Radiation Detection Market

Radiation Detection Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709933 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

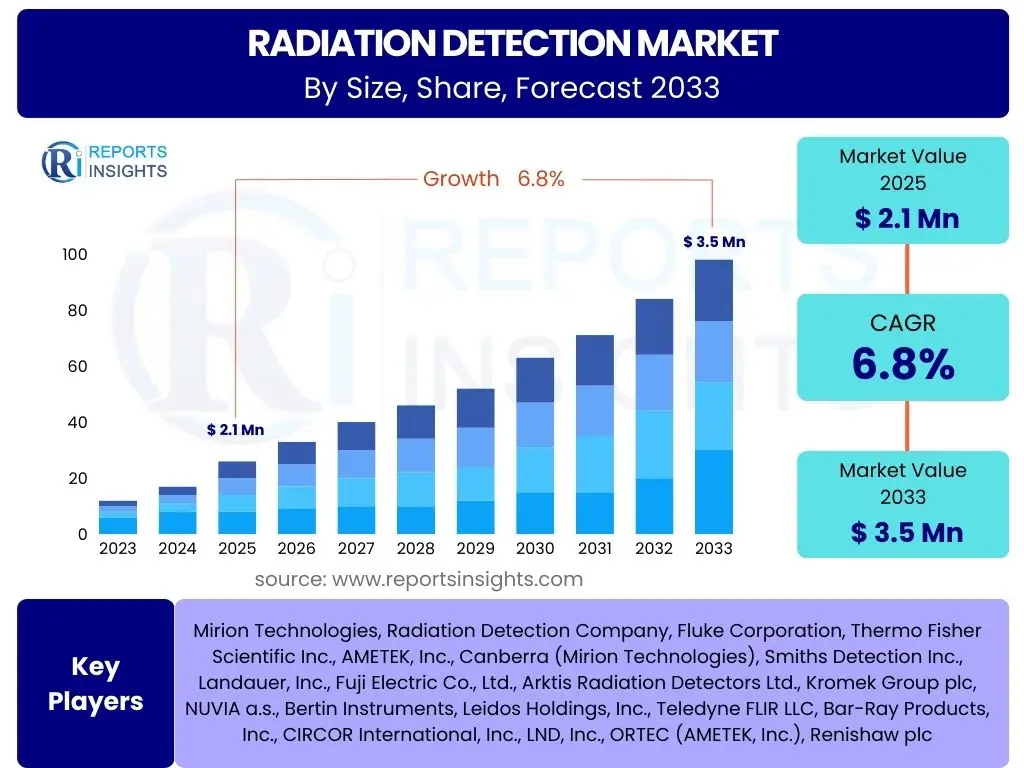

Radiation Detection Market Size

According to Reports Insights Consulting Pvt Ltd, The Radiation Detection Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 3.5 Billion by the end of the forecast period in 2033.

Key Radiation Detection Market Trends & Insights

The radiation detection market is currently experiencing significant technological evolution, driven by the increasing need for advanced monitoring and safety solutions across diverse sectors. Common user questions frequently revolve around the adoption of more sensitive and compact detection systems, the integration of data analytics for predictive capabilities, and the growing demand for personal dosimeters in hazardous environments. Furthermore, there is considerable interest in the development of multi-purpose detectors that can identify various types of radiation, enhancing operational flexibility and efficiency in critical applications such as homeland security and environmental protection. These trends reflect a broader industry shift towards smarter, more integrated, and user-friendly radiation detection technologies, aiming to improve safety standards and operational effectiveness. The market is also seeing a surge in demand for real-time monitoring solutions, propelled by stringent regulatory requirements and the necessity for immediate threat assessment in nuclear facilities and healthcare settings.

Another prominent trend attracting user attention is the miniaturization of radiation detectors, making them suitable for wearable devices and drones, which extends their utility into difficult-to-access or remote areas. This focus on portability and ease of deployment is crucial for first responders, defense personnel, and environmental cleanup crews. Additionally, advancements in material science are leading to the development of new scintillator materials and semiconductor detectors offering higher efficiency, faster response times, and improved spectral resolution. These innovations are critical for applications requiring precise identification of isotopes, such as nuclear forensics and medical diagnostics. The market is thus characterized by a continuous drive towards innovation, aiming to meet the evolving demands of various end-use industries by providing more accurate, reliable, and adaptable detection solutions.

- Miniaturization and portability of detection devices for enhanced mobility and access.

- Integration of advanced data analytics and machine learning for predictive insights and improved accuracy.

- Increased adoption of real-time monitoring solutions in industrial and healthcare settings.

- Development of multi-purpose detectors capable of identifying various radiation types.

- Expansion of personal dosimetry for enhanced worker safety in hazardous environments.

- Advancements in scintillator and semiconductor materials for higher efficiency and resolution.

AI Impact Analysis on Radiation Detection

User inquiries concerning the impact of Artificial Intelligence on radiation detection often center on how AI can enhance the accuracy and speed of data analysis, automate complex detection processes, and provide predictive capabilities for radiation events. There is significant interest in AI's potential to differentiate between natural background radiation and illicit radioactive materials more effectively, thereby reducing false positives and improving the efficiency of security screening. Furthermore, users explore how AI algorithms can process vast amounts of sensor data from distributed networks, identifying anomalies and patterns that would be imperceptible to human operators, leading to earlier detection of threats or system malfunctions. The ability of AI to learn from historical data and adapt to new scenarios is also a key area of focus, promising more robust and intelligent detection systems.

The application of AI in radiation detection is poised to revolutionize several aspects, from improving the calibration and maintenance of detectors through predictive analytics to enhancing decision-making in emergency response situations. For instance, AI-powered systems can analyze spectral data from detectors to identify specific isotopes with greater precision, crucial for nuclear forensics and medical isotope production. Concerns often include the reliability of AI algorithms in critical safety applications, the need for extensive training data, and the cybersecurity implications of integrating AI into sensitive infrastructure. Despite these challenges, the prevailing expectation is that AI will significantly augment human capabilities, leading to more sophisticated, autonomous, and responsive radiation detection solutions across industries such as healthcare, defense, and environmental monitoring, ultimately enhancing overall safety and operational efficiency.

- Enhanced data analysis and pattern recognition for improved threat identification and reduced false positives.

- Automation of complex detection and classification tasks, increasing operational efficiency.

- Predictive maintenance for radiation detectors, optimizing system uptime and reliability.

- Advanced anomaly detection in radiation signatures, crucial for early warning systems.

- Support for rapid decision-making in emergency response scenarios through real-time data interpretation.

- Development of intelligent, adaptive algorithms for more accurate isotope identification.

Key Takeaways Radiation Detection Market Size & Forecast

Key takeaways from the radiation detection market size and forecast frequently address the underlying factors driving market expansion, the critical applications fueling demand, and the geographical regions expected to exhibit the most robust growth. Users are keen to understand which segments, such as healthcare or defense, will offer the most significant opportunities for investment and technological innovation. The forecast indicates a sustained growth trajectory, primarily influenced by heightened global security concerns, the expanding adoption of nuclear medicine, and the imperative for environmental radiation monitoring. This growth underscores the increasing awareness and regulatory emphasis on radiation safety across various industrial and public sectors, making radiation detection technology an indispensable component of modern infrastructure and safety protocols. The market is not only growing in traditional applications but also expanding into new areas, driven by miniaturization and integration with other technologies.

A crucial insight is the growing emphasis on advanced and smart detection solutions, moving beyond basic monitoring to sophisticated, networked systems capable of real-time data processing and threat assessment. This shift is particularly evident in nuclear power generation, where stringent safety regulations necessitate continuous innovation in detection capabilities. The Asia Pacific region is anticipated to emerge as a dominant growth hub, propelled by rapid industrialization, increasing investments in nuclear energy infrastructure, and rising healthcare expenditures. These dynamics create a fertile ground for manufacturers and service providers to introduce advanced radiation detection technologies, emphasizing the market's long-term potential. Understanding these key takeaways is essential for stakeholders to strategically position themselves within this evolving and vital market. The demand for personal protective equipment, including advanced dosimeters, is also a significant driver in developed economies, reflecting a proactive approach to occupational safety.

- Sustained market growth driven by increasing global security threats and nuclear power expansion.

- Significant demand surge from the healthcare sector due to advancements in nuclear medicine and radiotherapy.

- Asia Pacific region projected for rapid expansion due to industrialization and energy investments.

- Emphasis on smart, integrated, and real-time detection systems for enhanced safety and efficiency.

- Technological innovation, including miniaturization and AI integration, is central to future market development.

- Growing regulatory pressures and heightened awareness of radiation safety are foundational growth drivers.

Radiation Detection Market Drivers Analysis

The radiation detection market is primarily propelled by a confluence of factors, including stringent government regulations aimed at nuclear safety and security, the expanding global nuclear power generation capacity, and the increasing applications of nuclear medicine in healthcare. As countries worldwide commit to reducing carbon emissions, nuclear power remains a viable, low-carbon energy source, necessitating robust radiation monitoring systems throughout its lifecycle, from fuel processing to waste management. This demand extends beyond power generation to various industrial applications, where radiation sources are utilized for sterilization, non-destructive testing, and process control, each requiring precise and reliable detection mechanisms. The continuous evolution of these sectors creates a constant need for advanced and efficient radiation detection technologies, driving innovation and market expansion.

Furthermore, the growing global threat of nuclear proliferation and radiological terrorism mandates sophisticated detection capabilities for homeland security, border control, and defense applications. Governments and security agencies are heavily investing in advanced detection equipment to safeguard critical infrastructure and public safety. Simultaneously, the medical field sees an increasing use of radiation in diagnostic imaging, cancer therapy, and various therapeutic procedures, which, while beneficial, necessitates strict monitoring to ensure patient and occupational safety. This dual demand from both security-conscious public sectors and rapidly expanding medical fields acts as a powerful catalyst for the radiation detection market, driving product development and broader adoption of these critical technologies across diverse end-use industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Demand for Nuclear Power Generation | +1.5% | APAC, Europe, North America | Medium to Long-term (2025-2033) |

| Growing Applications in Medical & Healthcare Sector | +1.2% | Global (Developed Economies) | Short to Long-term (2025-2033) |

| Rising Global Security Concerns and Defense Spending | +1.0% | North America, Europe, Middle East | Short to Medium-term (2025-2030) |

| Strict Regulatory Frameworks for Radiation Safety | +0.8% | Global (OECD Countries) | Short to Long-term (2025-2033) |

| Technological Advancements in Detector Capabilities | +0.7% | Global | Medium to Long-term (2027-2033) |

Radiation Detection Market Restraints Analysis

Despite the robust growth drivers, the radiation detection market faces several restraints that could impede its expansion. One significant challenge is the high cost associated with advanced radiation detection equipment, particularly specialized systems used in nuclear facilities or high-security applications. The initial investment, coupled with ongoing maintenance and calibration expenses, can be prohibitive for smaller organizations or those in developing economies. This cost factor often leads to extended procurement cycles and a slower adoption rate for cutting-edge technologies. Furthermore, the complexity of operating and maintaining sophisticated detection systems requires highly skilled personnel, and a shortage of such expertise globally presents a substantial operational hurdle. This talent gap can limit the effective deployment and utilization of advanced detection solutions, particularly in regions with nascent nuclear or security infrastructure.

Another major restraint is the intricate and ever-evolving regulatory landscape governing radiation safety and security. While regulations drive demand for compliance, they can also impose significant barriers to market entry for new technologies and can slow down the innovation cycle due to lengthy approval processes. The need for precise calibration, adherence to international standards, and continuous auditing adds to the operational burden for end-users and manufacturers alike. Additionally, public perception and apprehension regarding radiation exposure, even at safe levels, can influence policy decisions and hinder the expansion of applications involving radioactive materials. These multifaceted restraints necessitate strategic approaches from market players to overcome these challenges, focusing on cost-effective solutions, workforce development, and proactive engagement with regulatory bodies to ensure sustainable market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Detection Systems | -0.9% | Global (Developing Economies) | Short to Medium-term (2025-2030) |

| Lack of Skilled Professionals for Operation & Maintenance | -0.7% | Global | Medium-term (2026-2031) |

| Complex and Stringent Regulatory Approval Processes | -0.6% | Europe, North America | Long-term (2025-2033) |

| Perceived Risks and Public Apprehension towards Radiation | -0.5% | Europe, North America | Long-term (2025-2033) |

| Technological Obsolescence & High R&D Investment | -0.4% | Global | Medium to Long-term (2027-2033) |

Radiation Detection Market Opportunities Analysis

The radiation detection market is ripe with opportunities driven by several emerging trends and unmet needs across various industries. One significant opportunity lies in the burgeoning demand from emerging economies, particularly in Asia Pacific and Latin America, where rapid industrialization, expansion of nuclear power infrastructure, and increasing healthcare investments are creating new avenues for detector deployment. These regions often prioritize cost-effective yet reliable solutions, opening doors for manufacturers to offer scalable and accessible technologies. Furthermore, the integration of radiation detection with Internet of Things (IoT) platforms and advanced data analytics presents a substantial opportunity to create networked monitoring systems, providing real-time data, predictive insights, and enhanced situational awareness, especially in large-scale industrial complexes and smart city initiatives. This fusion of technologies moves beyond simple detection to comprehensive environmental and security management.

Another area of immense potential resides in the development of highly portable, wearable, and drone-mounted detection devices. These innovations cater to the growing need for dynamic monitoring in challenging environments, such as disaster zones, remote industrial sites, and urban security patrols. Such devices offer greater flexibility, rapid deployment capabilities, and minimize human exposure risks, thereby expanding the market's reach into new operational paradigms. Additionally, the increasing focus on space exploration and extraterrestrial resource mining represents a niche yet high-growth opportunity for specialized radiation detectors capable of operating under extreme conditions. Customization and miniaturization, combined with robust performance, are key in addressing these specialized demands, signaling a shift towards highly tailored and application-specific solutions that can significantly broaden the market's overall scope and revenue streams in the long term.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Economies (APAC, Latin America) | +1.3% | APAC, Latin America | Medium to Long-term (2025-2033) |

| Integration with IoT, AI, and Advanced Analytics | +1.1% | Global | Medium to Long-term (2026-2033) |

| Development of Portable, Wearable, and Drone-mounted Detectors | +1.0% | Global | Short to Medium-term (2025-2030) |

| Growing Demand for Environmental Monitoring | +0.9% | Europe, North America | Medium to Long-term (2027-2033) |

| Applications in Space Exploration & Niche Scientific Research | +0.6% | North America, Europe | Long-term (2028-2033) |

Radiation Detection Market Challenges Impact Analysis

The radiation detection market faces several significant challenges that can hinder its growth and operational efficiency. One primary challenge is the technical complexity involved in developing detectors capable of accurately distinguishing between various radiation types and energies, especially in mixed radiation fields or environments with high background noise. Achieving high sensitivity, resolution, and speed while ensuring robustness and reliability in diverse operating conditions requires substantial R&D investment and advanced material science. Furthermore, maintaining the calibration and accuracy of detectors over long periods and across varying environmental conditions presents a continuous operational challenge. Any deviation in performance can lead to serious safety implications or inaccurate data, making regular calibration and rigorous quality control essential but resource-intensive.

Another major challenge is the persistent issue of high manufacturing costs for advanced semiconductor and scintillator materials, which directly impacts the final product price and market accessibility. Supply chain vulnerabilities for these specialized components, often sourced from a limited number of suppliers, can lead to production delays and increased costs. Moreover, the dynamic nature of threats, such as evolving nuclear materials or new forms of radiological dispersion devices, demands continuous innovation and adaptation of detection technologies, placing a constant burden on manufacturers to stay ahead. Addressing these challenges requires strategic collaboration between industry players, research institutions, and regulatory bodies to foster innovation, streamline supply chains, and develop cost-effective, high-performance solutions that meet the evolving demands of a complex and critical market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Complexity and High R&D Costs | -0.8% | Global | Long-term (2025-2033) |

| Supply Chain Vulnerabilities for Specialized Components | -0.6% | Global | Short to Medium-term (2025-2028) |

| Maintaining Detector Calibration and Accuracy | -0.5% | Global | Long-term (2025-2033) |

| Evolving Threat Landscape and Need for Adaptation | -0.4% | Global | Medium to Long-term (2026-2033) |

| Data Interpretation and Management for Large Sensor Networks | -0.3% | Global | Medium-term (2025-2030) |

Radiation Detection Market - Updated Report Scope

This report provides a comprehensive analysis of the global Radiation Detection Market, offering in-depth insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and regions. It delves into the latest technological advancements, including the impact of AI and IoT, and evaluates their potential to reshape the industry landscape. The scope encompasses detailed market segmentation by detector type, application, end-use industry, and geography, presenting a holistic view of the market's current state and future trajectory. Strategic profiles of key market players are also included to offer competitive intelligence and understand market positioning, making this a critical resource for stakeholders seeking to navigate the complex dynamics of the radiation detection sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 3.5 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mirion Technologies, Radiation Detection Company, Fluke Corporation, Thermo Fisher Scientific Inc., AMETEK, Inc., Canberra (Mirion Technologies), Smiths Detection Inc., Landauer, Inc., Fuji Electric Co., Ltd., Arktis Radiation Detectors Ltd., Kromek Group plc, NUVIA a.s., Bertin Instruments, Leidos Holdings, Inc., Teledyne FLIR LLC, Bar-Ray Products, Inc., CIRCOR International, Inc., LND, Inc., ORTEC (AMETEK, Inc.), Renishaw plc |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The radiation detection market is segmented to provide a granular understanding of its diverse applications and technological landscape. This segmentation is crucial for identifying specific growth pockets, understanding regional preferences, and tailoring product development to meet specialized needs. The primary segments include categorization by detector type, such as Geiger-Muller counters, scintillators, and solid-state detectors, each offering distinct advantages in terms of sensitivity, energy resolution, and cost. Further segmentation by end-use industry highlights the varied applications in healthcare, defense, nuclear power, and environmental monitoring, underscoring the broad utility of these technologies across critical sectors. This multi-dimensional approach to segmentation helps to accurately map market dynamics and forecast future trends, enabling stakeholders to make informed strategic decisions.

- By Type: Geiger-Muller Counters, Scintillators, Solid-State Detectors (Semiconductor Detectors), Ionization Chambers, Proportional Counters, and Others.

- By End-Use Industry: Healthcare, Defense & Homeland Security, Nuclear Power Plants, Industrial, Environmental Monitoring, Oil & Gas, and Research & Academic Institutions.

- By Application: Radiation Monitoring, Personal Dosimetry, Contamination Monitoring, Spectroscopy, Imaging, and Threat Detection.

- By Offering: Hardware (Detectors, Monitors, Dosimeters), Software (Analysis, Visualization, Control), and Services (Calibration, Maintenance, Training, Consulting).

Regional Highlights

- North America: A mature market characterized by significant investments in homeland security, defense, and healthcare infrastructure. The region benefits from stringent regulatory frameworks and a strong presence of key technology providers, driving demand for advanced detection systems and personal dosimetry.

- Europe: Exhibits robust growth driven by nuclear power decommissioning activities, a strong focus on environmental monitoring, and a growing adoption of nuclear medicine. Strict EU safety regulations and a proactive approach to CBRN threat detection contribute to sustained market demand.

- Asia Pacific (APAC): Projected to be the fastest-growing region, fueled by rapid industrialization, increasing investments in nuclear power generation (e.g., China, India), and expanding healthcare sectors. Rising awareness of radiation safety and growing defense expenditures also contribute significantly to market expansion.

- Latin America: An emerging market with growing demand driven by investments in the oil & gas sector, mining industries, and nascent nuclear energy programs. Economic development and increasing focus on public safety are gradually stimulating market growth.

- Middle East & Africa (MEA): Marked by increasing investments in nuclear power projects (e.g., UAE, Saudi Arabia), burgeoning oil & gas exploration, and a rising focus on homeland security. The region presents significant long-term growth opportunities, albeit with market development in early stages.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Radiation Detection Market.- Mirion Technologies

- Radiation Detection Company

- Fluke Corporation

- Thermo Fisher Scientific Inc.

- AMETEK, Inc.

- Canberra (Mirion Technologies)

- Smiths Detection Inc.

- Landauer, Inc.

- Fuji Electric Co., Ltd.

- Arktis Radiation Detectors Ltd.

- Kromek Group plc

- NUVIA a.s.

- Bertin Instruments

- Leidos Holdings, Inc.

- Teledyne FLIR LLC

- Bar-Ray Products, Inc.

- CIRCOR International, Inc.

- LND, Inc.

- ORTEC (AMETEK, Inc.)

- Renishaw plc

Frequently Asked Questions

Analyze common user questions about the Radiation Detection market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is radiation detection and why is it important?

Radiation detection involves identifying and measuring ionizing radiation. It is crucial for ensuring safety in environments with radioactive materials, monitoring nuclear facilities, protecting personnel in healthcare and defense, and detecting illicit radioactive substances to prevent security threats. Its importance stems from safeguarding human health and national security.

What are the main types of radiation detectors?

The primary types of radiation detectors include Geiger-Muller counters for general purpose detection, scintillators known for high efficiency, solid-state (semiconductor) detectors offering high energy resolution, and ionization chambers and proportional counters for precise measurement of radiation dose. Each type is suited for specific applications based on its characteristics.

How is AI impacting the radiation detection market?

AI is significantly enhancing radiation detection by improving data analysis, reducing false positives, automating complex tasks, and providing predictive insights. It helps in more accurate isotope identification, optimizes detector performance through predictive maintenance, and aids rapid decision-making in critical situations by processing vast amounts of sensor data.

Which industries are the primary end-users of radiation detection technology?

Key end-user industries include healthcare (nuclear medicine, radiotherapy), defense and homeland security (CBRN detection, border control), nuclear power plants, various industrial applications (non-destructive testing, sterilization), environmental monitoring, and research institutions. These sectors rely heavily on precise radiation detection for safety, compliance, and operational efficiency.

What are the key growth drivers for the radiation detection market?

The market's growth is primarily driven by increasing global security concerns, the expanding adoption of nuclear medicine and diagnostic imaging in healthcare, the global push for nuclear power as a clean energy source, and stringent regulatory frameworks mandating radiation safety and monitoring. Technological advancements also play a crucial role in enabling new applications and improving detector performance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted