Inductor Market

Inductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705251 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

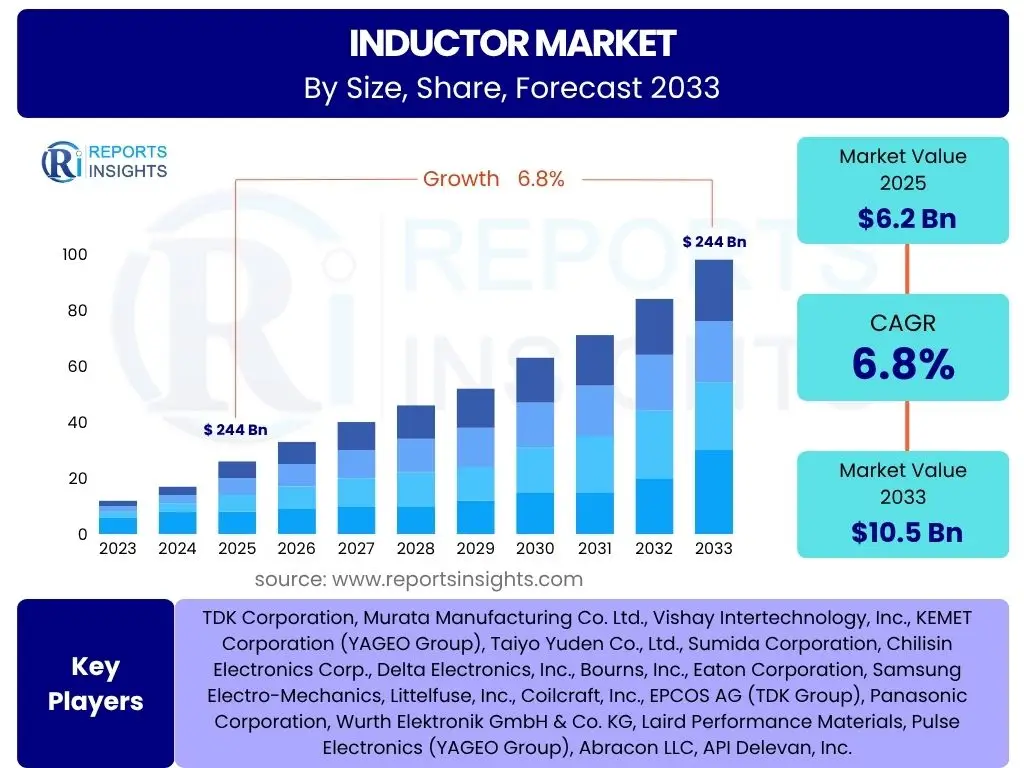

Inductor Market Size

According to Reports Insights Consulting Pvt Ltd, The Inductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 10.5 Billion by the end of the forecast period in 2033.

Key Inductor Market Trends & Insights

The Inductor market is undergoing significant transformations driven by advancements in various electronics sectors. Key trends indicate a strong push towards miniaturization and higher performance, particularly in response to the growing demand for compact and efficient electronic devices. The proliferation of 5G technology, the expansion of the Internet of Things (IoT), and the rapid adoption of electric vehicles (EVs) are major catalysts shaping the industry's trajectory. These applications necessitate inductors that can operate effectively at higher frequencies and temperatures while maintaining excellent power efficiency.

Furthermore, there is a rising focus on the development of specialized inductors for advanced power management systems and high-frequency noise suppression. Manufacturers are investing in new materials and fabrication techniques to meet the stringent requirements of next-generation electronics, including better thermal management and electromagnetic compatibility (EMC). This has led to an increased emphasis on custom inductor designs that cater to specific application needs, moving beyond standard off-the-shelf components. The convergence of these technological demands points to a future where inductors are more integrated, efficient, and robust.

- Miniaturization and compact designs for space-constrained applications.

- Development of high-frequency and high-current inductors.

- Integration of inductors into power modules and System-in-Packages (SiP).

- Adoption of advanced materials (e.g., amorphous metals, ferrites) for improved performance.

- Increased demand for shielded inductors to minimize electromagnetic interference (EMI).

- Focus on energy-efficient designs for reduced power consumption.

- Growing prevalence of automotive-grade inductors for harsh environments.

AI Impact Analysis on Inductor

Artificial intelligence (AI) is set to profoundly influence the Inductor market across its entire value chain, from design and manufacturing to demand generation. In the design phase, AI-powered simulation tools and algorithms can optimize inductor parameters for specific applications, reducing development cycles and improving performance metrics such as efficiency, size, and thermal management. AI can analyze vast datasets of material properties and design variations to identify optimal configurations that human designers might miss. This accelerates innovation and allows for the creation of highly customized components tailored to complex AI hardware requirements, such as those found in neural processing units (NPUs) and high-performance computing (HPC) systems.

From a manufacturing standpoint, AI integration facilitates predictive maintenance of production lines, leading to higher yields and reduced downtime. Machine learning algorithms can detect anomalies in manufacturing processes, ensuring consistent quality and enabling proactive adjustments. This is particularly crucial for complex inductor fabrication processes where precision is paramount. Furthermore, the burgeoning demand for AI-driven devices across sectors like autonomous vehicles, smart homes, and industrial automation directly fuels the need for more sophisticated and reliable inductors. These AI applications require robust power delivery networks and advanced signal filtering, pushing the boundaries of inductor technology and creating new market segments for specialized components.

- AI-driven design optimization leading to more efficient and compact inductors.

- Predictive maintenance and quality control in inductor manufacturing using AI.

- Increased demand for high-performance inductors to support AI processors and hardware.

- Development of specialized inductors for AI at the edge and IoT devices.

- AI accelerating material discovery for next-generation inductor cores.

- Enhanced supply chain management and demand forecasting for inductors through AI analytics.

Key Takeaways Inductor Market Size & Forecast

The Inductor market is poised for robust growth through 2033, driven primarily by the relentless expansion of the electronics industry and the increasing complexity of modern electronic systems. The forecasted market size underscores the critical role inductors play in power management, signal processing, and noise reduction across a multitude of applications. A significant takeaway is the market's resilience, adapting to evolving technological landscapes such as the rollout of 5G, the proliferation of IoT devices, and the surging demand for electric vehicles. These sectors are not just driving volume but also pushing the boundaries of inductor technology, requiring higher performance, smaller footprints, and enhanced reliability.

The growth trajectory also highlights the importance of innovation in materials science and manufacturing processes. As device form factors shrink and power requirements intensify, the ability to produce highly efficient and durable inductors becomes a key competitive differentiator. The market is witnessing a shift towards specialized components designed for specific high-frequency, high-power, or high-temperature applications, indicating a mature yet dynamic market segment. Overall, the market's future is closely tied to the broader trends in digitalization, automation, and energy efficiency, positioning inductors as indispensable components in the global technological infrastructure.

- Market size projected to reach USD 10.5 Billion by 2033, demonstrating substantial growth.

- Consistent CAGR of 6.8% indicates steady expansion driven by electronics proliferation.

- Miniaturization and performance enhancement are central to future market development.

- Key growth drivers include 5G, IoT, electric vehicles, and AI hardware.

- Innovation in materials and manufacturing techniques is crucial for market competitiveness.

- Emerging applications requiring high-frequency and high-power inductors are pivotal.

Inductor Market Drivers Analysis

The global Inductor market is propelled by several robust drivers stemming from the pervasive expansion of electronics across various industries. A primary driver is the rapid proliferation of advanced consumer electronics, including smartphones, wearables, and high-performance computing devices, all of which require sophisticated power management and signal integrity. Furthermore, the global rollout of 5G infrastructure necessitates high-frequency inductors for base stations, mobile devices, and networking equipment, contributing significantly to market demand. The increasing adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) also presents a strong impetus, as inductors are vital components in their power conversion systems, battery management, and onboard charging units.

Beyond consumer and automotive sectors, the industrial and healthcare electronics markets are exhibiting strong growth, demanding specialized inductors for automation systems, medical devices, and power supplies. The expanding Internet of Things (IoT) ecosystem, encompassing smart home devices, industrial IoT, and connected health solutions, fuels the need for compact, efficient, and reliable inductors for their vast array of sensors and communication modules. Lastly, the global focus on renewable energy systems, such as solar inverters and wind power converters, along with the development of smart grid technologies, requires robust power inductors capable of handling high currents and voltages, further bolstering market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Consumer Electronics | +1.2% | Asia Pacific, North America, Europe | 2025-2033 |

| 5G Technology Deployment | +0.9% | Global, particularly Asia Pacific (China, South Korea), North America | 2025-2030 |

| Electric Vehicle (EV) Adoption | +1.1% | Europe, Asia Pacific (China), North America | 2025-2033 |

| Expansion of IoT Devices | +0.8% | Global | 2025-2033 |

| Industrial Automation & Robotics | +0.6% | Asia Pacific, Europe, North America | 2025-2033 |

| Renewable Energy Systems Development | +0.5% | Global | 2025-2033 |

Inductor Market Restraints Analysis

Despite the positive growth outlook, the Inductor market faces several significant restraints that could impede its expansion. One prominent challenge is the volatility and unpredictability of raw material prices, particularly for copper, iron, and various magnetic materials. Fluctuations in these commodity prices directly impact manufacturing costs and can lead to increased product prices, potentially dampening demand or squeezing profit margins for manufacturers. Furthermore, the complex global supply chain for electronic components, exacerbated by geopolitical tensions and unforeseen events like pandemics, poses a constant threat of disruptions, leading to lead time extensions and production delays.

Another key restraint stems from the intense competitive landscape within the inductor market. Numerous players, ranging from large multinational corporations to smaller specialized firms, vie for market share, often leading to pricing pressures and reduced profitability. The demand for ever-smaller and higher-performing inductors also presents technical design challenges. Miniaturization often requires innovative materials and complex manufacturing processes, which can increase research and development costs and production complexities. Additionally, the increasing regulatory scrutiny concerning environmental standards and material sourcing adds another layer of compliance burden for manufacturers, potentially limiting market entry for new players or increasing operational costs for existing ones.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -0.7% | Global | 2025-2033 |

| Supply Chain Disruptions | -0.6% | Global | 2025-2030 |

| Intense Market Competition & Price Pressures | -0.5% | Global | 2025-2033 |

| Design Complexity for High-Frequency/Power | -0.4% | Global | 2025-2033 |

| Increasing Regulatory Compliance | -0.3% | Europe, North America, Asia Pacific | 2025-2033 |

Inductor Market Opportunities Analysis

Significant opportunities exist within the Inductor market, driven by emerging technologies and evolving industry needs. The burgeoning market for high-frequency applications, particularly in advanced communication systems such as satellite internet (LEO constellations), mmWave 5G, and high-speed data centers, creates a strong demand for inductors capable of operating efficiently at elevated frequencies with minimal loss. The continuous electrification trend in the automotive sector, extending beyond EVs to include ADAS (Advanced Driver-Assistance Systems) and autonomous driving technologies, opens vast avenues for specialized, automotive-grade inductors that can withstand harsh operating conditions and meet stringent reliability standards.

Furthermore, the rapid advancements in medical devices, including portable diagnostics, implantable electronics, and high-resolution imaging systems, represent a niche but high-value opportunity for custom, miniature, and biocompatible inductors. The expansion of industrial IoT (IIoT) and smart factory initiatives also presents growth prospects, as these applications require robust and reliable inductors for power conversion, sensor interfacing, and motor control in demanding industrial environments. Finally, the growing adoption of artificial intelligence and machine learning in edge devices and specialized hardware creates new requirements for compact and highly efficient power inductors to support the computational demands of AI accelerators, presenting a fertile ground for innovation and market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High-Frequency Communication Systems | +1.0% | Global | 2025-2033 |

| Advanced Automotive Electronics (ADAS, Autonomous Driving) | +0.9% | Europe, North America, Asia Pacific | 2025-2033 |

| Miniaturized Medical Devices | +0.7% | North America, Europe | 2025-2033 |

| Industrial IoT (IIoT) & Smart Factories | +0.6% | Asia Pacific, Europe | 2025-2033 |

| AI Hardware Acceleration at the Edge | +0.8% | Global | 2025-2033 |

Inductor Market Challenges Impact Analysis

The Inductor market faces several critical challenges that demand innovative solutions and strategic adjustments from manufacturers. One significant challenge is managing heat dissipation, especially in miniaturized inductors designed for high-power or high-frequency applications. As components shrink, the ability to effectively dissipate heat becomes more complex, potentially leading to performance degradation or device failure. Related to this, electromagnetic interference (EMI) and radio frequency interference (RFI) are persistent concerns. As electronic devices become more densely packed and operate at higher frequencies, the risk of unwanted noise and signal disruption increases, requiring advanced shielding and design techniques for inductors.

Another challenge is maintaining optimal performance across a wide range of operating temperatures. Inductors used in automotive, industrial, and certain consumer applications must withstand extreme thermal variations without compromising their inductance, Q-factor, or saturation characteristics. The integration of inductors into complex integrated circuits and power modules also presents design and manufacturing complexities, requiring seamless collaboration between component suppliers and system designers. Finally, the market is continually battling the proliferation of counterfeit products, which not only pose quality and reliability risks but also erode legitimate manufacturers' revenue and reputation, necessitating robust supply chain verification and protection measures.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management in Miniaturized Inductors | -0.6% | Global | 2025-2033 |

| Electromagnetic Interference (EMI) & RFI Mitigation | -0.5% | Global | 2025-2033 |

| Maintaining Performance in Extreme Temperatures | -0.4% | Automotive, Industrial, Military segments | 2025-2033 |

| Integration Complexities in Advanced Systems | -0.3% | Global | 2025-2033 |

| Combatting Counterfeit Products | -0.2% | Asia Pacific (source), Global (impact) | 2025-2033 |

Inductor Market - Updated Report Scope

This report provides a comprehensive analysis of the global Inductor market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers market size estimations, growth forecasts, and a thorough examination of the drivers, restraints, opportunities, and challenges shaping the industry from 2025 to 2033, with historical data from 2019 to 2023. The scope includes various inductor types, applications, and end-use industries, providing a holistic view for stakeholders seeking strategic market intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 10.5 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TDK Corporation, Murata Manufacturing Co. Ltd., Vishay Intertechnology, Inc., KEMET Corporation (YAGEO Group), Taiyo Yuden Co., Ltd., Sumida Corporation, Chilisin Electronics Corp., Delta Electronics, Inc., Bourns, Inc., Eaton Corporation, Samsung Electro-Mechanics, Littelfuse, Inc., Coilcraft, Inc., EPCOS AG (TDK Group), Panasonic Corporation, Wurth Elektronik GmbH & Co. KG, Laird Performance Materials, Pulse Electronics (YAGEO Group), Abracon LLC, API Delevan, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Inductor market is comprehensively segmented by various criteria to provide a granular understanding of its dynamics and growth drivers. These segments include type, core type, application, and end-use industry, each reflecting distinct technological requirements and market demands. The "By Type" segmentation captures the different manufacturing approaches and physical characteristics of inductors, such as wire-wound for high current applications or multilayer for miniaturization. "By Core Type" categorizes inductors based on their magnetic core material, which significantly impacts performance parameters like inductance, saturation current, and frequency response.

The "By Application" segment delineates the primary functions inductors serve within electronic circuits, ranging from power conversion and filtering to RF applications, highlighting their indispensable role across various system architectures. Lastly, the "By End-Use Industry" segmentation identifies the key sectors driving demand for inductors, illustrating how industries like consumer electronics, automotive, and telecommunications are major consumers. This multi-faceted segmentation allows for a detailed analysis of market trends, technological preferences, and growth opportunities within specific niches of the inductor landscape, providing crucial insights for market participants and strategic planning.

- By Type: Wire-Wound Inductors, Multilayer Inductors, Film Type Inductors, Molded Inductors, Ceramic Inductors, Other Inductor Types.

- By Core Type: Air Core, Ferrite Core, Iron Core, Ceramic Core.

- By Application: Power Converters, EMI/RFI Filtering, RF Chokes, Transformers, Resonators, Oscillators.

- By End-Use Industry: Consumer Electronics, Automotive, Telecommunications, Industrial, Healthcare, Aerospace & Defense, Energy & Power.

Regional Highlights

- Asia Pacific (APAC): Dominates the Inductor market due to its robust manufacturing base for consumer electronics, automotive components, and telecommunication equipment. Countries like China, Japan, South Korea, and Taiwan are major production hubs and significant consumers, driven by high demand for smartphones, 5G infrastructure, and electric vehicles. The region is also at the forefront of AI and IoT adoption, further fueling demand.

- North America: Exhibits strong growth, primarily driven by technological innovation, increasing investment in data centers, electric vehicles, and defense applications. The presence of major automotive OEMs and a thriving semiconductor industry, coupled with significant R&D in high-frequency communications and AI hardware, contributes to the region's market expansion.

- Europe: A significant market influenced by its strong automotive industry (especially EVs and ADAS), industrial automation sector, and advancements in renewable energy technologies. Countries such as Germany, France, and the UK are key contributors, focusing on high-reliability and specialized inductor solutions for demanding applications.

- Latin America: Expected to show steady growth, albeit from a smaller base, driven by increasing smartphone penetration, expanding automotive manufacturing, and developing telecommunications infrastructure, particularly in countries like Brazil and Mexico.

- Middle East and Africa (MEA): Emerging market with growth potential linked to infrastructure development, increasing adoption of consumer electronics, and nascent automotive and industrial sectors. Investments in smart city projects and renewable energy initiatives are also expected to drive demand for inductors in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Inductor Market.- TDK Corporation

- Murata Manufacturing Co. Ltd.

- Vishay Intertechnology, Inc.

- KEMET Corporation (YAGEO Group)

- Taiyo Yuden Co., Ltd.

- Sumida Corporation

- Chilisin Electronics Corp.

- Delta Electronics, Inc.

- Bourns, Inc.

- Eaton Corporation

- Samsung Electro-Mechanics

- Littelfuse, Inc.

- Coilcraft, Inc.

- EPCOS AG (TDK Group)

- Panasonic Corporation

- Wurth Elektronik GmbH & Co. KG

- Laird Performance Materials

- Pulse Electronics (YAGEO Group)

- Abracon LLC

- API Delevan, Inc.

Frequently Asked Questions

What is the projected growth rate of the Inductor Market?

The Inductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated value of USD 10.5 Billion by 2033.

Which factors are primarily driving the Inductor Market's growth?

Key drivers include the rapid expansion of consumer electronics, global deployment of 5G technology, increasing adoption of electric vehicles, proliferation of IoT devices, and advancements in industrial automation and renewable energy systems.

How is AI impacting the Inductor market?

AI influences the Inductor market by enabling advanced design optimization, improving manufacturing efficiency through predictive maintenance, and driving demand for high-performance inductors in AI-powered hardware and edge computing devices.

What are the main challenges faced by the Inductor market?

Major challenges include managing thermal dissipation in miniaturized components, mitigating electromagnetic interference (EMI), ensuring performance in extreme temperatures, navigating complex system integration, and combating counterfeit products.

Which region holds the largest share in the Inductor market?

The Asia Pacific region currently holds the largest share in the Inductor market, driven by its dominant electronics manufacturing industry and high demand from countries like China, Japan, and South Korea.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted