Frac Sand Market

Frac Sand Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706286 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

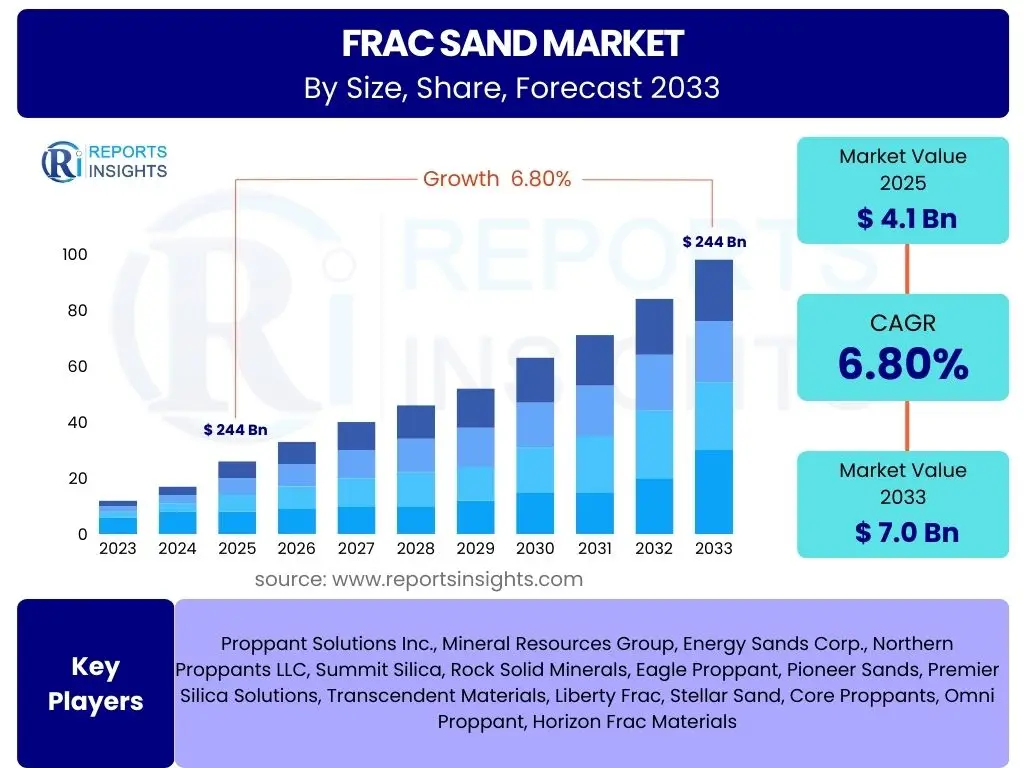

Frac Sand Market Size

According to Reports Insights Consulting Pvt Ltd, The Frac Sand Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.1 Billion in 2025 and is projected to reach USD 7.0 Billion by the end of the forecast period in 2033.

Key Frac Sand Market Trends & Insights

The Frac Sand market is experiencing significant evolution driven by shifts in the global energy landscape and technological advancements in drilling and completion techniques. A primary trend observed is the increasing proppant intensity per well, as operators in unconventional plays opt for longer lateral sections and higher sand volumes to maximize hydrocarbon recovery. This strategy necessitates a consistent and high-quality supply of frac sand, influencing procurement and logistics strategies across the industry. Concurrently, the industry is witnessing a notable shift towards in-basin sand, driven by efforts to reduce transportation costs and environmental footprints.

Another prominent insight is the growing emphasis on environmental, social, and governance (ESG) factors. Energy companies are increasingly scrutinizing their supply chains for sustainability, leading to demand for frac sand suppliers who can demonstrate responsible mining practices, efficient water management, and reduced carbon emissions. This trend also encourages innovation in proppant technology, including the development of lighter, more durable, or specially coated proppants that can improve well performance while potentially reducing the overall volume required. Furthermore, the integration of data analytics and digital tools is enhancing supply chain efficiency, from predicting demand to optimizing transportation routes, ensuring timely delivery and cost-effectiveness.

- Increased proppant intensity per well in unconventional plays.

- Growing preference for in-basin frac sand to optimize logistics and reduce costs.

- Rising focus on ESG compliance and sustainable sourcing practices.

- Development of advanced proppant technologies for enhanced well performance.

- Adoption of digital tools and analytics for supply chain optimization.

- Consolidation among sand producers and service companies.

- Volatility in oil and gas prices influencing demand fluctuations.

- Expansion of international unconventional drilling activities.

AI Impact Analysis on Frac Sand

The integration of Artificial Intelligence (AI) within the frac sand sector is primarily viewed through the lens of operational efficiency, cost reduction, and optimized resource utilization. User inquiries frequently center on how AI can streamline the complex logistics of frac sand supply, from predicting demand fluctuations to optimizing transport routes and inventory management. AI's predictive capabilities are particularly valuable in anticipating well completion schedules and proppant requirements, thereby minimizing overstocking or shortages, which are critical for cost control in a volatile market.

Beyond logistics, AI is expected to play a significant role in enhancing the quality control of frac sand, enabling real-time analysis of particle size distribution, sphericity, and crush strength to ensure optimal proppant performance downhole. Furthermore, AI-driven analytics can optimize the blend of frac sand during hydraulic fracturing operations, adapting to geological conditions to maximize hydrocarbon flow and recovery. This data-driven approach allows for more precise and effective well completions, reducing waste and improving overall economic viability. The long-term expectation is that AI will foster a more agile, responsive, and cost-efficient frac sand supply chain, making operations more resilient to market dynamics.

- Predictive analytics for optimizing frac sand demand forecasting and inventory management.

- AI-driven optimization of transportation routes and logistics, reducing delivery times and costs.

- Enhanced quality control through real-time AI analysis of sand properties (e.g., grain size, sphericity).

- Automated well completion design, recommending optimal proppant types and volumes based on geological data.

- Improved supply chain visibility and risk management through AI-powered monitoring.

- Potential for reduced environmental footprint by optimizing resource allocation and transport.

Key Takeaways Frac Sand Market Size & Forecast

The Frac Sand market forecast indicates a period of steady growth, primarily underpinned by the continued global reliance on unconventional oil and gas resources. A key takeaway is that the market's trajectory is intimately linked with the investment cycles in exploration and production (E&P) activities, particularly in North America. While volatility in crude oil prices remains a factor, the underlying trend towards optimizing well performance through higher proppant intensity per well is expected to sustain demand. This signifies that even in a fluctuating price environment, operators prioritize efficiency and recovery, driving the need for consistent, high-quality frac sand supplies.

Another crucial insight is the accelerating trend towards regionalization in frac sand sourcing, with in-basin mining operations gaining prominence. This strategic shift is not merely a cost-saving measure but also a response to increasing environmental considerations and the desire for more resilient supply chains. Furthermore, technological advancements, both in drilling techniques and in proppant design, are continually shaping the market, creating opportunities for specialized products and services. The forecast reflects an industry adapting to both economic pressures and evolving environmental standards, positioning itself for sustainable growth by enhancing logistical efficiencies and product innovation.

- Sustained demand driven by unconventional oil and gas production, particularly in North America.

- Increasing proppant intensity per well as operators seek to maximize hydrocarbon recovery.

- Shift towards in-basin sand production reducing transportation costs and environmental impact.

- Market growth influenced by E&P investment cycles and global energy demand.

- Technological advancements in drilling and proppant quality contributing to market evolution.

- Emphasis on supply chain efficiency and optimization to mitigate market volatility.

Frac Sand Market Drivers Analysis

The primary driver for the Frac Sand market is the sustained growth in unconventional oil and gas exploration and production activities, particularly hydraulic fracturing. The effectiveness of hydraulic fracturing in unlocking vast reserves from shale formations has led to its widespread adoption, especially in North America. As operators continue to refine drilling techniques, such as extending lateral lengths and increasing the number of stages per well, the demand for frac sand as a proppant intensifies significantly. This increase in proppant intensity per well, where more sand is pumped into each wellbore, is a direct contributor to market expansion, ensuring sustained consumption even with fewer new wells drilled in some periods.

Furthermore, advancements in drilling and completion technologies, including pad drilling and multi-well completions, have made extraction more efficient and economically viable, encouraging further investment in unconventional plays. The global energy demand, especially for natural gas as a cleaner transitional fuel, also bolsters the market for frac sand. Regions outside North America, such as Argentina, China, and parts of the Middle East, are increasingly exploring their shale potential, opening new geographical markets for frac sand suppliers. These factors collectively create a robust demand environment for frac sand, pushing market growth through increased consumption rates per well and the opening of new operational fronts.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Unconventional Oil & Gas Production | +1.5% | North America, Argentina, China | Medium-term to Long-term |

| Increasing Proppant Intensity Per Well | +1.2% | Global (especially US Basins) | Short-term to Medium-term |

| Technological Advancements in Drilling & Completion | +0.8% | Global | Medium-term |

| Rising Global Energy Demand | +0.7% | Global | Long-term |

| Development of New Shale Plays Internationally | +0.5% | Argentina, China, Middle East | Long-term |

Frac Sand Market Restraints Analysis

The Frac Sand market faces significant restraints primarily stemming from the inherent volatility of crude oil and natural gas prices. Fluctuations in energy commodity prices directly impact exploration and production (E&P) spending by oil and gas companies, leading to reduced drilling and completion activity. When prices are low, operators often scale back operations, defer projects, or reduce proppant volumes to cut costs, directly diminishing demand for frac sand. This unpredictability makes long-term investment planning challenging for sand producers and creates an environment of demand uncertainty.

Environmental regulations and public opposition to hydraulic fracturing present another substantial restraint. Growing concerns over water usage, potential groundwater contamination, and seismic activity associated with fracking can lead to stricter operational permits, moratoriums, or outright bans in certain regions. These regulatory hurdles increase operational costs for energy companies and can limit the geographical scope of hydraulic fracturing, thereby curtailing the market for frac sand. Furthermore, the high transportation costs associated with moving frac sand from mines to well sites, especially for distant operations, can erode profit margins for both suppliers and operators, sometimes making local, lower-quality sand more economically attractive despite performance trade-offs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Crude Oil & Natural Gas Prices | -1.5% | Global | Short-term to Medium-term |

| Stringent Environmental Regulations & Public Opposition | -1.0% | North America, Europe | Medium-term |

| High Transportation & Logistics Costs | -0.8% | Global (especially landlocked regions) | Short-term to Long-term |

| Competition from Alternative Energy Sources | -0.5% | Global | Long-term |

| Oversupply of Sand & Price Compression | -0.7% | North America | Short-term |

Frac Sand Market Opportunities Analysis

The Frac Sand market is poised for significant opportunities driven by the continuous innovation in drilling and completion techniques. The pursuit of greater efficiency and higher ultimate recovery from unconventional reservoirs leads operators to experiment with optimized proppant designs, including specialized coatings or lightweight alternatives. These advancements create niches for manufacturers developing premium or tailored frac sand products that offer enhanced conductivity, reduced embedment, or improved transport efficiency, allowing them to command better pricing and differentiate from commodity sand. Such innovations not only meet evolving operational demands but also address environmental concerns by potentially reducing the overall sand volume required.

Another compelling opportunity lies in the expansion of unconventional drilling activities into new international basins. While North America remains the dominant market, countries in Latin America (e.g., Argentina's Vaca Muerta shale), Asia Pacific (e.g., China's shale gas), and the Middle East are actively exploring and developing their shale resources. These emerging markets represent untapped demand for frac sand, offering growth avenues for suppliers capable of navigating diverse regulatory environments and logistical challenges. Furthermore, the growing emphasis on localized or in-basin proppant sourcing presents an opportunity for companies to invest in regional mining and processing facilities, thereby reducing transportation costs, improving supply chain resilience, and catering more effectively to specific regional demands.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Proppant Technologies | +1.0% | Global | Medium-term to Long-term |

| Expansion into New International Unconventional Plays | +0.9% | Latin America, Asia Pacific, Middle East | Long-term |

| Increased Focus on In-basin & Regional Sourcing | +0.8% | North America (Permian, Appalachia) | Short-term to Medium-term |

| Optimization of Logistics & Supply Chain Efficiency | +0.6% | Global | Short-term |

| Utilization in Enhanced Oil Recovery (EOR) Techniques | +0.4% | Global | Long-term |

Frac Sand Market Challenges Impact Analysis

The Frac Sand market faces significant challenges, primarily from the cyclical nature and volatility of the oil and gas industry. Sudden and sharp declines in crude oil prices can lead to immediate reductions in drilling activity and proppant consumption, causing an oversupply of sand and intense price competition among suppliers. This volatility makes it difficult for companies to maintain stable profit margins, plan for future investments, and retain skilled labor. Furthermore, the capital-intensive nature of mining and processing operations, coupled with the specialized logistics required, means that market downturns can quickly strain financial health and lead to consolidation or exits for less resilient players.

Another key challenge involves the increasing scrutiny and associated costs related to environmental compliance and social responsibility. Frac sand mining can have environmental impacts related to land use, water consumption, and dust emissions, leading to stricter regulations and higher operational costs for permits and mitigation efforts. Social license to operate is also becoming more challenging, with communities expressing concerns about noise, heavy truck traffic, and perceived environmental risks. These pressures necessitate significant investments in sustainable practices and community engagement, adding to the overall cost structure and potentially delaying or preventing new projects. Supply chain disruptions, such as infrastructure limitations for rail or trucking, also pose a recurring challenge, impacting timely delivery and adding to logistical complexities and costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Market Volatility & Price Fluctuations | -1.2% | Global | Short-term |

| Environmental Compliance & Regulatory Hurdles | -0.9% | North America, Europe | Medium-term |

| High Logistics & Transportation Costs | -0.7% | Global | Short-term to Medium-term |

| Oversupply and Intense Competition | -0.6% | North America | Short-term |

| Infrastructure Limitations (Rail/Trucking) | -0.5% | Specific US Basins | Medium-term |

Frac Sand Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Frac Sand market, covering historical data from 2019 to 2023, with detailed forecasts extending from 2025 to 2033. It elucidates market size estimations, growth drivers, restraints, opportunities, and challenges influencing the industry's trajectory. The report segments the market by type, application, and region, offering granular insights into demand and supply dynamics across key geographic areas and end-use sectors. Furthermore, it profiles key industry players, providing an understanding of the competitive landscape, recent developments, and strategic initiatives shaping the market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 7.0 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Proppant Solutions Inc., Mineral Resources Group, Energy Sands Corp., Northern Proppants LLC, Summit Silica, Rock Solid Minerals, Eagle Proppant, Pioneer Sands, Premier Silica Solutions, Transcendent Materials, Liberty Frac, Stellar Sand, Core Proppants, Omni Proppant, Horizon Frac Materials |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Frac Sand market is comprehensively segmented to provide a detailed understanding of its various facets, enabling stakeholders to identify specific growth drivers and market dynamics. The primary segmentation by type includes Northern White sand, known for its high-purity silica and excellent crush strength, often sourced from Wisconsin and Minnesota. Brown (Permian) sand, predominantly found in Texas, offers cost advantages due to its proximity to major drilling basins despite slightly lower quality specifications. Ceramic proppants, while more expensive, provide superior crush resistance and conductivity for challenging well conditions, while resin-coated proppants are designed for enhanced conductivity and flowback control. Other types include specialized or locally sourced alternatives.

Application-wise, the Oil and Gas sector is the overwhelming consumer of frac sand, utilizing it extensively in hydraulic fracturing to prop open fractures in shale and tight rock formations. Beyond this, a smaller portion of frac sand is employed in construction for high-strength concrete and industrial applications, such as filtration and glass manufacturing, though these represent minor segments compared to the energy sector. Further segmentation by mesh size (e.g., 20/40, 30/50, 40/70, 70/140) categorizes sand based on particle size, which is critical for optimizing well performance across different geological conditions and completion strategies. Each mesh size serves specific functions, with coarser sands offering higher conductivity and finer sands allowing for deeper penetration into complex fracture networks.

- By Type: Northern White, Brown (Permian), Ceramic, Resin-Coated, Others

- By Application: Oil and Gas, Construction, Industrial, Others

- By Mesh Size: 20/40, 30/50, 40/70, 70/140, Others

Regional Highlights

- North America: Dominates the global Frac Sand market due to extensive unconventional oil and gas resources, particularly in the United States (Permian Basin, Marcellus, Eagle Ford) and Canada (Western Canadian Sedimentary Basin). The region benefits from established infrastructure, advanced drilling technologies, and a mature hydraulic fracturing industry. The shift towards in-basin sand production is a notable trend, optimizing logistics and reducing costs for operators.

- Europe: Exhibits limited but niche demand for frac sand, primarily in countries with nascent shale gas exploration or mature conventional fields requiring enhanced recovery techniques. Environmental regulations and public opposition to fracking pose significant challenges, limiting widespread adoption and market growth.

- Asia Pacific (APAC): Emerging as a potential growth market, driven by China's considerable shale gas reserves and increasing interest in unconventional resource development across other countries like Australia and India. While still in early stages compared to North America, government initiatives to boost domestic energy production could stimulate future demand.

- Latin America: Argentina stands out as a key growth region due to the Vaca Muerta shale play, which holds substantial oil and gas potential. Other countries like Brazil are also exploring unconventional resources, contributing to growing regional demand for frac sand and related services.

- Middle East and Africa (MEA): Shows increasing potential for unconventional resource development, particularly in countries like Saudi Arabia and the UAE, which are exploring their shale gas and tight oil reserves. While still nascent, long-term strategic energy diversification efforts could drive future frac sand demand in the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Frac Sand Market.- Proppant Solutions Inc.

- Mineral Resources Group

- Energy Sands Corp.

- Northern Proppants LLC

- Summit Silica

- Rock Solid Minerals

- Eagle Proppant

- Pioneer Sands

- Premier Silica Solutions

- Transcendent Materials

- Liberty Frac

- Stellar Sand

- Core Proppants

- Omni Proppant

- Horizon Frac Materials

Frequently Asked Questions

What is Frac Sand used for?

Frac sand, also known as proppant, is primarily used in hydraulic fracturing (fracking) operations. It is pumped into oil and gas wells to prop open fractures created in the rock formations, allowing hydrocarbons (oil and natural gas) to flow freely to the surface.

What are the main types of Frac Sand?

The main types of frac sand include Northern White (high-purity silica), Brown/Permian (regionally sourced, lower cost), Ceramic (man-made, high strength), and Resin-Coated (enhanced conductivity and flowback control).

How large is the global Frac Sand market?

The global Frac Sand market is estimated at USD 4.1 Billion in 2025 and is projected to reach USD 7.0 Billion by 2033, growing at a CAGR of 6.8%.

What are the key drivers of Frac Sand market growth?

Key drivers include the global expansion of unconventional oil and gas production, increasing proppant intensity per well, and continuous technological advancements in drilling and completion techniques.

What challenges does the Frac Sand market face?

The market faces challenges such as volatility in crude oil prices, stringent environmental regulations, high transportation costs, and occasional oversupply leading to intense price competition.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted