Cloud Storage and File Sharing Service Market

Cloud Storage and File Sharing Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705790 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Cloud Storage and File Sharing Service Market Size

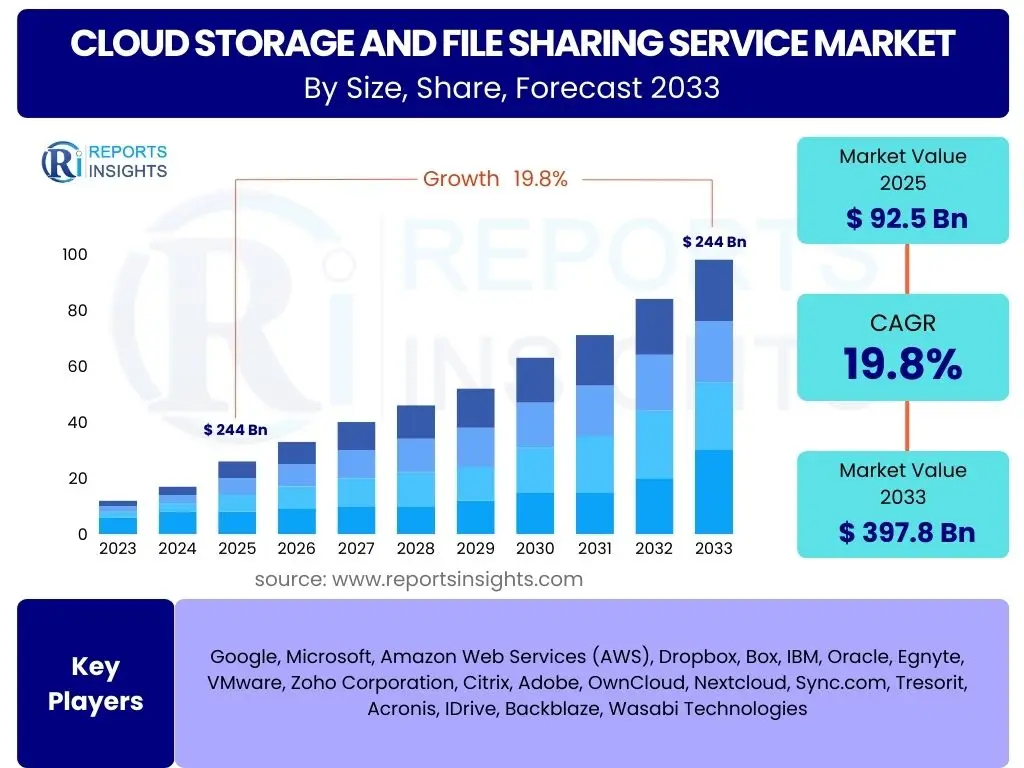

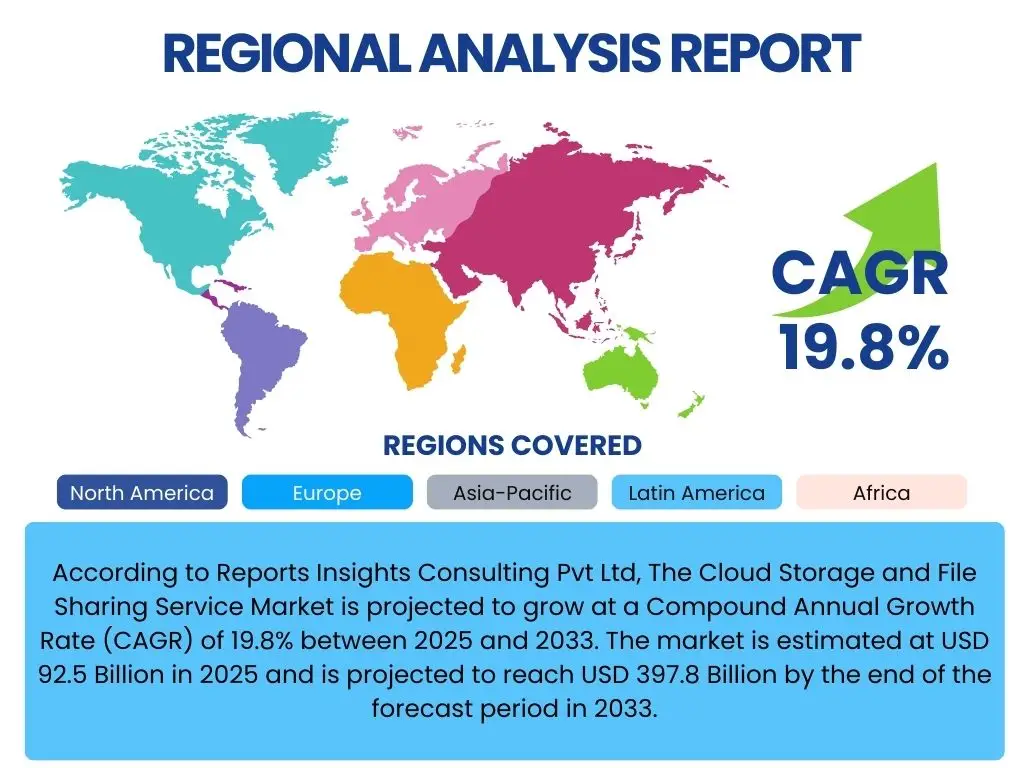

According to Reports Insights Consulting Pvt Ltd, The Cloud Storage and File Sharing Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.8% between 2025 and 2033. The market is estimated at USD 92.5 Billion in 2025 and is projected to reach USD 397.8 Billion by the end of the forecast period in 2033.

Key Cloud Storage and File Sharing Service Market Trends & Insights

The Cloud Storage and File Sharing Service market is undergoing significant transformation, driven by the escalating volume of digital data and the imperative for secure, accessible, and collaborative data management solutions. Enterprises and individuals are increasingly seeking flexible infrastructure that supports remote workforces and distributed operations. This trend is characterized by a strong move towards hybrid and multi-cloud strategies, allowing organizations to optimize costs, enhance resilience, and comply with diverse regulatory requirements across various cloud environments. The emphasis is shifting from mere storage to intelligent data management, encompassing advanced features for data lifecycle management, compliance, and real-time synchronization.

Another prominent trend involves the heightened focus on data sovereignty and compliance. As global regulations like GDPR and CCPA become more stringent, businesses are prioritizing solutions that offer granular control over data location and access, ensuring adherence to regional laws. Furthermore, the integration of advanced security features, such as end-to-end encryption, robust access controls, and threat detection mechanisms, is no longer optional but a fundamental requirement. The proliferation of rich media content and large datasets from IoT devices also necessitates scalable and high-performance storage solutions, driving innovation in file synchronization and sharing technologies that can handle diverse data types efficiently.

- Exponential data growth driving demand for scalable infrastructure.

- Increased adoption of hybrid and multi-cloud strategies for flexibility and resilience.

- Heightened focus on data security, privacy, and regulatory compliance (e.g., GDPR, CCPA).

- Rising demand for advanced collaboration tools integrated with file sharing services.

- Emergence of edge computing requiring distributed and localized storage capabilities.

- Development of intelligent data management features like automatic tiering and lifecycle management.

- Sustainability concerns influencing demand for energy-efficient cloud infrastructure.

AI Impact Analysis on Cloud Storage and File Sharing Service

Artificial intelligence is profoundly reshaping the cloud storage and file sharing landscape by introducing unprecedented levels of automation, optimization, and intelligence into data management. Organizations are keen to understand how AI can alleviate the complexities associated with massive data volumes, particularly concerning data organization, retrieval, and security. AI-powered algorithms are being deployed to automate mundane tasks like data classification, deduplication, and archival, thereby significantly reducing operational overhead and improving storage efficiency. Users are exploring how AI can transform unstructured data into actionable insights, enabling more efficient search capabilities and better decision-making processes within their collaborative environments.

The impact of AI extends significantly into security and compliance, addressing major concerns about data breaches and regulatory adherence. AI-driven analytics can detect anomalous activities, predict potential security threats, and automatically enforce compliance policies, providing a proactive defense mechanism for sensitive data. Furthermore, AI is crucial for optimizing storage resource allocation by dynamically adjusting capacity based on usage patterns and predicting future needs, ensuring cost-effectiveness and performance. There is a growing expectation that AI will deliver more intuitive user experiences through intelligent search, personalized recommendations, and self-healing storage systems, though concerns persist regarding the ethical implications of AI in data access and the potential for bias in automated decision-making.

- AI-driven data optimization, including intelligent tiering and deduplication, to enhance storage efficiency.

- Automated data classification and tagging for improved organization and retrieval.

- Enhanced security features through AI-powered threat detection, anomaly detection, and access control.

- Predictive analytics for storage capacity planning and resource allocation.

- Improved data governance and compliance automation through AI-driven policy enforcement.

- Intelligent search and discovery capabilities for faster access to relevant information.

- Development of self-healing and self-optimizing storage systems through machine learning.

Key Takeaways Cloud Storage and File Sharing Service Market Size & Forecast

The Cloud Storage and File Sharing Service market is poised for robust and sustained growth through the forecast period, reflecting its integral role in modern digital infrastructure. The significant projected increase in market size underscores the intensifying adoption of cloud-based solutions across enterprises of all scales, driven by the ongoing digital transformation initiatives, the proliferation of remote and hybrid work models, and the exponential generation of data from diverse sources. This expansion is not merely about storage capacity but also about the increasing sophistication of services offered, including enhanced security, seamless collaboration features, and intelligent data management capabilities.

The market's trajectory indicates that cloud storage and file sharing are no longer supplementary but foundational technologies for business continuity, innovation, and competitive advantage. The growth forecast highlights the immense opportunities for service providers to innovate in areas such as hybrid cloud solutions, industry-specific applications, and integrating emerging technologies like AI and edge computing. Companies that can deliver highly secure, compliant, scalable, and user-friendly solutions will be well-positioned to capitalize on this expanding market, catering to the evolving needs for efficient and resilient data ecosystems.

- The market exhibits strong growth potential, driven by global digital transformation.

- Cloud storage and file sharing are becoming essential for enterprise operations and remote work.

- Significant opportunities exist in providing specialized, secure, and compliant solutions.

- Innovation in hybrid cloud, AI integration, and edge computing will be key growth enablers.

- Demand for scalable and collaborative data management solutions will continue to accelerate.

Cloud Storage and File Sharing Service Market Drivers Analysis

The primary drivers propelling the Cloud Storage and File Sharing Service market forward are intrinsically linked to the global digital transformation and the evolving nature of work. Enterprises across all sectors are rapidly migrating their IT infrastructure and data to the cloud to achieve greater operational efficiency, scalability, and cost optimization. This shift is particularly pronounced as organizations seek to reduce reliance on expensive on-premises hardware and gain the flexibility to scale storage resources up or down dynamically based on fluctuating business needs. The inherent agility of cloud services allows businesses to respond quickly to market changes and innovate at an accelerated pace, providing a compelling alternative to traditional storage methods.

Furthermore, the widespread adoption of remote and hybrid work models has significantly amplified the demand for robust cloud storage and file sharing solutions. These services facilitate seamless collaboration among geographically dispersed teams, enabling real-time document editing, version control, and secure access to critical files from any location and device. The explosion of data, driven by IoT, big data analytics, and rich media content, necessitates scalable and cost-effective storage solutions that traditional infrastructure often struggles to provide. Cloud storage offers unlimited capacity and advanced data management tools to handle these massive datasets, while file sharing platforms ensure that this data can be effectively distributed and accessed by authorized personnel, fostering productivity and connectivity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation Initiatives | +2.5% | Global | Short to Mid-term (2025-2029) |

| Increasing Remote and Hybrid Work Models | +1.8% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Explosive Growth of Data (Big Data, IoT) | +2.0% | Global | Long-term (2025-2033) |

| Cost Efficiency and Scalability Benefits | +1.5% | Global (especially SMEs) | Short to Long-term (2025-2033) |

Cloud Storage and File Sharing Service Market Restraints Analysis

Despite the strong growth drivers, the Cloud Storage and File Sharing Service market faces several significant restraints that could temper its expansion. Foremost among these are persistent concerns regarding data security and privacy. Organizations, especially those handling sensitive information like financial or healthcare data, remain wary of storing critical assets with third-party providers due to potential vulnerabilities, cyberattacks, and unauthorized access. High-profile data breaches in the past have amplified these anxieties, prompting a cautious approach from businesses that prioritize the integrity and confidentiality of their data above all else. Addressing these security perceptions through robust encryption, access controls, and transparent security practices is critical for wider adoption.

Another substantial restraint is the complexity of regulatory compliance and data sovereignty requirements. Different countries and regions impose distinct laws on where data can be stored and how it must be handled (e.g., GDPR in Europe, CCPA in California). This patchwork of regulations creates significant challenges for global businesses seeking a unified cloud strategy, often forcing them to adopt fragmented solutions or incur additional costs to ensure compliance. Furthermore, the issue of vendor lock-in poses a considerable barrier, as migrating large volumes of data and applications from one cloud provider to another can be a complex, time-consuming, and expensive endeavor. This potential for vendor dependency often discourages organizations from fully committing to a single cloud provider, leading to slower adoption rates or a preference for hybrid solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security and Privacy Concerns | -1.5% | Global | Short to Mid-term (2025-2030) |

| Regulatory Compliance and Data Sovereignty | -1.0% | Europe, Asia Pacific, Developing Regions | Long-term (2025-2033) |

| Vendor Lock-in and Migration Complexity | -0.8% | Global (Large Enterprises) | Mid to Long-term (2027-2033) |

| Dependency on High-Speed Internet Connectivity | -0.5% | Rural Areas, Emerging Markets | Short to Mid-term (2025-2029) |

Cloud Storage and File Sharing Service Market Opportunities Analysis

The Cloud Storage and File Sharing Service market presents numerous opportunities for innovation and growth, particularly through the expansion of hybrid and multi-cloud environments. As organizations seek to balance the benefits of public cloud with the control of private infrastructure, hybrid cloud solutions offer a compelling pathway, allowing data and applications to reside in the most appropriate environment. This approach mitigates concerns around data sovereignty and security while still leveraging the scalability of public cloud services. The increasing complexity of enterprise IT landscapes further fuels the demand for multi-cloud strategies, enabling businesses to avoid vendor lock-in and optimize for specific workloads across various cloud providers. Solutions that offer seamless data synchronization, consistent management, and unified security policies across these disparate environments will find significant market traction.

Another significant opportunity lies in the integration of emerging technologies such as Artificial Intelligence (AI) and Machine Learning (ML), and Edge Computing. AI/ML can transform raw stored data into actionable intelligence, enabling predictive analytics, automated data management, and enhanced security protocols. Services that embed these capabilities will deliver greater value beyond mere storage, driving efficiency and insights for users. Furthermore, the proliferation of IoT devices and the need for low-latency data processing at the source are creating new demand for edge computing, where data is processed closer to its origin. Cloud storage and file sharing solutions that extend seamlessly to the edge, offering localized storage and synchronization with centralized cloud infrastructure, will capture a growing segment of the market focused on real-time data analysis and distributed operations. Specialized solutions tailored to specific industry verticals (e.g., healthcare, media, finance) also represent a fertile ground for growth, addressing unique compliance, security, and performance requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Hybrid and Multi-Cloud Deployments | +2.2% | Global (Large Enterprises) | Mid to Long-term (2027-2033) |

| Integration with AI and Machine Learning | +2.0% | Global | Mid to Long-term (2027-2033) |

| Growth in Edge Computing and IoT Data | +1.7% | North America, Europe, Asia Pacific | Long-term (2029-2033) |

| Development of Industry-Specific Solutions | +1.5% | Global (Healthcare, BFSI, Media) | Short to Long-term (2025-2033) |

Cloud Storage and File Sharing Service Market Challenges Impact Analysis

The Cloud Storage and File Sharing Service market faces significant challenges related to data migration and interoperability, particularly for established enterprises with legacy systems. Moving vast quantities of existing data, applications, and workflows from on-premises infrastructure to the cloud can be a highly complex, time-consuming, and resource-intensive undertaking. This process often involves managing data consistency, ensuring compatibility between diverse systems, and mitigating downtime, posing substantial technical and operational hurdles. Furthermore, ensuring seamless interoperability between different cloud environments and between cloud and on-premises systems remains a challenge, hindering the fluid movement and management of data across hybrid and multi-cloud architectures. Businesses must carefully plan and execute these migrations, often requiring specialized expertise and tools, which adds to the overall cost and complexity of cloud adoption.

Another critical challenge stems from the ever-evolving cybersecurity threat landscape. Cloud environments, while inherently designed with robust security measures, are still attractive targets for cybercriminals due to the aggregation of vast amounts of data. The sophistication of ransomware attacks, phishing attempts, and other malicious activities continues to increase, demanding continuous investment in advanced security technologies, threat intelligence, and skilled security personnel. Ensuring data sovereignty and compliance with a burgeoning array of international and regional regulations (such as data localization laws) also presents a persistent challenge for global service providers and their clients. The costs associated with securing data, ensuring compliance, and managing complex hybrid environments can be substantial, potentially deterring some organizations, especially Small and Medium-sized Enterprises (SMEs), from fully embracing cloud solutions due to perceived high initial investments or ongoing operational expenditures.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Data Migration and Interoperability | -0.7% | Global (especially large legacy enterprises) | Short to Mid-term (2025-2030) |

| Evolving Cybersecurity Threats and Data Breaches | -1.1% | Global | Long-term (2025-2033) |

| Compliance with Diverse Data Sovereignty Laws | -1.2% | Europe, China, India | Long-term (2025-2033) |

| High Initial Investment and Ongoing Cost Management | -0.9% | SMEs, Developing Economies | Short to Mid-term (2025-2029) |

Cloud Storage and File Sharing Service Market - Updated Report Scope

This report provides a comprehensive analysis of the Cloud Storage and File Sharing Service Market, covering historical data, current market conditions, and future projections from 2025 to 2033. It delves into the key market trends, growth drivers, restraints, opportunities, and challenges shaping the industry. The scope includes an in-depth segmentation analysis by deployment model, end-user, service type, and industry vertical, along with detailed regional insights. The report also highlights the competitive landscape, profiling leading market players and their strategies, offering a holistic view for stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 92.5 Billion |

| Market Forecast in 2033 | USD 397.8 Billion |

| Growth Rate | 19.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Google, Microsoft, Amazon Web Services (AWS), Dropbox, Box, IBM, Oracle, Egnyte, VMware, Zoho Corporation, Citrix, Adobe, OwnCloud, Nextcloud, Sync.com, Tresorit, Acronis, IDrive, Backblaze, Wasabi Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cloud Storage and File Sharing Service market is meticulously segmented to provide a granular understanding of its dynamics, catering to the diverse needs of various user groups and industries. This segmentation is crucial for identifying specific market niches, understanding consumer preferences, and developing targeted solutions. The market is primarily broken down by component, distinguishing between the core storage solutions themselves and the associated services that support their deployment and ongoing management. Services encompass critical aspects such as consulting, system integration, and maintenance, which are vital for successful cloud adoption and optimization.

Further segmentation by deployment model (public, private, hybrid) reflects the different architectural preferences and security requirements of organizations, from those seeking maximal scalability and cost-efficiency to those prioritizing control and compliance. Service type segmentation (SaaS, IaaS, PaaS) categorizes solutions based on the level of abstraction and management provided by the vendor, appealing to different technical capabilities and operational models. Lastly, end-user segmentation differentiates between the needs of Small and Medium Enterprises (SMEs) and Large Enterprises, while industry vertical analysis highlights the specialized requirements of sectors like BFSI, Healthcare, IT & Telecom, and Media & Entertainment, enabling service providers to tailor offerings to specific industry challenges and regulatory environments.

- By Component: Storage Solutions, Services

- By Deployment Model: Public Cloud, Private Cloud, Hybrid Cloud

- By Service Type: SaaS (Software as a Service), IaaS (Infrastructure as a Service), PaaS (Platform as a Service)

- By End-User: Small & Medium Enterprises (SMEs), Large Enterprises

- By Industry Vertical: BFSI, Healthcare & Life Sciences, IT & Telecom, Media & Entertainment, Education, Government & Public Sector, Manufacturing, Retail & Consumer Goods, Others

Regional Highlights

- North America: This region is expected to maintain its dominant position in the Cloud Storage and File Sharing Service market. Driven by early technology adoption, the presence of major cloud service providers, and a high concentration of large enterprises with robust IT infrastructures, North America exhibits high demand. The strong emphasis on digital transformation, widespread adoption of hybrid work models, and significant investments in advanced cloud technologies contribute to its sustained growth.

- Europe: Europe represents a significant market, characterized by stringent data protection regulations such as GDPR, which drives demand for compliant and secure cloud storage solutions. The region is seeing increasing adoption across various industries, with a growing focus on hybrid cloud deployments to balance public cloud flexibility with national data sovereignty requirements. Digitalization initiatives across the EU further bolster market expansion.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid digital transformation, increasing internet penetration, and the burgeoning number of SMEs adopting cloud services. Countries like China, India, Japan, and Australia are making substantial investments in cloud infrastructure, driving demand for scalable storage and collaboration tools to support their expanding digital economies and remote workforces.

- Latin America: This region is experiencing steady growth in cloud storage and file sharing adoption. Increasing foreign investments, improving digital infrastructure, and a growing awareness of cloud benefits among local businesses are key drivers. While starting from a lower base, the region offers significant opportunities for providers focusing on cost-effective and scalable solutions for emerging enterprises.

- Middle East and Africa (MEA): The MEA region is witnessing gradual but consistent growth, driven by government initiatives to diversify economies, invest in digital infrastructure, and promote cloud adoption across sectors like oil and gas, healthcare, and finance. Data center investments and increasing internet connectivity are creating a more favorable environment for cloud services, though security and regulatory concerns remain important considerations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cloud Storage and File Sharing Service Market.- Microsoft

- Amazon Web Services (AWS)

- Dropbox

- Box

- IBM

- Oracle

- Egnyte

- VMware

- Zoho Corporation

- Citrix

- Adobe

- OwnCloud

- Nextcloud

- Sync.com

- Tresorit

- Acronis

- IDrive

- Backblaze

- Wasabi Technologies

Frequently Asked Questions

Analyze common user questions about the Cloud Storage and File Sharing Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is cloud storage and how does it differ from traditional storage?

Cloud storage involves saving digital data on remote servers accessible via the internet, rather than directly on a local device or dedicated on-premises hardware. It offers on-demand scalability, ubiquitous access, and typically a pay-as-you-go cost model, contrasting with the fixed capacity, physical maintenance, and upfront capital expenditure of traditional storage.

What are the primary benefits of adopting cloud storage and file sharing services for businesses?

Businesses gain significant advantages, including enhanced accessibility for remote teams, improved collaboration through real-time sharing and co-editing, substantial cost savings by reducing infrastructure investment, superior data scalability to accommodate growth, and robust disaster recovery capabilities ensuring business continuity.

How do cloud storage providers ensure the security and privacy of user data?

Cloud storage providers implement multiple layers of security, including advanced encryption for data in transit and at rest, multi-factor authentication, granular access controls, regular security audits, and compliance with industry standards. They also often employ AI for threat detection and anomaly monitoring to proactively protect data.

What are the main challenges organizations face when migrating to cloud storage or adopting file sharing services?

Key challenges include ensuring data security and privacy compliance (especially with evolving regulations like GDPR), managing the complexity of migrating large volumes of existing data, avoiding vendor lock-in, integrating with legacy systems, and addressing potential latency issues depending on internet connectivity and data location.

How is Artificial Intelligence (AI) influencing the future of cloud storage and file sharing?

AI is transforming cloud storage by enabling intelligent data management, such as automated classification, optimized tiering, and enhanced deduplication. It also bolsters security through predictive threat detection and anomaly analysis, and improves user experience via intelligent search and personalized content recommendations, leading to more efficient and smarter storage solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted