Pet Food Flexible Packaging Market

Pet Food Flexible Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701486 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

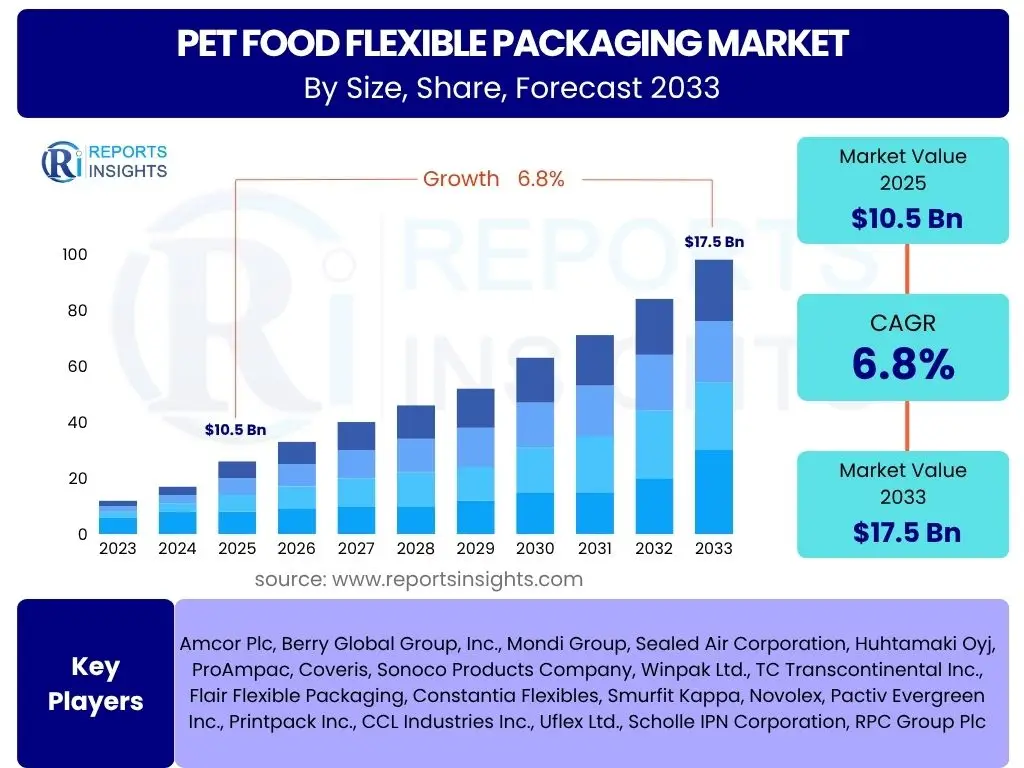

Pet Food Flexible Packaging Market Size

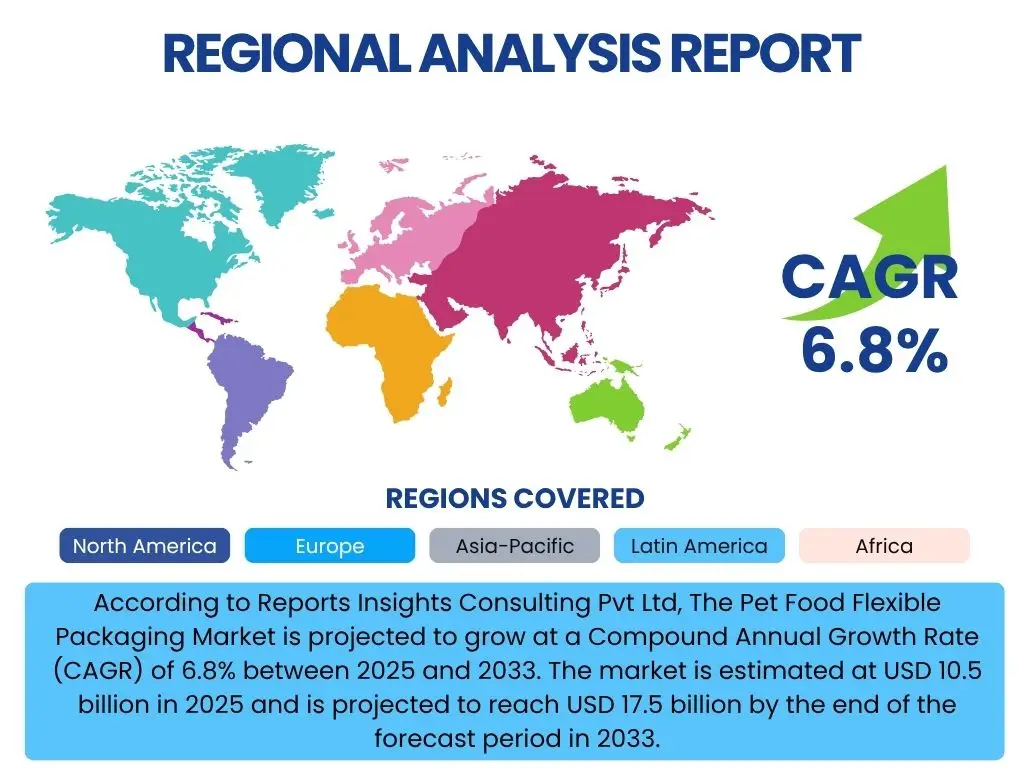

According to Reports Insights Consulting Pvt Ltd, The Pet Food Flexible Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 10.5 billion in 2025 and is projected to reach USD 17.5 billion by the end of the forecast period in 2033.

Key Pet Food Flexible Packaging Market Trends & Insights

User inquiries frequently revolve around the dynamic shifts and innovative directions within the pet food flexible packaging sector. Common questions highlight the increasing consumer demand for convenient, sustainable, and aesthetically pleasing packaging solutions. There is significant interest in how technological advancements and evolving pet owner preferences are shaping product presentation and preservation. Furthermore, the impact of e-commerce on packaging design, emphasizing durability and efficiency for shipping, is a recurrent theme.

Pet owners are increasingly discerning about the environmental footprint of products, leading to a surge in demand for recyclable, compostable, or bio-based packaging materials. Concurrently, the humanization of pets drives demand for premium and differentiated packaging that mirrors human food trends, including resealability and single-serve options. These trends collectively underscore a market moving towards greater functionality, sustainability, and consumer-centric design.

- Increased adoption of sustainable and eco-friendly packaging materials, including recyclable plastics, compostable films, and paper-based solutions.

- Rising demand for convenient packaging formats such as stand-up pouches, re-sealable bags, and single-serve portions, driven by busy lifestyles.

- Growth in e-commerce necessitating durable, lightweight, and shipping-efficient packaging solutions.

- Premiumization of pet food leading to sophisticated packaging designs, enhanced graphics, and specialized functional features.

- Technological advancements in printing (e.g., digital printing) allowing for greater customization and brand differentiation.

AI Impact Analysis on Pet Food Flexible Packaging

Common user questions regarding AI's influence on the pet food flexible packaging industry frequently address its potential to optimize production processes, enhance quality control, and streamline supply chain management. Users are keen to understand how AI can lead to more efficient material usage, reduce waste, and improve operational forecasting. There is also interest in AI's role in personalized packaging design and consumer insights, though concerns about data privacy and the initial investment required for AI implementation are also noted.

AI's analytical capabilities offer transformative potential, moving beyond traditional automation to predictive and adaptive systems. This enables manufacturers to anticipate maintenance needs, optimize inventory levels, and even tailor packaging features based on real-time market data and consumer feedback. The integration of AI promises not only cost efficiencies and reduced environmental impact but also a more responsive and innovative approach to packaging development.

- AI-driven optimization of production lines, leading to reduced waste, increased efficiency, and predictive maintenance for packaging machinery.

- Enhanced quality control through AI-powered visual inspection systems that detect defects with high precision and speed.

- Improved supply chain management and logistics, including demand forecasting, inventory optimization, and route planning for distribution.

- Personalization and customization of packaging designs based on consumer data and AI-driven market trend analysis.

- Development of smart packaging solutions integrating AI for real-time monitoring of product freshness, authenticity, and traceability.

Key Takeaways Pet Food Flexible Packaging Market Size & Forecast

Analysis of common user questions concerning the pet food flexible packaging market size and forecast reveals a strong interest in understanding the primary drivers behind its projected growth and the factors that might influence its trajectory. Users frequently ask about the role of evolving consumer preferences, the impact of pet humanization, and the increasing focus on sustainability in shaping market expansion. The overarching insight is that the market's growth is fundamentally tied to the dynamic shifts in pet ownership demographics, consumer values, and technological advancements in packaging materials and processes.

The forecast indicates sustained growth, primarily propelled by the global increase in pet ownership and the growing trend of treating pets as family members, which translates into demand for high-quality, convenient, and ethically produced pet food and its packaging. While innovations in sustainable packaging and e-commerce readiness present significant opportunities, challenges related to raw material price volatility and regulatory complexities remain critical considerations for market stakeholders.

- The market is poised for robust growth, driven by rising global pet adoption rates and the humanization of pets.

- Sustainability initiatives, including recyclable and biodegradable materials, are becoming central to packaging innovation and consumer preference.

- E-commerce expansion significantly influences packaging design, favoring lightweight, durable, and stackable formats.

- Technological advancements in barrier properties and printing are enhancing product preservation and brand appeal.

- The industry faces challenges related to raw material cost fluctuations and the need for scalable recycling infrastructure.

Pet Food Flexible Packaging Market Drivers Analysis

The pet food flexible packaging market is propelled by several robust drivers, primarily stemming from evolving pet owner demographics and preferences. The global increase in pet ownership, coupled with the growing trend of humanizing pets, directly fuels demand for premium and specialized pet food products, which in turn necessitates advanced packaging solutions. Consumers are increasingly seeking convenience in pet care, driving the adoption of flexible packaging formats like stand-up pouches and resealable bags that offer ease of use, storage, and portion control. Furthermore, the rapid expansion of e-commerce channels for pet food sales mandates packaging that is lightweight, durable, and optimized for shipping efficiency, thereby boosting the flexible packaging segment.

A significant driver is the heightened consumer awareness regarding environmental issues, leading to a strong preference for sustainable and eco-friendly packaging. This has spurred innovations in recyclable, compostable, and bio-based flexible materials, pushing manufacturers to invest in greener solutions to meet market demand and regulatory pressures. The aesthetic appeal and branding opportunities offered by flexible packaging also contribute to its growth, allowing pet food brands to differentiate themselves on crowded shelves through high-quality graphics and innovative designs. These combined factors create a powerful impetus for the sustained expansion of the pet food flexible packaging market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Pet Ownership & Humanization Trend | +1.5% | Global (North America, Europe, Asia Pacific) | Long-term (2025-2033) |

| Increasing Demand for Convenient Packaging Solutions | +1.2% | Developed Markets (North America, Europe) | Mid-term (2025-2029) |

| Growth of E-commerce for Pet Food Sales | +1.0% | Global (Strong in Asia Pacific, North America) | Long-term (2025-2033) |

| Growing Emphasis on Sustainable Packaging | +0.9% | Europe, North America | Long-term (2025-2033) |

| Technological Advancements in Packaging Materials & Printing | +0.7% | Global | Mid-term to Long-term (2025-2033) |

Pet Food Flexible Packaging Market Restraints Analysis

Despite the robust growth drivers, the pet food flexible packaging market faces several significant restraints that could temper its expansion. One primary concern is the volatility in raw material prices, particularly for polymers and other petrochemical derivatives used in plastic films. Fluctuations in crude oil prices directly impact the cost of production, leading to unpredictable operating expenses for packaging manufacturers and potentially higher prices for end-users. This unpredictability can hinder long-term planning and investment in new technologies or sustainable solutions.

Another major restraint is the increasing stringency of regulations concerning plastic waste and environmental pollution. Governments globally are implementing stricter policies on single-use plastics and promoting circular economy models, which can impose significant compliance costs on packaging companies. While these regulations drive innovation in sustainable materials, they also present challenges in terms of material sourcing, manufacturing processes, and waste management infrastructure. Furthermore, competition from alternative packaging formats, such as rigid packaging (e.g., cans, rigid plastic containers) and growing consumer preference for fresh or frozen pet food that might require different packaging solutions, could also limit the market share of flexible packaging. The complexity of recycling multi-layer flexible packaging also remains a hurdle, contributing to consumer and regulatory scrutiny.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% | Global | Mid-term (2025-2029) |

| Stringent Environmental Regulations on Plastics | -0.7% | Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Challenges in Recycling Multi-Layer Flexible Packaging | -0.6% | Global | Long-term (2025-2033) |

| Competition from Rigid Packaging & Alternative Formats | -0.5% | Global | Long-term (2025-2033) |

| High Initial Investment for Sustainable Technology Adoption | -0.4% | Global | Short-term (2025-2027) |

Pet Food Flexible Packaging Market Opportunities Analysis

The pet food flexible packaging market presents numerous opportunities for growth and innovation, driven by evolving consumer demands and technological advancements. A significant opportunity lies in the continuous development and wider adoption of fully recyclable and compostable flexible packaging solutions. As environmental concerns escalate, brands that can offer genuinely sustainable packaging without compromising product integrity or convenience will gain a competitive edge. This includes advancements in mono-material flexible films and bio-based polymers, which address the challenges of traditional multi-layer structures.

Another promising avenue is the integration of smart packaging technologies, such as QR codes, RFID tags, and NFC chips, which can provide enhanced traceability, authenticity verification, and interactive consumer engagement. These technologies can offer valuable information about product origin, nutritional content, and even personalized feeding recommendations, catering to the tech-savvy pet owner. Furthermore, the expansion into emerging markets, particularly in Asia Pacific and Latin America, where pet ownership is on the rise and disposable incomes are increasing, offers substantial untapped potential. These regions are experiencing rapid urbanization and a growing middle class, leading to higher demand for packaged pet food and, consequently, flexible packaging solutions. Customization and personalization trends, enabled by digital printing technologies, also open doors for brands to create unique packaging designs that resonate with specific consumer segments, enhancing brand loyalty and market appeal.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Sustainable Packaging Solutions | +1.3% | Global | Long-term (2025-2033) |

| Integration of Smart Packaging Technologies | +1.0% | Developed Markets (North America, Europe) | Mid-term to Long-term (2027-2033) |

| Expansion into Emerging Markets | +0.9% | Asia Pacific, Latin America | Long-term (2025-2033) |

| Customization & Personalization of Packaging | +0.8% | Global | Mid-term (2025-2029) |

| Innovation in Barrier Properties for Enhanced Shelf Life | +0.7% | Global | Long-term (2025-2033) |

Pet Food Flexible Packaging Market Challenges Impact Analysis

The pet food flexible packaging market, while dynamic, contends with several significant challenges that necessitate strategic responses from industry players. One major challenge is managing the complexity of waste management and achieving a truly circular economy for flexible packaging materials. Despite advancements in recyclable films, the widespread infrastructure for collection, sorting, and processing of multi-layer flexible plastics remains inadequate in many regions. This deficiency not only contributes to environmental concerns but also hinders brands from fully capitalizing on their sustainability claims and meeting consumer expectations for end-of-life solutions.

Another critical challenge is maintaining cost-effectiveness while simultaneously innovating for sustainability and enhanced functionality. Developing new, high-performance sustainable materials often involves higher initial costs and longer development cycles, which can strain profit margins, especially for smaller players. Furthermore, fierce competition within the packaging industry and from pet food brands seeking to differentiate themselves requires continuous investment in R&D and marketing, adding to operational complexities. Navigating the evolving regulatory landscape, which varies significantly across different countries and regions regarding packaging materials, labeling, and waste disposal, also poses a substantial hurdle for global players. Companies must adapt to diverse compliance requirements while striving for standardized solutions. Lastly, supply chain disruptions, whether due to geopolitical events, natural disasters, or pandemics, can significantly impact raw material availability and logistics, leading to production delays and increased costs, underscoring the need for resilient and diversified supply networks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Developing Scalable Recycling Infrastructure for Flexible Packaging | -0.9% | Global | Long-term (2025-2033) |

| Balancing Sustainability with Cost-Effectiveness | -0.8% | Global | Long-term (2025-2033) |

| Navigating Complex & Evolving Regulatory Landscape | -0.7% | Europe, North America | Long-term (2025-2033) |

| Supply Chain Vulnerabilities & Disruptions | -0.6% | Global | Short-term to Mid-term (2025-2027) |

| Maintaining Product Safety and Shelf-Life with New Materials | -0.5% | Global | Mid-term (2025-2029) |

Pet Food Flexible Packaging Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Pet Food Flexible Packaging Market, covering historical trends, current market dynamics, and future projections. It delves into the market size, growth drivers, restraints, opportunities, and challenges influencing the industry's trajectory. The scope extends to a detailed segmentation analysis by material, packaging type, application, and pet type, alongside a robust regional assessment to offer a holistic market view.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.5 billion |

| Market Forecast in 2033 | USD 17.5 billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor Plc, Berry Global Group, Inc., Mondi Group, Sealed Air Corporation, Huhtamaki Oyj, ProAmpac, Coveris, Sonoco Products Company, Winpak Ltd., TC Transcontinental Inc., Flair Flexible Packaging, Constantia Flexibles, Smurfit Kappa, Novolex, Pactiv Evergreen Inc., Printpack Inc., CCL Industries Inc., Uflex Ltd., Scholle IPN Corporation, RPC Group Plc |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The pet food flexible packaging market is comprehensively segmented to provide granular insights into its diverse components and their respective growth trajectories. These segmentations are critical for understanding specific market dynamics, consumer preferences, and technological advancements across different material types, packaging formats, product applications, and pet categories. Each segment exhibits unique characteristics and growth drivers, reflecting the varied demands within the global pet food industry.

Analyzing these segments allows stakeholders to identify niche opportunities, understand competitive landscapes, and tailor their strategies for maximum impact. The market's complexity necessitates a multi-faceted approach, wherein material innovations, design trends, and application-specific requirements collectively shape the demand for flexible packaging solutions. The detailed breakdown provides a roadmap for companies looking to specialize or diversify their offerings in this evolving market.

- By Material: Includes Plastics (Polyethylene, Polypropylene, PET, EVOH, Nylon), Paper, Bioplastics (PLA, PHA), Aluminum, and Other Materials.

- By Packaging Type: Comprises Pouches (Stand-up Pouches, Flat Pouches, Gusseted Pouches), Bags (Form-Fill-Seal Bags, Wicketed Bags), Wraps, Films, Lids, and Other Packaging Types.

- By Application: Covers packaging solutions for Dry Food, Wet Food, Treats & Chews, and Other Pet Food Products.

- By Pet Type: Categorizes packaging demand based on pets such as Dogs, Cats, Fish, Birds, and Other Pets.

Regional Highlights

- North America: This region holds a significant share in the pet food flexible packaging market, driven by high rates of pet ownership, the humanization of pets, and a strong demand for premium and convenient pet food products. The U.S. and Canada lead in adopting innovative and sustainable packaging solutions, with a growing focus on e-commerce compatible designs.

- Europe: Europe is a key market, characterized by stringent environmental regulations and a strong consumer preference for sustainable and recyclable packaging. Countries like Germany, the UK, and France are at the forefront of adopting eco-friendly materials and advanced printing technologies in pet food packaging.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, APAC's market expansion is fueled by increasing disposable incomes, rising pet ownership in countries like China, India, and Japan, and the rapid urbanization trends. The region presents immense opportunities for both established and emerging players to cater to a burgeoning middle class seeking convenient and high-quality pet food packaging.

- Latin America: This region shows steady growth, driven by an expanding pet population and a gradual shift towards processed pet food. Brazil and Mexico are leading the adoption of flexible packaging solutions, though economic stability and infrastructure development remain key factors influencing market penetration.

- Middle East and Africa (MEA): While currently a smaller market, the MEA region is expected to witness moderate growth, supported by increasing urbanization and a rise in pet ownership in countries like UAE and South Africa. The market is still in its nascent stages, offering potential for future expansion as awareness and disposable incomes grow.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pet Food Flexible Packaging Market.- Amcor Plc

- Berry Global Group, Inc.

- Mondi Group

- Sealed Air Corporation

- Huhtamaki Oyj

- ProAmpac

- Coveris

- Sonoco Products Company

- Winpak Ltd.

- TC Transcontinental Inc.

- Flair Flexible Packaging

- Constantia Flexibles

- Smurfit Kappa

- Novolex

- Pactiv Evergreen Inc.

- Printpack Inc.

- CCL Industries Inc.

- Uflex Ltd.

- Scholle IPN Corporation

- RPC Group Plc

Frequently Asked Questions

Analyze common user questions about the Pet Food Flexible Packaging market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is pet food flexible packaging?

Pet food flexible packaging refers to packaging materials that are non-rigid, such as pouches, bags, and films, commonly used for pet food products. These solutions are lightweight, adaptable, and offer benefits like extended shelf life, convenience, and vibrant branding opportunities for both dry and wet pet food.

Why is sustainable packaging important for pet food?

Sustainable packaging for pet food is crucial due to increasing environmental awareness among consumers and stricter regulations on plastic waste. It helps reduce ecological footprint, appeals to environmentally conscious pet owners, and supports circular economy initiatives through recyclable, compostable, or bio-based materials.

How does e-commerce impact pet food flexible packaging?

The rise of e-commerce has significantly influenced pet food flexible packaging by driving demand for durable, lightweight, and compact designs that can withstand shipping rigors. Packaging must be optimized for efficient logistics, minimized damage, and reduced shipping costs, often favoring robust yet flexible formats.

What are the key materials used in pet food flexible packaging?

Key materials include various plastics like polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET), often used in multi-layer structures for barrier properties. Paper, aluminum foils, and emerging bioplastics (e.g., PLA, PHA) are also increasingly utilized, particularly for sustainable solutions.

What are the future trends in pet food flexible packaging?

Future trends involve continued innovation in sustainable materials, the integration of smart packaging technologies for enhanced traceability and consumer engagement, and greater customization through digital printing. There will also be a growing emphasis on high-barrier films to extend shelf life and convenience features like easy-open and resealable closures.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted