Fluid Catalytic Cracking Market

Fluid Catalytic Cracking Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703698 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

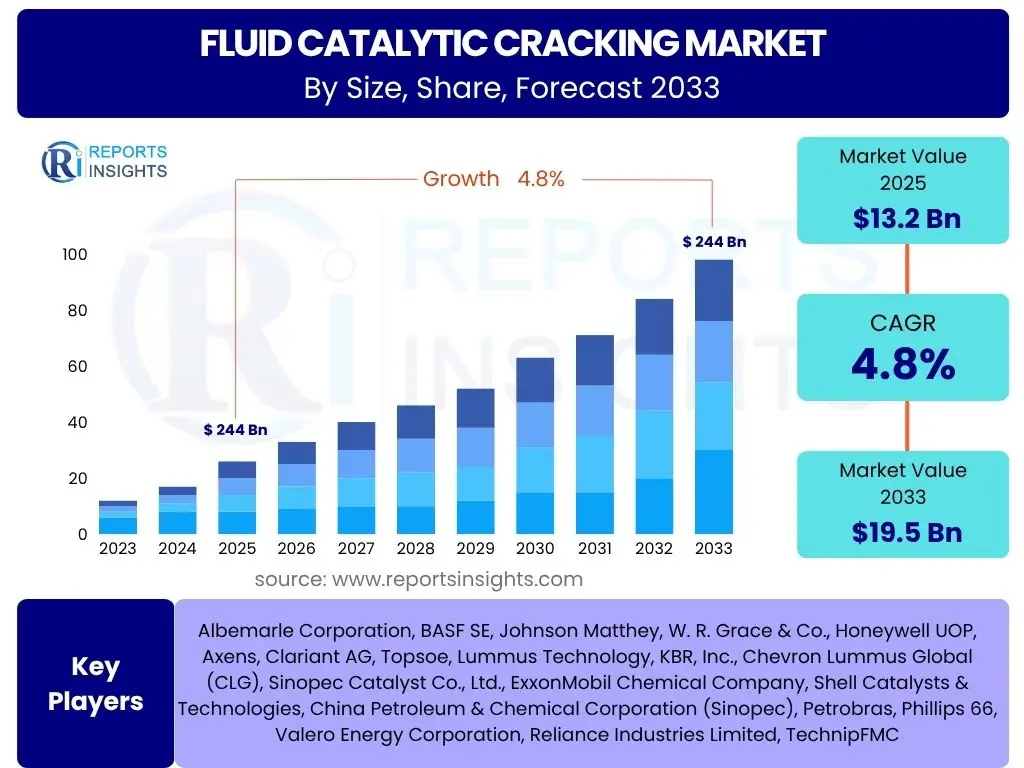

Fluid Catalytic Cracking Market Size

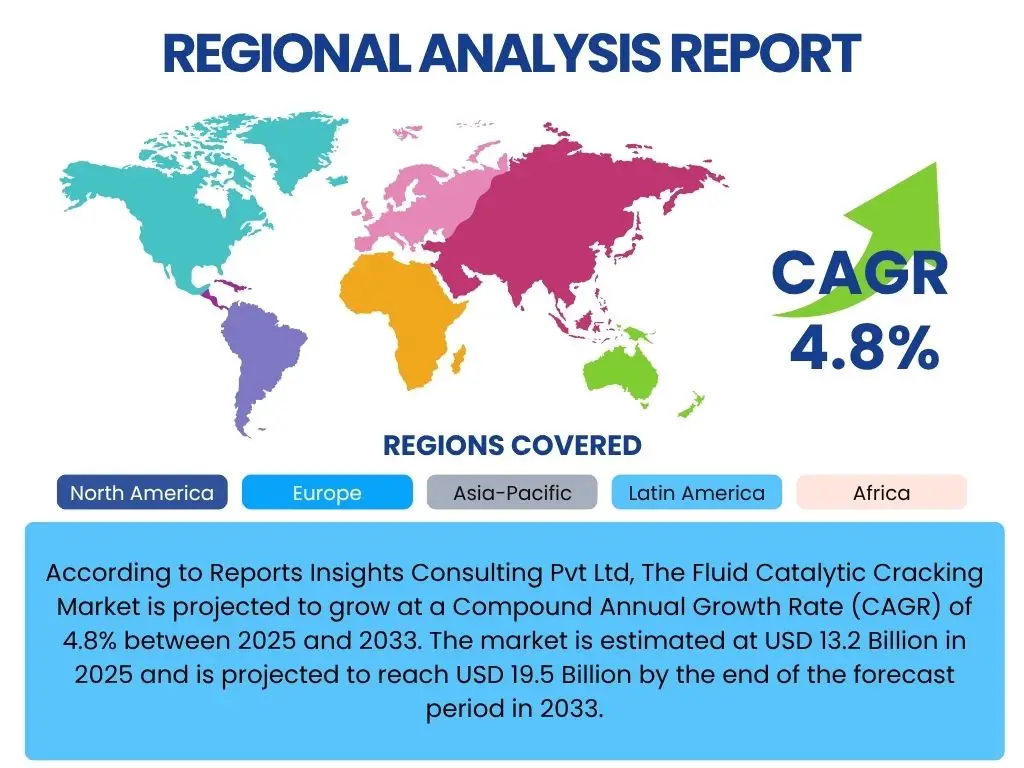

According to Reports Insights Consulting Pvt Ltd, The Fluid Catalytic Cracking Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 13.2 Billion in 2025 and is projected to reach USD 19.5 Billion by the end of the forecast period in 2033.

Key Fluid Catalytic Cracking Market Trends & Insights

The Fluid Catalytic Cracking (FCC) market is undergoing significant transformation driven by shifts in global energy demand, evolving fuel specifications, and a heightened focus on environmental sustainability. Refiners are increasingly seeking FCC solutions that offer greater flexibility in feedstock processing, enabling the conversion of heavier, more complex crude oil fractions into higher-value, lighter products like gasoline and propylene. This demand is further intensified by the global push for cleaner fuels and reduced emissions, necessitating advanced catalyst technologies and optimized operational strategies within FCC units.

A notable trend involves the development and adoption of high-performance FCC catalysts designed to improve yield distribution, enhance octane numbers, and minimize undesirable by-products. These catalysts are critical in meeting stringent regulatory requirements for sulfur content and other pollutants. Furthermore, digitalization and automation are becoming integral to FCC operations, with real-time data analytics and predictive maintenance solutions optimizing unit performance, reducing downtime, and improving overall efficiency. The emphasis on maximizing profitability from every barrel of crude processed continues to drive innovation in this sector.

Another emerging insight is the growing interest in co-processing renewable or bio-based feedstocks within existing FCC units. This trend aims to align traditional refining with circular economy principles and contribute to decarbonization efforts. While still in nascent stages, the integration of bio-feeds offers a pathway to produce sustainable aviation fuels and bio-gasoline, diversifying the product portfolio of refiners. These strategic shifts collectively underscore a market moving towards greater efficiency, sustainability, and adaptability in response to dynamic energy landscapes.

- Increasing demand for lighter distillates and petrochemical feedstocks.

- Advancements in high-performance and selective FCC catalyst technologies.

- Rising adoption of digital twins and AI-driven process optimization in refineries.

- Stringent environmental regulations driving demand for cleaner fuels.

- Growing interest in co-processing bio-feedstocks in FCC units.

AI Impact Analysis on Fluid Catalytic Cracking

The integration of Artificial Intelligence (AI) and machine learning (ML) within Fluid Catalytic Cracking operations represents a significant paradigm shift, offering transformative potential for process optimization, predictive maintenance, and enhanced operational efficiency. User inquiries frequently center on how AI can improve the notoriously complex and energy-intensive FCC process. AI algorithms, particularly those leveraging historical and real-time operational data, can identify subtle correlations and patterns that human operators or traditional control systems might miss. This capability allows for more precise control over reaction conditions, leading to optimized product yields, reduced energy consumption, and improved catalyst utilization. The proactive nature of AI-driven analytics minimizes the risk of costly shutdowns and maximizes throughput.

Moreover, AI's influence extends to the realm of catalyst development and feedstock characterization. By analyzing vast datasets related to catalyst composition, performance under varying conditions, and feedstock properties, AI can accelerate the discovery and optimization of new catalyst formulations. This capability is crucial for developing catalysts that can handle increasingly challenging feedstocks or produce specific high-value products more efficiently. Concerns often revolve around the quality and quantity of data required for effective AI implementation, the cybersecurity implications of connected systems, and the need for skilled personnel capable of deploying and managing AI solutions within a refinery environment.

Despite these challenges, the long-term expectations for AI in FCC units remain high, focusing on achieving higher levels of autonomy and predictive capability. AI can enable advanced process control, leading to real-time adjustments that optimize the entire cracking process, from feedstock injection to product separation. Furthermore, AI-powered systems can simulate various operational scenarios, helping operators make informed decisions and respond proactively to market demands or unforeseen events. The ultimate goal is to create more resilient, efficient, and profitable FCC operations through intelligent automation.

- Enhanced process optimization through real-time data analysis and predictive modeling.

- Improved yield and selectivity of desired products by precise operational adjustments.

- Predictive maintenance for critical FCC equipment, reducing unplanned downtime.

- Accelerated catalyst development and formulation through AI-driven material science.

- Better energy efficiency and reduced emissions through optimized unit control.

Key Takeaways Fluid Catalytic Cracking Market Size & Forecast

The Fluid Catalytic Cracking market is poised for robust growth, driven by an evolving energy landscape and the continuous demand for lighter transportation fuels and petrochemical feedstocks. A significant takeaway is the strategic importance of FCC units in the modern refining complex, acting as a crucial bottleneck for converting heavy crude fractions into high-value products. The forecast indicates a steady expansion, primarily propelled by increasing global energy consumption, particularly in developing economies, coupled with the need for refiners to enhance profitability through deeper conversion of crude oil. Innovations in catalyst technology and process optimization will be pivotal in shaping this growth trajectory.

Another critical insight highlights the dual pressure on refiners: maximizing economic output while adhering to increasingly stringent environmental regulations. This necessitates ongoing investment in advanced FCC technologies that not only improve yields and operational efficiency but also minimize sulfur content and other undesirable emissions. The market's resilience is further underscored by its adaptability to varying crude oil qualities, including sour and heavy crudes, which are becoming more prevalent. The ability of FCC units to process diverse feedstocks effectively ensures their continued relevance and necessity in the refining value chain.

The projected growth underscores substantial opportunities for stakeholders across the value chain, from catalyst manufacturers to technology licensors and engineering service providers. Collaboration and strategic partnerships focused on sustainable refining practices, digital transformation, and the integration of novel feedstocks will be key to unlocking future market potential. The market will continue to witness a blend of capacity expansions in growth regions and efficiency-driven upgrades in mature markets, all contributing to a dynamic and expanding sector within the global energy industry.

- Consistent market expansion driven by global fuel demand and petrochemical needs.

- Strategic imperative for refiners to upgrade heavy oil fractions into high-value products.

- Technological advancements in catalysts and digital solutions are key growth enablers.

- Emphasis on environmental compliance and sustainable operations as core drivers.

- Significant investment opportunities across the FCC technology and services ecosystem.

Fluid Catalytic Cracking Market Drivers Analysis

The Fluid Catalytic Cracking market is fundamentally driven by the persistent global demand for lighter petroleum products, particularly gasoline and propylene, which are essential for transportation and the petrochemical industry. As the world's population and industrial activities continue to expand, so does the need for these refined products, placing a continuous impetus on refineries to maximize their production efficiency. The economic viability of refineries is heavily reliant on their ability to convert low-value heavy crude oil fractions into higher-value distillates, a process where FCC units play a critical, irreplaceable role.

Moreover, the increasingly complex and heavier crude oil grades available in the market necessitate advanced conversion technologies. FCC units are uniquely equipped to handle these challenging feedstocks, making them indispensable for modern refining operations. Coupled with this is the global trend towards stricter environmental regulations concerning fuel quality, sulfur content, and emissions. These regulations compel refiners to upgrade their FCC processes and adopt advanced catalysts that can produce cleaner-burning fuels, thereby driving investment and innovation within the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Demand for Transportation Fuels | +1.5% | Asia Pacific, North America, Middle East | Short to Medium Term (2025-2029) |

| Increasing Complexity of Crude Oil Feedstocks | +1.2% | Global, particularly regions with heavy crude processing | Medium Term (2026-2030) |

| Stringent Environmental Regulations for Fuel Quality | +1.0% | Europe, North America, parts of Asia Pacific | Medium to Long Term (2027-2033) |

Fluid Catalytic Cracking Market Restraints Analysis

The Fluid Catalytic Cracking market faces several significant restraints that could temper its growth trajectory. One primary impediment is the substantial capital expenditure required for the construction of new FCC units or for major upgrades to existing ones. These projects involve complex engineering, specialized equipment, and extensive regulatory approvals, leading to high upfront costs and extended payback periods. This financial burden can deter smaller refiners or those operating with tighter margins from investing in capacity expansion or technological improvements.

Another crucial restraint is the volatility and uncertainty in crude oil prices, which directly impact refiners' profitability and, consequently, their investment decisions in FCC technologies. Significant fluctuations in feedstock costs can make long-term planning challenging and may lead to postponed or cancelled projects. Furthermore, increasing global emphasis on renewable energy sources and the long-term prospect of reduced fossil fuel consumption, particularly in the transportation sector due to the rise of electric vehicles, could pose a structural threat to demand for conventional fuels over the longer forecast period.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for New FCC Units | -0.8% | Global | Short to Medium Term (2025-2029) |

| Volatility in Crude Oil Prices and Profit Margins | -0.7% | Global | Short Term (2025-2027) |

| Long-term Shift Towards Electrification of Transport | -0.5% | Developed Economies (Europe, North America) | Long Term (2030-2033) |

Fluid Catalytic Cracking Market Opportunities Analysis

Despite existing challenges, the Fluid Catalytic Cracking market is rich with opportunities stemming from technological innovation and evolving industrial needs. One significant opportunity lies in the development and adoption of advanced catalyst formulations that offer enhanced selectivity towards high-value products like propylene and butylenes, which are critical building blocks for the petrochemical industry. As the demand for these petrochemicals continues to outpace that of traditional fuels in some regions, refiners are looking to optimize their FCC units for maximum petrochemical output, opening new revenue streams.

Another promising area involves the integration of alternative feedstocks, including bio-based oils, waste plastics, and pyrolysis oils, into the FCC process. This co-processing approach not only aligns with sustainability goals and circular economy principles but also provides refiners with greater feedstock flexibility and resilience against fluctuations in conventional crude supplies. Such innovations require significant R&D investment but present a pathway for traditional refineries to decarbonize their operations and contribute to a more sustainable energy future.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Optimization for Petrochemical Production (Propylene) | +1.3% | Asia Pacific, North America, Europe | Medium Term (2026-2030) |

| Integration of Bio-based and Waste Feedstocks | +1.1% | Europe, North America, parts of Asia Pacific | Medium to Long Term (2027-2033) |

| Digitalization and Automation for Process Efficiency | +0.9% | Global | Short to Medium Term (2025-2029) |

Fluid Catalytic Cracking Market Challenges Impact Analysis

The Fluid Catalytic Cracking market faces several operational and strategic challenges that can impede efficiency and profitability. A persistent challenge is the management of catalyst deactivation, which occurs due to coke deposition and metal contamination on the catalyst surface. This deactivation necessitates frequent regeneration or replacement of catalysts, adding to operational costs and impacting unit uptime. Optimizing catalyst activity and extending its lifespan while maintaining high conversion rates remains a complex engineering feat for refiners globally.

Another significant hurdle is adhering to constantly evolving and increasingly stringent environmental regulations, particularly concerning sulfur oxides (SOx), nitrogen oxides (NOx), and particulate matter emissions from FCC units. Compliance often requires substantial investments in emission control technologies, such as flue gas treatment systems, which can increase operating expenses and reduce overall profitability. Balancing the economic imperative with environmental responsibility continues to be a delicate act for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Catalyst Deactivation and Lifespan | -0.6% | Global | Ongoing |

| Compliance with Stricter Environmental Regulations | -0.7% | Europe, North America, Developed Asia Pacific | Ongoing |

| High Energy Consumption and Operational Costs | -0.5% | Global | Ongoing |

Fluid Catalytic Cracking Market - Updated Report Scope

This comprehensive report meticulously analyzes the Fluid Catalytic Cracking (FCC) market, providing an in-depth understanding of its current landscape and future trajectory. It encompasses a detailed examination of market size estimations, historical growth trends, and forward-looking projections up to 2033. The scope includes a thorough exploration of key market drivers, restraints, opportunities, and challenges that collectively influence market dynamics, offering a holistic perspective for stakeholders.

The study also delves into significant market trends, highlighting technological advancements in catalyst development, process optimization, and the integration of digital solutions such as AI and machine learning within FCC operations. Furthermore, the report provides a granular segmentation analysis across various parameters including catalyst types, applications, and product output, offering insights into specific market niches and their growth potential. A dedicated section profiles leading market players, outlining their strategic initiatives and competitive positioning.

Geographical analysis forms a crucial part of this report, detailing market performance and future prospects across major regions including North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. This regional breakdown assists in identifying high-growth markets and understanding localized market specificities, thus enabling targeted strategic planning for companies operating within or seeking to enter the Fluid Catalytic Cracking sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.2 Billion |

| Market Forecast in 2033 | USD 19.5 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Albemarle Corporation, BASF SE, Johnson Matthey, W. R. Grace & Co., Honeywell UOP, Axens, Clariant AG, Topsoe, Lummus Technology, KBR, Inc., Chevron Lummus Global (CLG), Sinopec Catalyst Co., Ltd., ExxonMobil Chemical Company, Shell Catalysts & Technologies, China Petroleum & Chemical Corporation (Sinopec), Petrobras, Phillips 66, Valero Energy Corporation, Reliance Industries Limited, TechnipFMC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fluid Catalytic Cracking market is comprehensively segmented to provide granular insights into its diverse components and dynamics. This segmentation facilitates a deeper understanding of market drivers, consumer preferences, and technological adoption across different product types, applications, and geographic regions. By categorizing the market based on catalyst type, for instance, the report highlights the dominance of zeolite-based catalysts and the growing importance of various additives that enhance specific FCC outcomes, such as octane boosting or sulfur reduction. This level of detail helps identify specific innovation hotspots and areas of market saturation.

Further segmentation by application provides clarity on the primary end-uses of FCC technology, primarily focusing on gasoline and propylene production. While gasoline production has historically been the cornerstone, the increasing demand for propylene as a petrochemical feedstock is shifting investment priorities and driving the development of catalysts optimized for higher olefin yields. Understanding these application-specific demands is crucial for catalyst manufacturers and technology providers to tailor their offerings effectively. This segmentation also includes other emerging applications, reflecting the versatility and adaptability of FCC units in modern refineries.

The market is also analyzed by product output, encompassing various fractions like gasoline, LPG, and different types of cycle oils, offering a complete picture of the value chain. Lastly, segmentation by feedstock type, from traditional vacuum gas oil to increasingly processed heavy fuel oil, residue, and nascent bio-based feedstocks, illustrates the industry's drive towards feedstock flexibility and sustainable processing. This multi-faceted segmentation ensures that all critical aspects of the FCC market are thoroughly examined, providing a robust framework for strategic decision-making.

- By Catalyst Type: Zeolite Based (Y-zeolite, ZSM-5, Others), Additives (Sulfur Oxide Scavengers, Light Olefin Enhancers, Octane Enhancers, Metals Passivators)

- By Application: Gasoline Production, Propylene Production, Butadiene Production, Other Petrochemicals

- By Product: Gasoline, Liquefied Petroleum Gas (LPG), Light Cycle Oil (LCO), Heavy Cycle Oil (HCO), Coke

- By Feedstock: Vacuum Gas Oil (VGO), Heavy Fuel Oil, Residue, Bio-based Feedstocks

Regional Highlights

- North America: A mature market characterized by significant refining capacity and ongoing investments in upgrading existing FCC units for cleaner fuels and higher value products. Strong emphasis on digital transformation and advanced catalyst utilization.

- Europe: Driven by stringent environmental regulations and a focus on decarbonization. Refiners are exploring sustainable feedstocks and optimizing FCC operations to meet emissions targets and produce specialty chemicals.

- Asia Pacific (APAC): The fastest-growing region, fueled by rising energy demand, increasing urbanization, and new refinery construction, particularly in China and India. Significant opportunities for new FCC installations and technological upgrades.

- Latin America: Market growth is influenced by the need to process heavy crude oils prevalent in the region. Investments are often directed towards enhancing refining complexity and increasing domestic fuel production.

- Middle East and Africa (MEA): Characterized by abundant crude oil reserves and ambitious downstream expansion projects. Focus on building integrated refining and petrochemical complexes, driving demand for FCC technology.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fluid Catalytic Cracking Market.- Albemarle Corporation

- BASF SE

- Johnson Matthey

- W. R. Grace & Co.

- Honeywell UOP

- Axens

- Clariant AG

- Topsoe

- Lummus Technology

- KBR, Inc.

- Chevron Lummus Global (CLG)

- Sinopec Catalyst Co., Ltd.

- ExxonMobil Chemical Company

- Shell Catalysts & Technologies

- China Petroleum & Chemical Corporation (Sinopec)

- Petrobras

- Phillips 66

- Valero Energy Corporation

- Reliance Industries Limited

- TechnipFMC

Frequently Asked Questions

What is Fluid Catalytic Cracking (FCC)?

Fluid Catalytic Cracking is a crucial refining process that converts high-boiling, heavy hydrocarbon fractions of petroleum crude oils into more valuable, lighter products like gasoline, liquefied petroleum gas (LPG), and olefins. This conversion occurs through a catalytic reaction at high temperatures in a fluid bed reactor.

What are the primary products derived from FCC?

The primary products of the FCC process include high-octane gasoline, which is the main output, and valuable petrochemical feedstocks such as propylene and butylenes. Other significant by-products include liquefied petroleum gas (LPG), light cycle oil (LCO), and heavy cycle oil (HCO).

How do catalysts influence FCC unit performance?

Catalysts are central to FCC unit performance, directly impacting conversion rates, product selectivity, and overall operational efficiency. Advanced zeolite-based catalysts and various additives are designed to optimize yields of desired products, improve octane numbers, reduce undesirable by-products like coke, and enhance the unit's ability to process challenging feedstocks.

What environmental considerations are associated with FCC operations?

Environmental considerations in FCC operations primarily involve managing emissions such as sulfur oxides (SOx), nitrogen oxides (NOx), and particulate matter. Modern FCC units incorporate advanced emission control technologies and utilize specialized catalysts and additives to reduce these pollutants and comply with stringent environmental regulations.

What are the emerging trends shaping the future of the FCC market?

Emerging trends in the FCC market include a focus on producing more petrochemicals like propylene, the integration of bio-based and waste feedstocks for sustainable refining, and the increasing adoption of digital technologies, including AI and machine learning, for process optimization and predictive maintenance to enhance efficiency and profitability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted