Nuclear Waste Management System Market

Nuclear Waste Management System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706131 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

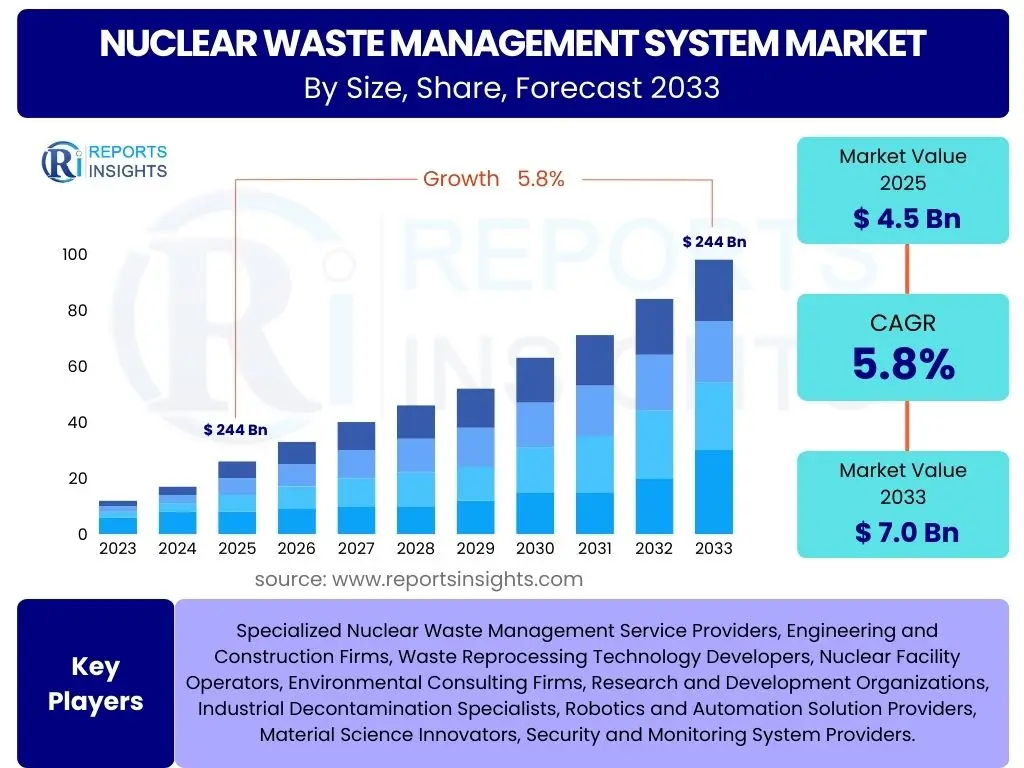

Nuclear Waste Management System Market Size

According to Reports Insights Consulting Pvt Ltd, The Nuclear Waste Management System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 4.5 billion in 2025 and is projected to reach USD 7.0 billion by the end of the forecast period in 2033.

Key Nuclear Waste Management System Market Trends & Insights

The Nuclear Waste Management System market is currently shaped by several significant trends driven by global energy demands and environmental considerations. There is a growing emphasis on developing advanced reprocessing technologies to minimize waste volume and extract valuable resources, reflecting a shift towards more sustainable nuclear fuel cycles. Concurrently, regulatory frameworks are evolving globally, with many nations strengthening safety standards and long-term disposal requirements, which necessitates continuous innovation in waste containment and monitoring solutions. The increasing public and governmental scrutiny on nuclear safety and environmental impact also pushes for greater transparency and robust, demonstrable waste management strategies.

Another prominent trend is the expansion of interim storage solutions, as the development of permanent geological repositories often faces delays due to political, social, and technical challenges. This drives demand for safe, secure, and long-term retrievable storage facilities. Furthermore, digitalization and automation are becoming integral to waste management processes, enhancing operational efficiency, improving safety protocols, and enabling precise tracking of radioactive materials from generation to disposal. The market is also seeing a rise in international collaboration and knowledge sharing, especially for research into deep geological disposal and advanced reactor designs that produce less waste.

- Advanced reprocessing technologies gaining traction for waste minimization and resource recovery.

- Stricter global regulatory frameworks and safety standards driving demand for innovative solutions.

- Increased focus on long-term, secure interim storage solutions due to delays in permanent repositories.

- Integration of digitalization and automation for enhanced efficiency, safety, and traceability.

- Growing international cooperation in research and development for waste disposal and new reactor technologies.

AI Impact Analysis on Nuclear Waste Management System

Artificial Intelligence (AI) is poised to revolutionize various aspects of nuclear waste management, addressing long-standing challenges related to safety, efficiency, and data analysis. Users commonly inquire about AI's role in predictive maintenance for waste handling equipment, enabling proactive interventions and reducing downtime in critical operations. AI-powered analytics can process vast amounts of sensor data from storage facilities, identifying anomalies and potential safety issues far more quickly and accurately than traditional methods, thereby enhancing the integrity and security of waste containment. Furthermore, robotics integrated with AI algorithms can undertake hazardous tasks such as waste characterization, sorting, and packaging in high-radiation environments, significantly minimizing human exposure and improving operational precision.

The application of AI extends to optimizing the entire waste lifecycle, from generation to final disposal. Machine learning models can predict the behavior of radioactive materials over millennia, aiding in the design and validation of long-term disposal sites. AI also plays a crucial role in data management and regulatory compliance, automating the extensive documentation and reporting required for nuclear waste. Concerns often revolve around the security of AI systems, the reliability of algorithms in safety-critical applications, and the need for robust validation processes to ensure their dependability in managing extremely hazardous materials. Despite these considerations, the overarching expectation is that AI will be a transformative force, leading to safer, more efficient, and more compliant nuclear waste management practices globally.

- Predictive maintenance for equipment and infrastructure within waste management facilities, enhancing operational reliability.

- Advanced analytics for real-time monitoring of waste storage, detecting anomalies and ensuring containment integrity.

- AI-driven robotics for automated handling, sorting, and packaging of radioactive materials in high-risk zones.

- Machine learning models for long-term behavior prediction of waste and optimization of disposal site selection and design.

- Enhanced data management and regulatory compliance through AI-powered automation and reporting.

Key Takeaways Nuclear Waste Management System Market Size & Forecast

Common user inquiries about the nuclear waste management system market often center on its growth trajectory, the drivers behind it, and the long-term viability of current and emerging solutions. A significant takeaway is the market's stable and sustained growth, projected at a CAGR of 5.8% through 2033, indicating a robust demand for sophisticated waste management solutions. This growth is primarily fueled by the continued operation and planned expansion of nuclear power generation globally, necessitating comprehensive strategies for managing spent fuel and other radioactive by-products. The substantial financial investment required for waste management, reflected in the market's multi-billion-dollar valuation, underscores its critical role within the broader nuclear energy sector and its long-term financial commitment.

The forecast highlights a clear trend towards technologically advanced and safer solutions. Market participants are increasingly focusing on innovations in reprocessing, interim storage, and final disposal technologies to meet evolving regulatory demands and public expectations. The market's expansion is not merely about capacity but also about enhancing the efficiency, safety, and environmental stewardship of waste handling processes. Furthermore, the long-term nature of nuclear waste management implies sustained opportunities for specialized service providers, technology developers, and infrastructure developers throughout the forecast period, emphasizing the need for durable partnerships and continuous research and development to address complex, multi-generational challenges.

- The market is poised for consistent growth driven by ongoing nuclear power operations and new builds.

- Significant investments are being directed towards advanced reprocessing and long-term storage solutions.

- Technological advancements are central to improving safety, efficiency, and environmental compliance in waste management.

- Long-term strategic planning and continuous R&D are crucial for addressing the enduring nature of nuclear waste.

- The market presents sustained opportunities for specialized services and infrastructure development.

Nuclear Waste Management System Market Drivers Analysis

The nuclear waste management system market is fundamentally driven by the indispensable need for safe and secure handling of radioactive by-products from nuclear activities. A primary driver is the increasing global demand for clean energy, leading to the construction of new nuclear power plants and the extended operation of existing ones. This expansion directly translates into a greater volume of spent nuclear fuel and other radioactive waste, thereby escalating the demand for robust management solutions. Concurrently, the rigorous enforcement of international and national safety regulations and environmental protection standards compels nuclear operators to invest in advanced and compliant waste management technologies and services. These stringent regulations ensure public safety and environmental integrity, pushing for continuous improvements in waste treatment, storage, and disposal.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Nuclear Power Generation Capacity | +1.5% | Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Stricter Regulatory Frameworks and Environmental Compliance | +1.2% | Global | Medium-term (2025-2029) |

| Technological Advancements in Waste Treatment and Reprocessing | +1.0% | Developed Nations (e.g., France, Japan, USA) | Long-term (2025-2033) |

| Growing Public Awareness and Demand for Safe Disposal | +0.8% | Global | Medium-term (2025-2029) |

| Need for Decommissioning Aging Nuclear Facilities | +0.7% | Europe, North America | Long-term (2025-2033) |

Nuclear Waste Management System Market Restraints Analysis

Despite the inherent necessity for nuclear waste management, the market faces several significant restraints that can impede its growth. One of the primary challenges is the exceptionally high capital expenditure required for developing and maintaining nuclear waste management infrastructure, including reprocessing plants, interim storage facilities, and deep geological repositories. These costs, coupled with the long operational timelines of such facilities, can deter investment and pose substantial financial burdens. Furthermore, public opposition and socio-political resistance to the siting of waste disposal facilities remain a persistent hurdle. Concerns over safety, environmental contamination, and potential long-term risks often lead to protracted legal and political battles, significantly delaying or even canceling projects.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Costs and Long Project Lifecycles | -1.3% | Global | Long-term (2025-2033) |

| Public Opposition and Socio-Political Resistance | -1.0% | Europe, North America, Asia Pacific | Medium-term (2025-2029) |

| Complex and Evolving Regulatory Frameworks | -0.8% | Global | Long-term (2025-2033) |

| Limited Availability of Permanent Disposal Sites | -0.7% | Global | Long-term (2025-2033) |

| Technological and Safety Uncertainties | -0.5% | Global | Medium-term (2025-2029) |

Nuclear Waste Management System Market Opportunities Analysis

The nuclear waste management system market is ripe with opportunities driven by innovation, global collaboration, and evolving energy policies. A significant opportunity lies in the continuous advancement of reprocessing technologies, which can significantly reduce the volume and radiotoxicity of high-level waste while recovering valuable fissile materials for reuse. This not only addresses waste concerns but also contributes to resource efficiency and proliferation resistance. Furthermore, the growing focus on interim storage solutions presents substantial opportunities for developing sophisticated, safe, and retrievable storage facilities, especially as permanent disposal options face delays. There is also a burgeoning market for the remediation and decommissioning of legacy nuclear sites, which require specialized expertise and technology to safely manage existing waste and dismantle old infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Reprocessing Technologies | +1.3% | Developed Nations (e.g., France, Japan, USA, Russia) | Long-term (2025-2033) |

| Expansion of Interim Storage Solutions and Facilities | +1.1% | Global | Medium-term (2025-2029) |

| Decommissioning and Remediation of Legacy Nuclear Sites | +0.9% | Europe, North America | Long-term (2025-2033) |

| International Collaboration and Knowledge Sharing | +0.8% | Global | Long-term (2025-2033) |

| Innovation in Waste Characterization and Monitoring | +0.7% | Global | Short-term (2025-2027) |

Nuclear Waste Management System Market Challenges Impact Analysis

The nuclear waste management system market faces complex and multifaceted challenges that require long-term strategic solutions. A significant hurdle is overcoming public mistrust and gaining social acceptance for waste disposal projects, which are often perceived as risks to local communities and the environment. This necessitates robust public engagement, transparent communication, and demonstrable safety measures. Another critical challenge is the immense financial and technical commitment required for research, development, and implementation of permanent disposal solutions, such as deep geological repositories. The long-term stability and safety of these sites, spanning thousands of years, present unprecedented engineering and scientific challenges, compounded by funding uncertainties and political shifts over such extended periods.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Public Acceptance and Stakeholder Engagement | -1.2% | Global | Long-term (2025-2033) |

| Long-term Funding and Political Will for Permanent Disposal | -1.0% | Global | Long-term (2025-2033) |

| Ensuring Long-term Safety and Security of Waste | -0.9% | Global | Long-term (2025-2033) |

| Complex Technical Hurdles for Deep Geological Repositories | -0.8% | Global | Long-term (2025-2033) |

| International Consensus on Waste Disposal Standards | -0.6% | Global | Medium-term (2025-2029) |

Nuclear Waste Management System Market - Updated Report Scope

This report provides a comprehensive analysis of the Nuclear Waste Management System Market, offering in-depth insights into its size, growth trajectory, key trends, drivers, restraints, opportunities, and challenges. The scope encompasses detailed segmentation across various waste types, management stages, service types, and end-use industries, along with a thorough regional assessment to highlight key market dynamics across different geographies. The study also includes a comprehensive impact analysis of Artificial Intelligence on the market, recognizing its transformative potential. Furthermore, it profiles key market players, providing a competitive landscape to understand market positioning and strategies. This report serves as an essential resource for stakeholders seeking to understand the current market scenario and future growth prospects in the nuclear waste management sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.0 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Specialized Nuclear Waste Management Service Providers, Engineering and Construction Firms, Waste Reprocessing Technology Developers, Nuclear Facility Operators, Environmental Consulting Firms, Research and Development Organizations, Industrial Decontamination Specialists, Robotics and Automation Solution Providers, Material Science Innovators, Security and Monitoring System Providers. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Nuclear Waste Management System Market is comprehensively segmented to provide granular insights into its diverse components and their respective contributions to market growth. These segmentations allow for a detailed analysis of specific waste streams, operational phases, specialized services, and the various industries that generate nuclear waste. Understanding these distinct segments is crucial for identifying key growth areas, assessing technological adoption rates, and tailoring strategies to meet specific industry needs or regulatory requirements.

- By Waste Type:

- High-level Waste (HLW): Primarily spent nuclear fuel and reprocessed waste.

- Intermediate-level Waste (ILW): Contains higher levels of radioactivity than LLW, requiring shielding.

- Low-level Waste (LLW): Contaminated items like tools, clothing, and paper, with low radioactivity.

- Mixed Waste: Contains both radioactive and hazardous chemical properties.

- By Management Stage:

- Storage: Temporary holding of waste pending further treatment or disposal.

- Transportation: Safe and secure movement of waste between facilities.

- Disposal: Permanent placement of waste in geological repositories or other long-term solutions.

- Reprocessing: Chemical separation of reusable nuclear materials from spent fuel.

- By Service Type:

- Decommissioning: Dismantling of nuclear facilities after their operational life.

- Decontamination: Removal or reduction of radioactive contamination.

- Site Remediation: Cleanup and restoration of contaminated land.

- Waste Treatment: Processes to reduce waste volume, toxicity, or mobility.

- Waste Storage & Disposal: Solutions for interim and permanent waste containment.

- By End-Use Industry:

- Nuclear Power Plants: Largest generators of nuclear waste.

- Research Institutions: Produce waste from scientific experiments and reactor operations.

- Healthcare: Generate radioactive waste from medical diagnostics and treatments.

- Industrial: Produce waste from industrial processes, sterilization, and non-destructive testing.

Regional Highlights

- North America: The region is a mature market driven by extensive nuclear power infrastructure and ongoing decommissioning efforts. The United States and Canada represent significant markets, with continuous investment in advanced storage solutions and waste characterization technologies. Regulatory clarity and a strong research and development ecosystem contribute to market stability and innovation.

- Europe: Europe showcases a diverse landscape, with countries like France leading in reprocessing capabilities and others focusing on deep geological disposal research (e.g., Finland, Sweden). The region faces significant decommissioning challenges for aging reactors and stringent environmental regulations, driving demand for innovative waste management services. Political and public acceptance remain key factors influencing project timelines.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market due to the rapid expansion of nuclear power generation in countries like China, India, and South Korea. The increasing number of new reactor builds creates a substantial demand for comprehensive waste management systems, including storage, transportation, and potential reprocessing facilities. Economic growth and energy security concerns are primary drivers.

- Latin America: Nuclear waste management in Latin America is characterized by developing nuclear programs in countries such as Argentina, Brazil, and Mexico. The market is smaller but presents growth opportunities as these nations mature their nuclear energy capabilities and address the long-term management of their accumulated waste. International cooperation and technology transfer are crucial for development in this region.

- Middle East and Africa (MEA): This region is emerging in nuclear energy, with countries like UAE developing new power plants, thus creating a nascent market for nuclear waste management. While currently smaller, future growth is anticipated as more nations in the MEA region explore nuclear energy to diversify their power grids, leading to an eventual need for robust waste management infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Nuclear Waste Management System Market.- Orano S.A.

- Veolia Environnement S.A.

- Waste Management, Inc.

- Kurion, Inc. (now part of Veolia)

- Studsvik AB

- Energon Solutions Group

- Hitachi Zosen Corporation

- Babcock International Group PLC

- EnergySolutions

- Jacobs Engineering Group Inc.

- Bechtel Corporation

- Amec Foster Wheeler (now part of Wood Group)

- Fluor Corporation

- Kore Energy Services

- TerraPower LLC

- Tepco Holdings Inc.

- Rosatom State Atomic Energy Corporation

- China National Nuclear Corporation (CNNC)

- Cameco Corporation

- EDF (Électricité de France)

Frequently Asked Questions

What is nuclear waste management?

Nuclear waste management encompasses all activities involved in the handling, treatment, storage, and disposal of radioactive waste generated from nuclear power generation, medical applications, industrial processes, and research. Its primary goal is to protect human health and the environment from the harmful effects of ionizing radiation over the very long periods that radioactive materials remain hazardous.

What are the main types of nuclear waste?

The main types of nuclear waste are High-Level Waste (HLW), Intermediate-Level Waste (ILW), and Low-Level Waste (LLW). HLW typically consists of spent nuclear fuel and reprocessed waste, possessing high radioactivity and heat. ILW contains lower radioactivity than HLW but still requires shielding. LLW, which accounts for the largest volume, includes everyday items with low levels of contamination.

What are the biggest challenges in nuclear waste management?

Key challenges in nuclear waste management include the extremely long half-lives of some radioactive isotopes, requiring disposal solutions that are stable for thousands to hundreds of thousands of years; high capital and operational costs; overcoming public and political opposition to disposal facility siting; ensuring long-term safety and security against accidental release or malevolent acts; and the complex regulatory frameworks governing the entire process.

What technologies are used for nuclear waste treatment and disposal?

Technologies used include vitrification (immobilizing HLW in glass), cementation (encasing ILW/LLW in concrete), incineration for combustible LLW, compaction for volume reduction, and various reprocessing techniques to separate reusable materials from spent fuel. For disposal, deep geological repositories are the most widely accepted long-term solution for HLW and ILW, involving burial deep underground in stable geological formations.

What is the market outlook for nuclear waste management systems?

The market outlook for nuclear waste management systems is positive, projected for steady growth at a CAGR of 5.8% from 2025 to 2033. This growth is driven by the continued operation and expansion of nuclear power plants, increasing decommissioning activities, and the global imperative for safer and more sustainable waste handling. Technological advancements, particularly in reprocessing and long-term storage, are expected to fuel innovation and market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted