Fluid Power Equipment Market

Fluid Power Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703931 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

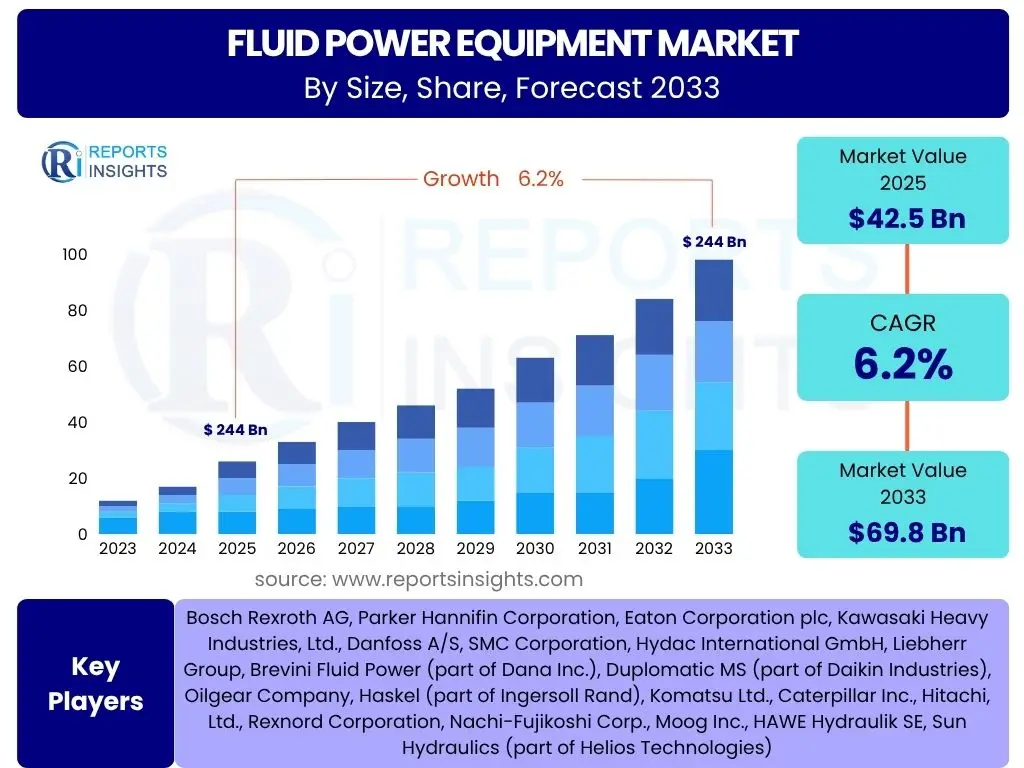

Fluid Power Equipment Market Size

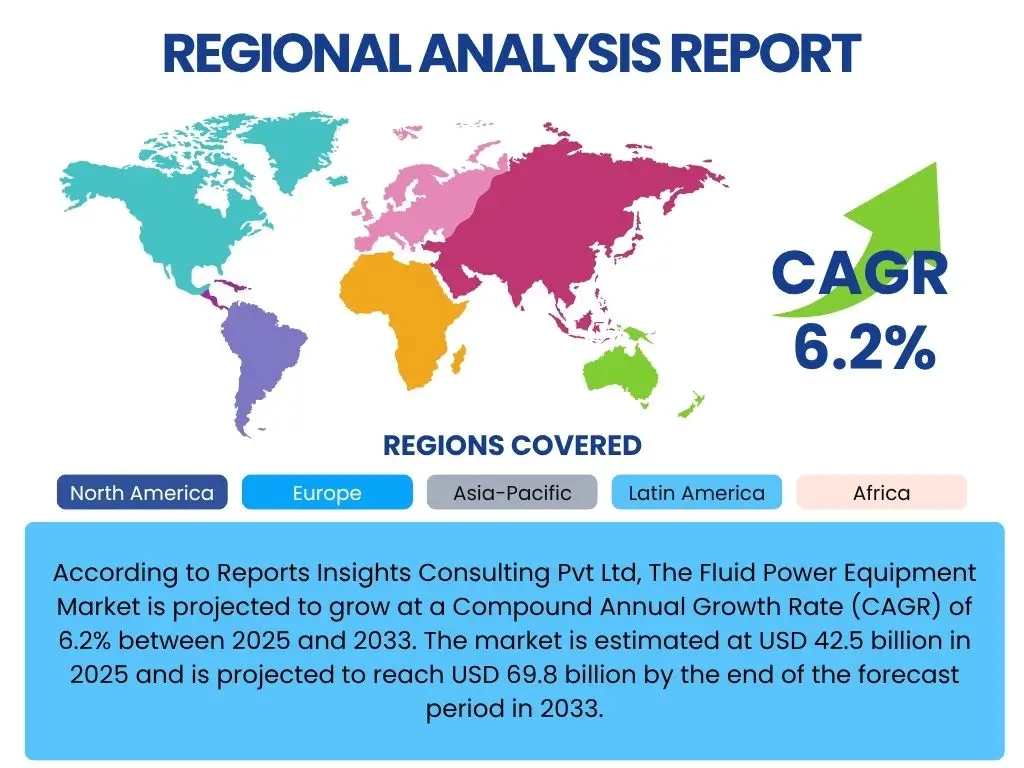

According to Reports Insights Consulting Pvt Ltd, The Fluid Power Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 42.5 billion in 2025 and is projected to reach USD 69.8 billion by the end of the forecast period in 2033.

Key Fluid Power Equipment Market Trends & Insights

The fluid power equipment market is undergoing a significant transformation, driven by a confluence of technological advancements and evolving industrial demands. Common inquiries from users frequently center on the integration of smart technologies, the drive towards energy efficiency, and the adoption of more sustainable practices. There is a clear interest in how traditional hydraulic and pneumatic systems are adapting to Industry 4.0 principles, particularly regarding real-time monitoring, predictive maintenance, and enhanced connectivity. Users are also keen to understand the shift from standalone components to integrated, system-level solutions that offer greater control and operational efficiency.

Another prominent area of user interest revolves around the customization and miniaturization of fluid power components to meet the precise requirements of diverse applications, ranging from compact robotics to large-scale construction machinery. The emphasis on reducing operational costs, improving safety standards, and minimizing environmental impact through more efficient and quieter systems is consistently highlighted. Furthermore, the global push for automation across manufacturing and processing industries is a core driver of these trends, compelling manufacturers to innovate and provide solutions that are both robust and intelligent. The market is thus witnessing a pivot towards intelligent fluid power systems capable of advanced diagnostics and seamless integration within complex industrial ecosystems.

- Integration of smart sensors and IoT for real-time monitoring and predictive maintenance.

- Increased demand for energy-efficient fluid power systems to reduce operational costs and environmental footprint.

- Miniaturization and customization of components to suit compact and specialized applications.

- Adoption of Industry 4.0 and automation technologies across diverse end-use sectors.

- Development of quieter and more environmentally friendly fluid power solutions.

AI Impact Analysis on Fluid Power Equipment

User queries regarding the impact of Artificial Intelligence (AI) on the fluid power equipment domain consistently point towards a significant paradigm shift, particularly in areas of operational efficiency, predictive capabilities, and design optimization. The primary expectation is that AI will enable fluid power systems to move beyond reactive maintenance to proactive, data-driven decision-making. Users frequently ask about how AI can analyze vast datasets from sensors embedded in hydraulic and pneumatic components to detect anomalies, predict component failures before they occur, and schedule maintenance optimally, thereby minimizing downtime and extending equipment lifespan. This shift from time-based or reactive maintenance to condition-based maintenance is a major focal point, promising substantial cost savings and improved reliability for industrial operations.

Furthermore, there is considerable interest in AI's role in optimizing the performance of fluid power systems. Users anticipate that AI algorithms can continuously monitor system parameters, such as pressure, flow, and temperature, and dynamically adjust settings to ensure peak efficiency under varying load conditions. This includes optimizing energy consumption by controlling pump speeds or valve positions in real time. Beyond operational aspects, AI is also expected to revolutionize the design and engineering phases, allowing for simulation-driven design, material optimization, and rapid prototyping of components. The integration of AI into control systems is also viewed as a pathway to more autonomous and adaptive fluid power applications, capable of self-correction and intelligent response to environmental changes, thereby enhancing overall system intelligence and robustness.

- Enhancement of predictive maintenance capabilities through data analytics and machine learning.

- Optimization of energy consumption and operational efficiency by real-time system adjustments.

- Automation of fluid power system design and simulation processes.

- Development of intelligent control systems for autonomous operation and adaptive performance.

- Improved fault detection and diagnostics, reducing downtime and maintenance costs.

Key Takeaways Fluid Power Equipment Market Size & Forecast

Analysis of common user questions regarding the Fluid Power Equipment market size and forecast reveals a strong interest in understanding the underlying drivers of growth, particularly technological advancements and expanding industrial applications. Users are keen to identify the segments poised for the most significant expansion and the regions that present the most lucrative opportunities over the forecast period. The increasing global emphasis on industrial automation, infrastructure development, and the adoption of advanced manufacturing techniques is consistently highlighted as a core factor influencing market trajectories. There is a clear demand for insights into how these macro trends translate into tangible growth figures for specific components and system types within the fluid power sector.

Another key area of inquiry revolves around the impact of economic cycles and supply chain dynamics on market stability and future projections. Users seek clarity on how potential disruptions, such as raw material price volatility or geopolitical shifts, might influence the projected growth rates and overall market value. Furthermore, the rising demand for energy-efficient and environmentally sustainable solutions is frequently cited, indicating a shift towards products that not only perform effectively but also align with global sustainability goals. These insights underscore a market that is resilient and adaptable, continuously innovating to meet the evolving demands of a diverse industrial landscape, positioning fluid power equipment as a foundational technology for global industrial progress.

- Significant growth projected, driven by increasing industrial automation and infrastructure investments.

- Technological advancements, including smart fluid power and IoT integration, are key enablers of market expansion.

- Demand for energy-efficient and environmentally compliant solutions will shape future product development.

- Emerging economies and continued industrialization in Asia Pacific offer substantial growth prospects.

- The market is resilient, adapting to economic shifts and supply chain challenges through innovation.

Fluid Power Equipment Market Drivers Analysis

The fluid power equipment market is significantly propelled by the pervasive trend of industrial automation across various sectors. The increasing adoption of automated processes in manufacturing, material handling, and assembly lines necessitates precise and reliable motion control solutions, which fluid power systems inherently provide. This global push for automation is not limited to developed economies but is rapidly expanding in emerging markets, driving substantial demand for hydraulic and pneumatic components. Furthermore, the continuous investment in infrastructure development projects worldwide, including construction of smart cities, transportation networks, and energy facilities, directly fuels the demand for heavy machinery and equipment that extensively utilize fluid power systems for their robust and high-force capabilities. This sustained global infrastructure spending ensures a consistent underlying demand for the industry.

Another critical driver is the escalating demand for energy-efficient solutions across industries seeking to reduce operational costs and comply with stricter environmental regulations. Modern fluid power systems are being engineered with advanced controls, variable speed drives, and improved designs to minimize energy consumption, making them more attractive to businesses aiming for sustainability. The burgeoning agricultural sector, with its increasing reliance on advanced farming machinery, and the steady growth in the automotive industry for both manufacturing processes and vehicle applications, further contribute to market expansion. These sectors increasingly depend on fluid power for tasks ranging from precision spraying and heavy lifting in agriculture to assembly and braking systems in automotive, showcasing the versatility and indispensability of fluid power technology in contemporary industrial ecosystems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation | +1.5% | Global, particularly Asia Pacific, Europe | Short to Long-term (2025-2033) |

| Growing Infrastructure Development | +1.2% | Asia Pacific, North America, Middle East & Africa | Mid to Long-term (2025-2033) |

| Demand for Energy-Efficient Solutions | +1.0% | Europe, North America, Global | Short to Mid-term (2025-2030) |

| Expansion of Automotive & Construction Industries | +0.8% | Global, especially China, India, USA | Short to Long-term (2025-2033) |

| Technological Advancements & IoT Integration | +0.7% | Global | Mid to Long-term (2027-2033) |

Fluid Power Equipment Market Restraints Analysis

Despite robust growth drivers, the fluid power equipment market faces notable restraints that could temper its expansion. One significant challenge is the relatively high initial investment cost associated with advanced hydraulic and pneumatic systems compared to alternative technologies. This capital expenditure can be prohibitive for small and medium-sized enterprises (SMEs) or in markets with limited budget allocations, potentially slowing down adoption rates. Additionally, the complexity involved in the installation, operation, and maintenance of sophisticated fluid power systems necessitates a highly skilled workforce. A global shortage of qualified technicians and engineers proficient in fluid power technology presents a substantial bottleneck, leading to increased operational costs and potential inefficiencies for end-users. This scarcity can impact the effective deployment and upkeep of advanced systems.

Environmental regulations and concerns regarding fluid leakage and waste disposal also act as significant restraints. Growing awareness and stringent mandates for environmental protection necessitate the development and use of eco-friendly fluids, sealed systems, and proper waste management, which can increase production costs and operational complexities for manufacturers and users. Furthermore, the inherent susceptibility of hydraulic systems to oil contamination and the need for regular fluid changes contribute to maintenance overheads and environmental risks. While pneumatic systems are generally cleaner, their lower power density can limit their application in heavy-duty scenarios, pushing industries towards electric or electromechanical alternatives that may offer cleaner and sometimes more efficient solutions, thereby posing a competitive threat to traditional fluid power.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs | -0.9% | Global, particularly developing economies | Short to Mid-term (2025-2030) |

| Shortage of Skilled Workforce | -0.8% | Global, particularly industrialized nations | Short to Long-term (2025-2033) |

| Strict Environmental Regulations & Waste Management | -0.7% | Europe, North America, Asia Pacific (China) | Mid to Long-term (2027-2033) |

| Maintenance Complexity & Fluid Contamination Risks | -0.6% | Global | Short to Long-term (2025-2033) |

| Competition from Electromechanical Systems | -0.5% | Global | Mid to Long-term (2027-2033) |

Fluid Power Equipment Market Opportunities Analysis

The fluid power equipment market is presented with significant opportunities arising from the expanding adoption of smart manufacturing and Industry 4.0 paradigms. The integration of advanced sensors, IoT capabilities, and data analytics into hydraulic and pneumatic systems opens new avenues for enhanced predictive maintenance, remote diagnostics, and optimized operational performance. This transformation from traditional components to intelligent, connected systems allows manufacturers to offer value-added services and solutions, moving beyond mere product sales to comprehensive lifecycle support. The growing emphasis on automation in emerging economies, particularly in Asia Pacific and Latin America, also presents a substantial opportunity for market players to penetrate new industrial sectors and expand their geographical footprint, leveraging the lower manufacturing costs and increasing industrialization in these regions.

Furthermore, the development of more sustainable and energy-efficient fluid power solutions offers a lucrative growth pathway. Innovations in variable speed pump drives, load-sensing systems, and the utilization of biodegradable fluids address environmental concerns and meet the demand for green technologies. This focus on sustainability not only aligns with global regulatory trends but also appeals to companies striving for corporate social responsibility, potentially leading to increased market share. The burgeoning demand from niche applications, such as robotics, aerospace, and defense, which require high power density, precision control, and reliability, provides additional avenues for specialized fluid power equipment. These high-value applications often justify the investment in advanced fluid power solutions, driving innovation and market growth in specialized segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Industry 4.0 & IoT | +1.3% | Global, particularly developed markets | Mid to Long-term (2027-2033) |

| Expansion in Emerging Markets | +1.1% | Asia Pacific, Latin America, MEA | Short to Long-term (2025-2033) |

| Development of Sustainable & Energy-Efficient Solutions | +1.0% | Europe, North America, Global | Short to Mid-term (2025-2030) |

| Growth in Niche Applications (Robotics, Aerospace) | +0.9% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Aftermarket Services & Retrofitting | +0.7% | Global | Short to Long-term (2025-2033) |

Fluid Power Equipment Market Challenges Impact Analysis

The fluid power equipment market faces several critical challenges that demand strategic responses from industry participants. Intense competition from alternative power transmission technologies, particularly electric and electromechanical systems, poses a significant threat. As industries increasingly prioritize energy efficiency, precision control, and noise reduction, electric actuators and servo drives are gaining traction in applications traditionally dominated by fluid power. This competitive pressure compels fluid power manufacturers to continuously innovate and highlight their distinct advantages, such as high power density, robustness, and suitability for harsh environments, to retain market share. Furthermore, the global nature of the market exposes it to the volatility of raw material prices, which can impact production costs and profit margins. Fluctuations in the cost of steel, aluminum, and other essential materials present an ongoing challenge to supply chain stability and pricing strategies.

Another significant challenge is the vulnerability of the global supply chain, as demonstrated by recent events such as the COVID-19 pandemic and geopolitical disruptions. Disruptions in the availability of components, logistics bottlenecks, and increased shipping costs can lead to production delays and higher prices, affecting market stability and customer satisfaction. The rapid pace of technological change also presents a challenge, requiring continuous investment in research and development to keep pace with evolving industry demands and emerging innovations. Companies must adapt to integrate new technologies like AI, IoT, and advanced materials into their offerings to remain competitive. Finally, economic slowdowns or recessions in key industrial sectors can directly impact demand for fluid power equipment, leading to reduced capital expenditure from end-users. Navigating these economic uncertainties and maintaining resilience in demand is a continuous challenge for the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Electromechanical Systems | -0.9% | Global | Short to Long-term (2025-2033) |

| Volatility in Raw Material Prices | -0.8% | Global | Short to Mid-term (2025-2028) |

| Supply Chain Disruptions | -0.7% | Global | Short to Mid-term (2025-2029) |

| Rapid Technological Obsolescence | -0.6% | Global | Mid to Long-term (2027-2033) |

| Economic Downturns in End-Use Industries | -0.5% | Global | Short-term (2025-2026) |

Fluid Power Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Fluid Power Equipment market, offering a detailed understanding of its current landscape, historical performance, and future projections. The report segments the market by component, type, application, and end-use industry, alongside a thorough regional analysis. It aims to deliver strategic insights for stakeholders, covering market size estimations, growth drivers, restraints, opportunities, and the competitive environment. The scope includes an assessment of technological advancements, such as the integration of IoT and AI, and their impact on market dynamics, providing a holistic view of the forces shaping the industry. The report also highlights key market trends and provides a detailed profile of leading companies, enabling businesses to make informed decisions and identify growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 42.5 Billion |

| Market Forecast in 2033 | USD 69.8 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 257 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Bosch Rexroth AG, Parker Hannifin Corporation, Eaton Corporation plc, Kawasaki Heavy Industries, Ltd., Danfoss A/S, SMC Corporation, Hydac International GmbH, Liebherr Group, Brevini Fluid Power (part of Dana Inc.), Duplomatic MS (part of Daikin Industries), Oilgear Company, Haskel (part of Ingersoll Rand), Komatsu Ltd., Caterpillar Inc., Hitachi, Ltd., Rexnord Corporation, Nachi-Fujikoshi Corp., Moog Inc., HAWE Hydraulik SE, Sun Hydraulics (part of Helios Technologies) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fluid Power Equipment market is comprehensively segmented to provide granular insights into its diverse components, technologies, applications, and end-use industries. This detailed segmentation enables a nuanced understanding of market dynamics, growth drivers, and opportunities within specific sub-sectors. The market is primarily categorized by component type, distinguishing between essential elements such as pumps, motors, valves, cylinders, filters, accumulators, hoses, and fittings, each playing a critical role in the functionality of fluid power systems. Understanding the demand trends for individual components is crucial for manufacturers and suppliers to optimize their production and distribution strategies. Beyond components, the market is broadly divided into hydraulic and pneumatic systems, reflecting the two core technologies that leverage fluid power principles, each with distinct advantages and application suitability.

Further segmentation by application categorizes the market into mobile and industrial uses, acknowledging the significant differences in operational environments and performance requirements for equipment used in construction, agriculture, and material handling (mobile) versus manufacturing, processing, and energy generation (industrial). Finally, the market is segmented by end-use industry, providing a vertical-specific analysis across key sectors such as construction, material handling, agriculture, automotive, mining, oil & gas, marine, aerospace & defense, and food & beverage. This allows for a deeper dive into the specific demands, regulatory landscapes, and growth trajectories of fluid power equipment within each industry. Such detailed segmentation helps stakeholders identify high-growth areas, develop targeted strategies, and cater to the unique needs of various market verticals, ensuring a comprehensive understanding of market penetration and future prospects.

- By Component: Pumps, Motors, Valves, Cylinders, Filters, Accumulators, Hoses, Fittings, Others.

- By Type: Hydraulic Systems, Pneumatic Systems.

- By Application: Mobile Applications, Industrial Applications.

- By End-Use Industry: Construction, Material Handling, Agriculture, Automotive, Mining, Oil & Gas, Marine, Aerospace & Defense, Food & Beverage, Others.

Regional Highlights

- North America: A mature market characterized by high adoption of automation, robust manufacturing, and significant investments in infrastructure and defense. The region shows strong demand for advanced and energy-efficient fluid power systems, driven by technological innovation and stringent environmental regulations.

- Europe: A leading region in technological advancement and sustainability, with a strong focus on Industry 4.0 integration and environmentally friendly fluid power solutions. Countries like Germany and Italy are hubs for manufacturing and R&D in this sector, emphasizing high-performance and precision-engineered components.

- Asia Pacific (APAC): The fastest-growing market due to rapid industrialization, burgeoning construction activities, and increasing automotive production in countries like China, India, and Southeast Asian nations. This region presents immense opportunities for market expansion, driven by large-scale infrastructure projects and growing automation needs across diverse industries.

- Latin America: An emerging market with increasing industrialization, particularly in Brazil and Mexico. Growth is propelled by expanding manufacturing bases, agricultural mechanization, and ongoing infrastructure development projects, though economic stability can influence market trajectory.

- Middle East and Africa (MEA): This region is experiencing growth driven by significant investments in oil & gas, construction, and infrastructure development, particularly in GCC countries. The demand for robust and reliable fluid power equipment for heavy-duty applications is substantial, alongside a growing focus on industrial diversification.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fluid Power Equipment Market.- Bosch Rexroth AG

- Parker Hannifin Corporation

- Eaton Corporation plc

- Kawasaki Heavy Industries, Ltd.

- Danfoss A/S

- SMC Corporation

- Hydac International GmbH

- Liebherr Group

- Brevini Fluid Power (part of Dana Inc.)

- Duplomatic MS (part of Daikin Industries)

- Oilgear Company

- Haskel (part of Ingersoll Rand)

- Komatsu Ltd.

- Caterpillar Inc.

- Hitachi, Ltd.

- Rexnord Corporation

- Nachi-Fujikoshi Corp.

- Moog Inc.

- HAWE Hydraulik SE

- Sun Hydraulics (part of Helios Technologies)

Frequently Asked Questions

Analyze common user questions about the Fluid Power Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Fluid Power Equipment?

Fluid power equipment encompasses systems and components that transmit power by utilizing pressurized fluids, either hydraulic (liquid) or pneumatic (gas), to generate motion, force, and control. These systems are integral to industrial automation, heavy machinery, and various precise control applications.

What are the primary types of Fluid Power Equipment?

The primary types are Hydraulic Systems, which use incompressible fluids like oil to transmit high power, ideal for heavy-duty applications, and Pneumatic Systems, which use compressible gases like air for lighter loads, faster response, and cleaner operations.

What are the main applications of Fluid Power Equipment?

Fluid power equipment finds extensive applications across various industries, including construction (excavators, loaders), material handling (forklifts, cranes), agriculture (tractors, harvesters), automotive manufacturing, mining, aerospace, and general industrial automation.

What key trends are influencing the Fluid Power Equipment market?

Key trends include the integration of IoT and smart sensors for predictive maintenance, a growing demand for energy-efficient and sustainable solutions, miniaturization of components for compact designs, and increased adoption of automation across diverse end-use sectors.

What challenges does the Fluid Power Equipment market face?

The market faces challenges such as high initial investment costs, a shortage of skilled labor, intense competition from electric and electromechanical systems, the volatility of raw material prices, and the need to comply with stringent environmental regulations regarding fluid leakage and disposal.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted