Furnace Carbon Black Market

Furnace Carbon Black Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706956 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

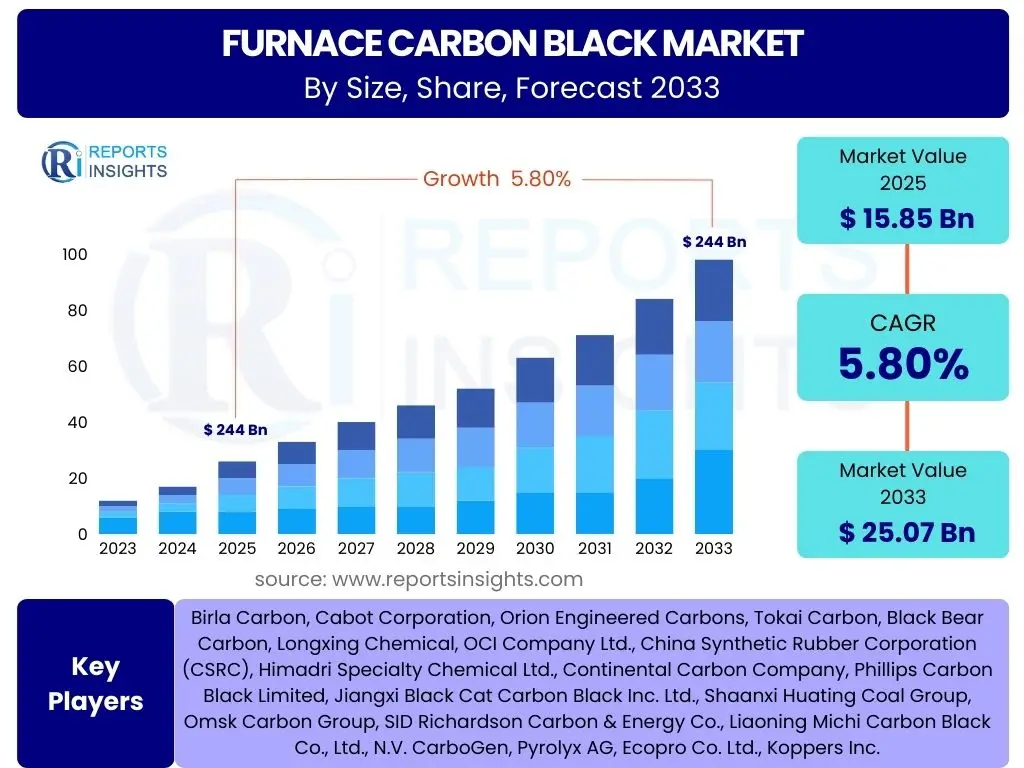

Furnace Carbon Black Market Size

According to Reports Insights Consulting Pvt Ltd, The Furnace Carbon Black Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 15.85 Billion in 2025 and is projected to reach USD 25.07 Billion by the end of the forecast period in 2033.

Key Furnace Carbon Black Market Trends & Insights

Common inquiries about market trends for furnace carbon black highlight a strong interest in sustainability initiatives, technological advancements in production, and the evolving demand landscape across various end-use industries. Users frequently question the impact of electric vehicles on tire demand, the growth trajectory of specialty carbon black, and the adoption of bio-based alternatives. There is also a keen focus on the influence of stringent environmental regulations and the strategies manufacturers are employing to comply while maintaining competitiveness. Overall, the market is observed to be in a dynamic phase, balancing traditional applications with emerging green technologies and innovative material demands.

The market is witnessing a significant shift towards more environmentally friendly production methods, including the exploration of pyrolysis processes for end-of-life tires and the development of carbon black from biomass sources. This trend is driven by increasing consumer awareness, corporate sustainability goals, and stricter global emissions standards. Concurrently, the demand for specialty carbon black grades is expanding rapidly, particularly in non-tire applications such such as plastics, coatings, and conductive polymers. These applications require specific properties like UV resistance, electrical conductivity, and enhanced pigmentation, pushing manufacturers to invest in research and development for customized solutions. The convergence of these trends underscores a dual focus on performance innovation and environmental responsibility within the furnace carbon black industry.

- Increasing adoption of sustainable and bio-based carbon black.

- Growing demand for specialty carbon black in non-tire applications.

- Development of advanced carbon black grades for enhanced performance.

- Impact of electric vehicle proliferation on tire and non-tire applications.

- Focus on circular economy principles, including carbon black recovery from waste tires.

AI Impact Analysis on Furnace Carbon Black

Users commonly inquire about the application of artificial intelligence in industrial processes, specifically how it can enhance efficiency, reduce costs, and improve product quality within the furnace carbon black sector. There is significant interest in predictive analytics for equipment maintenance, optimization of reaction parameters, and the potential for AI-driven material discovery. Concerns often revolve around data privacy, the initial investment required for AI integration, and the need for skilled personnel to manage these advanced systems. Expectations are high regarding AI's role in achieving greater sustainability through optimized energy consumption and reduced waste, reflecting a desire for both operational excellence and environmental stewardship.

The integration of AI technologies is poised to revolutionize several aspects of furnace carbon black production and supply chain management. AI-powered algorithms can analyze vast datasets from production lines to identify optimal operating conditions, leading to significant improvements in yield, consistency, and energy efficiency. This includes fine-tuning furnace temperatures, feedstock ratios, and reaction times to produce carbon black with precise specifications, thereby reducing off-spec material and waste. Furthermore, AI's capability in predictive maintenance can anticipate equipment failures, minimizing costly downtime and extending the lifespan of critical machinery. This proactive approach ensures smoother operations and reduces overall maintenance expenditures, contributing to a more resilient and cost-effective production environment.

Beyond process optimization, AI is also expected to play a crucial role in advancing research and development for new carbon black formulations. Machine learning models can quickly screen potential material combinations and predict their properties, accelerating the discovery of novel grades for emerging applications like advanced batteries or lightweight composites. In logistics, AI can optimize supply chain routes and inventory management, ensuring timely delivery of raw materials and finished products while minimizing transportation costs and carbon footprint. While the initial investment and the need for specialized data scientists present challenges, the long-term benefits in terms of operational efficiency, product innovation, and environmental performance are expected to drive significant AI adoption in the furnace carbon black market.

- Optimization of production processes for increased yield and energy efficiency.

- Predictive maintenance of machinery to reduce downtime and operational costs.

- Enhanced quality control through real-time data analysis and anomaly detection.

- Accelerated R&D for new carbon black formulations and applications.

- Improved supply chain management and logistics efficiency.

Key Takeaways Furnace Carbon Black Market Size & Forecast

Users frequently seek concise summaries of market projections, including factors driving growth, regional hotspots, and the overall trajectory of the furnace carbon black market. They are interested in understanding the dominant application areas, the influence of evolving regulatory landscapes, and the emergence of new product categories or sustainable alternatives. Queries also focus on the competitive intensity and the strategies adopted by leading players to maintain market position and expand their reach. The overarching goal for users is to grasp the most critical insights without delving into extensive data, allowing for quick strategic decision-making and a clear understanding of the market's future outlook.

The furnace carbon black market is projected to experience consistent growth, primarily propelled by sustained demand from the automotive industry, particularly in tire manufacturing, and a burgeoning need for specialty grades across various non-tire sectors. Asia Pacific is anticipated to remain the leading region due to robust industrial expansion and increasing vehicle production, while Europe and North America will focus on innovation and sustainable solutions. The market’s trajectory will increasingly be shaped by the shift towards environmentally friendly production methods and the development of advanced carbon black materials tailored for high-performance applications. This dynamic environment necessitates strategic adaptations from manufacturers to capitalize on new opportunities and mitigate challenges related to raw material volatility and environmental compliance.

- Stable growth driven by continuous demand from the global automotive sector.

- Significant expansion in specialty carbon black applications beyond tires.

- Asia Pacific region projected to maintain its dominance in market share.

- Increasing industry focus on sustainable production and bio-based alternatives.

- Innovation in product development to meet evolving performance requirements.

Furnace Carbon Black Market Drivers Analysis

The furnace carbon black market is significantly propelled by its extensive application across various industries, with the automotive sector, particularly tire manufacturing, serving as the primary growth engine. The continuous global production of vehicles, both passenger and commercial, directly correlates with the demand for tires, which heavily rely on carbon black for reinforcement, durability, and performance enhancement. As vehicle sales and usage continue to rise in emerging economies, the demand for replacement and original equipment tires consistently drives the consumption of furnace carbon black. This sustained demand from the automotive value chain underscores the fundamental importance of carbon black as a key component in mobility solutions.

Moreover, the increasing adoption of specialty carbon black in non-tire applications, including plastics, coatings, and inks, provides additional impetus to the market. These specialty grades offer enhanced UV resistance, electrical conductivity, and pigmentation capabilities, catering to the growing demands of diverse end-use industries like electronics, construction, and consumer goods. The expanding industrial rubber sector, encompassing products such as conveyor belts, hoses, and seals, also contributes substantially, as carbon black is indispensable for improving their mechanical properties and longevity. The ongoing innovations in material science, leading to new formulations and applications for carbon black across these diverse sectors, also play a crucial role in sustaining its market expansion, ensuring its relevance in an evolving industrial landscape.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Automotive Industry & Tire Production | +0.7% | Global, especially Asia Pacific (China, India), North America, Europe | Continuous, Mid- to Long-term |

| Increasing Demand from Industrial Rubber Products | +0.5% | Asia Pacific, Europe, North America | Mid-term |

| Expanding Application of Specialty Carbon Black in Plastics & Coatings | +0.6% | Global, particularly developed economies | Long-term |

| Rising Infrastructure and Construction Activities | +0.4% | Asia Pacific, Latin America, Middle East & Africa | Mid- to Long-term |

Furnace Carbon Black Market Restraints Analysis

Despite its widespread utility, the furnace carbon black market faces notable restraints that can impede its growth trajectory. One significant challenge stems from the volatility of crude oil prices, as petroleum-derived feedstocks are primary raw materials for carbon black production. Fluctuations in crude oil prices directly impact production costs, affecting manufacturers' profit margins and potentially leading to price instability in the downstream market, which can deter consistent demand. This dependency on fossil fuels also exposes the market to geopolitical risks and supply chain disruptions associated with global oil production and distribution, creating a degree of uncertainty for market participants.

Furthermore, increasingly stringent environmental regulations around the globe pose a considerable restraint. Carbon black production is an energy-intensive process that can generate significant air emissions, including greenhouse gases and particulate matter. Governments and environmental agencies are imposing stricter limits on these emissions, compelling manufacturers to invest heavily in pollution control technologies and sustainable production methods, which adds to operational costs and can slow down capacity expansion. Concerns about the health impacts of particulate matter exposure further amplify regulatory pressures, pushing the industry towards cleaner and more environmentally friendly alternatives, even as the cost of compliance rises significantly.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Crude Oil Prices and Feedstock Costs | -0.4% | Global | Short- to Mid-term |

| Stringent Environmental Regulations and Emissions Standards | -0.3% | Europe, North America, parts of Asia Pacific | Continuous, Long-term |

| Health Concerns Related to Carbon Black Exposure | -0.2% | Global, particularly in occupational settings | Continuous |

| Competition from Alternative Reinforcing Materials | -0.1% | Specific application segments | Long-term |

Furnace Carbon Black Market Opportunities Analysis

The furnace carbon black market is poised for significant opportunities driven by evolving industry trends and technological advancements. A key opportunity lies in the development and adoption of bio-based or "green" carbon black alternatives. As industries increasingly prioritize sustainability and circular economy principles, the demand for carbon black derived from renewable sources, such as biomass or end-of-life tires, is growing. This shift not only addresses environmental concerns related to traditional production but also offers a pathway to reduce reliance on fossil feedstocks, opening new market segments and attracting environmentally conscious consumers and manufacturers seeking to improve their product life cycle assessments. Investment in these sustainable pathways can create a competitive advantage for pioneering companies.

Additionally, the expansion of applications beyond traditional rubber and tire uses presents a substantial growth avenue. Carbon black is increasingly being utilized in emerging technologies, including advanced battery electrodes for electric vehicles and energy storage, conductive polymers for electronic components, and lightweight composites for automotive and aerospace industries. These high-value applications, driven by innovation in electric vehicles, portable electronics, and smart infrastructure, demand specialized grades of carbon black with tailored properties, creating premium market niches and fostering research and development investments. The increasing focus on recycling end-of-life products containing carbon black also creates opportunities for resource recovery and new business models within the circular economy framework, further diversifying revenue streams for manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based and Recycled Carbon Black (rCB) | +0.6% | Europe, North America, progressive Asia Pacific markets | Mid- to Long-term |

| Growing Applications in Conductive Polymers & Battery Technologies | +0.5% | Global, particularly tech-driven economies | Long-term |

| Increasing Use in High-Performance Coatings and Inks | +0.4% | Developed and developing economies | Mid-term |

| Digitalization and Automation of Production Processes | +0.3% | Global, leading manufacturers | Continuous |

Furnace Carbon Black Market Challenges Impact Analysis

The furnace carbon black market grapples with several inherent challenges that can impact its growth and operational stability. One primary challenge is the high energy consumption associated with the furnace process, which is a major contributor to operational costs and environmental footprint. The energy-intensive nature of converting hydrocarbon feedstocks into carbon black necessitates substantial fuel inputs, making the industry susceptible to energy price volatility and placing pressure on profitability, especially in regions with high energy costs or strict carbon pricing mechanisms. This also drives the need for continuous investment in energy efficiency technologies, which can be costly and requires significant capital expenditure.

Another significant challenge revolves around the environmental implications of waste disposal and emissions from production facilities. Despite efforts to mitigate pollution through advanced abatement technologies, the industry faces ongoing scrutiny regarding its environmental impact, including air quality concerns from particulate emissions and the proper management of solid waste by-products. Meeting increasingly stringent environmental regulations requires significant capital expenditure for plant upgrades and operational adjustments, which can be a barrier to entry for new players and a continuous cost for existing ones. Furthermore, maintaining supply chain resilience amidst geopolitical tensions, raw material supply fluctuations, and global logistical disruptions presents a constant challenge for ensuring consistent production and timely delivery to a global customer base, adding complexity to market operations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption and Operational Costs | -0.3% | Global | Continuous |

| Waste Management and Disposal Issues | -0.2% | Global, particularly regions with strict waste regulations | Long-term |

| Fluctuating Raw Material Quality and Availability | -0.1% | Global | Short- to Mid-term |

| Logistical Complexities and Supply Chain Disruptions | -0.2% | Global | Short-term |

Furnace Carbon Black Market - Updated Report Scope

This comprehensive report on the Furnace Carbon Black Market provides an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and regions. It offers a detailed forecast from 2025 to 2033, incorporating insights from historical data and current market dynamics. The scope covers a thorough examination of technological advancements, sustainability initiatives, and the competitive landscape, providing stakeholders with critical intelligence for strategic decision-making. The report aims to deliver actionable insights into market growth potential, key influencing factors, and regional market specificities, enabling a holistic understanding of the industry's trajectory and opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.85 Billion |

| Market Forecast in 2033 | USD 25.07 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Birla Carbon, Cabot Corporation, Orion Engineered Carbons, Tokai Carbon, Black Bear Carbon, Longxing Chemical, OCI Company Ltd., China Synthetic Rubber Corporation (CSRC), Himadri Specialty Chemical Ltd., Continental Carbon Company, Phillips Carbon Black Limited, Jiangxi Black Cat Carbon Black Inc. Ltd., Shaanxi Huating Coal Group, Omsk Carbon Group, SID Richardson Carbon & Energy Co., Liaoning Michi Carbon Black Co., Ltd., N.V. CarboGen, Pyrolyx AG, Ecopro Co. Ltd., Koppers Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Furnace Carbon Black Market is comprehensively segmented to provide a granular understanding of its diverse applications and product types, allowing for precise market analysis and strategic planning. This segmentation assists stakeholders in identifying high-growth areas and tailoring their offerings to specific industry needs. The classification by type, application, and end-use industry reflects the varied properties and functionalities of furnace carbon black, from reinforcing agents in rubber to specialty additives in paints and plastics, highlighting its versatility and indispensable role across numerous sectors.

The market's primary segmentation by type differentiates between Hard Carbon Black, known for its high reinforcement properties essential in tire treads, and Soft Carbon Black, which offers improved processability and is often used in inner liners and industrial rubber goods. Further segmentation by application outlines its critical roles in tires, various industrial rubber products, plastics, coatings & inks, and electrical & electronics, among others. The end-use industry segmentation provides insight into its consumption across major sectors such as automotive, building & construction, packaging, and consumer goods, indicating the broad economic reliance on this material. This multi-layered segmentation ensures a detailed perspective on market dynamics and consumer demand patterns.

- By Type:

- Hard Carbon Black

- Soft Carbon Black

- By Application:

- Tires

- Industrial Rubber Products

- Plastics

- Coatings & Inks

- Electrical & Electronics

- Others

- By End-Use Industry:

- Automotive

- Building & Construction

- Packaging

- Consumer Goods

- Others

Regional Highlights

- Asia Pacific: This region is poised to maintain its dominant position in the furnace carbon black market, primarily driven by robust growth in the automotive sector, especially in countries like China, India, Japan, and South Korea. Rapid industrialization, expanding manufacturing bases, and significant infrastructure development across the region fuel high demand for tires, industrial rubber products, and specialty applications. Favorable government policies supporting domestic manufacturing also contribute to the region's strong market presence and continued expansion.

- North America: The North American market exhibits stable demand, characterized by a mature automotive industry and a strong emphasis on research and development for advanced materials. Growth is largely propelled by the increasing adoption of specialty carbon black in high-performance plastics, conductive applications, and coatings. Stringent environmental regulations in the region are also driving innovation towards more sustainable production methods and the adoption of recycled carbon black.

- Europe: Europe represents a mature but innovation-driven market, with a significant focus on sustainability and circular economy initiatives. Demand for furnace carbon black is consistent from the automotive industry and industrial rubber sectors, coupled with a growing need for specialty grades in high-end applications. The region's strict environmental policies are compelling manufacturers to invest heavily in eco-friendly production processes and bio-based alternatives, fostering a competitive landscape focused on green solutions.

- Latin America: The Latin American market is emerging with significant growth potential, particularly in Brazil and Mexico, due to expanding automotive production and ongoing infrastructure development. While currently a smaller share, the region is expected to witness steady demand growth as industrial activities increase and consumer purchasing power improves.

- Middle East and Africa (MEA): This region is a nascent market for furnace carbon black but shows promising growth prospects driven by increasing industrialization, urbanization, and investment in manufacturing sectors. The market is expected to expand with rising demand from construction, automotive, and general industrial applications, albeit from a smaller base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Furnace Carbon Black Market.- Birla Carbon

- Cabot Corporation

- Orion Engineered Carbons

- Tokai Carbon

- Black Bear Carbon

- Longxing Chemical

- OCI Company Ltd.

- China Synthetic Rubber Corporation (CSRC)

- Himadri Specialty Chemical Ltd.

- Continental Carbon Company

- Phillips Carbon Black Limited

- Jiangxi Black Cat Carbon Black Inc. Ltd.

- Shaanxi Huating Coal Group

- Omsk Carbon Group

- SID Richardson Carbon & Energy Co.

- Liaoning Michi Carbon Black Co., Ltd.

- N.V. CarboGen

- Pyrolyx AG

- Ecopro Co. Ltd.

- Koppers Inc.

Frequently Asked Questions

Analyze common user questions about the Furnace Carbon Black market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Furnace Carbon Black and its primary uses?

Furnace carbon black is a finely divided form of amorphous carbon produced by the incomplete combustion of heavy petroleum products. Its primary use is as a reinforcing filler in rubber products, especially tires, where it enhances strength, durability, and wear resistance. It is also used as a pigment, UV stabilizer, and conductive agent in plastics, coatings, and inks.

How is the Furnace Carbon Black market segmented?

The market is primarily segmented by type (Hard Carbon Black, Soft Carbon Black), by application (Tires, Industrial Rubber Products, Plastics, Coatings & Inks, Electrical & Electronics, Others), and by end-use industry (Automotive, Building & Construction, Packaging, Consumer Goods, Others). These segments reflect its diverse functionalities and applications across various sectors.

What are the key factors driving the growth of the Furnace Carbon Black market?

Key drivers include the continuous growth of the global automotive industry and tire production, increasing demand for industrial rubber products, expanding applications of specialty carbon black in plastics and coatings, and rising infrastructure and construction activities. The material's essential role in enhancing product performance across these sectors underpins its market expansion.

What are the major challenges faced by the Furnace Carbon Black industry?

Major challenges include the volatility of crude oil prices affecting feedstock costs, stringent environmental regulations regarding emissions and waste disposal, high energy consumption in the production process, and the need for continuous investment in sustainable technologies. These factors impact profitability and operational complexity.

Which regions are expected to witness significant growth in the Furnace Carbon Black market?

Asia Pacific is projected to be the leading region due to its expanding automotive manufacturing base and rapid industrialization. North America and Europe will also see growth, driven by specialty applications and a strong focus on sustainable production methods. Emerging economies in Latin America and MEA are also showing potential for market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted