GaN Power Device Market

GaN Power Device Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706424 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

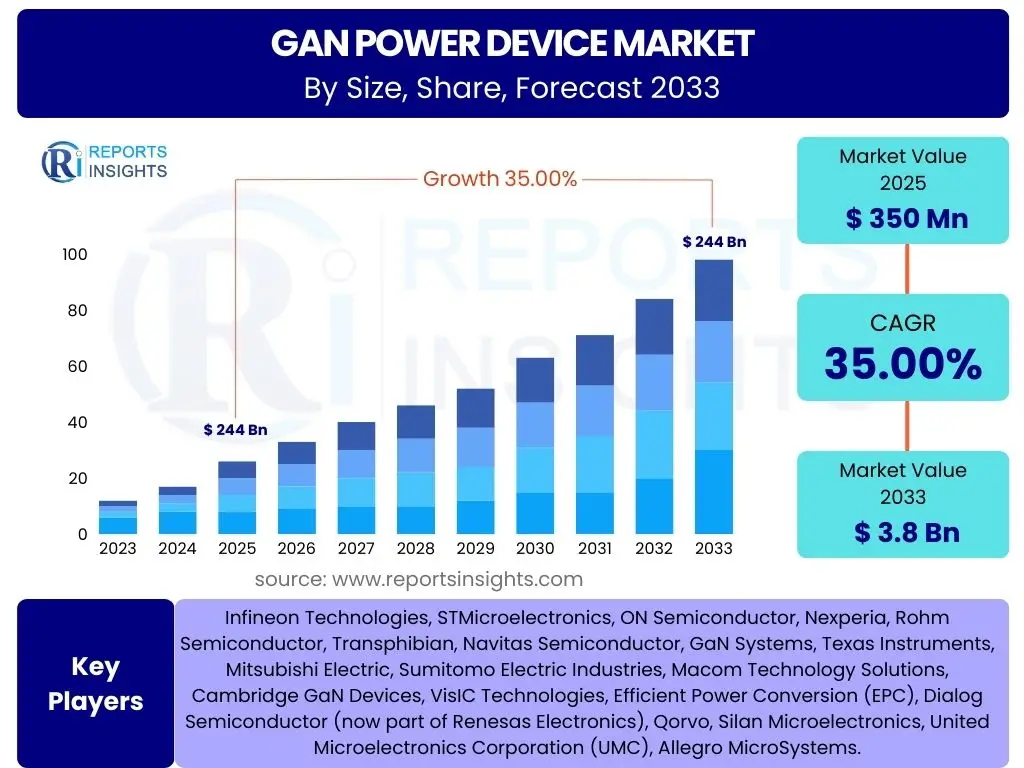

GaN Power Device Market Size

According to Reports Insights Consulting Pvt Ltd, The GaN Power Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 35.00% between 2025 and 2033. The market is estimated at USD 350 Million in 2025 and is projected to reach USD 3.8 Billion by the end of the forecast period in 2033.

Key GaN Power Device Market Trends & Insights

The GaN power device market is experiencing transformative growth driven by technological advancements and expanding application areas. A primary trend involves the increasing demand for energy-efficient and compact power solutions across various industries. This includes a notable shift towards higher power density in devices, enabling smaller form factors without compromising performance. Miniaturization remains a critical factor, directly influencing product design in consumer electronics and automotive applications.

Another significant trend is the growing adoption of GaN in fast charging technologies for consumer electronics, driven by the need for quicker charge times and reduced charger size. The automotive sector's electrification, particularly the rise of electric vehicles (EVs) and hybrid electric vehicles (HEVs), is also a major catalyst, with GaN power devices offering superior efficiency for onboard chargers and traction inverters. Furthermore, the expansion of 5G infrastructure and data centers is fueling demand for GaN solutions due to their ability to handle higher frequencies and power levels with reduced energy loss.

- Increasing demand for energy-efficient power solutions.

- Miniaturization and higher power density requirements across applications.

- Rapid adoption in consumer electronics for fast charging.

- Growing integration into electric vehicles (EVs) and associated charging infrastructure.

- Expansion of 5G telecommunications infrastructure and data centers.

- Technological advancements in GaN wafer size and packaging.

AI Impact Analysis on GaN Power Device

The pervasive integration of Artificial Intelligence (AI) across various sectors is significantly influencing the GaN power device market. AI, particularly in data centers, edge computing, and autonomous systems, necessitates highly efficient and compact power management solutions. GaN devices, with their superior switching speeds, lower power losses, and higher power density compared to traditional silicon, are ideally suited to meet the stringent power requirements of AI accelerators, servers, and related infrastructure. This synergy drives demand for GaN technology as the backbone for next-generation AI hardware, enabling more powerful and cooler operating environments.

Furthermore, the increasing deployment of AI in industrial automation, robotics, and smart grids also contributes to the demand for GaN power devices. These applications require robust, reliable, and energy-efficient power conversion to manage complex operations and process vast amounts of data. GaN's ability to operate at higher temperatures and frequencies makes it a preferred choice for such demanding environments, directly supporting the expansion and efficiency of AI-driven systems. The drive towards sustainable AI solutions also highlights GaN's importance, as its inherent efficiency helps reduce overall energy consumption in AI data centers.

- AI drives demand for highly efficient power solutions in data centers and edge AI.

- GaN's high power density supports compact and powerful AI hardware.

- Improved thermal management offered by GaN is crucial for high-performance AI processors.

- Enables higher switching frequencies vital for AI power conversion efficiency.

- Supports the development of autonomous systems and advanced robotics requiring robust power.

Key Takeaways GaN Power Device Market Size & Forecast

The GaN power device market is poised for exceptional growth, driven by its inherent advantages over traditional silicon-based solutions. The significant Compound Annual Growth Rate (CAGR) projected reflects a broad market acceptance and the increasing realization of GaN's capabilities in enhancing power efficiency and reducing system size across numerous applications. This rapid expansion is a direct consequence of ongoing technological innovations and the imperative for more sustainable and high-performance power solutions.

A central takeaway is the market's trajectory towards widespread adoption in diverse sectors, moving beyond initial niche applications. From consumer electronics requiring ultra-fast charging to the demanding environments of electric vehicles and 5G infrastructure, GaN is becoming an indispensable component. The forecast demonstrates a clear shift in the power electronics landscape, with GaN emerging as a key enabler for future technological advancements, emphasizing its critical role in energy conservation and miniaturization.

- Market to grow at a substantial CAGR of 35.00% from 2025 to 2033.

- Projected market value to reach USD 3.8 Billion by 2033.

- Strong demand from consumer electronics, automotive, and telecommunications sectors.

- Driven by the need for higher efficiency, smaller form factors, and improved thermal performance.

- Significant shift from traditional silicon-based devices to GaN technology.

GaN Power Device Market Drivers Analysis

The GaN power device market is propelled by a confluence of technological advancements and increasing demands for efficient power management. A primary driver is the accelerating trend towards energy efficiency across all electronic devices, stemming from environmental concerns and regulatory pressures. GaN's superior properties, such as lower on-resistance and faster switching speeds, significantly reduce power losses, making it ideal for applications where energy conservation is paramount.

Furthermore, the rapid expansion of electric vehicles (EVs), hybrid electric vehicles (HEVs), and their associated charging infrastructure is a major catalyst. GaN devices offer high power density and efficiency for onboard chargers, DC-DC converters, and traction inverters, directly contributing to smaller, lighter, and more efficient automotive power systems. Similarly, the global rollout of 5G networks and the proliferation of data centers are creating substantial demand for GaN, as these applications require power solutions that can handle high frequencies and reduce operational costs through improved efficiency and thermal performance.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Energy-Efficient Solutions | +8.5% | Global (Europe, North America, APAC) | 2025-2033 |

| Growth in Electric Vehicles (EVs) and Charging Infrastructure | +9.0% | Asia Pacific (China, Japan), Europe (Germany), North America (USA) | 2025-2033 |

| Expansion of 5G Infrastructure and Data Centers | +7.0% | Asia Pacific (China, South Korea), North America (USA), Europe | 2025-2030 |

| Miniaturization and Higher Power Density Requirements | +6.5% | Global (Consumer Electronics Hubs) | 2025-2033 |

| Adoption in Fast Charging Technologies for Consumer Electronics | +5.0% | Asia Pacific (China, India), North America, Europe | 2025-2030 |

GaN Power Device Market Restraints Analysis

Despite the significant growth prospects, the GaN power device market faces several restraints that could potentially impede its full market penetration. A notable challenge is the relatively higher manufacturing cost of GaN devices compared to established silicon-based power components. While the long-term total cost of ownership might be lower due to efficiency gains, the initial upfront investment can be a deterrent for some manufacturers, particularly in cost-sensitive applications.

Another key restraint involves concerns regarding the long-term reliability and robustness of GaN devices, especially in high-power and high-temperature applications. Although extensive testing is being conducted, the relatively newer market presence of GaN compared to decades of silicon technology means that design engineers and system integrators often require more convincing data and standardized testing procedures to fully trust GaN's performance in mission-critical applications. Additionally, the supply chain for GaN materials and manufacturing processes is still maturing, leading to potential limitations in scalability and availability compared to the highly optimized silicon supply chain.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Manufacturing Costs Compared to Silicon | -4.0% | Global | 2025-2028 |

| Reliability and Long-Term Stability Concerns | -3.5% | Global (Automotive, Industrial) | 2025-2029 |

| Lack of Standardized Testing Procedures | -2.0% | Global | 2025-2027 |

| Limited Supply Chain Maturity | -1.5% | Global | 2025-2027 |

GaN Power Device Market Opportunities Analysis

The GaN power device market is brimming with opportunities stemming from untapped application areas and ongoing technological maturation. A significant opportunity lies in the deeper penetration of GaN technology into emerging high-growth sectors such as aerospace and defense, where the demand for lightweight, efficient, and robust power systems is paramount. These sectors can greatly benefit from GaN's superior power density and thermal performance in constrained environments.

Furthermore, the continuous innovation in packaging technologies and wafer sizes (e.g., from 6-inch to 8-inch GaN-on-Si wafers) offers considerable opportunities for cost reduction and increased volume production. This scalability can make GaN more competitive and accessible for a wider range of mainstream applications. Strategic partnerships and collaborations between GaN device manufacturers, semiconductor foundries, and end-user industries are also crucial for accelerating adoption, fostering innovation, and addressing market-specific needs. The ongoing global push for renewable energy sources, such as solar power and wind energy, also presents a substantial opportunity for GaN, as it can significantly improve the efficiency of inverters and converters in these systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Aerospace and Defense | +6.0% | North America (USA), Europe | 2027-2033 |

| Further Penetration into Industrial Power Supplies and Motor Drives | +5.5% | Global | 2025-2033 |

| Development of Advanced Packaging Technologies and Larger Wafer Sizes | +7.0% | Global (Semiconductor Manufacturing Hubs) | 2025-2033 |

| Strategic Partnerships and Collaborations Across the Value Chain | +4.5% | Global | 2025-2033 |

| Increasing Use in Renewable Energy Systems (Solar Inverters) | +5.0% | Asia Pacific (China, India), Europe, North America | 2026-2033 |

GaN Power Device Market Challenges Impact Analysis

The GaN power device market faces several inherent challenges that require innovative solutions and strategic approaches. One significant challenge revolves around thermal management, particularly at higher power levels and increased switching frequencies. While GaN devices offer superior efficiency, dissipating heat effectively within smaller form factors remains a complex engineering task, impacting reliability and performance in demanding applications. This necessitates advanced cooling solutions and sophisticated package designs.

Another crucial challenge is the stiff competition from mature silicon carbide (SiC) technology, especially in high-power, high-voltage applications like electric vehicle powertrains and industrial motor drives. While GaN excels at lower to medium voltage ranges and very high frequencies, SiC has a well-established track record and a more mature supply chain in certain high-power segments. Furthermore, the need for specialized design expertise among engineers and system integrators presents a hurdle. Designing with GaN requires a deeper understanding of its unique characteristics, high-frequency behavior, and layout considerations, which can slow down adoption rates for companies less familiar with the technology.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management Issues at High Power Levels | -3.0% | Global | 2025-2030 |

| Competition from Mature Silicon Carbide (SiC) Technology | -4.5% | Global (Automotive, Industrial) | 2025-2033 |

| Need for Specialized Design Expertise | -2.5% | Global | 2025-2029 |

| Integration Complexities into Existing Systems | -1.8% | Global | 2025-2028 |

GaN Power Device Market - Updated Report Scope

This comprehensive market research report on the GaN Power Device Market provides an in-depth analysis of market dynamics, including drivers, restraints, opportunities, and challenges influencing market growth. It offers detailed market segmentation across device types, wafer sizes, voltage ranges, and diverse application areas, providing a granular view of market performance. The report includes regional insights, competitive landscape analysis, and a future outlook, equipping stakeholders with critical intelligence for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 350 Million |

| Market Forecast in 2033 | USD 3.8 Billion |

| Growth Rate | 35.00% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies, STMicroelectronics, ON Semiconductor, Nexperia, Rohm Semiconductor, Transphibian, Navitas Semiconductor, GaN Systems, Texas Instruments, Mitsubishi Electric, Sumitomo Electric Industries, Macom Technology Solutions, Cambridge GaN Devices, VisIC Technologies, Efficient Power Conversion (EPC), Dialog Semiconductor (now part of Renesas Electronics), Qorvo, Silan Microelectronics, United Microelectronics Corporation (UMC), Allegro MicroSystems. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The GaN power device market is broadly segmented based on device type, wafer size, voltage range, and various application sectors. This segmentation provides a granular understanding of the market dynamics, identifying specific growth pockets and technological preferences. Each segment exhibits unique characteristics and adoption rates, influenced by industry-specific requirements for power efficiency, size constraints, and cost considerations.

Analyzing these segments helps in comprehending the diverse landscape of GaN applications, from low-voltage consumer electronics to high-voltage industrial and automotive systems. The continued evolution of GaN technology is expected to further refine these segments, driving innovation and expanding market reach into new and existing domains.

- By Device Type:

- GaN Power ICs

- GaN Discretes

- By Wafer Size:

- 4-inch

- 6-inch

- 8-inch

- Others

- By Voltage Range:

- Low Voltage (0-200V)

- Medium Voltage (201-600V)

- High Voltage (601-1200V)

- By Application:

- Consumer Electronics

- Automotive

- Industrial

- Telecommunications

- Renewable Energy

- Others

Regional Highlights

- North America: A significant market driven by technological innovation, increasing adoption in data centers, telecommunications (5G), and early-stage EV integration. The presence of key research institutions and leading technology companies fosters advanced GaN development and application.

- Europe: Exhibits robust growth, particularly in the automotive sector due to strong EV mandates and investments in renewable energy infrastructure. Germany, France, and the UK are key contributors, focusing on industrial power supplies and energy-efficient solutions.

- Asia Pacific (APAC): Dominates the market due to its large consumer electronics manufacturing base (China, South Korea), rapid expansion of 5G networks, and significant investments in electric vehicle production. China is a major market for both production and consumption of GaN power devices. Japan also contributes significantly to technological advancements and automotive applications.

- Latin America: Expected to show gradual growth, primarily influenced by increasing investments in renewable energy projects and the nascent adoption of electric vehicles and associated charging infrastructure.

- Middle East and Africa (MEA): Growth is anticipated to be driven by infrastructure development, smart city initiatives, and increasing investments in solar power, creating demand for efficient power conversion solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the GaN Power Device Market.- Infineon Technologies

- STMicroelectronics

- ON Semiconductor

- Nexperia

- Rohm Semiconductor

- Transphibian

- Navitas Semiconductor

- GaN Systems

- Texas Instruments

- Mitsubishi Electric

- Sumitomo Electric Industries

- Macom Technology Solutions

- Cambridge GaN Devices

- VisIC Technologies

- Efficient Power Conversion (EPC)

- Dialog Semiconductor

- Qorvo

- Silan Microelectronics

- United Microelectronics Corporation (UMC)

- Allegro MicroSystems

Frequently Asked Questions

What is the projected growth rate of the GaN Power Device Market?

The GaN Power Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 35.00% between 2025 and 2033.

What are the primary applications driving the GaN Power Device Market?

The primary applications driving the GaN Power Device Market include consumer electronics (especially fast charging), electric vehicles (EVs) and charging infrastructure, 5G telecommunications, and data centers, due to GaN's efficiency and miniaturization benefits.

How does AI impact the demand for GaN Power Devices?

AI significantly impacts demand by requiring highly efficient, compact power management solutions for AI accelerators, servers, and edge computing. GaN's superior switching speeds and lower power losses are crucial for powering advanced AI hardware.

What are the main challenges facing the GaN Power Device Market?

Key challenges include higher manufacturing costs compared to silicon, concerns regarding long-term reliability in some applications, competition from mature silicon carbide (SiC) technology, and the need for specialized design expertise.

Which regions are leading in GaN Power Device market adoption?

Asia Pacific (APAC), particularly China, leads in adoption due to its large consumer electronics and EV manufacturing sectors. North America and Europe are also strong markets, driven by innovation in data centers, 5G, and automotive electrification.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted