Fuel Deposit Control Agent Market

Fuel Deposit Control Agent Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702069 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Fuel Deposit Control Agent Market Size

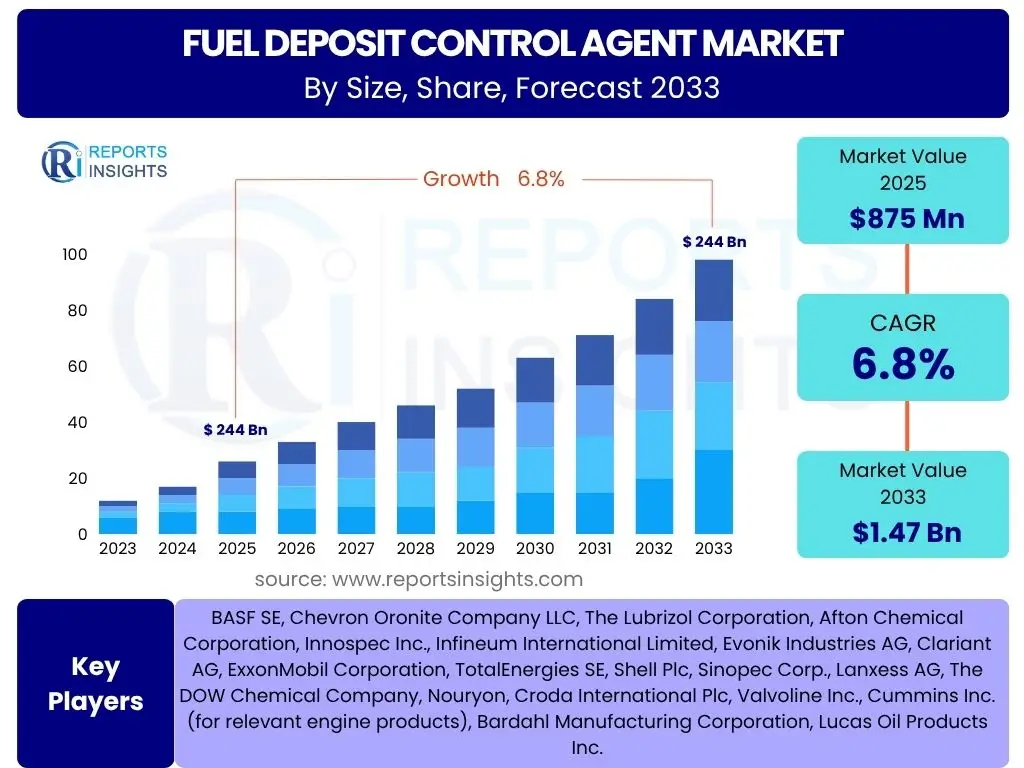

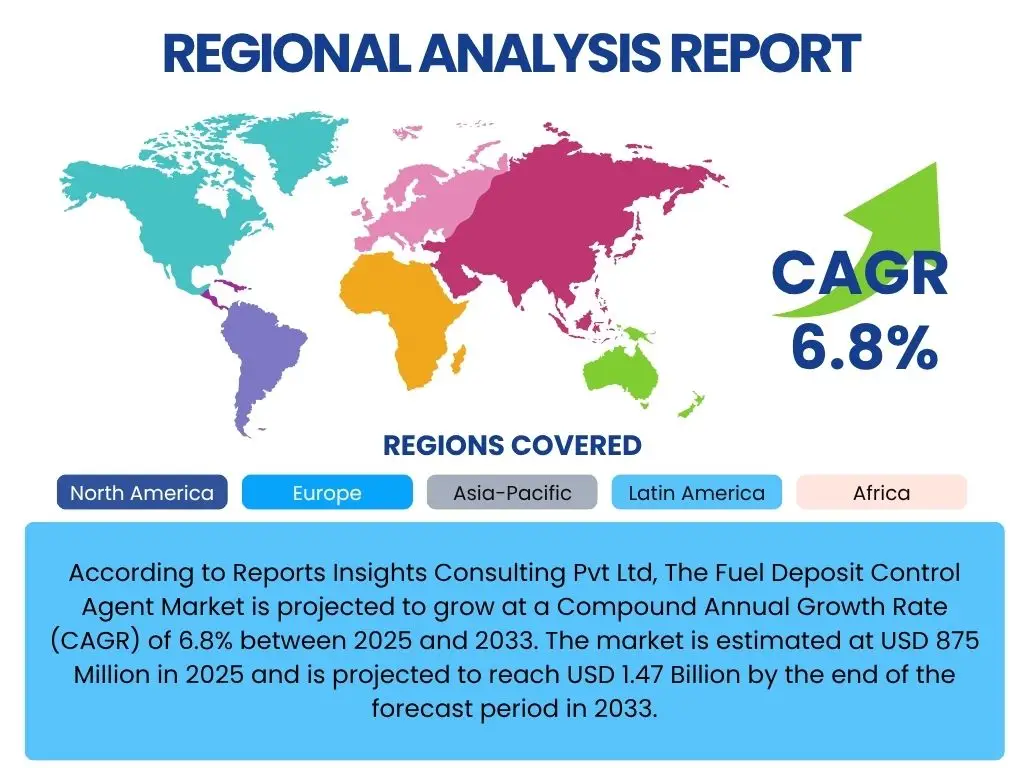

According to Reports Insights Consulting Pvt Ltd, The Fuel Deposit Control Agent Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 875 Million in 2025 and is projected to reach USD 1.47 Billion by the end of the forecast period in 2033.

Key Fuel Deposit Control Agent Market Trends & Insights

The Fuel Deposit Control Agent market is undergoing significant evolution, primarily driven by the global emphasis on enhancing fuel efficiency, reducing harmful emissions, and extending engine lifespan. A prominent trend is the increasing stringency of environmental regulations worldwide, which mandates lower particulate matter and nitrogen oxide emissions from internal combustion engines. This regulatory pressure compels fuel refiners and automotive manufacturers to adopt advanced deposit control agents that can effectively prevent the formation of carbon deposits in critical engine components such as injectors, valves, and combustion chambers. The market is witnessing a shift towards multi-functional additive packages that offer not only deposit control but also corrosion protection, lubrication, and friction modification benefits, catering to the sophisticated demands of modern engine technologies.

Another crucial insight is the growing demand for higher performance fuels and the proliferation of direct injection (DI) gasoline and common rail diesel engines. These advanced engine designs, while more efficient, are highly susceptible to deposit formation, which can severely impact their performance, fuel economy, and emissions profiles. Consequently, there is an escalating need for highly effective deposit control agents specifically engineered to prevent and remove deposits in these precision components. The rise of biofuels and flex-fuel vehicles also presents a unique set of challenges and opportunities, driving research and development into new additive chemistries compatible with diverse fuel blends and capable of addressing issues specific to these alternative fuels, such as water separation and stability.

- Increasingly stringent global emission regulations driving demand for cleaner burning fuels.

- Rising adoption of direct injection (DI) gasoline and common rail diesel engines requiring superior deposit control.

- Shift towards multi-functional additive packages offering comprehensive fuel treatment.

- Growing focus on fuel efficiency and engine longevity by consumers and industries.

- Emergence of new additive chemistries compatible with biofuels and alternative fuel blends.

- Technological advancements in fuel refining processes demanding specialized additive solutions.

AI Impact Analysis on Fuel Deposit Control Agent

Artificial Intelligence (AI) is poised to significantly transform various aspects of the Fuel Deposit Control Agent market, from research and development to manufacturing and supply chain management. Common user questions often revolve around how AI can accelerate the discovery of novel additive chemistries or optimize existing formulations. AI-powered predictive modeling and simulation tools can analyze vast datasets of chemical structures and their performance characteristics, dramatically shortening the time required for identifying promising candidates for new deposit control agents. This enables researchers to predict the efficacy of potential additives against various types of deposits under different engine conditions, reducing the need for extensive physical testing and thereby cutting R&D costs and time-to-market for innovative solutions.

Furthermore, AI can enhance operational efficiency and quality control within the manufacturing processes of fuel additives. Users frequently inquire about AI's role in optimizing production parameters and ensuring product consistency. Machine learning algorithms can monitor real-time production data, identify anomalies, predict equipment failures, and optimize batch processes to maintain stringent quality standards for deposit control agents. In the supply chain, AI-driven analytics can improve demand forecasting, inventory management, and logistics, ensuring a more resilient and responsive supply of these critical chemicals to refiners and blenders. While the direct application in engine operation might be limited, AI's indirect influence through optimized additive development and deployment will be profound, addressing concerns about cost-effectiveness, performance reliability, and environmental impact.

- Accelerated discovery and design of novel deposit control chemistries through AI-driven predictive modeling and simulation.

- Optimization of manufacturing processes for fuel additives, enhancing efficiency and product quality.

- Improved demand forecasting and supply chain management for raw materials and finished products.

- Personalized additive formulations based on specific fuel types and engine characteristics using data analytics.

- Predictive maintenance for engine components, potentially informing the targeted use of specific deposit control agents.

Key Takeaways Fuel Deposit Control Agent Market Size & Forecast

The Fuel Deposit Control Agent market is positioned for robust growth throughout the forecast period, driven by an confluence of regulatory mandates, technological advancements in engine design, and increasing consumer awareness regarding vehicle maintenance and efficiency. A key takeaway is the consistent upward trajectory of market size, reflecting the indispensable role these agents play in modern fuel systems. The forecasted growth underscores the persistent need for effective solutions to combat fuel system deposits, which directly impact engine performance, fuel economy, and emission compliance across various transportation and industrial sectors. This growth is not merely volumetric but also indicative of a market that is evolving towards more specialized, high-performance, and environmentally benign additive formulations.

Another crucial insight from the market forecast is the strong correlation between market expansion and the global push for sustainability. As countries worldwide implement stricter emission standards and as manufacturers develop more intricate and sensitive engine designs, the reliance on advanced fuel deposit control agents becomes paramount. The market will continue to be influenced by innovations in fuel chemistry, the adoption of alternative fuels, and the ongoing modernization of vehicle fleets in developing economies. Consequently, companies operating in this space will need to prioritize research and development, strategic partnerships, and global market penetration to capitalize on the sustained demand for sophisticated fuel treatment solutions that deliver tangible benefits in terms of operational efficiency and environmental protection.

- Significant market growth projected through 2033, driven by regulatory and technological factors.

- Increasing importance of deposit control agents in achieving optimal engine performance and fuel efficiency.

- Strong demand across diverse applications including automotive, marine, and industrial sectors.

- Emphasis on advanced, multi-functional additive solutions to meet evolving engine requirements.

- Continuous innovation in additive chemistry to address challenges posed by new fuel types and engine designs.

Fuel Deposit Control Agent Market Drivers Analysis

The Fuel Deposit Control Agent market is primarily propelled by the global imperative to enhance engine efficiency and comply with increasingly stringent environmental regulations. The continuous development of advanced internal combustion engines, including Gasoline Direct Injection (GDI) and common rail diesel systems, necessitates cleaner fuel delivery to maintain optimal performance and prevent premature wear. These sophisticated engine designs are highly susceptible to carbon deposits, which can severely impede fuel atomization, airflow, and combustion efficiency. Consequently, the demand for effective fuel deposit control agents is rising as they are crucial for preventing deposit formation on injectors, intake valves, and combustion chambers, thereby ensuring consistent engine operation, maximizing fuel economy, and reducing harmful emissions.

Furthermore, the escalating global vehicle parc, particularly in emerging economies, contributes significantly to market growth. As more vehicles are introduced, the collective demand for fuel additives to maintain engine health and performance increases. Simultaneously, rising fuel prices incentivize consumers and fleet operators to seek solutions that enhance fuel efficiency and prolong engine life, making deposit control agents a cost-effective investment. The growing awareness among end-users about the long-term benefits of using quality fuel additives, coupled with original equipment manufacturers (OEMs) increasingly recommending or factory-filling vehicles with fuels containing such additives, further stimulates market expansion. This confluence of regulatory, technological, economic, and awareness factors creates a robust demand environment for fuel deposit control agents.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasingly Stringent Emission Regulations | +1.5% | North America, Europe, Asia Pacific | Short-to-Medium Term |

| Growth in Automotive Production and Vehicle Parc | +1.2% | Asia Pacific, Latin America, MEA | Medium-to-Long Term |

| Advancements in Engine Technologies (GDI, Common Rail) | +1.0% | Global | Short-to-Medium Term |

| Rising Consumer Awareness on Fuel Efficiency & Engine Health | +0.8% | Global, particularly developed markets | Medium Term |

Fuel Deposit Control Agent Market Restraints Analysis

Despite robust growth drivers, the Fuel Deposit Control Agent market faces several notable restraints that could temper its expansion. One significant challenge is the volatility in crude oil prices, which directly impacts fuel costs. When fuel prices are low and stable, consumers and fleet operators may perceive less immediate need for additives aimed at improving fuel efficiency, potentially leading to reduced adoption rates. Conversely, extremely high fuel prices might shift consumer focus purely to basic fuel affordability rather than performance-enhancing additives. This price sensitivity, particularly in cost-conscious markets, can limit the willingness of end-users to invest in additional fuel treatments, despite their long-term benefits for engine health and fuel economy.

Another key restraint is the high cost associated with research and development for new and more effective additive formulations. Developing innovative chemistries that meet evolving performance requirements and comply with environmental standards is a capital-intensive and time-consuming process. The regulatory landscape around chemical registration and environmental impact assessment can also be complex and varied across different regions, creating barriers to market entry for new products and increasing operational costs for manufacturers. Furthermore, a general lack of widespread consumer awareness or misconceptions about the efficacy of fuel additives in certain regions can act as a significant impediment, as some users may view them as unnecessary expenses rather than essential maintenance components.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Crude Oil Prices and Fuel Costs | -0.7% | Global | Short-to-Medium Term |

| High Research & Development Costs for New Formulations | -0.5% | Global | Medium-to-Long Term |

| Lack of Widespread Consumer Awareness in Emerging Markets | -0.4% | Latin America, MEA, parts of APAC | Medium Term |

| Competition from Engine Design Improvements Reducing Deposit Formation | -0.3% | Global | Long Term |

Fuel Deposit Control Agent Market Opportunities Analysis

The Fuel Deposit Control Agent market presents compelling opportunities for growth, particularly through the development of multi-functional additive packages and expansion into untapped or rapidly evolving markets. There is an increasing demand for comprehensive fuel treatment solutions that not only prevent deposits but also offer a range of additional benefits such as improved lubricity, corrosion inhibition, anti-foaming properties, and water demulsification. Companies that can innovate and offer such integrated solutions will gain a competitive edge, addressing the holistic needs of modern engines and diverse fuel types, including those with higher ethanol or biodiesel content. This shift towards value-added offerings creates avenues for premium product development and market differentiation.

Furthermore, significant opportunities lie in the marine and aviation sectors, which are increasingly under pressure to adopt cleaner fuels and reduce their environmental footprint. The advent of low-sulfur fuels and alternative marine fuels (e.g., LNG, methanol) introduces new challenges related to fuel stability and deposit formation, creating a niche for specialized deposit control agents tailored to these applications. Geographically, emerging economies in Asia Pacific, Latin America, and the Middle East and Africa represent substantial growth potential. These regions are experiencing rapid industrialization and a surge in vehicle ownership, often with less stringent fuel quality standards, thereby amplifying the need for effective fuel deposit control to protect engine assets and improve operational efficiencies. Strategic partnerships with fuel distributors and engine manufacturers in these regions can unlock significant market share.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Multi-functional Additive Packages | +1.3% | Global | Short-to-Medium Term |

| Expanding Application in Marine and Aviation Fuels | +1.0% | Global, particularly coastal and major aviation hubs | Medium-to-Long Term |

| Untapped Market Potential in Emerging Economies | +0.9% | Asia Pacific, Latin America, MEA | Short-to-Long Term |

| Integration with Biofuels and Alternative Fuel Chemistries | +0.7% | Europe, North America, Brazil | Medium-to-Long Term |

Fuel Deposit Control Agent Market Challenges Impact Analysis

The Fuel Deposit Control Agent market faces several inherent challenges that demand strategic navigation from industry players. One significant hurdle is the fluctuating prices and availability of key raw materials used in the production of these chemical additives. Many active ingredients are derived from petrochemicals, making their supply chains vulnerable to geopolitical events, crude oil price volatility, and disruptions in chemical manufacturing. This can lead to increased production costs, margin pressures, and challenges in maintaining consistent product pricing for end-users. Ensuring a stable and cost-effective supply of high-quality raw materials is a continuous challenge for manufacturers in this segment.

Another critical challenge is the intense competitive landscape, characterized by the presence of both large multinational chemical companies and specialized additive formulators. This competitive pressure often leads to pricing wars and necessitates continuous innovation to maintain market share. Furthermore, the market is susceptible to the proliferation of counterfeit or sub-standard products, especially in less regulated markets, which not only erode legitimate market share but also damage consumer trust in the efficacy of fuel additives. Rapid advancements in engine technologies, such as the increasing adoption of electric vehicles (EVs) and hybrid vehicles, present a long-term existential challenge to the traditional fuel additive market, as the demand for conventional fuels and their corresponding additives may decline over several decades, prompting companies to diversify or adapt their product portfolios.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuations in Raw Material Prices and Supply | -0.6% | Global | Short-to-Medium Term |

| Intense Competition and Pricing Pressures | -0.5% | Global | Short-to-Medium Term |

| Threat of Counterfeit Products in Underserved Markets | -0.4% | Asia Pacific, Latin America, MEA | Short-to-Medium Term |

| Long-term Impact of Electric Vehicle (EV) Adoption | -0.2% | Global, particularly developed markets | Long Term |

Fuel Deposit Control Agent Market - Updated Report Scope

This market research report provides a comprehensive analysis of the Fuel Deposit Control Agent market, offering in-depth insights into its size, growth trajectory, key trends, drivers, restraints, opportunities, and challenges across various segments and major geographies. The report covers historical market performance, current market dynamics, and future projections, aiming to equip stakeholders with actionable intelligence for strategic decision-making. It delves into the impact of technological advancements and regulatory shifts on market evolution, providing a holistic view of the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 875 Million |

| Market Forecast in 2033 | USD 1.47 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Chevron Oronite Company LLC, The Lubrizol Corporation, Afton Chemical Corporation, Innospec Inc., Infineum International Limited, Evonik Industries AG, Clariant AG, ExxonMobil Corporation, TotalEnergies SE, Shell Plc, Sinopec Corp., Lanxess AG, The DOW Chemical Company, Nouryon, Croda International Plc, Valvoline Inc., Cummins Inc. (for relevant engine products), Bardahl Manufacturing Corporation, Lucas Oil Products Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fuel Deposit Control Agent market is meticulously segmented to provide a granular view of its diverse applications and chemical compositions. This comprehensive segmentation allows for a precise understanding of demand patterns and growth drivers across various end-use industries and fuel types. The primary segments include categorization by the type of fuel they treat, the underlying chemical composition of the agents, their specific application areas, and the end-use channels through which they are distributed, reflecting the multifaceted nature of the market and the varied requirements of its consumers.

- By Type:

- Gasoline Deposit Control Agents: Formulations optimized for gasoline engines, addressing issues like intake valve deposits and fuel injector deposits in both port fuel injection (PFI) and gasoline direct injection (GDI) systems.

- Diesel Deposit Control Agents: Designed for diesel engines, tackling problems such as common rail injector deposits, internal diesel injector deposits (IDID), and fuel filter plugging.

- Aviation Fuel Deposit Control Agents: Specialized additives for aviation turbine fuels (jet fuels), focusing on thermal stability and deposit prevention in high-temperature environments.

- Marine Fuel Deposit Control Agents: Formulations for marine diesel and heavy fuel oils, addressing deposit control, sludge prevention, and corrosion in large marine engines.

- By Chemistry:

- Polyisobutylene Amine (PIBA): Widely used for gasoline engines, known for its detergency and ability to clean intake valves.

- Polyether Amine (PEA): Highly effective for both PFI and GDI engines, offering superior cleaning of fuel injectors and combustion chambers.

- Polyisobutylene Succinimide (PIBSI): Primarily used as dispersants and detergents in various fuel and lubricant applications.

- Others: Includes a range of other chemistries and co-additives like fatty acids, polyol esters, and other polymeric dispersants that enhance the performance of primary deposit control agents.

- By Application:

- Automotive: The largest segment, covering both passenger vehicles (cars, SUVs) and commercial vehicles (trucks, buses), driven by emission regulations and engine efficiency demands.

- Industrial: Applications in power generation, construction, agriculture, and other industrial machinery utilizing diesel or gasoline engines.

- Marine: Essential for large marine vessels, including cargo ships, tankers, and passenger liners, to maintain engine efficiency and reduce operational costs.

- Aviation: Used in jet aircraft to prevent fuel system deposits and maintain engine performance and safety.

- Others: Includes railway locomotives, small engines (e.g., lawnmowers, motorcycles), and stationary engines.

- By End-Use:

- OEMs (Original Equipment Manufacturers): Additives supplied directly to vehicle manufacturers or integrated into factory-fill fuels.

- Aftermarket: Products sold through retail channels, service stations, and automotive parts stores for consumer and commercial vehicle owners to add to their fuel tanks.

Regional Highlights

- North America: This region represents a mature market for Fuel Deposit Control Agents, characterized by stringent emission regulations and a strong emphasis on engine performance and fuel efficiency. The presence of major automotive manufacturers and a high demand for advanced fuel additive technologies contribute to its significant market share. Innovation in additive chemistries and the adoption of advanced engine technologies like GDI drive consistent demand.

- Europe: Europe is a key market, largely driven by the European Union's strict environmental policies and rigorous emission standards (e.g., Euro 6/7). There is a strong focus on developing high-performance, eco-friendly fuel additives. The region's robust automotive industry and the increasing penetration of vehicles with sophisticated fuel injection systems underpin the demand for advanced deposit control solutions.

- Asia Pacific (APAC): APAC stands out as the largest and fastest-growing market for Fuel Deposit Control Agents. This growth is primarily fueled by rapid industrialization, burgeoning vehicle production, increasing disposable incomes, and less stringent, yet evolving, fuel quality standards in several countries like China, India, and Southeast Asian nations. The region's expanding transportation and industrial sectors present immense opportunities for market players.

- Latin America: This region is experiencing steady growth, driven by increasing vehicle sales, urbanization, and a growing awareness among consumers about vehicle maintenance and fuel efficiency. While regulatory frameworks may be less uniform compared to developed regions, the demand for improved fuel quality and engine protection is on the rise, creating a fertile ground for market expansion.

- Middle East and Africa (MEA): The MEA region is witnessing growth propelled by significant investments in infrastructure, industrial development, and an expanding transportation sector. While the region is a major oil producer, varying fuel quality and the need to protect engine assets in diverse operational environments contribute to the demand for fuel deposit control agents, particularly in the industrial and commercial segments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fuel Deposit Control Agent Market.- BASF SE

- Chevron Oronite Company LLC

- The Lubrizol Corporation

- Afton Chemical Corporation

- Innospec Inc.

- Infineum International Limited

- Evonik Industries AG

- Clariant AG

- ExxonMobil Corporation

- TotalEnergies SE

- Shell Plc

- Sinopec Corp.

- Lanxess AG

- The DOW Chemical Company

- Nouryon

- Croda International Plc

- Valvoline Inc.

- Cummins Inc.

- Bardahl Manufacturing Corporation

- Lucas Oil Products Inc.

Frequently Asked Questions

Analyze common user questions about the Fuel Deposit Control Agent market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are fuel deposit control agents?

Fuel deposit control agents are chemical additives engineered to prevent and remove harmful deposits that accumulate in an engine's fuel system and combustion chamber, ensuring optimal engine performance and efficiency. They are typically added to gasoline, diesel, or other fuels.

How do fuel deposit control agents improve engine performance and fuel efficiency?

By preventing and cleaning deposits on critical components like fuel injectors, intake valves, and combustion chambers, these agents ensure proper fuel atomization, airflow, and combustion. This leads to improved power output, smoother engine operation, reduced emissions, and enhanced fuel economy.

What are the main types of fuel deposit control agents?

The primary types are classified by their chemical composition and target fuel type. Common chemistries include Polyisobutylene Amine (PIBA), Polyether Amine (PEA), and Polyisobutylene Succinimide (PIBSI), formulated for specific use in gasoline, diesel, aviation, or marine fuels.

Which industries widely utilize fuel deposit control agents?

Fuel deposit control agents are extensively used across various industries, predominantly in the automotive sector (passenger and commercial vehicles), industrial machinery, marine shipping, and aviation. They are crucial for maintaining the efficiency and longevity of engines in these applications.

What are the future trends influencing the Fuel Deposit Control Agent market?

Future trends include increasingly stringent emission regulations, the proliferation of advanced engine technologies (e.g., GDI), growing demand for multi-functional additive packages, the integration of AI in R&D, and the development of agents compatible with biofuels and other alternative fuel chemistries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted