Natural Refrigerant Market

Natural Refrigerant Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707491 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

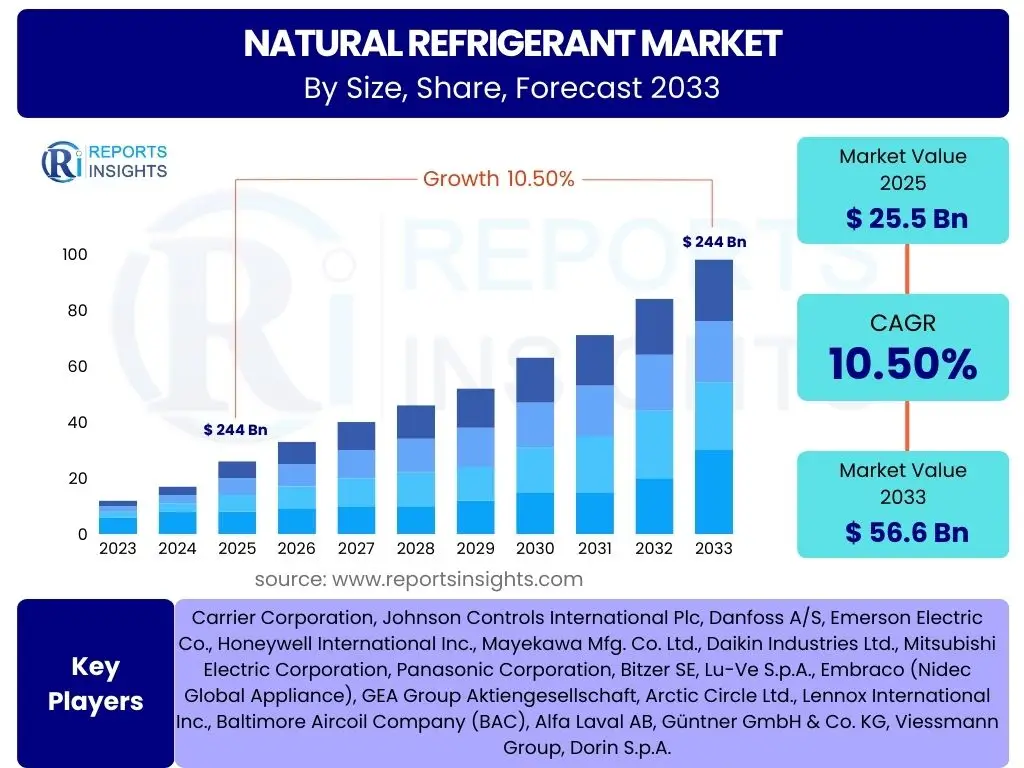

Natural Refrigerant Market Size

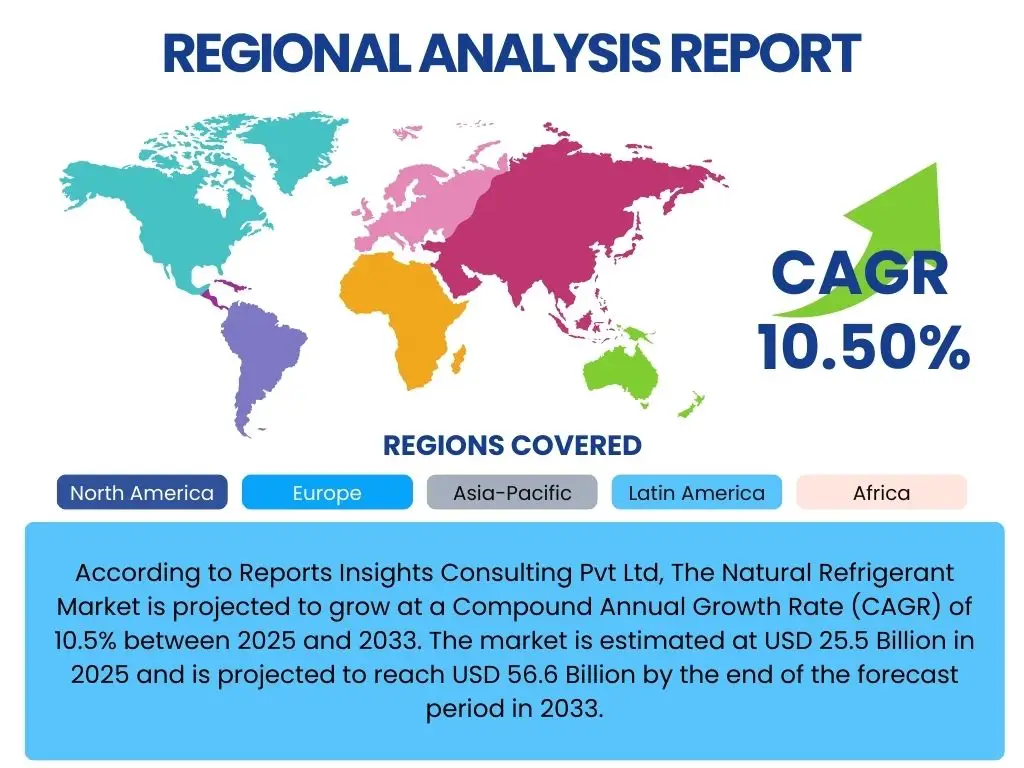

According to Reports Insights Consulting Pvt Ltd, The Natural Refrigerant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 56.6 Billion by the end of the forecast period in 2033.

Key Natural Refrigerant Market Trends & Insights

The Natural Refrigerant market is currently experiencing significant transformative trends driven by escalating environmental concerns and stringent regulatory frameworks globally. A primary trend involves the accelerating shift from traditional synthetic refrigerants, such as HFCs, to naturally occurring alternatives like CO2, ammonia, and hydrocarbons. This transition is largely propelled by international agreements and national legislations aimed at phasing down substances with high global warming potential, creating a robust demand for sustainable cooling solutions across various industrial and commercial sectors. The imperative to reduce carbon footprints and enhance energy efficiency is reshaping product development and deployment strategies within the industry.

Another prominent insight is the continuous innovation in natural refrigerant technologies, focusing on improving system efficiency, safety, and cost-effectiveness. Advancements in transcritical CO2 systems, for instance, are expanding their applicability to warmer climates, overcoming previous geographical limitations. Similarly, improvements in ammonia-based systems are addressing safety concerns through low-charge designs, making them more appealing for a broader range of applications. This technological evolution is crucial for broader market adoption, as it directly impacts the economic viability and operational benefits for end-users.

Furthermore, the market is witnessing an increasing convergence of sustainability goals with economic incentives. Governments and organizations are offering grants, subsidies, and tax benefits for businesses that invest in natural refrigerant technologies, further accelerating their adoption. This confluence of environmental responsibility, technological readiness, and financial support is creating a favorable ecosystem for the growth of natural refrigerants, solidifying their position as a long-term solution in the global cooling landscape. The demand for plug-and-play solutions and modular systems is also on the rise, simplifying installation and reducing upfront costs.

- Stringent regulatory shifts phasing out high GWP refrigerants.

- Increased demand for energy-efficient and sustainable cooling solutions.

- Technological advancements in CO2 transcritical and low-charge ammonia systems.

- Growing adoption in commercial refrigeration, industrial, and HVAC sectors.

- Rising consumer and corporate environmental consciousness.

- Government incentives and subsidies promoting natural refrigerant adoption.

- Focus on system integration and smart controls for optimized performance.

AI Impact Analysis on Natural Refrigerant

Artificial Intelligence is poised to significantly impact the Natural Refrigerant market by optimizing system performance, enhancing predictive maintenance, and streamlining operational efficiencies. AI-powered algorithms can analyze vast datasets from refrigeration systems, including temperature, pressure, energy consumption, and environmental conditions, to fine-tune operating parameters in real-time. This optimization leads to reduced energy consumption, minimizing operational costs and further enhancing the environmental benefits of natural refrigerants. For instance, AI can predict optimal defrost cycles or adjust compressor speeds based on ambient conditions, leading to considerable energy savings for end-users.

Moreover, AI plays a crucial role in predictive maintenance, shifting from reactive repairs to proactive interventions. Machine learning models can detect anomalies in system behavior, such as subtle changes in pressure or motor vibrations, indicating potential equipment failure before it occurs. This foresight enables timely maintenance, reducing downtime, extending the lifespan of refrigeration equipment, and preventing costly refrigerant leaks. The integration of AI into monitoring systems also enhances the safety of ammonia and hydrocarbon installations by providing early warning signals and enabling rapid response protocols, thereby mitigating risks associated with flammable or toxic refrigerants.

Beyond operational improvements, AI can contribute to the design and deployment phases by simulating complex system behaviors and identifying optimal configurations for natural refrigerant-based cooling. This allows manufacturers and system designers to develop more efficient and cost-effective solutions tailored to specific applications, accelerating market adoption. Furthermore, AI can aid in supply chain management for natural refrigerants and components, optimizing inventory levels and logistics, ensuring the timely availability of necessary resources. The confluence of AI with IoT (Internet of Things) devices will create intelligent, self-optimizing refrigeration networks, pushing the boundaries of efficiency and sustainability in the sector.

- Optimized energy consumption through real-time system adjustments.

- Enhanced predictive maintenance, reducing downtime and operational costs.

- Improved safety protocols for natural refrigerant systems through early anomaly detection.

- Accelerated design and simulation of efficient refrigeration systems.

- Streamlined supply chain and logistics for natural refrigerants.

- Integration with IoT for intelligent, self-regulating cooling networks.

- Data-driven decision-making for equipment upgrades and maintenance scheduling.

Key Takeaways Natural Refrigerant Market Size & Forecast

The Natural Refrigerant market is poised for robust growth, with a projected CAGR of 10.5% from 2025 to 2033, reaching USD 56.6 Billion by the end of the forecast period. This significant expansion underscores the industry's commitment to transitioning away from conventional synthetic refrigerants, driven by a global consensus on environmental protection and climate change mitigation. The growth trajectory highlights the increasing market acceptance and technological maturity of natural refrigerant solutions across diverse applications, from commercial supermarkets to heavy industrial processes. This indicates a strong investment potential and a shift towards sustainable practices within the cooling sector globally.

A crucial takeaway is the pervasive influence of regulatory mandates, such as the F-Gas Regulation in Europe and similar initiatives in North America and Asia, which are compelling industries to adopt natural alternatives. These regulations, coupled with growing corporate sustainability agendas, are creating an irreversible momentum for natural refrigerants. The forecast growth is not merely organic but is significantly accelerated by policy pressures and a rising awareness of the long-term economic and environmental benefits associated with these green technologies, including energy efficiency and lower total cost of ownership over time. The market is increasingly characterized by a focus on innovation that addresses specific application challenges and expands the reach of natural refrigerant solutions.

Furthermore, the market's trajectory indicates a shift towards a more diversified portfolio of natural refrigerants, with CO2, ammonia, and hydrocarbons each finding their niche based on application, scale, and regional preferences. The substantial increase in market value reflects not only volume growth but also continuous technological refinement and the emergence of new applications. For stakeholders, this signals a compelling opportunity to invest in research and development, manufacturing capabilities, and service infrastructure supporting natural refrigerant solutions, ensuring alignment with future market demands and environmental mandates. The market is becoming a cornerstone of sustainable infrastructure development, particularly in cold chain logistics and temperature-controlled environments.

- Strong projected CAGR of 10.5% indicating significant market expansion.

- Market value set to more than double from USD 25.5 Billion (2025) to USD 56.6 Billion (2033).

- Growth driven by stringent environmental regulations and corporate sustainability initiatives.

- Increased technological maturity and market acceptance of natural refrigerant solutions.

- Diverse portfolio of CO2, ammonia, and hydrocarbons gaining traction across applications.

- Favorable investment climate for R&D, manufacturing, and service in natural refrigerants.

Natural Refrigerant Market Drivers Analysis

The Natural Refrigerant market is primarily driven by a confluence of escalating environmental concerns and stringent global regulations aimed at phasing out ozone-depleting substances and high global warming potential (GWP) refrigerants. International agreements such as the Montreal Protocol and Kigali Amendment, alongside regional policies like the European F-Gas Regulation, are compelling industries worldwide to adopt eco-friendly cooling solutions. This regulatory push creates a significant demand for natural alternatives, which inherently possess low or zero GWP, positioning them as the preferred choice for future refrigeration and air conditioning systems. The increasing corporate focus on sustainability and ESG (Environmental, Social, and Governance) metrics further amplifies this demand, as companies strive to reduce their carbon footprint and demonstrate environmental stewardship. This alignment of policy and corporate responsibility is a foundational driver for market growth.

Another powerful driver is the growing awareness among consumers and industries regarding the energy efficiency and long-term cost benefits of natural refrigerant systems. While initial investment costs for natural refrigerant systems can sometimes be higher, their superior energy performance, especially in optimized systems like transcritical CO2, leads to significant operational savings over their lifecycle. Advances in compressor technology, heat exchangers, and system controls are continuously improving the efficiency of these systems. Furthermore, the inherent stability and longevity of natural refrigerants contribute to reduced maintenance needs and a lower total cost of ownership, making them an economically attractive option in the long run. The increasing availability of skilled technicians and improved service infrastructure also contributes to the ease of adoption and operational reliability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations (e.g., F-Gas Regulation) | +3.0% | Europe, North America, Japan, Australia | Short to Medium-term (2025-2029) |

| Growing Awareness of Climate Change & Sustainability Goals | +2.5% | Global, particularly developed economies | Medium to Long-term (2027-2033) |

| Enhanced Energy Efficiency of Natural Refrigerant Systems | +2.0% | Global, all sectors | Medium to Long-term (2026-2033) |

| Increasing Investment in Cold Chain Infrastructure | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium-term (2025-2030) |

Natural Refrigerant Market Restraints Analysis

Despite the strong growth drivers, the Natural Refrigerant market faces several notable restraints, primarily centered around the high initial capital investment required for these systems. Natural refrigerant-based equipment, particularly advanced CO2 transcritical systems and specialized ammonia installations, often come with higher upfront costs compared to traditional HFC-based systems. This cost differential can be a significant barrier for small and medium-sized enterprises (SMEs) or regions with limited access to capital, despite the long-term operational savings. The complexity of these systems also often requires specialized components and installation techniques, further contributing to the elevated initial expenditure. This economic hurdle necessitates supportive policies and financing mechanisms to accelerate broader adoption.

Another significant restraint involves the safety concerns associated with certain natural refrigerants and the need for specialized infrastructure and skilled labor. Ammonia, while highly efficient, is toxic and flammable, requiring strict safety protocols, leak detection systems, and dedicated ventilation. Similarly, hydrocarbons like propane are highly flammable, necessitating explosion-proof equipment and careful handling. The specific properties of CO2, which operates at very high pressures, demand robust and precise engineering. These inherent characteristics necessitate specialized training for installation, maintenance, and emergency response personnel, which is not yet universally available, especially in developing regions. A lack of widespread standardized training programs and certified technicians can hinder market penetration and adoption rates.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment Costs | -2.0% | Global, particularly emerging economies | Short to Medium-term (2025-2030) |

| Safety Concerns (Toxicity for NH3, Flammability for HCs) | -1.5% | Global, especially sensitive applications | Short to Medium-term (2025-2029) |

| Lack of Skilled Technicians and Specialized Infrastructure | -1.0% | Developing Regions, select developed countries | Medium-term (2026-2031) |

| System Complexity and High Operating Pressures (CO2) | -0.8% | Global, new installations | Short to Medium-term (2025-2028) |

Natural Refrigerant Market Opportunities Analysis

The Natural Refrigerant market presents significant opportunities for growth and innovation, particularly in the expansion into new application areas and untapped geographical markets. As regulatory pressures intensify globally, sectors traditionally reliant on synthetic refrigerants, such as small commercial refrigeration units, residential air conditioning, and mobile air conditioning (MAC) in vehicles, are increasingly exploring natural alternatives. Innovations in micro-channel heat exchangers and compact compressor designs are making CO2 and hydrocarbon systems viable for smaller-scale applications. Emerging economies in Asia Pacific, Latin America, and Africa, with their burgeoning populations and developing cold chain infrastructure, represent vast, underpenetrated markets where natural refrigerants can be introduced as the primary solution, bypassing the legacy HFC infrastructure.

Another compelling opportunity lies in the continuous technological advancements and the development of hybrid systems. Ongoing research and development are focused on improving the efficiency, safety, and cost-effectiveness of natural refrigerant technologies. This includes advancements in variable speed compressors, intelligent control systems, and heat recovery solutions that further enhance the energy performance of natural refrigerant systems. The integration of natural refrigerants with other sustainable technologies, such as solar power for refrigeration units or waste heat recovery systems, opens new avenues for energy-neutral or positive installations. Furthermore, the development of training and certification programs for technicians specifically on natural refrigerants represents a significant opportunity to address the skill gap and facilitate widespread adoption, transforming a restraint into an area of growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Applications (e.g., Residential HVAC, MAC) | +2.5% | Global, particularly developed markets | Medium to Long-term (2027-2033) |

| Growth in Emerging Economies & Developing Cold Chains | +2.0% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium-term (2025-2030) |

| Technological Advancements and Hybrid System Development | +1.8% | Global, R&D focused regions | Medium to Long-term (2026-2033) |

| Government Incentives and Green Building Initiatives | +1.2% | Europe, North America, Australia, parts of Asia | Short to Medium-term (2025-2029) |

Natural Refrigerant Market Challenges Impact Analysis

The Natural Refrigerant market faces significant challenges, particularly concerning the initial high costs and the complexity of system design and installation. While natural refrigerants offer long-term operational savings, the upfront capital expenditure for purchasing and installing systems that safely and efficiently utilize CO2, ammonia, or hydrocarbons can be considerably higher than conventional HFC systems. This cost barrier is exacerbated by the need for specialized, robust components capable of handling the unique pressures (for CO2) or flammability/toxicity (for ammonia and hydrocarbons), which often require custom engineering. The complexity involved in designing and integrating these systems, especially for retrofits or large-scale industrial applications, necessitates highly specialized expertise, further adding to the cost and project lead times. This complexity can deter smaller businesses or those with limited technical resources from adopting natural refrigerant solutions.

Another critical challenge is the persistent lack of a sufficiently large pool of skilled technicians trained in the installation, maintenance, and safe handling of natural refrigerants. Unlike synthetic refrigerants, natural refrigerants have specific characteristics that demand specialized knowledge and strict adherence to safety protocols. For example, servicing an ammonia refrigeration plant requires different training and certifications compared to an R410A system. The scarcity of adequately trained professionals can lead to higher service costs, potential safety hazards if systems are mishandled, and slower adoption rates, particularly in regions where training infrastructure is nascent. Bridging this skill gap through comprehensive training programs and certification schemes is crucial for the sustainable growth and widespread acceptance of natural refrigerant technologies. Overcoming these challenges will require concerted efforts from industry stakeholders, educational institutions, and regulatory bodies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Costs & System Complexity | -2.0% | Global, particularly cost-sensitive markets | Short to Medium-term (2025-2029) |

| Insufficient Skilled Workforce and Training Infrastructure | -1.8% | Developing Economies, parts of Developed Economies | Medium-term (2026-2031) |

| Competition from Low-GWP Synthetic Alternatives | -1.2% | Global, particularly in niche applications | Short to Medium-term (2025-2028) |

| Perception of Safety Risks (for Flammable/Toxic Refrigerants) | -1.0% | Global, public facing sectors | Short to Medium-term (2025-2030) |

Natural Refrigerant Market - Updated Report Scope

This comprehensive report delves into the Natural Refrigerant market, offering an in-depth analysis of its current landscape, historical performance, and future projections. It provides critical insights into market size estimations, growth drivers, restraints, opportunities, and challenges influencing the industry. The scope encompasses detailed segmentation analysis by refrigerant type, application, and end-use industry, alongside a thorough regional assessment to highlight key market dynamics across different geographies. Strategic profiling of major market players is also included, providing a holistic view of the competitive landscape and strategic initiatives shaping the market's evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 56.6 Billion |

| Growth Rate | 10.5% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Carrier Corporation, Johnson Controls International Plc, Danfoss A/S, Emerson Electric Co., Honeywell International Inc., Mayekawa Mfg. Co. Ltd., Daikin Industries Ltd., Mitsubishi Electric Corporation, Panasonic Corporation, Bitzer SE, Lu-Ve S.p.A., Embraco (Nidec Global Appliance), GEA Group Aktiengesellschaft, Arctic Circle Ltd., Lennox International Inc., Baltimore Aircoil Company (BAC), Alfa Laval AB, Güntner GmbH & Co. KG, Viessmann Group, Dorin S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Natural Refrigerant market is comprehensively segmented to provide a granular understanding of its diverse components and their respective market dynamics. Segmentation by type includes Carbon Dioxide (CO2), Ammonia (NH3), Hydrocarbons (Propane, Isobutane, Propylene, Ethane), Water, and Air. Each refrigerant type possesses unique properties, advantages, and ideal applications, influencing their adoption rates across different industries. CO2, for instance, is gaining traction in commercial refrigeration due to its non-flammable and non-toxic nature, while ammonia remains dominant in large-scale industrial applications due to its high efficiency and low cost.

Further segmentation is conducted by application, covering Commercial Refrigeration, Industrial Refrigeration, Air Conditioning & Heat Pumps, and Mobile Air Conditioning. Commercial refrigeration is a significant growth area driven by increasing demand from supermarkets and cold storage facilities seeking sustainable solutions. Industrial refrigeration, with its high cooling demands, continues to rely heavily on ammonia but is also exploring CO2 cascades. The Air Conditioning and Heat Pump sector represents a nascent but rapidly growing segment, particularly with the push for residential and commercial HVAC systems using natural refrigerants. Mobile Air Conditioning, especially in the automotive sector, is exploring CO2 as a long-term alternative to traditional refrigerants.

The market is also segmented by end-use industry, encompassing Food & Beverage, Chemical & Pharmaceutical, Oil & Gas, Healthcare, Retail, Logistics, Automotive, Building & Construction, and Data Centers. The Food & Beverage sector, including processing, storage, and retail, is a primary consumer of natural refrigerants due to stringent cold chain requirements and sustainability goals. The Chemical & Pharmaceutical industries also show increasing adoption for precise temperature control. Emerging applications in data centers and automotive further highlight the expanding scope of natural refrigerant technologies across diverse industrial and commercial landscapes, reflecting a broad-based shift towards eco-friendly cooling solutions.

- By Type:

- Carbon Dioxide (CO2)

- Ammonia (NH3)

- Hydrocarbons (Propane, Isobutane, Propylene, Ethane)

- Water

- Air

- By Application:

- Commercial Refrigeration

- Supermarkets

- Restaurants

- Cold Storage

- Display Cases

- Industrial Refrigeration

- Food & Beverage Processing

- Chemical

- Pharmaceutical

- Oil & Gas

- Air Conditioning & Heat Pumps

- Residential HVAC

- Commercial HVAC

- Industrial HVAC

- District Cooling/Heating

- Mobile Air Conditioning

- Automotive

- Transport Refrigeration

- Commercial Refrigeration

- By End-Use Industry:

- Food & Beverage

- Chemical & Pharmaceutical

- Oil & Gas

- Healthcare

- Retail

- Logistics

- Automotive

- Building & Construction

- Data Centers

Regional Highlights

The Natural Refrigerant market exhibits distinct regional dynamics, driven by varied regulatory landscapes, economic development, and environmental consciousness.

- North America: This region is a significant market, propelled by stringent environmental regulations, corporate sustainability initiatives, and technological advancements. The U.S. and Canada are actively phasing down HFCs, fostering innovation in CO2 and hydrocarbon systems for commercial refrigeration and industrial applications. Investment in energy-efficient solutions and a robust cold chain infrastructure also contribute to market growth.

- Europe: Europe is a frontrunner in the adoption of natural refrigerants, largely due to the stringent F-Gas Regulation and strong environmental policies. Countries like Germany, the UK, and the Nordic nations have been pioneers in implementing CO2 transcritical systems in supermarkets and ammonia-based industrial refrigeration. The region's focus on decarbonization and circular economy principles continues to drive significant market expansion.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, driven by rapid industrialization, urbanization, and increasing demand for cold chain solutions, particularly in China, India, Japan, and Southeast Asian countries. While some countries are still catching up on regulations, the sheer market size, growing environmental awareness, and rising energy costs are accelerating the adoption of natural refrigerants in commercial and industrial sectors. Government initiatives to develop sustainable infrastructure also play a crucial role.

- Latin America: This region is experiencing nascent but accelerating growth, influenced by global regulatory trends and increasing foreign investment in retail and food processing sectors. Brazil, Mexico, and Argentina are key countries where natural refrigerants, particularly CO2 and ammonia, are gaining traction in supermarkets and industrial cold storage, albeit with challenges related to initial costs and local technical expertise.

- Middle East and Africa (MEA): The MEA region is emerging as a potential growth market, driven by rising demand for refrigeration in burgeoning food retail, hospitality, and pharmaceutical sectors, especially in the GCC countries and South Africa. While adoption is slower due to a reliance on conventional technologies and less stringent regulations, increasing awareness of energy efficiency and sustainability, coupled with new construction projects, is creating opportunities for natural refrigerant systems.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Natural Refrigerant Market.- Carrier Corporation

- Johnson Controls International Plc

- Danfoss A/S

- Emerson Electric Co.

- Honeywell International Inc.

- Mayekawa Mfg. Co. Ltd.

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Bitzer SE

- Lu-Ve S.p.A.

- Embraco (Nidec Global Appliance)

- GEA Group Aktiengesellschaft

- Arctic Circle Ltd.

- Lennox International Inc.

- Baltimore Aircoil Company (BAC)

- Alfa Laval AB

- Güntner GmbH & Co. KG

- Viessmann Group

- Dorin S.p.A.

Frequently Asked Questions

What are natural refrigerants?

Natural refrigerants are naturally occurring substances used for cooling, possessing low or zero Global Warming Potential (GWP) and Ozone Depletion Potential (ODP). Common examples include carbon dioxide (CO2), ammonia (NH3), hydrocarbons (e.g., propane, isobutane), water, and air. They are considered environmentally friendly alternatives to synthetic refrigerants like HFCs, HFOs, and CFCs.

Why are natural refrigerants gaining popularity?

Natural refrigerants are gaining popularity primarily due to stringent environmental regulations phasing out high-GWP synthetic refrigerants, growing awareness of climate change, and their superior energy efficiency in many applications. They offer a sustainable solution to reduce carbon footprints and align with global sustainability goals, providing long-term operational cost savings.

What are the main applications of natural refrigerants?

Natural refrigerants are widely used across various applications including commercial refrigeration (supermarkets, cold storage), industrial refrigeration (food processing, chemical plants), residential and commercial air conditioning and heat pumps, and mobile air conditioning (automotive, transport refrigeration).

What are the challenges in adopting natural refrigerants?

Key challenges include higher initial capital costs for equipment, safety concerns associated with flammability (hydrocarbons) and toxicity (ammonia), and the need for a specialized and skilled workforce for installation and maintenance. Operating CO2 systems also involves handling high pressures, which requires robust system designs.

How does AI impact the natural refrigerant market?

AI significantly impacts the market by optimizing system performance for enhanced energy efficiency, enabling predictive maintenance to reduce downtime, and improving safety protocols through real-time monitoring and anomaly detection. AI also aids in accelerating system design and managing the supply chain for components, driving overall operational excellence.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted