Cloud Management for the OpenStack Market

Cloud Management for the OpenStack Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706154 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Cloud Management for the OpenStack Market Size

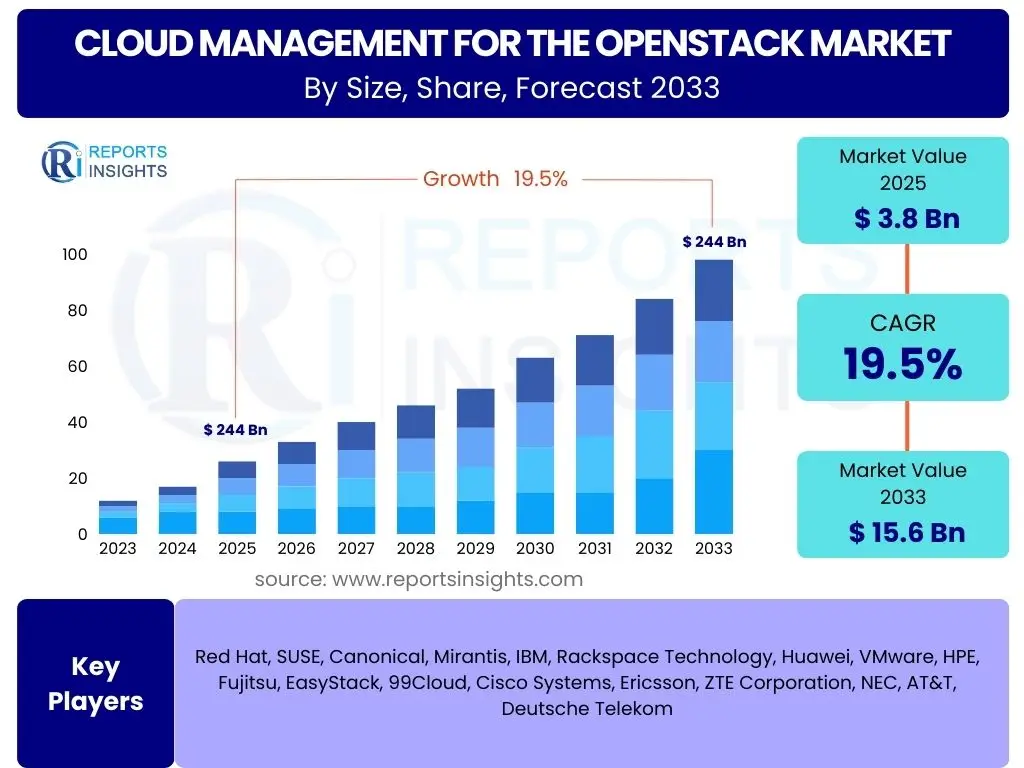

According to Reports Insights Consulting Pvt Ltd, The Cloud Management for the OpenStack Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.5% between 2025 and 2033. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 15.6 Billion by the end of the forecast period in 2033.

Key Cloud Management for the OpenStack Market Trends & Insights

The Cloud Management for the OpenStack market is experiencing significant transformation, driven by evolving enterprise cloud strategies and technological advancements. Key trends indicate a strong emphasis on hybrid and multi-cloud environments, where OpenStack plays a pivotal role in providing a flexible, open-source foundation. Users are increasingly seeking solutions that offer enhanced automation capabilities, seamless integration with container orchestration platforms like Kubernetes, and robust security features to manage complex, distributed cloud infrastructures effectively. The focus is on achieving operational efficiency, cost optimization, and greater agility in deploying and managing cloud resources.

Furthermore, the market is witnessing a surge in demand for managed OpenStack services, as organizations aim to offload the complexities of deployment and ongoing management to expert providers. This trend is particularly prevalent among enterprises that lack the in-house expertise or resources to maintain intricate OpenStack environments. There is also a growing interest in leveraging OpenStack for edge computing initiatives, driven by the need for localized processing and reduced latency. The continuous innovation within the OpenStack community, coupled with the rising adoption of open-source solutions across industries, ensures the platform's sustained relevance and growth in the broader cloud ecosystem.

- Increased adoption of hybrid and multi-cloud strategies.

- Deeper integration with containerization technologies like Kubernetes.

- Emphasis on automation and orchestration tools for operational efficiency.

- Growing demand for robust security and compliance features.

- Rising popularity of managed OpenStack services.

- Expansion of OpenStack deployments for edge computing.

- Focus on AI and ML-driven cloud management for predictive analytics.

AI Impact Analysis on Cloud Management for the OpenStack

Artificial intelligence is profoundly reshaping the landscape of Cloud Management for OpenStack, addressing critical user demands for enhanced automation, optimization, and predictive capabilities. Users are keen on understanding how AI can alleviate the operational complexities inherent in large-scale OpenStack deployments, particularly concerning resource allocation, performance monitoring, and fault prediction. AI-driven solutions are emerging as essential tools for automating routine tasks, such as scaling resources based on demand fluctuations, identifying anomalies, and proactively addressing potential system failures before they impact services. This shift allows IT teams to move from reactive troubleshooting to proactive management, significantly improving system uptime and efficiency.

The integration of AI and machine learning algorithms into OpenStack management platforms facilitates intelligent workload placement, optimizing infrastructure utilization and reducing operational costs. Predictive analytics, powered by AI, enables better capacity planning and helps prevent performance bottlenecks by forecasting future resource needs. Furthermore, AI contributes to enhanced security postures by detecting unusual patterns and potential threats in real-time within the OpenStack environment. While concerns about data privacy, algorithm transparency, and the initial investment in AI infrastructure exist, the overwhelming user expectation is that AI will continue to be a transformative force, enabling more autonomous, efficient, and resilient OpenStack cloud operations.

- Automated resource provisioning and scaling for optimal performance.

- Predictive analytics for capacity planning and preventing outages.

- Enhanced anomaly detection and proactive fault resolution.

- Intelligent workload balancing and placement.

- Optimized energy consumption and cost efficiency through smart resource management.

- Improved security posture through AI-driven threat detection and response.

- Streamlined operations and reduced manual intervention.

Key Takeaways Cloud Management for the OpenStack Market Size & Forecast

The Cloud Management for the OpenStack market is poised for substantial growth, driven by the increasing enterprise adoption of open-source cloud solutions and the strategic shift towards hybrid cloud architectures. A primary takeaway is the accelerating demand for sophisticated management tools that can handle the complexity of distributed OpenStack environments, emphasizing automation, orchestration, and seamless integration with other cloud technologies. Businesses are recognizing OpenStack's ability to provide an agile, cost-effective, and vendor-agnostic foundation for their digital transformation initiatives, leading to sustained investment in related management solutions. The market forecast underscores a robust expansion, reflecting the platform's critical role in future cloud infrastructure deployments.

Another crucial insight is the continued evolution of OpenStack towards supporting emerging technologies such as edge computing, 5G networks, and advanced AI/ML workloads. This adaptability ensures its relevance across diverse industries and use cases. The market's growth is also significantly influenced by the availability of specialized managed services, which democratize access to OpenStack for organizations lacking extensive in-house expertise. Overall, the key takeaway is that OpenStack, backed by comprehensive management solutions, remains a vital component of the enterprise cloud strategy, offering flexibility, control, and innovation capabilities that align with modern business demands for scalability and efficiency.

- Sustained high growth rate driven by open-source cloud adoption.

- Critical importance of advanced automation and orchestration.

- Hybrid and multi-cloud strategies are primary market drivers.

- Growing reliance on managed services for OpenStack deployment and maintenance.

- OpenStack's increasing role in supporting edge computing and 5G infrastructure.

- Emphasis on cost efficiency and operational agility as core benefits.

Cloud Management for the OpenStack Market Drivers Analysis

The Cloud Management for the OpenStack market is significantly propelled by the increasing enterprise preference for open-source cloud platforms that offer flexibility, control, and cost advantages over proprietary solutions. Organizations are keen on avoiding vendor lock-in and customizing their cloud infrastructure to meet specific operational requirements, which OpenStack inherently supports. The escalating adoption of hybrid and multi-cloud strategies further fuels demand, as businesses seek a unified management plane to seamlessly orchestrate workloads across various environments, including on-premise OpenStack clouds and public cloud services. This allows for greater agility and resilience in their IT operations.

Furthermore, the growing need for enhanced automation and orchestration capabilities to manage large, complex cloud environments is a substantial driver. Cloud management solutions for OpenStack enable automated provisioning, scaling, and monitoring, leading to improved operational efficiency and reduced manual overhead. The increasing demand for containerization and microservices architectures, which often leverage OpenStack as their underlying infrastructure, also contributes significantly to market expansion. As businesses continue their digital transformation journeys, the ability to rapidly deploy and manage applications on a scalable, open-source platform becomes paramount, directly boosting the market for OpenStack management tools and services.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing adoption of hybrid and multi-cloud strategies | +1.2% | Global, particularly North America & Europe | 2025-2033 |

| Demand for open-source, vendor-agnostic cloud solutions | +1.0% | Global | 2025-2033 |

| Increased need for cloud automation and orchestration | +0.9% | Global | 2025-2033 |

| Rising adoption of containerization (e.g., Kubernetes on OpenStack) | +0.8% | North America, Asia Pacific | 2025-2030 |

| Focus on cost efficiency and operational expenditure reduction | +0.7% | Global, particularly SMEs | 2025-2033 |

Cloud Management for the OpenStack Market Restraints Analysis

Despite its significant advantages, the Cloud Management for the OpenStack market faces several notable restraints that could temper its growth trajectory. One of the primary challenges is the perceived complexity associated with deploying, configuring, and maintaining OpenStack environments, especially for organizations without specialized in-house expertise. The steep learning curve and the need for highly skilled personnel can be deterrents, particularly for small and medium-sized enterprises (SMEs) or those transitioning from traditional IT infrastructures. This complexity often leads to higher initial deployment costs and longer implementation times, making proprietary cloud solutions appear more straightforward in the short term.

Another significant restraint is the intense competition from established public cloud providers like Amazon Web Services, Microsoft Azure, and Google Cloud Platform, which offer comprehensive, fully managed services with extensive ecosystems and robust support. These hyperscalers present an alternative that can seem less daunting to enterprises prioritizing simplicity and immediate scalability. Additionally, concerns regarding security and compliance in self-managed OpenStack environments, coupled with the need for continuous updates and patching, can pose significant challenges for organizations. The market also grapples with the perception of fragmented vendor support, which, although improving, can still create apprehension among potential adopters seeking unified solutions and consistent technical assistance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of OpenStack deployment and management | -0.8% | Global, particularly SMEs | 2025-2030 |

| Shortage of skilled OpenStack professionals | -0.7% | Global | 2025-2033 |

| Competition from public cloud providers (AWS, Azure, GCP) | -0.6% | North America, Europe | 2025-2033 |

| Security and compliance concerns in self-managed environments | -0.5% | Global | 2025-2033 |

| Higher initial capital expenditure for on-premise deployments | -0.4% | Emerging markets | 2025-2028 |

Cloud Management for the OpenStack Market Opportunities Analysis

Significant opportunities exist within the Cloud Management for the OpenStack market, driven by evolving technological landscapes and strategic business shifts. The expansion into edge computing represents a substantial growth avenue, as OpenStack's flexibility and open-source nature make it an ideal platform for managing distributed infrastructure at the network edge. With the proliferation of IoT devices and the demand for real-time data processing, enterprises increasingly require localized cloud environments, where OpenStack can provide the necessary compute and storage capabilities managed efficiently from a central location. This synergy between OpenStack and edge computing is expected to unlock new use cases and market segments, particularly in industries like manufacturing, retail, and telecommunications.

Another key opportunity lies in the burgeoning market for AI and Machine Learning (ML) workloads. OpenStack, combined with robust management tools, can provide a scalable and customizable infrastructure for training and deploying AI/ML models, offering a compelling alternative to proprietary platforms. Furthermore, the increasing demand for specialized industry-specific cloud solutions creates avenues for vendors to tailor OpenStack management offerings to meet the unique compliance, performance, and integration requirements of verticals such as healthcare, BFSI, and government. The growing reliance on managed OpenStack services also presents a lucrative opportunity for service providers to cater to organizations seeking to leverage OpenStack benefits without the burden of complex in-house management, thereby expanding the market's accessibility and adoption.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing adoption of edge computing | +1.5% | Global, particularly APAC and Europe | 2026-2033 |

| Increased demand for AI/ML workload support | +1.3% | North America, Europe | 2025-2033 |

| Expansion of managed services for OpenStack | +1.1% | Global | 2025-2033 |

| Development of industry-specific OpenStack solutions | +0.9% | Global | 2025-2030 |

| Integration with 5G infrastructure deployments | +0.8% | Asia Pacific, Europe | 2027-2033 |

Cloud Management for the OpenStack Market Challenges Impact Analysis

The Cloud Management for the OpenStack market faces several critical challenges that can impact its growth trajectory and adoption rates. One significant challenge is the ongoing perception of complexity and the steep learning curve associated with OpenStack itself. Despite advancements in management tools, the underlying architecture requires a certain level of technical expertise, which can deter organizations with limited IT resources or those accustomed to simpler, more abstract cloud interfaces. This complexity extends to troubleshooting and maintaining stability in large-scale deployments, demanding continuous investment in training and specialized staff.

Another prominent challenge is ensuring seamless interoperability and avoiding vendor lock-in within the OpenStack ecosystem. While OpenStack promotes open standards, the proliferation of various distributions and third-party integrations can lead to compatibility issues and increase the effort required for multi-vendor deployments. Furthermore, the rapid pace of technological change in the broader cloud landscape, coupled with intense competition from well-established public cloud providers offering fully managed services, forces OpenStack solution providers to continuously innovate and demonstrate clear value propositions. Data governance, regulatory compliance, and security in a highly customizable and often self-managed environment also remain persistent hurdles, requiring robust management solutions that address these concerns comprehensively and consistently across diverse operational contexts.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining interoperability across diverse OpenStack components | -0.9% | Global | 2025-2030 |

| Addressing perceptions of OpenStack's complexity | -0.8% | Global | 2025-2033 |

| Rapid evolution of cloud technologies and feature parity | -0.7% | Global | 2025-2033 |

| Ensuring data governance and regulatory compliance | -0.6% | Europe (GDPR), Asia Pacific | 2025-2033 |

| Mitigating security vulnerabilities in open-source environments | -0.5% | Global | 2025-2033 |

Cloud Management for the OpenStack Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Cloud Management for the OpenStack market, detailing its current size, historical performance, and future growth projections. It meticulously examines key market drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders. The report segments the market by component, deployment type, organization size, and end-user industry, providing a granular view of market dynamics across various applications and user bases. Furthermore, it includes a detailed regional analysis and profiles of leading market participants, ensuring a holistic understanding of the competitive landscape and regional market nuances.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 15.6 Billion |

| Growth Rate | 19.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Red Hat, SUSE, Canonical, Mirantis, IBM, Rackspace Technology, Huawei, VMware, HPE, Fujitsu, EasyStack, 99Cloud, Cisco Systems, Ericsson, ZTE Corporation, NEC, AT&T, Deutsche Telekom |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cloud Management for the OpenStack market is meticulously segmented to provide a detailed understanding of its diverse facets and varying demands across different user profiles and application scenarios. This granular segmentation helps in identifying specific growth opportunities and market dynamics within each category. The market is primarily analyzed based on its components, distinguishing between the software platforms and solutions that provide management capabilities, and the services that support their deployment, operation, and maintenance. This includes professional services for implementation and customization, as well as ongoing managed services and technical support, which are crucial for organizations lacking in-house OpenStack expertise.

Further segmentation by deployment type clarifies adoption patterns across public, private, and hybrid cloud environments, reflecting the diverse strategies enterprises employ for their cloud infrastructure. The market also differentiates based on organization size, examining the distinct needs and adoption rates of large enterprises versus small and medium-sized businesses (SMEs), each facing unique challenges and opportunities in managing OpenStack. Finally, a comprehensive end-user industry segmentation provides insights into the specific requirements and applications of OpenStack management in key verticals such as IT & Telecommunications, BFSI, Government, Healthcare, and Manufacturing, among others. This multi-dimensional approach ensures a thorough and actionable analysis of the market landscape.

- By Component:

- Software (Platform, Solutions)

- Services (Professional Services, Managed Services, Support & Maintenance)

- By Deployment Type:

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size:

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- By End-User Industry:

- BFSI

- IT & Telecommunications

- Government & Public Sector

- Retail & E-commerce

- Healthcare

- Manufacturing

- Media & Entertainment

- Others

Regional Highlights

- North America: This region is a leading market for Cloud Management for OpenStack, driven by early and widespread adoption of cloud technologies, significant investments in hybrid cloud strategies, and the presence of numerous key technology providers. The high demand for automation and advanced cloud orchestration solutions among large enterprises and government agencies contributes to its dominant market share.

- Europe: The European market demonstrates robust growth, propelled by increasing digital transformation initiatives, stringent data sovereignty regulations necessitating private cloud deployments, and a strong emphasis on open-source solutions. Countries like Germany, the UK, and France are at the forefront of OpenStack adoption, particularly in telecommunications and research sectors.

- Asia Pacific (APAC): APAC is anticipated to be the fastest-growing region, fueled by rapid economic development, escalating IT expenditure, and the widespread adoption of cloud computing across diverse industries. Emerging economies like China and India are witnessing significant investments in data centers and cloud infrastructure, driving demand for scalable and flexible OpenStack management solutions, especially for edge computing and 5G deployments.

- Latin America: This region is experiencing steady growth, attributed to increasing cloud adoption by enterprises seeking cost-effective and agile infrastructure solutions. Government initiatives for digital transformation and the expansion of IT infrastructure are creating new opportunities for OpenStack management services.

- Middle East and Africa (MEA): The MEA market is gradually expanding, driven by digital initiatives, smart city projects, and diversification efforts away from traditional economies. Growing awareness of open-source benefits and increasing investments in telecommunications and data centers are key factors contributing to the adoption of OpenStack management solutions in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cloud Management for the OpenStack Market.- Red Hat

- SUSE

- Canonical

- Mirantis

- IBM

- Rackspace Technology

- Huawei

- VMware

- HPE

- Fujitsu

- EasyStack

- 99Cloud

- Cisco Systems

- Ericsson

- ZTE Corporation

- NEC

- AT&T

- Deutsche Telekom

Frequently Asked Questions

Analyze common user questions about the Cloud Management for the OpenStack market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is OpenStack Cloud Management?

OpenStack Cloud Management refers to the tools, platforms, and services designed to deploy, monitor, optimize, and secure cloud infrastructure built on OpenStack. It enables efficient resource orchestration, automation, and operational control over OpenStack components, ensuring high performance and reliability for diverse workloads.

Why is Cloud Management important for OpenStack environments?

Cloud Management is crucial for OpenStack environments due to their inherent complexity and scale. It streamlines operations, automates routine tasks, optimizes resource utilization, enhances security, and provides comprehensive visibility, enabling organizations to maximize the benefits of their OpenStack cloud while minimizing operational overhead and costs.

How does AI impact OpenStack Cloud Management?

AI significantly impacts OpenStack Cloud Management by enabling advanced automation, predictive analytics, and intelligent resource allocation. AI-driven solutions can predict system failures, optimize performance in real-time, automate scaling, and enhance threat detection, leading to more autonomous, efficient, and resilient cloud operations.

What are the key benefits of using OpenStack for enterprise cloud?

Key benefits of using OpenStack for enterprise cloud include avoiding vendor lock-in due to its open-source nature, high customization capabilities to meet specific business needs, cost efficiency compared to proprietary solutions, and the flexibility to deploy hybrid and multi-cloud strategies seamlessly. It offers full control over the cloud infrastructure.

What are the primary challenges in managing an OpenStack cloud?

Primary challenges in managing an OpenStack cloud include the complexity of deployment and maintenance, a potential shortage of skilled personnel, ensuring robust security and compliance, and maintaining interoperability across various components. These challenges often necessitate specialized management tools or managed services to mitigate effectively.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted