Government Cloud Market

Government Cloud Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702045 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Government Cloud Market Size

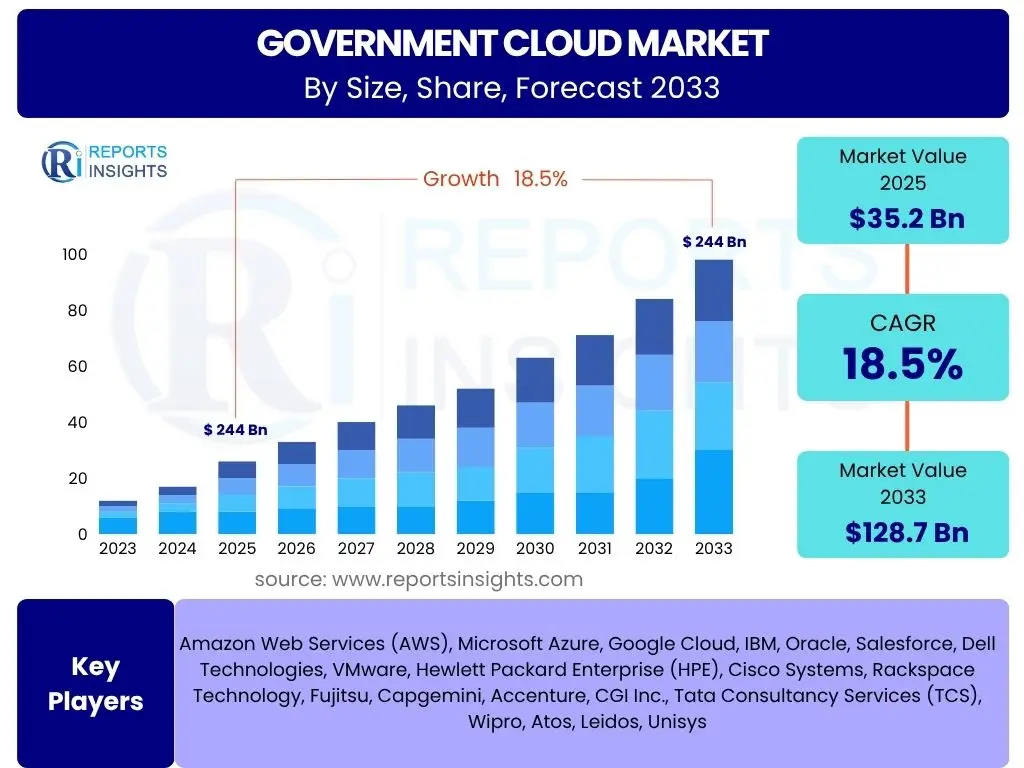

According to Reports Insights Consulting Pvt Ltd, The Government Cloud Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 35.2 billion in 2025 and is projected to reach USD 128.7 billion by the end of the forecast period in 2033.

Key Government Cloud Market Trends & Insights

The Government Cloud market is currently undergoing significant transformation, driven by an urgent need for digital modernization across public sector entities globally. Key trends indicate a definitive shift towards more agile, scalable, and secure IT infrastructures, moving away from traditional on-premise solutions. Governments are increasingly recognizing the strategic imperative of cloud adoption to enhance public service delivery, streamline operations, and bolster national security. This evolution is underpinned by a growing emphasis on data sovereignty and compliance, leading to the development of specialized government-grade cloud offerings.

Furthermore, the market is observing a strong preference for hybrid and multi-cloud strategies, allowing agencies to leverage the benefits of various cloud environments while maintaining control over sensitive data. There is also a notable surge in the adoption of cloud-native technologies, including containers and serverless computing, to accelerate application development and deployment. The integration of advanced analytics and artificial intelligence capabilities within cloud platforms is becoming critical for data-driven decision-making and operational efficiencies, marking a new era of intelligent government services.

- Accelerated digital transformation and modernization initiatives across government agencies.

- Rising adoption of hybrid and multi-cloud strategies for flexibility and resilience.

- Increased focus on data sovereignty, security, and compliance tailored for public sector needs.

- Growing demand for cloud-native technologies, including microservices and serverless architectures.

- Integration of advanced analytics and Artificial Intelligence (AI) for enhanced decision-making.

- Emphasis on green IT and sustainable cloud solutions to reduce carbon footprint.

AI Impact Analysis on Government Cloud

Artificial intelligence is rapidly transforming the landscape of government cloud computing, fundamentally altering how public services are delivered and managed. The integration of AI within government cloud environments is driven by the imperative to process vast datasets, derive actionable insights, and automate complex tasks, thereby enhancing operational efficiency and responsiveness. Governments are exploring AI for applications ranging from predictive analytics for policy-making and resource allocation to intelligent automation of administrative processes and advanced cybersecurity threat detection. This integration necessitates robust, scalable, and secure cloud infrastructure capable of supporting AI workloads, driving demand for specialized AI-ready cloud services.

However, the widespread adoption of AI in government clouds also brings forth significant considerations regarding data privacy, ethical AI deployment, and the potential for algorithmic bias. Public sector entities are keen on leveraging AI's transformative power but are equally concerned about ensuring transparency, accountability, and citizen trust. This leads to a demand for cloud solutions that offer strong governance frameworks, explainable AI capabilities, and secure data handling protocols. The synergy between AI and cloud computing is expected to unlock unprecedented capabilities for governments, from smarter cities and improved public health systems to more secure defense infrastructures, making AI a central pillar of future government cloud strategies.

- Enhanced data processing and analytical capabilities, enabling deeper insights from government data.

- Automation of routine administrative tasks, leading to significant operational efficiencies.

- AI-driven cybersecurity for proactive threat detection and robust defense of government assets.

- Development of intelligent public services, such as smart city applications and citizen support systems.

- Demand for specialized cloud infrastructure optimized for AI and machine learning workloads.

- Increased focus on ethical AI guidelines, transparency, and data privacy within cloud deployments.

Key Takeaways Government Cloud Market Size & Forecast

The Government Cloud market is poised for robust and sustained growth over the forecast period, reflecting a critical shift in public sector IT strategies worldwide. The significant projected CAGR and market size indicate that governments are increasingly committed to leveraging cloud technologies for their inherent benefits in scalability, cost-efficiency, and innovation. This growth is not merely a technological upgrade but a fundamental re-platforming of government operations, aiming for greater agility, resilience, and improved citizen services in a rapidly evolving digital landscape. The forecast underscores the essential role of cloud computing in national digital transformation agendas.

A primary takeaway is the accelerating momentum behind digital government initiatives, which form the bedrock of cloud adoption. The demand for secure, compliant, and sovereign cloud solutions will continue to drive investments, particularly in hybrid and private cloud deployments that cater to the unique security and regulatory needs of the public sector. The market's expansion is also testament to the growing understanding among government leaders of cloud's capacity to foster innovation, enhance data security, and support critical functions from defense to public health. This period will see an emphasis on strategic partnerships between cloud providers and government agencies to tailor solutions that meet specific public sector requirements.

- The market is undergoing rapid expansion, driven by widespread government digital transformation mandates.

- Significant investment is directed towards enhancing public sector efficiency and service delivery through cloud adoption.

- Security, data sovereignty, and regulatory compliance remain paramount considerations driving cloud solution design.

- Hybrid and multi-cloud models are gaining prominence due to their flexibility and ability to meet diverse agency needs.

- Cloud technology is becoming integral to national infrastructure, supporting critical services and innovation.

Government Cloud Market Drivers Analysis

The Government Cloud market is primarily driven by the global imperative for digital transformation within public sector organizations. Governments worldwide are under increasing pressure to modernize their legacy IT infrastructures, enhance citizen services, and improve operational efficiencies, all of which are significantly facilitated by cloud computing. The inherent scalability and flexibility of cloud solutions enable agencies to rapidly adapt to changing demands, deploy new services, and manage fluctuating workloads without substantial upfront capital expenditure, making it an attractive alternative to traditional on-premise systems.

Furthermore, the escalating volume of government data, coupled with the need for advanced analytics and artificial intelligence capabilities, necessitates robust and scalable cloud platforms. Cloud environments provide the foundational infrastructure required to process, store, and analyze large datasets, supporting data-driven policy-making and fostering innovation across various government functions. The ongoing efforts to reduce operational costs and optimize resource allocation also serve as powerful drivers, as cloud models often shift IT spending from CapEx to OpEx, providing financial agility and predictability. Lastly, the heightened focus on cybersecurity and disaster recovery planning post-pandemic has compelled governments to adopt more resilient cloud architectures that offer enhanced security features and business continuity capabilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation Initiatives | +3.2% | Global, particularly North America, Europe, and APAC | 2025-2033 (Long-term) |

| Need for Cost Efficiency & Scalability | +2.8% | Global | 2025-2033 (Long-term) |

| Increasing Cybersecurity Threats | +2.5% | Global, prominent in developed economies | 2025-2030 (Medium-term) |

| Data Proliferation & Analytics Demand | +2.0% | Global | 2025-2033 (Long-term) |

| Post-Pandemic Resiliency & Business Continuity | +1.5% | Global | 2025-2028 (Short-to-Medium term) |

Government Cloud Market Restraints Analysis

Despite the compelling drivers for cloud adoption, the Government Cloud market faces several significant restraints that could impede its growth. One of the primary concerns is the stringent regulatory and compliance requirements unique to government data. Public sector data, often sensitive and critical, is subject to numerous national and international regulations concerning data sovereignty, privacy, and security. Adhering to these complex compliance frameworks can be challenging for cloud providers and government agencies alike, requiring specialized certifications and continuous audits, which can slow down adoption and increase operational overhead.

Another substantial restraint is the pervasive issue of legacy IT infrastructure. Many government agencies operate on decades-old systems that are deeply integrated and difficult to migrate to cloud environments. The cost, complexity, and disruption associated with modernizing these legacy systems, coupled with a general resistance to change within bureaucratic structures, often act as significant barriers. Furthermore, concerns about vendor lock-in, where agencies become overly dependent on a single cloud provider's proprietary technologies, pose a challenge. Governments seek flexibility and interoperability, and the fear of being unable to switch providers easily can deter full cloud commitment, driving a preference for hybrid or multi-cloud strategies that mitigate this risk.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Regulatory & Compliance Requirements | -1.8% | Global, particularly EU (GDPR), US (FedRAMP) | 2025-2033 (Long-term) |

| Legacy IT Infrastructure & Migration Challenges | -1.5% | Global, prominent in established economies | 2025-2033 (Long-term) |

| Data Sovereignty Concerns | -1.2% | Global, highly relevant in Europe, Asia Pacific | 2025-2033 (Long-term) |

| Vendor Lock-in Fears & Interoperability Issues | -0.8% | Global | 2025-2030 (Medium-term) |

Government Cloud Market Opportunities Analysis

The Government Cloud market presents significant opportunities for growth, primarily through the expansion of specialized, government-specific cloud offerings. As public sector entities increasingly demand solutions tailored to their unique compliance, security, and operational needs, providers capable of delivering "government-ready" or sovereign cloud environments will find substantial market traction. This includes developing dedicated regions, enhanced security features, and accreditation for specific government standards, thereby addressing the core concerns that have traditionally slowed cloud adoption within this sector. The rise of community clouds, designed to serve a specific group of government organizations with shared interests and security requirements, also represents a burgeoning opportunity for niche market penetration and collaborative resource sharing.

Furthermore, the growing emphasis on smart city initiatives and the widespread adoption of emerging technologies like Artificial Intelligence (AI), Machine Learning (ML), and Edge Computing create new avenues for cloud service providers. Governments are seeking cloud platforms that can effectively support these data-intensive and computationally demanding applications, enabling real-time analytics for urban planning, public safety, and infrastructure management. The ongoing digital transformation in developing economies, coupled with their relatively nascent cloud adoption rates, offers greenfield opportunities for providers to establish foundational cloud infrastructures and services. Partnerships with local system integrators and technology providers in these regions can facilitate market entry and accelerate the adoption of cloud solutions tailored to local requirements and growth trajectories.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sovereign & Community Clouds | +2.5% | Europe, Asia Pacific, select North America | 2025-2033 (Long-term) |

| Integration of AI, ML, and Edge Computing | +2.2% | Global, especially developed nations | 2025-2033 (Long-term) |

| Smart City and IoT Initiatives | +1.8% | Global, prominent in urban areas | 2025-2030 (Medium-term) |

| Digital Transformation in Developing Economies | +1.5% | Asia Pacific, Latin America, MEA | 2025-2033 (Long-term) |

Government Cloud Market Challenges Impact Analysis

The Government Cloud market faces several critical challenges that can impede seamless adoption and deployment. A significant hurdle is the persistent skills gap within government agencies. Many public sector organizations lack the in-house expertise required to effectively plan, implement, and manage complex cloud environments, including cloud architecture, cybersecurity, and data analytics. This necessitates reliance on external consultants or extensive training programs, which can add to costs and project timelines, slowing the pace of cloud migration and optimization. The recruitment and retention of skilled cloud professionals are also difficult for governments, often due to competitive private sector salaries and opportunities.

Another major challenge revolves around complex procurement processes and bureaucratic inertia. Government procurement cycles are notoriously lengthy and rigid, making it difficult for agencies to quickly adopt innovative cloud technologies or adapt to rapidly evolving market offerings. The inherent resistance to change within large governmental organizations, coupled with risk aversion and fragmented decision-making, can significantly delay or even halt cloud initiatives. Furthermore, ensuring seamless interoperability between various cloud services and existing legacy systems, as well as between different cloud providers in a multi-cloud strategy, remains a technical challenge. Achieving consistent data formats, API compatibility, and integrated security policies across disparate environments requires significant effort and expertise, impacting the efficiency and cost-effectiveness of cloud deployments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Skills Gap & Workforce Development | -1.0% | Global | 2025-2033 (Long-term) |

| Complex Procurement Processes & Bureaucracy | -0.9% | Global, pronounced in highly regulated countries | 2025-2030 (Medium-term) |

| Interoperability & Integration with Legacy Systems | -0.7% | Global | 2025-2033 (Long-term) |

| Funding & Budget Constraints | -0.5% | Global, variable by region/country economic health | 2025-2030 (Medium-term) |

Government Cloud Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Government Cloud market, offering a detailed overview of its current size, historical performance, and future growth projections. The scope includes a thorough examination of key market trends, significant drivers, formidable restraints, emerging opportunities, and prevailing challenges influencing the market's trajectory. Furthermore, the report delves into the impact of Artificial Intelligence on government cloud solutions, presenting a nuanced perspective on its transformative potential. It also covers extensive market segmentation by various categories and provides regional insights, offering a holistic view of the market dynamics essential for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.2 Billion |

| Market Forecast in 2033 | USD 128.7 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM, Oracle, Salesforce, Dell Technologies, VMware, Hewlett Packard Enterprise (HPE), Cisco Systems, Rackspace Technology, Fujitsu, Capgemini, Accenture, CGI Inc., Tata Consultancy Services (TCS), Wipro, Atos, Leidos, Unisys |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Government Cloud market is comprehensively segmented to provide a detailed understanding of its diverse components and adoption patterns across various government functions and infrastructure types. This segmentation allows for a granular analysis of how different service models, deployment strategies, and government levels are contributing to the market's growth and evolving needs. Each segment reflects specific requirements and opportunities, enabling stakeholders to identify key areas of investment and strategic focus. Understanding these segmentations is crucial for tailoring cloud solutions that meet the distinct demands of public sector organizations, from federal defense agencies to local municipal services.

The market is primarily broken down by service model, including Infrastructure as a Service (IaaS) for fundamental computing resources, Platform as a Service (PaaS) for development and deployment environments, and Software as a Service (SaaS) for ready-to-use applications. Deployment models differentiate between Public, Private, Hybrid, and Community Clouds, each chosen based on varying levels of security, control, and compliance needs. Furthermore, the segmentation by government level highlights the distinct requirements of federal, state, local, and defense entities, while application-based segmentation showcases the diverse use cases for cloud across governmental operations, from data storage to advanced analytics and security management.

- By Service Model:

- IaaS (Infrastructure as a Service): Provides fundamental computing resources, including virtualized servers, networking, and storage.

- PaaS (Platform as a Service): Offers a platform for developers to build, run, and manage applications without managing underlying infrastructure.

- SaaS (Software as a Service): Delivers ready-to-use software applications over the internet, typically on a subscription basis.

- By Deployment Model:

- Private Cloud: Dedicated cloud infrastructure used exclusively by a single government organization, often on-premise or hosted by a third party.

- Public Cloud: Cloud services offered by third-party providers over the public internet, shared among multiple tenants.

- Hybrid Cloud: A combination of private and public cloud environments, allowing data and applications to be shared between them.

- Community Cloud: Shared cloud infrastructure for a specific community of organizations with shared concerns, e.g., multiple government agencies.

- By Government Level:

- Federal Government: Includes national-level ministries, departments, and agencies.

- State & Local Government: Encompasses regional and municipal government bodies.

- Defense & Military: Specific cloud solutions for national defense and armed forces operations.

- Public Sector Agencies: Other non-federal/state entities, such as public health organizations, educational institutions, and utilities.

- By Application:

- Storage & Backup: Cloud-based solutions for data storage, archiving, and disaster recovery.

- Disaster Recovery: Services ensuring business continuity and data accessibility in case of system failures or disasters.

- Data Analytics: Cloud platforms for processing, analyzing, and deriving insights from large datasets.

- Identity & Access Management (IAM): Solutions for managing digital identities and controlling access to resources.

- Security Management: Cloud-based tools and services for comprehensive cybersecurity, threat detection, and compliance.

- CRM (Customer Relationship Management): Cloud-hosted systems for managing citizen interactions and services.

- ERP (Enterprise Resource Planning): Integrated cloud software for managing core business processes across an organization.

- Content Management: Solutions for creating, managing, and distributing digital content and documents.

- Others: Includes specialized applications like GIS (Geographic Information Systems), HR, and financial management.

Regional Highlights

- North America: This region is a dominant force in the Government Cloud market, driven by substantial federal spending, extensive digital transformation initiatives, and the early adoption of cloud technologies. Countries like the United States and Canada are leading in the implementation of secure government-specific cloud frameworks, such as FedRAMP in the U.S., which foster a robust ecosystem for cloud service providers. The region benefits from a mature IT infrastructure and a strong focus on enhancing national security, citizen services, and data analytics capabilities through cloud adoption.

- Europe: Europe is characterized by a strong emphasis on data sovereignty, privacy (under GDPR), and specific national cloud strategies (e.g., G-Cloud in the UK, Gaia-X in Germany/France). This drives demand for highly secure, localized, and compliant cloud solutions, often favoring private and hybrid cloud models. While adoption might be slower than in North America due to regulatory complexities and diverse national policies, there is significant growth driven by EU-level digital initiatives and public sector modernization programs. Countries like the UK, Germany, and France are key contributors to market expansion.

- Asia Pacific (APAC): The APAC region is experiencing the most rapid growth in the Government Cloud market, fueled by accelerating digital transformation efforts, smart city initiatives, and increasing investments in IT infrastructure across emerging economies like India, China, and Southeast Asian nations. Governments in this region are prioritizing cloud adoption to improve public service delivery, support economic development, and enhance disaster management capabilities. While cost-efficiency and scalability are primary drivers, concerns around data localization and cybersecurity are also gaining prominence, shaping the deployment models.

- Latin America: This region is witnessing nascent but steady growth in government cloud adoption. Countries like Brazil and Mexico are increasingly investing in cloud technologies to modernize public administration, improve transparency, and enhance citizen services. The market here is driven by the need for cost optimization, scalability, and improved data management. While challenges related to budget constraints and digital literacy persist, the growing awareness of cloud benefits is creating new opportunities for market expansion and public sector innovation.

- Middle East and Africa (MEA): The MEA region presents a significant long-term growth opportunity, particularly in the Middle East with its ambitious smart city projects and digital transformation agendas in countries like UAE and Saudi Arabia. African nations are also gradually increasing their cloud adoption, driven by the need for modern infrastructure, improved governance, and enhanced public service access. Cybersecurity remains a critical concern, leading to demand for robust, secure, and often regionally hosted cloud solutions. Investments in data centers and cloud infrastructure are expanding across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Government Cloud Market.- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- IBM

- Oracle

- Salesforce

- Dell Technologies

- VMware

- Hewlett Packard Enterprise (HPE)

- Cisco Systems

- Rackspace Technology

- Fujitsu

- Capgemini

- Accenture

- CGI Inc.

- Tata Consultancy Services (TCS)

- Wipro

- Atos

- Leidos

- Unisys

Frequently Asked Questions

What is the Government Cloud Market?

The Government Cloud Market refers to the provision of cloud computing services, including Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), specifically tailored for public sector organizations at federal, state, local, and defense levels. These services are designed to meet stringent government requirements for security, compliance, data sovereignty, and operational resilience, supporting digital transformation initiatives and enhancing public service delivery.

Why are governments increasingly adopting cloud solutions?

Governments are adopting cloud solutions to achieve greater operational efficiency, reduce IT costs, enhance scalability and agility for public services, and improve data security. Cloud platforms enable rapid deployment of new applications, facilitate advanced data analytics, support remote work capabilities, and provide robust disaster recovery options, all crucial for modernizing public administration and responding effectively to evolving citizen needs and unforeseen crises.

What are the primary security concerns for government cloud adoption?

The primary security concerns for government cloud adoption include data sovereignty, ensuring data remains within national borders; compliance with specific regulatory frameworks like FedRAMP or GDPR; protecting highly sensitive information from cyber threats; and managing access control effectively. Governments require cloud solutions with advanced encryption, robust access management, continuous monitoring, and proven track records of securing sensitive public sector data against sophisticated attacks.

What types of cloud deployment models are most popular in the government sector?

In the government sector, hybrid cloud and private cloud deployment models are particularly popular due to their ability to balance the benefits of cloud with strict security and compliance needs. Private clouds offer dedicated infrastructure and greater control over sensitive data, while hybrid clouds allow governments to leverage the scalability of public cloud for less sensitive workloads while keeping critical data on a private infrastructure. Community clouds, designed for specific government groups, are also gaining traction.

How does Artificial Intelligence (AI) impact the Government Cloud market?

AI significantly impacts the Government Cloud market by driving demand for advanced processing capabilities, enabling intelligent automation of public services, enhancing cybersecurity through predictive analytics, and supporting data-driven policy-making. Cloud platforms provide the scalable infrastructure necessary to run complex AI and machine learning workloads, facilitating the development of smart cities, optimizing resource allocation, and improving citizen engagement through AI-powered applications, all while raising considerations for ethical deployment and data privacy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted