging workforce and a gap in specialized technical training often lead to operational inefficiencies and increased downtime. Moreover, the industry grapples with stringent and evolving regulatory compliance requirements, which necessitate continuous adaptation in valve design, manufacturing processes, and certification, adding complexity and cost to operations. Intense price competition from both domestic and international players further compresses profit margins, forcing companies to innovate while simultaneously managing costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats to Connected Valve Systems | -0.9% | Global | Ongoing (2025-2033) |

| Skilled Labor Shortages | -0.7% | North America, Europe | Long-term (2025-2033) |

| Stringent Regulatory Compliance and Evolving Standards | -0.6% | Global | Ongoing (2025-2033) |

| Intense Price Competition | -0.5% | Asia Pacific, Global | Ongoing (2025-2033) |

| Disruptions in Global Supply Chains | -0.4% | Global | Short to Mid-term (2025-2028) |

Industrial Valve in Oil and Gas Market - Updated Report Scope

This report provides a comprehensive analysis of the Industrial Valve in Oil and Gas Market, encompassing market dynamics, competitive landscape, and future growth projections. It offers an in-depth assessment of market size, trends, drivers, restraints, opportunities, and challenges affecting the industry across various segments and key geographical regions. The scope includes detailed segmentation by valve type, material, end-use industry, application, and operation, alongside a profiling of key market players and their strategic initiatives, ensuring a holistic view of the market's current state and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 27.9 Billion |

| Growth Rate | 5.2% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Emerson, Flowserve Corporation, Baker Hughes, IMI Plc, Metso Outotec, Parker Hannifin, Valvitalia S.p.A., Neway Valve, Kitz Corporation, Crane Co., Rotork Plc, Velan Inc., Samson AG, Spirax Sarco, Leser GmbH & Co. KG, Bray International, Apollo Valves, Burkert Fluid Control Systems, WEIR Group, Pentair Valves & Controls |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial valve market in the oil and gas sector is segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of demand patterns, technological preferences, and regional variations, offering valuable insights for stakeholders. The market's complexity necessitates detailed categorization by valve type, which includes ubiquitous components like ball, gate, and globe valves, alongside specialized control and safety valves crucial for operational integrity and safety.

Further segmentation by material highlights the critical role of material science in valve performance, with distinctions made between various steel alloys, cast iron, and specialized materials like duplex and cryogenic alloys tailored for specific operational environments. End-use industry segmentation divides the market into upstream, midstream, and downstream sectors, each with unique valve requirements and operational challenges. Lastly, segmentation by application (onshore vs. offshore) and operation type (manual, actuated, automatic) provides a comprehensive view of how valves are deployed and managed across the oil and gas value chain.

- By Type: Gate Valve, Globe Valve, Ball Valve, Butterfly Valve, Check Valve, Plug Valve, Control Valve, Safety Relief Valve, Other Valves (e.g., Diaphragm, Needle).

- By Material: Cast Iron, Steel (Carbon Steel, Stainless Steel, Alloy Steel), Cryogenic, Bronze, Duplex, Other Materials.

- By End-Use Industry: Upstream (Exploration & Production), Midstream (Transportation & Storage), Downstream (Refining & Processing).

- By Application: Onshore, Offshore.

- By Operation: Manual, Actuated (Electric, Pneumatic, Hydraulic), Automatic.

Regional Highlights

- North America: This region is a dominant force in the industrial valve in oil and gas market, primarily driven by extensive unconventional oil and gas exploration and production, particularly in shale formations. The robust midstream infrastructure, significant investments in pipeline networks, and the constant need for upgrading aging facilities contribute substantially to market growth. Stringent safety regulations and a strong emphasis on automation further boost the demand for advanced and intelligent valve solutions across the United States and Canada.

- Europe: Characterized by a mature oil and gas industry, Europe's market for industrial valves is largely driven by maintenance, repair, and overhaul (MRO) activities on existing infrastructure, alongside increasing investments in natural gas and LNG terminals to diversify energy sources. The region's stringent environmental regulations and focus on reducing emissions also compel the adoption of high-performance and leak-proof valve technologies, driving innovation in sustainable solutions.

- Asia Pacific (APAC): The APAC region represents the fastest-growing market, propelled by rapidly increasing energy demand from developing economies such as China, India, and Southeast Asian countries. Significant investments in new upstream, midstream, and downstream projects, including large-scale refinery expansions and LNG export terminals, are fueling substantial demand for industrial valves. The region also benefits from growing industrialization and urbanization, leading to new energy infrastructure development.

- Latin America: This region is experiencing growth due to the development of vast offshore oil and gas reserves, particularly in Brazil and Guyana, and the expansion of natural gas infrastructure. Investments in new exploration and production projects, coupled with the modernization of existing facilities, are driving the demand for industrial valves. Economic recovery and government initiatives to boost energy independence also contribute to market expansion.

- Middle East and Africa (MEA): As a primary global hub for oil and gas production, the MEA region continues to be a major market for industrial valves. Large-scale upstream projects, expansion of export terminals, and significant investments in downstream refining and petrochemical capacities are key drivers. The region's long-term energy strategies focusing on maximizing production and diversifying energy exports ensure sustained demand for advanced and reliable valve systems.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Valve in Oil and Gas Market.- Emerson

- Flowserve Corporation

- Baker Hughes

- IMI Plc

- Metso Outotec

- Parker Hannifin

- Valvitalia S.p.A.

- Neway Valve

- Kitz Corporation

- Crane Co.

- Rotork Plc

- Velan Inc.

- Samson AG

- Spirax Sarco

- Leser GmbH & Co. KG

- Bray International

- Apollo Valves

- Burkert Fluid Control Systems

- WEIR Group

- Pentair Valves & Controls

Frequently Asked Questions

What are the primary factors driving the industrial valve market in oil and gas?

The market is primarily driven by increasing global energy demand, significant investments in midstream infrastructure like pipelines and LNG terminals, the crucial need to replace and upgrade aging oil and gas facilities, and stringent safety and environmental regulations demanding high-integrity valve solutions.

How is digitalization impacting the industrial valve sector?

Digitalization is profoundly impacting the sector by enabling smart valves with IIoT connectivity, fostering predictive maintenance capabilities, allowing for remote monitoring and control, and optimizing operational efficiency through real-time data analytics. This leads to reduced downtime and enhanced safety.

What are the key challenges faced by valve manufacturers in the oil and gas industry?

Key challenges include cybersecurity threats to networked valve systems, a persistent shortage of skilled labor for advanced valve technologies, stringent and evolving regulatory compliance requirements, intense price competition from global players, and potential disruptions in global supply chains.

Which regions exhibit the highest growth potential for industrial valves in oil and gas?

The Asia Pacific region shows the highest growth potential due to increasing energy demand and significant investments in new oil and gas infrastructure. North America also maintains strong growth, driven by unconventional resource development and infrastructure modernization.

What types of valves are most commonly used in downstream oil and gas operations?

In downstream operations (refining and processing), common valve types include globe valves for throttling, gate valves for isolation, ball valves for quick shut-off, check valves for backflow prevention, and control valves for automated process regulation. Safety relief valves are also critical for overpressure protection.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted