HFC Refrigerant Market

HFC Refrigerant Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706359 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

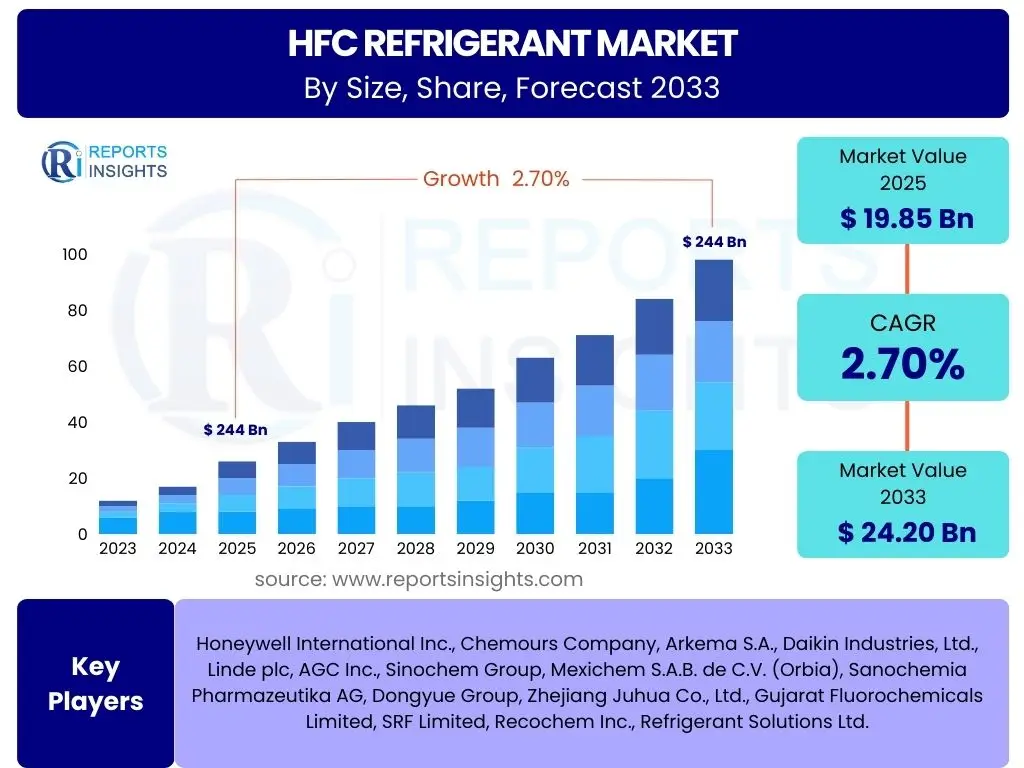

HFC Refrigerant Market Size

According to Reports Insights Consulting Pvt Ltd, The HFC Refrigerant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 2.7% between 2025 and 2033. The market is estimated at USD 19.85 Billion in 2025 and is projected to reach USD 24.20 Billion by the end of the forecast period in 2033. This growth, while modest, signifies a complex market dynamic where increasing demand for cooling and refrigeration services globally coexists with stringent regulations aimed at phasing down the production and consumption of high-Global Warming Potential (GWP) hydrofluorocarbons (HFCs).

Key HFC Refrigerant Market Trends & Insights

The HFC refrigerant market is undergoing a significant transformation driven by global environmental initiatives and technological advancements. Key user questions frequently revolve around the regulatory landscape, the emergence of alternative refrigerants, and the overarching shift towards more sustainable cooling solutions. The dominant trend is the structured phase-down of high-GWP HFCs, mandated by international agreements such as the Kigali Amendment to the Montreal Protocol and regional regulations like the European Union’s F-Gas Regulation. This regulatory pressure is compelling manufacturers and end-users to transition towards refrigerants with lower environmental impact, including hydrofluoroolefins (HFOs), natural refrigerants like CO2, ammonia, and hydrocarbons, and other innovative blends.

Beyond regulatory compliance, the market is witnessing a strong emphasis on energy efficiency in refrigeration and air conditioning systems. This trend is not only a response to rising energy costs but also an integral part of reducing the overall carbon footprint of cooling technologies. Innovations in equipment design, compressor technology, and heat exchange mechanisms are enabling the use of low-GWP refrigerants more effectively while simultaneously improving system performance. Furthermore, the concept of a circular economy is gaining traction, promoting better refrigerant management through reclamation, recycling, and destruction programs to minimize emissions from the existing installed base.

The convergence of digitalization and the cooling sector also represents a pivotal trend. Smart HVACR systems, equipped with sensors and IoT capabilities, are becoming more prevalent, enabling real-time monitoring, predictive maintenance, and optimized energy consumption. This integration facilitates better leak detection, efficient system operation, and improved compliance with refrigerant management protocols. The shift reflects a broader industry commitment to not only comply with environmental mandates but also to innovate for long-term sustainability and operational excellence across various applications, from commercial refrigeration to mobile air conditioning.

- Global phase-down of high-GWP HFCs driven by the Kigali Amendment and regional regulations.

- Increasing adoption and development of low-GWP alternatives, including HFOs and natural refrigerants (CO2, ammonia, hydrocarbons).

- Growing focus on energy efficiency in refrigeration and air conditioning equipment design.

- Emphasis on circular economy principles through improved refrigerant recovery, recycling, and reclamation programs.

- Integration of smart technologies, IoT, and digitalization for enhanced system monitoring and management.

- Expansion of cold chain infrastructure, particularly in developing economies, necessitating new and efficient refrigerant solutions.

AI Impact Analysis on HFC Refrigerant

The integration of Artificial intelligence (AI) is set to significantly influence the HFC refrigerant market, with common user inquiries often focusing on how AI can enhance efficiency, reduce environmental impact, and streamline operations. AI applications are primarily impacting predictive maintenance for HVACR systems, enabling early detection of potential failures and refrigerant leaks. By analyzing vast datasets from sensors within refrigeration and air conditioning units, AI algorithms can identify subtle anomalies that indicate a pending equipment malfunction or a refrigerant leak, thereby allowing for proactive interventions. This not only prevents costly breakdowns and extends the lifespan of equipment but also crucially minimizes the release of HFCs into the atmosphere, contributing directly to environmental compliance and sustainability goals.

Beyond maintenance, AI is revolutionizing the optimization of refrigerant charge and system performance. Advanced AI models can analyze real-time operational data, environmental conditions, and energy consumption patterns to fine-tune refrigerant flow and system parameters. This optimization ensures that refrigeration and air conditioning systems operate at peak efficiency, consuming less energy and potentially requiring lower refrigerant charges. Such capabilities are invaluable in reducing both direct HFC emissions and indirect emissions associated with energy generation. Furthermore, AI-driven insights can guide the design and selection of new systems, recommending optimal refrigerant types and equipment configurations based on specific application requirements and long-term environmental targets.

In the broader supply chain and regulatory compliance landscape, AI offers significant advantages for the HFC refrigerant market. AI can be leveraged to forecast demand for various refrigerants, manage inventory, and optimize logistics, especially crucial as the industry transitions to new refrigerant types. This foresight helps prevent shortages or overstocking and can streamline the distribution of alternative refrigerants. For regulatory compliance, AI-powered platforms can track refrigerant usage, emissions, and maintenance records, automating reporting processes and ensuring adherence to international and regional phase-down schedules. This robust data management and analytical capability will be essential for navigating the complex and evolving regulatory environment surrounding HFCs and their alternatives, enhancing accountability and operational transparency across the industry.

- AI-driven predictive maintenance for HVACR systems to prevent refrigerant leaks and equipment failures.

- Optimization of refrigerant charge and system performance for enhanced energy efficiency.

- Real-time monitoring and anomaly detection to minimize HFC emissions.

- Supply chain optimization for new and alternative refrigerants, improving logistics and inventory management.

- Automated compliance tracking and reporting for regulatory adherence to phase-down schedules.

- Development of smart diagnostic tools for technicians to efficiently manage and service refrigerant systems.

Key Takeaways HFC Refrigerant Market Size & Forecast

A primary takeaway from the HFC refrigerant market analysis is the intricate balance between persistent demand for cooling solutions and the imperative to adhere to global environmental regulations. User questions frequently highlight this tension, asking how the market can grow while simultaneously phasing out its primary product. The market's projected growth, despite the HFC phase-down, is largely underpinned by a robust expansion in various application sectors, particularly in emerging economies where urbanization, rising disposable incomes, and the expansion of cold chain logistics are driving significant demand for refrigeration and air conditioning. This underlying demand necessitates continued innovation, focusing on the development and deployment of next-generation, environmentally benign refrigerants and energy-efficient cooling technologies.

Another crucial insight is the accelerating transition towards low-GWP and natural refrigerants, which is not merely a compliance exercise but a strategic pivot for long-term sustainability. Companies that proactively invest in research and development for these alternatives, along with associated equipment and infrastructure, are positioned to capture significant market share in the coming years. This shift requires substantial capital investment, technological adaptation, and workforce retraining across the value chain. The market forecast underscores that while HFCs will continue to be used in existing equipment for some time, new installations and retrofits will increasingly favor alternatives, thereby reshaping the industry landscape significantly over the forecast period.

Ultimately, the market is characterized by a dual imperative: satisfying the ever-growing global need for cooling and meeting stringent environmental targets. This presents both challenges and opportunities. Manufacturers and service providers must navigate complex regulatory frameworks, manage supply chain transitions, and educate end-users on the benefits and requirements of new technologies. The long-term success in the HFC refrigerant market will depend on the industry's collective ability to innovate sustainably, ensure safe handling of new refrigerants, and deliver solutions that are both environmentally responsible and economically viable, thereby cementing a pathway towards a low-carbon future for the cooling sector.

- The market is undergoing a fundamental shift from high-GWP HFCs to low-GWP alternatives due to global environmental regulations.

- Despite the phase-down, overall market growth is driven by increasing demand for cooling and refrigeration in diverse applications, especially in developing regions.

- Significant investment in research and development of new refrigerants and energy-efficient technologies is crucial for market players.

- Regulatory compliance, particularly with the Kigali Amendment and regional F-Gas regulations, remains a primary determinant of market evolution.

- Opportunities exist in retrofitting existing HFC systems with low-GWP alternatives and developing robust circular economy practices for refrigerant management.

HFC Refrigerant Market Drivers Analysis

The HFC refrigerant market continues to be influenced by a set of robust drivers, despite the ongoing global phase-down initiatives. A primary driver is the pervasive and growing demand for refrigeration and air conditioning across residential, commercial, and industrial sectors. Rapid urbanization, particularly in emerging economies, leads to increased construction of residential buildings, commercial complexes, and data centers, all requiring sophisticated cooling systems. Additionally, rising global temperatures and improved living standards are fueling the adoption of air conditioning units in regions previously less saturated, thereby creating a sustained need for refrigerants. This fundamental demand ensures that even as the industry transitions away from high-GWP HFCs, the underlying market for cooling technologies remains strong, necessitating the supply of existing HFCs for servicing and a rapid increase in demand for alternative solutions for new installations.

Furthermore, the expansion of cold chain logistics, especially in the food & beverage and pharmaceutical industries, acts as a significant market driver. As global trade increases and consumer preferences shift towards fresh and frozen products, the integrity of the cold chain from production to consumption becomes paramount. This requires reliable and efficient refrigeration systems for transportation, storage, and retail, which historically have relied heavily on HFCs. While new investments are directed towards low-GWP solutions, the vast existing infrastructure continues to operate with HFCs, necessitating ongoing demand for maintenance and servicing. This persistent need for cold chain reliability, coupled with the growth of pharmaceutical distribution networks that demand precise temperature control, ensures that the refrigerant market, including its HFC segment for legacy systems, maintains a baseline level of activity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Demand for Cooling & Refrigeration | +3.5% | Asia Pacific, Middle East & Africa, Latin America | 2025-2033 (Mid to Long-term) |

| Expansion of Cold Chain Infrastructure | +2.8% | Global, especially Emerging Economies | 2025-2030 (Mid-term) |

| Urbanization & Infrastructure Development | +2.2% | India, China, Southeast Asia | 2025-2033 (Long-term) |

HFC Refrigerant Market Restraints Analysis

The HFC refrigerant market faces significant restraints primarily due to stringent environmental regulations and the escalating costs associated with compliance and the transition to alternative technologies. The most prominent restraint is the global HFC phase-down mandated by the Kigali Amendment to the Montreal Protocol, alongside regional regulations like the EU F-Gas Regulation and the U.S. AIM Act. These policies impose strict limits on HFC production and consumption, driving down their availability and increasing their price, thereby directly curtailing market growth for these substances. Companies are compelled to invest heavily in research and development for low-GWP alternatives, retrofitting existing equipment, and developing entirely new systems, which often entails substantial capital expenditure that can impede market expansion.

Beyond regulatory pressures, the inherent high costs associated with new, environmentally friendly refrigerants and the equipment designed to use them also act as a significant restraint. Many low-GWP alternatives, particularly HFOs, are currently more expensive to produce than traditional HFCs. Furthermore, the specialized components and complex system designs required for these new refrigerants, such as those for flammable or high-pressure applications, can add to the upfront investment for end-users. This economic barrier, coupled with the need for extensive retraining of technicians and installers to safely handle and apply these new substances, creates a considerable hurdle for widespread adoption and limits the overall growth trajectory of the market segment still relying on or transitioning from HFCs, compelling a faster shift to alternatives rather than a sustained HFC presence.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Global Environmental Regulations (HFC Phase-down) | -4.5% | Global, particularly Europe, North America | 2025-2033 (Mid to Long-term) |

| High Cost of Alternative Refrigerants & Transitioning Equipment | -3.0% | Global | 2025-2030 (Mid-term) |

| Limited Availability of Skilled Workforce for New Technologies | -1.5% | Global | 2025-2028 (Short to Mid-term) |

HFC Refrigerant Market Opportunities Analysis

Despite the prevailing regulatory challenges, the HFC refrigerant market, primarily its transitional phase, presents significant opportunities driven by the innovation in low-GWP alternatives and the imperative for energy efficiency. A major opportunity lies in the burgeoning development and commercialization of new generations of refrigerants, including Hydrofluoroolefins (HFOs), Hydrocarbons (HCs), Carbon Dioxide (CO2), and Ammonia (NH3). These alternatives offer significantly lower Global Warming Potentials (GWP) and in some cases, enhanced thermodynamic properties, making them attractive for a wide range of applications. Companies that invest in the research, production, and distribution of these sustainable refrigerants are well-positioned to lead the market's evolution, capturing demand as industries shift away from traditional HFCs and seek more environmentally responsible cooling solutions for new installations and future systems.

Another substantial opportunity exists in the retrofitting and servicing of the vast installed base of HFC-dependent equipment. With millions of existing refrigeration and air conditioning systems globally still operating on high-GWP HFCs, there is a continuous need for maintenance, repair, and eventually, conversion to more sustainable alternatives. This creates a lucrative market for specialized services, including refrigerant reclamation, recycling, and conversion kits that enable the use of lower-GWP drop-in or near drop-in replacements. Furthermore, the focus on enhancing energy efficiency in new and existing systems presents an avenue for growth, as integrating advanced technologies that reduce power consumption while using sustainable refrigerants addresses both environmental and operational cost concerns. This dual focus on lower GWP and higher energy efficiency helps meet current regulatory demands and positions companies for long-term growth in a market increasingly focused on holistic environmental performance.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Low-GWP & Natural Refrigerants | +5.8% | Global | 2026-2033 (Mid to Long-term) |

| Retrofitting & Servicing of Existing HFC Systems | +4.2% | Europe, North America, Developed Asia Pacific | 2025-2030 (Mid-term) |

| Technological Advancements in Energy-Efficient HVACR Systems | +3.5% | Global | 2025-2033 (Long-term) |

HFC Refrigerant Market Challenges Impact Analysis

The HFC refrigerant market, navigating its transition, faces several formidable challenges that could impede its growth and smooth evolution. A significant hurdle is the safety concerns associated with many low-GWP alternative refrigerants. While natural refrigerants like ammonia and hydrocarbons offer excellent environmental profiles, they come with flammability or toxicity risks, necessitating stringent safety protocols, specialized equipment design, and extensive training for technicians. Similarly, some HFOs, while having very low GWP, are mildly flammable, introducing new handling and installation considerations. Ensuring the safe adoption and widespread deployment of these alternatives requires significant investment in infrastructure, safety standards, and workforce education, which adds complexity and cost to the transition process, potentially slowing down the pace of adoption.

Another critical challenge is managing the supply chain for new refrigerants and preventing the illegal trade of restricted HFCs. As HFC production quotas decline, a black market for these refrigerants can emerge, undermining regulatory efforts and posing environmental risks. Policing and enforcing regulations across international borders are complex and resource-intensive. Furthermore, the global supply chains for new, often proprietary, alternative refrigerants and their associated components can be vulnerable to disruptions, affecting availability and pricing. This complexity is compounded by the substantial research and development costs required to innovate next-generation refrigerant solutions and systems, alongside the significant capital investment needed to scale up production facilities for these new substances. These factors collectively pose substantial operational and financial burdens on market players, affecting their ability to adapt quickly and efficiently to the evolving market landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Safety Concerns (Flammability, Toxicity) of Alternative Refrigerants | -2.8% | Global | 2025-2030 (Mid-term) |

| Illegal Trade & Smuggling of Restricted HFCs | -1.8% | Europe, Asia Pacific | 2025-2028 (Short to Mid-term) |

| High R&D Costs for Next-Gen Solutions & Production Scaling | -1.2% | Global | 2025-2033 (Long-term) |

HFC Refrigerant Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the HFC Refrigerant Market, detailing its size, growth trajectory, and critical drivers, restraints, opportunities, and challenges influencing its dynamics from 2019 to 2033. The study meticulously segments the market by product type, application, and end-use industry, offering granular insights into specific market performances and emerging trends. Furthermore, it includes a robust regional analysis across key geographies and profiles leading companies, offering a competitive landscape view. The report aims to furnish stakeholders with actionable insights to navigate the evolving regulatory environment and capitalize on opportunities arising from the global transition towards sustainable cooling solutions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.85 Billion |

| Market Forecast in 2033 | USD 24.20 Billion |

| Growth Rate | 2.7% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., Chemours Company, Arkema S.A., Daikin Industries, Ltd., Linde plc, AGC Inc., Sinochem Group, Mexichem S.A.B. de C.V. (Orbia), Sanochemia Pharmazeutika AG, Dongyue Group, Zhejiang Juhua Co., Ltd., Gujarat Fluorochemicals Limited, SRF Limited, Recochem Inc., Refrigerant Solutions Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The HFC refrigerant market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective dynamics. This segmentation is crucial for identifying specific growth pockets, understanding technological shifts, and formulating targeted strategies within the evolving regulatory landscape. By breaking down the market into product types, key applications, and end-use industries, stakeholders can gain granular insights into where demand is shifting and which segments are poised for significant transformation as the global phase-down of high-GWP HFCs progresses and low-GWP alternatives gain traction. This structured analysis highlights both the persisting relevance of certain HFCs for legacy systems and the rapid growth areas for new refrigerant solutions.

- By Product Type:

- R-134a: Widely used in automotive air conditioning and chillers.

- R-410A: Dominant in residential and commercial air conditioning systems.

- R-404A: Primarily used in commercial refrigeration and transport refrigeration.

- R-507: A blend similar to R-404A, used in low and medium-temperature refrigeration.

- R-407C: Used in air conditioning and some medium-temperature refrigeration applications.

- R-32: Gaining traction as a low-GWP alternative, especially in air conditioning.

- Others: Including various blends and niche HFCs.

- By Application:

- Refrigeration:

- Commercial Refrigeration (supermarkets, cold storage)

- Industrial Refrigeration (food processing, chemical plants)

- Domestic Refrigeration (household refrigerators, freezers)

- Air Conditioning:

- Residential Air Conditioning

- Commercial Air Conditioning (office buildings, hotels)

- Automotive Air Conditioning

- Heat Pumps

- Chillers

- Others (e.g., medical devices, fire suppression)

- By End-Use Industry:

- Food & Beverage

- Pharmaceutical

- Automotive

- Chemical

- Retail (supermarkets, convenience stores)

- Commercial Buildings (offices, hotels, malls)

- Residential

- Others

Regional Highlights

- Asia Pacific (APAC): Expected to be the fastest-growing region driven by rapid urbanization, increasing disposable incomes, and the expansion of the cold chain infrastructure in countries like India, China, and Southeast Asian nations. While demand for new cooling systems is high, the region is also witnessing increased adoption of low-GWP alternatives, particularly in new installations, balancing growth with environmental considerations.

- Europe: A pioneering region in the HFC phase-down, primarily driven by the stringent F-Gas Regulation. Europe is at the forefront of adopting natural refrigerants and HFOs, leading to significant investments in research and development for sustainable cooling solutions. The market here is characterized by a strong emphasis on retrofitting existing systems and compliance with strict environmental standards.

- North America: Influenced by the U.S. AIM Act and Canadian regulations, North America is undergoing a structured HFC phase-down, fostering innovation in low-GWP refrigerants and energy-efficient technologies. The region exhibits strong adoption rates for new technologies in commercial and industrial applications, balancing environmental goals with economic efficiency.

- Latin America: Showing steady growth driven by increasing demand for air conditioning and refrigeration, particularly in urban areas. The region is in the early to mid-stages of adapting to HFC phase-down initiatives, with opportunities for both traditional HFCs for servicing existing systems and the gradual introduction of alternatives for new developments.

- Middle East & Africa (MEA): Experiencing significant market expansion due to population growth, infrastructure development, and rising temperatures. While HFCs remain prevalent in many applications, awareness and adoption of sustainable alternatives are gradually increasing, driven by international commitments and growing environmental concerns within the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the HFC Refrigerant Market.- Honeywell International Inc.

- Chemours Company

- Arkema S.A.

- Daikin Industries, Ltd.

- Linde plc

- AGC Inc.

- Sinochem Group

- Mexichem S.A.B. de C.V. (Orbia)

- Sanochemia Pharmazeutika AG

- Dongyue Group

- Zhejiang Juhua Co., Ltd.

- Gujarat Fluorochemicals Limited

- SRF Limited

- Recochem Inc.

- Refrigerant Solutions Ltd.

- Mitsubishi Chemical Corporation

- Asahi Glass Co., Ltd.

- Air Liquide

- Ingersoll Rand Inc.

- Trane Technologies plc

Frequently Asked Questions

What are HFC refrigerants and why are they being phased down?

HFCs (hydrofluorocarbons) are synthetic refrigerants widely used in air conditioning, refrigeration, and heat pump systems. They are being phased down globally due to their high Global Warming Potential (GWP), contributing significantly to climate change. International agreements like the Kigali Amendment aim to reduce their production and consumption to mitigate environmental impact.

What are the primary alternatives to high-GWP HFCs?

The primary alternatives to high-GWP HFCs include low-GWP HFOs (hydrofluoroolefins), and natural refrigerants such as CO2 (carbon dioxide), ammonia (NH3), and hydrocarbons (e.g., propane, isobutane). These alternatives offer significantly lower environmental impact, although some may present flammability or toxicity considerations requiring specialized system designs and handling.

How do regulations like the Kigali Amendment impact the HFC refrigerant market?

Regulations like the Kigali Amendment enforce a gradual, structured phase-down of HFC production and consumption globally. This drives demand for low-GWP alternatives, encourages investment in new technologies, and shifts market dynamics away from traditional HFCs, impacting supply, pricing, and overall market structure as industries transition to more sustainable solutions.

What role does energy efficiency play in the future of refrigeration and air conditioning?

Energy efficiency is crucial for the future of refrigeration and air conditioning. More efficient systems reduce operational costs and significantly lower indirect greenhouse gas emissions from energy consumption, complementing direct emission reductions from refrigerant choice. This dual focus supports global climate goals by minimizing the overall environmental footprint of cooling technologies.

What are the key challenges in transitioning to new refrigerant technologies?

Key challenges include the higher initial cost of new low-GWP refrigerants and compatible equipment, safety concerns (e.g., flammability) with some alternatives, the need for extensive retraining of the workforce for safe handling and installation, and potential supply chain disruptions for emerging chemicals. Overcoming these requires significant industry collaboration and investment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted