Glass grade Silica Sand Market

Glass grade Silica Sand Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701624 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

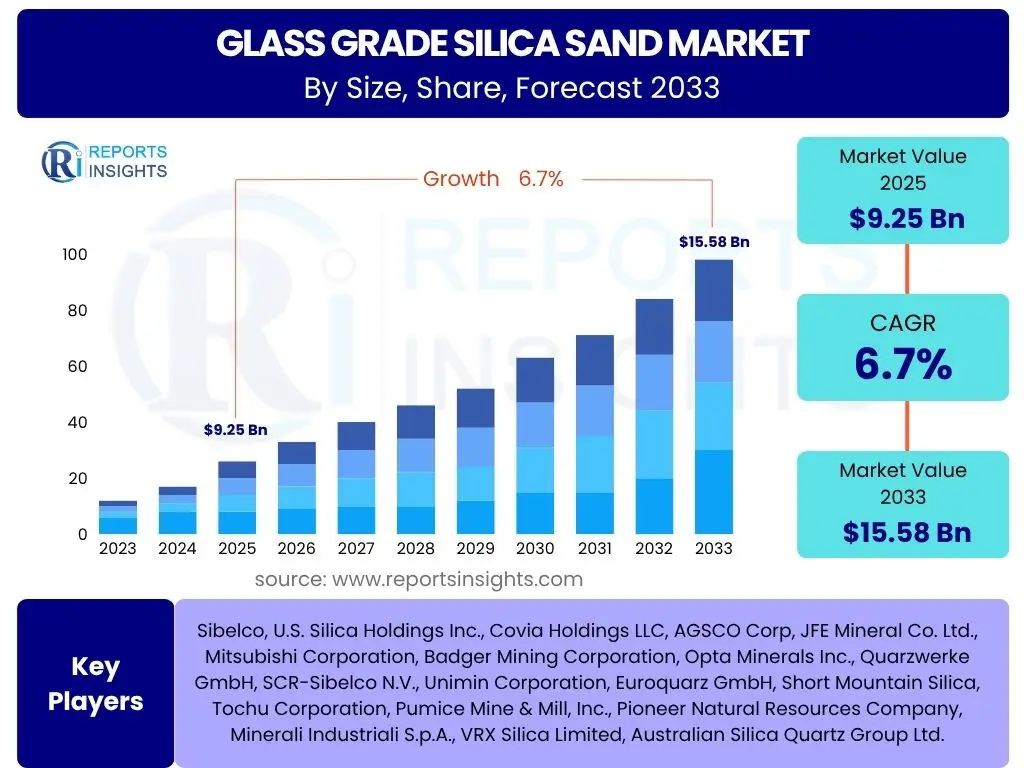

Glass grade Silica Sand Market Size

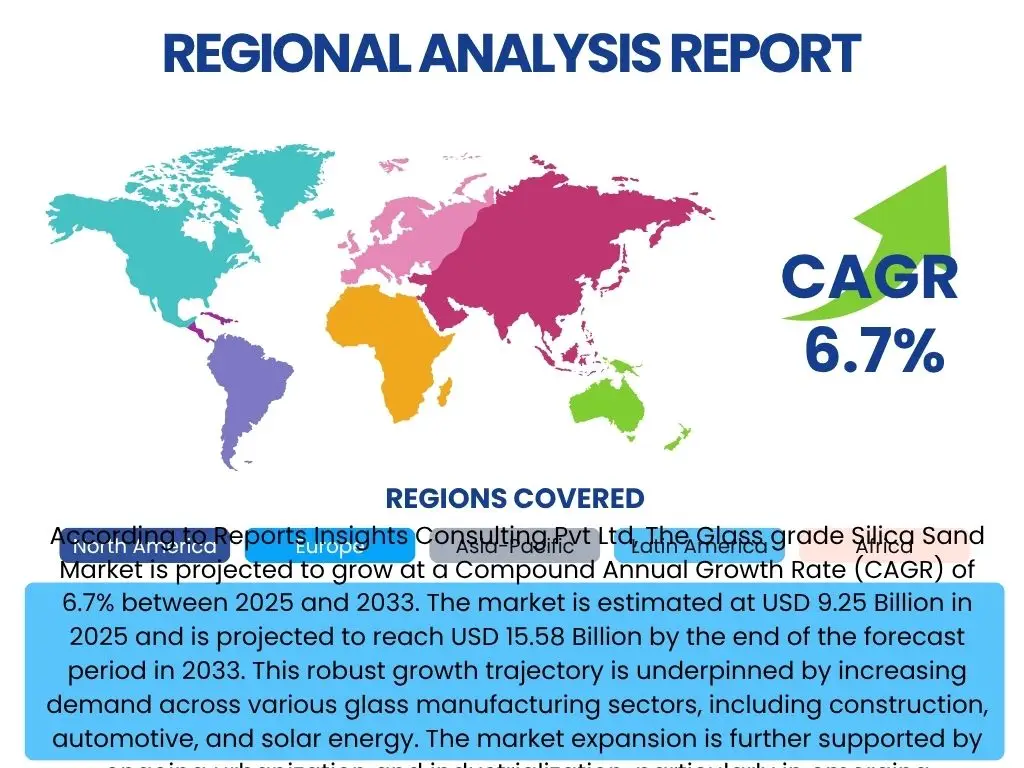

According to Reports Insights Consulting Pvt Ltd, The Glass grade Silica Sand Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 9.25 Billion in 2025 and is projected to reach USD 15.58 Billion by the end of the forecast period in 2033. This robust growth trajectory is underpinned by increasing demand across various glass manufacturing sectors, including construction, automotive, and solar energy. The market expansion is further supported by ongoing urbanization and industrialization, particularly in emerging economies, which continue to drive the need for high-quality glass products.

The valuation reflects the critical role of silica sand as a primary raw material for glass production, where its purity directly influences the quality and performance of the final glass product. The market's consistent upward trend is indicative of sustained investments in manufacturing capacities and technological advancements aimed at optimizing glass properties and production efficiency. As industries pivot towards sustainable and high-performance materials, the demand for specialized, high-purity glass grade silica sand is expected to intensify, contributing significantly to the market's projected value.

Key Glass grade Silica Sand Market Trends & Insights

Common user inquiries about the Glass grade Silica Sand market frequently revolve around emerging applications, sustainability initiatives, and technological advancements that shape the industry's future. The market is witnessing a significant shift towards higher purity silica sand grades, driven by the escalating demand for advanced glass products in electronics, solar panels, and specialized architectural applications. This focus on purity is paralleled by increasing industry attention to sustainable mining practices and supply chain transparency, as environmental regulations become more stringent and corporate social responsibility gains prominence. Additionally, the integration of automation and data analytics in silica sand processing is enhancing efficiency and consistency, further refining the quality of the raw material.

Another prominent trend is the geographical diversification of sourcing and manufacturing, with a noticeable increase in exploration for new deposits and the establishment of processing facilities in proximity to growing end-use markets. This strategic realignment aims to mitigate logistics costs and ensure a stable supply amidst global trade complexities. Furthermore, the market is influenced by the circular economy concept, with research and development efforts exploring the viability of recycled glass (cullet) as a partial substitute for virgin silica sand, although high-purity glass applications largely continue to rely on primary sources.

- Growing demand for high-purity silica sand for solar glass and electronics displays.

- Increasing adoption of sustainable mining practices and environmental compliance.

- Technological advancements in silica sand processing to enhance quality and reduce impurities.

- Regionalization of supply chains to reduce logistics costs and ensure security of supply.

- Focus on specialized silica sand grades for high-performance glass applications.

AI Impact Analysis on Glass grade Silica Sand

User inquiries concerning AI's influence on the Glass grade Silica Sand domain often explore how artificial intelligence can optimize mining operations, improve raw material quality control, and enhance supply chain efficiencies. AI's immediate impact is evident in the precision and productivity of silica sand extraction and processing. Through predictive analytics and machine learning algorithms, AI can optimize excavation routes, predict equipment maintenance needs, and fine-tune processing parameters, leading to reduced energy consumption, minimized waste, and improved yield of desired sand grades. This level of operational intelligence allows producers to maintain consistent quality, a critical factor for glass manufacturers.

Furthermore, AI-driven solutions are transforming quality assurance for glass grade silica sand. Computer vision systems combined with AI can conduct rapid and highly accurate analyses of sand composition, particle size distribution, and impurity levels, far exceeding manual capabilities. This ensures that the silica sand meets the stringent purity requirements for various glass applications, from float glass to optical fibers. In the supply chain, AI algorithms can optimize logistics, forecast demand more accurately, and manage inventory levels efficiently, thereby reducing transportation costs and ensuring timely delivery to glass manufacturing plants worldwide.

- AI-powered predictive maintenance for mining equipment, reducing downtime and operational costs.

- Enhanced quality control and impurity detection using AI and computer vision systems.

- Optimization of processing parameters and energy consumption in sand washing and sorting plants.

- AI-driven demand forecasting and supply chain optimization for efficient logistics and inventory management.

- Development of smart mining operations for resource extraction and environmental impact assessment.

Key Takeaways Glass grade Silica Sand Market Size & Forecast

Common user questions regarding key takeaways from the Glass grade Silica Sand market size and forecast typically focus on the primary growth drivers, the most promising application segments, and the overall trajectory of market development. The market is poised for significant expansion, largely propelled by the sustained growth of the global construction and automotive industries, which are major consumers of flat glass. Concurrently, the burgeoning solar energy sector, with its demand for specialized solar glass, represents a high-growth niche within the market, emphasizing the need for ultra-high purity silica sand.

Another crucial takeaway is the increasing emphasis on technological innovation, not only in the extraction and processing of silica sand but also in the development of new glass compositions that demand specific sand characteristics. This drives investments in research and development to refine purification techniques and identify new high-quality deposits. Geographically, Asia Pacific continues to be the dominant region due to robust industrial growth and urbanization, while other regions are focusing on specialized applications and optimizing their existing capacities to meet evolving demands.

- The market exhibits robust growth, driven primarily by the construction, automotive, and solar energy sectors.

- Demand for high-purity and specialized silica sand grades is accelerating due to advanced glass applications.

- Technological advancements in processing and quality control are pivotal for market competitiveness.

- Asia Pacific remains the largest and fastest-growing region, fueled by industrial development.

- Sustainability and supply chain efficiency are increasingly critical factors influencing market dynamics.

Glass grade Silica Sand Market Drivers Analysis

The Glass grade Silica Sand market is significantly influenced by several key drivers that collectively contribute to its growth trajectory. A primary driver is the accelerating demand for flat glass, which finds extensive applications in construction for windows, facades, and interior design, as well as in the automotive industry for windshields and various vehicle components. The global urbanization trend and infrastructure development projects in emerging economies further amplify this demand. As cities expand and new commercial and residential structures are erected, the consumption of glass, and consequently glass grade silica sand, sees a proportionate increase.

Another significant driver is the rapid expansion of the solar energy sector. The production of solar panels requires high-purity glass, which in turn necessitates very pure silica sand. Governments worldwide are investing heavily in renewable energy sources, and the declining cost of solar technology has made it more accessible, leading to a surge in solar panel installations. This directly translates into heightened demand for specialized glass grade silica sand. Furthermore, technological advancements in glass manufacturing, such as the development of lightweight, stronger, and more energy-efficient glass, push the demand for specific, high-quality silica sand grades to meet stringent performance requirements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for flat glass in construction and automotive sectors | +2.1% | Global, particularly Asia Pacific, North America, Europe | Short to Long-term (2025-2033) |

| Expansion of the solar energy industry and increased solar panel production | +1.8% | China, India, USA, Europe | Medium to Long-term (2027-2033) |

| Urbanization and infrastructure development projects | +1.5% | Emerging economies (APAC, Latin America, MEA) | Medium to Long-term (2026-2033) |

| Technological advancements in specialty glass manufacturing (e.g., electronics, display) | +1.3% | Global, particularly East Asia, North America, Europe | Medium-term (2025-2030) |

Glass grade Silica Sand Market Restraints Analysis

Despite the positive growth outlook, the Glass grade Silica Sand market faces several restraints that could impede its expansion. Stringent environmental regulations and the complexities involved in obtaining mining permits pose a significant challenge. Governments globally are implementing stricter rules regarding land use, environmental impact assessments, and ecological restoration, making it harder and more expensive to establish new mining operations or expand existing ones. This regulatory burden can lead to delays in project approvals, increased operational costs, and sometimes, outright denial of permits, limiting the supply of raw materials.

Another notable restraint is the high cost and logistical challenges associated with transporting silica sand. Silica sand is a bulk commodity, and its transportation over long distances, especially from remote mining sites to glass manufacturing hubs, can be very expensive. Fuel price fluctuations, inadequate infrastructure, and trade barriers can further exacerbate these costs, impacting the profitability of producers and increasing the final price of glass products. Furthermore, the finite nature of high-purity silica sand deposits, coupled with concerns over resource depletion and the need for meticulous geological surveys, can limit the availability of optimal quality raw material, pushing prices up and potentially impacting market growth in specific regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent environmental regulations and complex mining permits | -1.2% | Global, particularly Europe, North America, Australia | Short to Long-term (2025-2033) |

| High logistics and transportation costs of bulk raw material | -0.9% | Global | Short to Medium-term (2025-2030) |

| Depletion of high-purity silica sand deposits and resource availability concerns | -0.7% | Region-specific (e.g., Southeast Asia, some parts of Europe) | Medium to Long-term (2027-2033) |

| Volatility in energy prices impacting production costs | -0.6% | Global | Short-term (2025-2027) |

Glass grade Silica Sand Market Opportunities Analysis

Opportunities in the Glass grade Silica Sand market are primarily driven by evolving industry needs and technological advancements. The burgeoning demand for advanced and high-performance glass in sectors such as electronics, automotive displays, and specialized architectural applications presents a significant opportunity. As consumer electronics like smartphones, tablets, and smart home devices become more prevalent, the need for high-quality, scratch-resistant, and aesthetically superior display glass escalates. Similarly, the automotive industry's shift towards electric vehicles and autonomous driving necessitates larger, more sophisticated displays and sensors, creating a niche for ultra-high purity silica sand.

The increasing focus on renewable energy, particularly solar power, offers another substantial growth avenue. The continued expansion of solar farms and rooftop installations globally fuels a consistent demand for solar glass, which requires specific properties derived from premium glass grade silica sand. Furthermore, opportunities exist in developing sustainable mining practices and circular economy initiatives, such as enhancing glass recycling technologies. While recycled cullet currently cannot fully replace virgin silica sand for all high-purity applications, advancements in processing recycled materials could create new supply streams and reduce environmental impact, appealing to environmentally conscious industries and consumers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in demand for high-performance glass in electronics and display technologies | +1.9% | East Asia, North America, Europe | Medium to Long-term (2026-2033) |

| Expansion of the renewable energy sector, especially solar glass applications | +1.7% | China, India, USA, European Union | Medium to Long-term (2027-2033) |

| Increasing R&D in new glass compositions requiring specialized silica sand | +1.1% | Global, particularly developed economies | Medium-term (2025-2030) |

| Development of sustainable mining practices and efficient resource utilization | +0.8% | Global | Short to Medium-term (2025-2030) |

Glass grade Silica Sand Market Challenges Impact Analysis

The Glass grade Silica Sand market confronts several challenges that demand strategic responses from industry players. One significant challenge is the ongoing risk of supply chain disruptions. Geopolitical tensions, natural disasters, and global health crises can severely impact mining operations, transportation networks, and overall logistics, leading to shortages and price volatility. Given that silica sand is a foundational raw material, any disruption can have ripple effects throughout the glass manufacturing industry, affecting production schedules and profitability.

Maintaining consistent quality and purity across large volumes of silica sand is another persistent challenge. Glass manufacturers have very specific requirements for chemical composition, particle size distribution, and impurity levels, as these factors directly influence the clarity, strength, and optical properties of the final glass product. Achieving and consistently maintaining these high standards requires sophisticated processing technologies, rigorous quality control measures, and significant investment in infrastructure. Furthermore, the competitive landscape and pricing pressures in the commodity market can challenge profitability, especially for producers of standard-grade silica sand, necessitating cost efficiency and value-added product differentiation to remain viable.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply chain disruptions and geopolitical instability | -1.0% | Global | Short-term (2025-2027) |

| Maintaining consistent high quality and purity standards | -0.8% | Global | Short to Medium-term (2025-2030) |

| Intense market competition and pricing pressures | -0.6% | Global | Short to Long-term (2025-2033) |

| High capital investment required for new mining and processing facilities | -0.5% | Global | Long-term (2028-2033) |

Glass grade Silica Sand Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Glass grade Silica Sand Market, covering historical data, current trends, and future projections. It delves into the market dynamics, including drivers, restraints, opportunities, and challenges, offering a holistic view for stakeholders. The report segments the market by type, application, and regional outlook, providing granular insights into demand patterns and growth potential across various segments. It also profiles key players, offering competitive intelligence and strategic recommendations for market participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.25 Billion |

| Market Forecast in 2033 | USD 15.58 Billion |

| Growth Rate | 6.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sibelco, U.S. Silica Holdings Inc., Covia Holdings LLC, AGSCO Corp, JFE Mineral Co. Ltd., Mitsubishi Corporation, Badger Mining Corporation, Opta Minerals Inc., Quarzwerke GmbH, SCR-Sibelco N.V., Unimin Corporation, Euroquarz GmbH, Short Mountain Silica, Tochu Corporation, Pumice Mine & Mill, Inc., Pioneer Natural Resources Company, Minerali Industriali S.p.A., VRX Silica Limited, Australian Silica Quartz Group Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Glass grade Silica Sand market is meticulously segmented to provide a detailed understanding of its diverse components and their respective growth dynamics. These segmentations allow for a granular analysis of market trends, consumer preferences, and technological shifts across different product types, application areas, and end-use industries. Understanding these segments is crucial for stakeholders to identify lucrative opportunities, tailor their strategies, and allocate resources effectively within the evolving market landscape.

The segmentation by type reflects the varying purity levels of silica sand, which directly correlates with its suitability for specific glass products, with high-purity grades commanding premium prices for advanced applications. Application-based segmentation highlights the dominant consuming sectors, such as flat glass for construction and automotive, and the rapidly growing specialty glass segment, including solar and display glass. Furthermore, the end-use industry segmentation provides a broader perspective on how different economic sectors drive the demand for glass, thereby influencing the silica sand market.

- By Type: High Purity Silica Sand, Medium Purity Silica Sand, Low Purity Silica Sand

- By Application: Flat Glass, Container Glass, Fiberglass, Specialty Glass (Solar Glass, Optical Glass, Laboratory Glass, Display Glass), Tableware, Other Glass Products

- By End-Use Industry: Construction, Automotive, Electronics, Solar Energy, Consumer Goods, Pharmaceuticals, Others

Regional Highlights

- Asia Pacific (APAC): Dominates the Glass grade Silica Sand market due to rapid industrialization, burgeoning construction activities, and expanding automotive and electronics manufacturing bases in countries like China, India, and Southeast Asian nations. The region also leads in solar panel production, driving demand for high-purity silica sand.

- North America: Characterized by a mature market with significant demand from the construction, automotive, and specialty glass sectors. Focus on technological advancements in glass manufacturing and increasing emphasis on sustainable sourcing and high-quality products.

- Europe: A key region with a strong focus on high-value specialty glass, including automotive glass, architectural glass, and pharmaceutical glass. Strict environmental regulations drive innovation in sustainable mining and processing techniques.

- Latin America: Exhibiting steady growth, primarily driven by infrastructure development and increasing demand for flat glass in construction and automotive industries. Brazil and Mexico are significant contributors to regional market expansion.

- Middle East and Africa (MEA): Emerging as a growth hub with increasing investments in construction and industrial development, particularly in the GCC countries. The region's vast natural resources offer potential for new silica sand mining projects, though logistical challenges remain.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Glass grade Silica Sand Market.- Sibelco

- U.S. Silica Holdings Inc.

- Covia Holdings LLC

- AGSCO Corp

- JFE Mineral Co. Ltd.

- Mitsubishi Corporation

- Badger Mining Corporation

- Opta Minerals Inc.

- Quarzwerke GmbH

- SCR-Sibelco N.V.

- Unimin Corporation

- Euroquarz GmbH

- Short Mountain Silica

- Tochu Corporation

- Pumice Mine & Mill, Inc.

- Pioneer Natural Resources Company

- Minerali Industriali S.p.A.

- VRX Silica Limited

- Australian Silica Quartz Group Ltd.

Frequently Asked Questions

What is Glass grade Silica Sand?

Glass grade silica sand is a high-purity form of silicon dioxide (SiO2), typically with over 98% silica content, and very low levels of impurities such as iron, alumina, and chromite. It is the primary raw material used in the manufacturing of all types of glass due to its unique chemical and physical properties that contribute to the clarity, strength, and optical characteristics of glass products.

What are the primary applications of Glass grade Silica Sand?

The primary applications include flat glass (used in windows, automotive windshields), container glass (bottles, jars), fiberglass, and various specialty glasses such as solar panels, optical glass, laboratory equipment, and display screens for electronics.

Which region dominates the Glass grade Silica Sand market?

Asia Pacific (APAC) currently dominates the Glass grade Silica Sand market. This is primarily due to rapid industrialization, extensive construction activities, and the booming electronics and solar energy sectors in countries like China, India, and other Southeast Asian nations, which are major consumers of glass products.

What key factors are driving the growth of the Glass grade Silica Sand market?

Key growth drivers include the increasing demand for flat glass in construction and automotive industries, the rapid expansion of the solar energy sector, ongoing urbanization and infrastructure development, and technological advancements in specialty glass manufacturing requiring higher purity silica sand.

What are the major challenges facing the Glass grade Silica Sand market?

Major challenges include stringent environmental regulations and complex mining permits, high logistics and transportation costs, depletion of high-purity silica sand deposits, and the need to maintain consistent quality and purity amidst intense market competition.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted