Flexible Packaging Market

Flexible Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702649 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

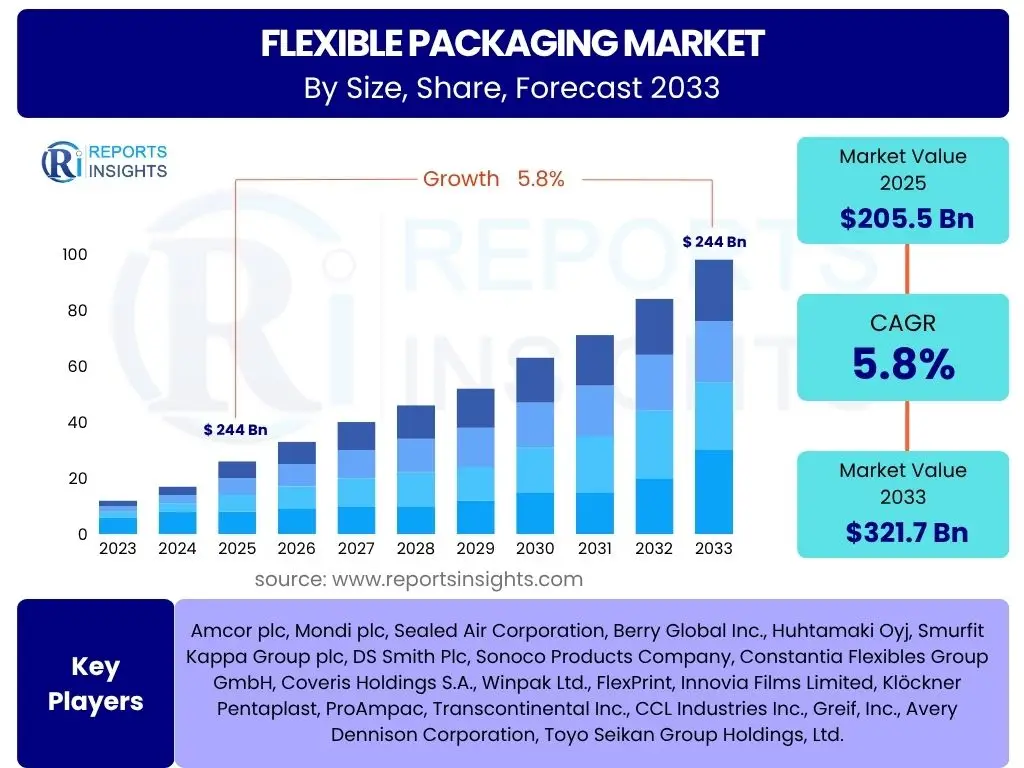

Flexible Packaging Market Size

According to Reports Insights Consulting Pvt Ltd, The Flexible Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 205.5 Billion in 2025 and is projected to reach USD 321.7 Billion by the end of the forecast period in 2033.

Key Flexible Packaging Market Trends & Insights

The flexible packaging market is undergoing significant transformation, driven by evolving consumer preferences and industry demands. A prominent trend involves the escalating focus on sustainability, with consumers and brands actively seeking environmentally friendly packaging solutions, including recyclable, compostable, and bio-based materials. This push extends to the circular economy, where the entire lifecycle of packaging is considered, from material sourcing to end-of-life management. Another key insight is the continuous innovation in material science, leading to the development of high-barrier films that extend product shelf life and reduce food waste, alongside advanced printing technologies that enhance brand appeal and consumer engagement. Furthermore, the rapid growth of e-commerce has spurred demand for lightweight, durable, and protective packaging solutions that can withstand the rigors of shipping while minimizing material use.

Beyond material innovation, automation and digitalization are becoming increasingly integral to flexible packaging operations. Manufacturers are investing in smart factory initiatives to optimize production processes, improve efficiency, and reduce operational costs. This includes the adoption of advanced robotics for handling and packing, as well as data analytics for quality control and predictive maintenance. The market is also witnessing a shift towards customized and personalized packaging, leveraging digital printing capabilities to cater to niche markets and direct-to-consumer models. These trends collectively underscore an industry that is dynamic, responsive to global challenges, and committed to both performance and ecological responsibility.

- Growing demand for sustainable and eco-friendly packaging solutions.

- Advancements in high-barrier film technologies for extended shelf life.

- Increased adoption of digital printing for customization and shorter runs.

- Proliferation of lightweight and convenient packaging formats.

- Integration of smart packaging features for enhanced consumer interaction and traceability.

- Rise of e-commerce driving demand for durable and efficient packaging.

AI Impact Analysis on Flexible Packaging

The integration of Artificial Intelligence (AI) is set to revolutionize various facets of the flexible packaging industry, addressing concerns related to operational efficiency, supply chain complexities, and sustainability targets. Users are keenly interested in how AI can optimize production lines through predictive maintenance, reducing downtime and improving throughput. AI-driven vision systems are enhancing quality control by accurately detecting defects at high speeds, minimizing waste, and ensuring product integrity. Furthermore, AI algorithms can analyze vast datasets to forecast demand more accurately, leading to optimized inventory management and reduced overproduction, which directly contributes to cost savings and environmental benefits.

Beyond manufacturing, AI holds significant promise in the design and development phases of flexible packaging. It can accelerate material innovation by simulating properties of new polymers and composites, identifying optimal structures for specific barrier requirements or recycling capabilities. AI also plays a crucial role in optimizing supply chain logistics, enabling dynamic routing, warehouse automation, and real-time tracking, which reduces lead times and improves delivery reliability. For end-of-life solutions, AI-powered sorting technologies are improving the efficiency and accuracy of waste segregation, paving the way for more effective recycling processes and a truly circular economy for flexible packaging materials. These applications demonstrate AI's potential to drive both economic and environmental improvements across the sector.

- Enhanced quality control and defect detection through AI-powered vision systems.

- Optimized production efficiency and predictive maintenance on manufacturing lines.

- Improved supply chain management, logistics, and demand forecasting.

- Accelerated material research and development for sustainable solutions.

- AI-driven personalized packaging design and consumer insights.

- Advanced sorting and recycling processes for circular economy initiatives.

Key Takeaways Flexible Packaging Market Size & Forecast

The flexible packaging market is poised for robust growth, driven by sustained demand across diverse end-use industries, particularly food and beverage, pharmaceuticals, and personal care. A primary takeaway is the industry's strong commitment to innovation in sustainable solutions, which is not merely a trend but a fundamental shift responding to regulatory pressures and consumer preferences for eco-friendly products. The forecast indicates that while traditional plastics will remain prevalent, there will be an accelerated shift towards mono-materials, recyclable designs, and bio-based alternatives, significantly influencing market dynamics and investment priorities.

Another critical insight derived from the market forecast is the significant impact of e-commerce expansion, necessitating flexible packaging formats that offer durability, lightweight properties, and efficient space utilization during transit. Regional growth patterns reveal Asia Pacific as a powerhouse, fueled by industrialization, population growth, and increasing disposable incomes, while mature markets in North America and Europe will see growth propelled by innovation and sustainability mandates. This dual focus on market expansion in emerging economies and product evolution in established regions underscores a resilient and adaptable industry, continuously seeking equilibrium between performance, cost-effectiveness, and environmental responsibility.

- Consistent market expansion driven by diversified end-use applications.

- Sustainability initiatives are critical for long-term growth and market competitiveness.

- Technological advancements in materials and processes are key growth enablers.

- E-commerce proliferation significantly influences packaging design and demand.

- Emerging economies, particularly in Asia Pacific, represent substantial growth opportunities.

Flexible Packaging Market Drivers Analysis

The flexible packaging market is significantly influenced by a confluence of macroeconomic factors and evolving consumer demands. The escalating demand for convenience foods and beverages, coupled with the rising disposable incomes globally, particularly in emerging economies, propels the adoption of flexible packaging due to its lightweight nature, ease of use, and portability. Moreover, the inherent benefits of flexible packaging, such as extended shelf life and reduced material consumption compared to rigid alternatives, align well with the industry's push for sustainability and cost efficiency. The continuous expansion of organized retail and e-commerce platforms further amplifies this demand, as flexible packaging offers optimal protection and reduced shipping costs.

Innovation in material science and packaging technologies also serves as a crucial driver, enabling the development of advanced barrier films, smart packaging solutions, and more sustainable substrates. These innovations not only meet stringent regulatory requirements but also cater to consumer preferences for safer, fresher, and more environmentally responsible products. The pharmaceutical and healthcare sectors, with their stringent sterility and protection needs, increasingly rely on flexible packaging, further bolstering market growth. The versatility and adaptability of flexible packaging solutions make them indispensable across a wide array of industries, ensuring their sustained relevance and expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for convenience foods & beverages | +1.5% | Global, especially Asia Pacific & Latin America | Short to Medium Term (2025-2029) |

| Increasing focus on sustainable and recyclable packaging | +1.2% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

| Expansion of e-commerce and online retail | +1.0% | Global | Short to Medium Term (2025-2030) |

| Technological advancements in barrier films & smart packaging | +0.8% | North America, Europe, China | Medium Term (2026-2031) |

| Rising demand from pharmaceutical & healthcare sectors | +0.7% | Global | Long Term (2028-2033) |

Flexible Packaging Market Restraints Analysis

Despite its dynamic growth, the flexible packaging market faces several significant restraints that could impede its expansion. Foremost among these are the stringent regulatory frameworks, particularly concerning plastic waste and single-use plastics, which are increasingly being enacted across various regions. These regulations often necessitate substantial investments in new materials and recycling infrastructure, imposing cost pressures on manufacturers. Additionally, the fluctuating prices of raw materials, primarily petrochemicals, introduce volatility into production costs, making long-term planning and pricing strategies challenging for market players. The reliance on fossil-fuel-derived polymers also presents an environmental liability, driving public scrutiny and the search for viable alternatives.

Another key restraint is the current lack of robust recycling infrastructure for multi-material flexible packaging formats, which often comprise layers of different polymers, making them difficult to sort and recycle economically. This technical challenge contributes to lower recycling rates for flexible packaging compared to rigid formats, impacting its overall sustainability profile. Competition from rigid packaging solutions, especially for certain applications where product protection or stacking strength is paramount, also acts as a constraint. Overcoming these restraints requires concerted efforts in material innovation, policy advocacy, and the establishment of scalable recycling solutions to ensure the long-term viability and growth of the flexible packaging industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent environmental regulations on plastics | -0.9% | Europe, North America, India | Short to Medium Term (2025-2030) |

| Volatile raw material prices (e.g., polymers) | -0.7% | Global | Short Term (2025-2027) |

| Challenges in recycling multi-layer flexible packaging | -0.6% | Global | Medium to Long Term (2027-2033) |

| Competition from rigid packaging alternatives | -0.5% | Global | Medium Term (2026-2031) |

Flexible Packaging Market Opportunities Analysis

The flexible packaging market is ripe with opportunities, particularly in the realm of sustainable innovation. The burgeoning demand for eco-friendly solutions presents a significant avenue for growth, as companies invest heavily in developing recyclable, compostable, and bio-degradable flexible packaging materials. This includes single-material solutions that simplify recycling processes and plant-based polymers that reduce reliance on fossil fuels. Brands are increasingly eager to adopt these solutions to enhance their environmental credentials and meet consumer expectations, creating a robust market for pioneers in sustainable packaging technologies.

Further opportunities lie in the expansion into emerging markets, where rapid urbanization, increasing disposable incomes, and the growth of organized retail create fertile ground for flexible packaging adoption. Regions such as Asia Pacific, Latin America, and Africa are experiencing significant economic development, driving demand for packaged goods across various sectors. Additionally, the integration of smart packaging technologies, such as QR codes, NFC tags, and sensors, offers avenues for enhanced consumer engagement, product traceability, and improved supply chain efficiency, providing a competitive edge for companies that embrace these innovations. The convergence of these trends—sustainability, geographical expansion, and technological integration—defines a dynamic landscape rich with growth potential for flexible packaging manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of sustainable and recyclable packaging solutions | +1.3% | Global, particularly Europe & North America | Medium to Long Term (2027-2033) |

| Growth in emerging economies and untapped markets | +1.1% | Asia Pacific, Latin America, MEA | Short to Medium Term (2025-2030) |

| Integration of smart packaging for enhanced functionality | +0.9% | North America, Europe, Developed Asia | Medium Term (2026-2032) |

| Expansion into new application areas (e.g., medical, industrial) | +0.8% | Global | Long Term (2028-2033) |

Flexible Packaging Market Challenges Impact Analysis

The flexible packaging market confronts several critical challenges that demand strategic responses from industry participants. A primary concern is the escalating issue of plastic waste and its environmental impact, leading to a negative public perception of plastic-based packaging. This widespread concern puts immense pressure on manufacturers to innovate rapidly towards more sustainable and circular solutions, often at significant research and development costs. The complexity of regulatory compliance across diverse geographies, particularly concerning material composition, recycling targets, and chemical safety, adds another layer of challenge for global players seeking to standardize their offerings.

Supply chain disruptions, ranging from raw material shortages to geopolitical events, pose a constant threat to production schedules and cost stability. The global nature of the packaging industry means that localized issues can have cascading effects across the entire value chain. Furthermore, the need for substantial capital investment in advanced machinery for sustainable material processing and high-tech printing solutions presents a barrier to entry for smaller players and requires significant financial commitment from established firms. Addressing these challenges necessitates robust innovation pipelines, diversified supply chains, and active participation in industry-wide collaborations aimed at fostering a more sustainable and resilient flexible packaging ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative public perception & plastic waste concerns | -0.8% | Global | Short to Long Term (2025-2033) |

| High investment required for sustainable infrastructure | -0.7% | Global | Medium Term (2026-2031) |

| Complexities of supply chain management & material sourcing | -0.6% | Global | Short to Medium Term (2025-2029) |

| Intense competition and pricing pressures | -0.5% | Global | Short Term (2025-2027) |

Flexible Packaging Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the global flexible packaging market, providing critical insights into its current landscape, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, segmentation across various materials, product types, and end-use applications, and a thorough examination of regional dynamics. It also highlights key market trends, identifies prominent drivers, restraints, opportunities, and challenges influencing market evolution. The report offers strategic profiles of leading market players, competitive landscape analysis, and a forward-looking forecast to empower stakeholders with actionable intelligence for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 205.5 Billion |

| Market Forecast in 2033 | USD 321.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Mondi plc, Sealed Air Corporation, Berry Global Inc., Huhtamaki Oyj, Smurfit Kappa Group plc, DS Smith Plc, Sonoco Products Company, Constantia Flexibles Group GmbH, Coveris Holdings S.A., Winpak Ltd., FlexPrint, Innovia Films Limited, Klöckner Pentaplast, ProAmpac, Transcontinental Inc., CCL Industries Inc., Greif, Inc., Avery Dennison Corporation, Toyo Seikan Group Holdings, Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The flexible packaging market is broadly segmented by material, product type, and application, each category revealing distinct growth patterns and competitive landscapes. Understanding these segments is crucial for identifying specific market opportunities and challenges. The material segment highlights the dominance of plastics, albeit with a growing shift towards sustainable alternatives like bioplastics and paper-based solutions, driven by environmental mandates and consumer preference. The product type segment showcases the versatility of flexible packaging, from ubiquitous pouches and bags to advanced films and wraps, each catering to specific industry needs for protection, convenience, and shelf appeal. Finally, the application segment illustrates the widespread adoption of flexible packaging across diverse end-use industries, underscoring its essential role in modern commerce and consumer goods.

Within these broad categories, further sub-segmentation provides granular detail. For instance, plastic materials are broken down by polymer type, reflecting their varied properties and uses, while pouches are differentiated by their design and functionality (e.g., stand-up, retort). The application analysis delves into specific sub-sectors within food & beverages, pharmaceuticals, and personal care, detailing how flexible packaging meets unique requirements in terms of barrier properties, sterilization, and branding. This comprehensive segmentation allows for a nuanced understanding of market dynamics, enabling stakeholders to pinpoint high-growth areas and tailor strategies accordingly, fostering innovation and market penetration in key niches.

- By Material

- Plastic: This sub-segment includes Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), Polyamide (PA), Ethylene Vinyl Alcohol (EVOH), and Polyethylene Terephthalate (PET). Plastics remain dominant due to their versatility, barrier properties, and cost-effectiveness, though there's an increasing drive towards mono-materials for easier recycling.

- Paper: Comprising Kraft Paper and Coated Paper, this segment is gaining traction due to its recyclability and renewable nature, particularly for dry foods, e-commerce, and personal care products.

- Aluminum Foil: Valued for its excellent barrier properties against moisture, oxygen, and light, aluminum foil is critical for pharmaceuticals and retort pouches.

- Bioplastics: Emerging rapidly, this category includes Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), and starch-based polymers, offering biodegradable and compostable alternatives.

- By Product Type

- Pouches: A highly versatile and growing segment, including Stand-up pouches, Flat pouches, Retort pouches (for shelf-stable foods), and Spouted pouches (for liquids and gels). They offer convenience, reduced material usage, and enhanced shelf appeal.

- Bags: Encompasses Heavy-duty bags (for industrial goods), Wicketed bags (for automated filling), and general Shopping bags, crucial for bulk goods and retail.

- Films: A broad category including Stretch films (for bundling), Shrink films (for product conformity), Lidding films (for trays), and various high-performance Barrier films (for product preservation).

- Wraps: Such as Cling films for food preservation and Industrial wraps for protection during transport.

- Sachets: Small, single-serve packets for liquids, powders, and gels, prevalent in personal care, food, and pharmaceuticals.

- Lids & Labels: Providing sealing and branding functionalities, often integrated with other flexible or rigid formats.

- By Application

- Food & Beverages: The largest application segment, covering Dairy, Meat, Poultry & Seafood, Bakery & Confectionery, Snacks, Fruits & Vegetables, Beverages, and Prepared Foods. Flexible packaging extends shelf life, ensures freshness, and offers convenience.

- Pharmaceutical & Healthcare: Crucial for protecting sterile medical devices, drugs, and other healthcare products, including Blister packs and IV bags, demanding high barrier and tamper-evident features.

- Personal Care & Cosmetics: Used for products like shampoos, lotions, and creams in forms such as shampoo sachets, cream tubes, and cosmetic pouches, emphasizing portability and attractive aesthetics.

- Industrial & Chemical: Encompassing packaging for fertilizers, chemicals, and other industrial goods, requiring robust and durable solutions like large bags and specialized pouches.

- Other Applications: Includes sectors like Pet Food, Agriculture (for seeds, pesticides), and various general Consumer Goods, benefiting from the adaptability and cost-effectiveness of flexible packaging.

Regional Highlights

- North America: This region is characterized by high consumption of convenience foods and a strong emphasis on sustainable packaging solutions. Consumers in North America are increasingly willing to pay a premium for eco-friendly and recyclable flexible packaging. The market is driven by technological advancements, particularly in barrier films and digital printing, and a robust e-commerce sector. Regulations are also playing a significant role in pushing brands towards more circular packaging models, leading to investments in advanced recycling technologies and bio-based materials.

- Europe: Europe is at the forefront of the sustainability movement in flexible packaging, driven by stringent regulations like the EU Packaging and Packaging Waste Directive (PPWD) and consumer demand for circular economy solutions. Countries like Germany and the UK are pioneering efforts in extended producer responsibility (EPR) schemes and developing advanced recycling infrastructure. Innovation in mono-materials, compostable solutions, and chemical recycling is particularly strong here, aimed at reducing plastic waste and achieving ambitious recycling targets. The food and beverage sector remains a primary application, with a growing focus on food waste reduction through improved packaging.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for flexible packaging, fueled by rapid industrialization, increasing disposable incomes, and urbanization, especially in countries like China, India, and Southeast Asia. The burgeoning middle-class population and the expansion of organized retail and e-commerce platforms are significant drivers. While cost-effectiveness remains a key consideration, there is a growing awareness and demand for sustainable packaging, particularly from multinational corporations operating in the region. Investments in production capacity and technology are substantial to meet the escalating regional demand across diverse end-use industries.

- Latin America: This region shows promising growth in flexible packaging, primarily driven by expanding food and beverage consumption, increasing urbanization, and the nascent but growing e-commerce sector. Brazil and Mexico are key markets, benefiting from foreign investments and local demand for convenient and affordable packaged goods. While sustainability initiatives are gaining momentum, economic stability and infrastructure development remain crucial factors influencing market growth and the adoption of advanced packaging solutions.

- Middle East and Africa (MEA): The MEA region is experiencing growth propelled by population growth, economic diversification efforts, and increasing investment in the manufacturing and food processing sectors. Countries in the GCC region are seeing a rise in demand for high-quality, barrier-protected flexible packaging due to climatic conditions and increasing import dependency for packaged foods. While sustainability is an emerging concern, the primary drivers remain convenience, shelf life extension, and cost-efficiency. Infrastructure development for recycling is still in early stages but shows potential for future growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Flexible Packaging Market.- Amcor plc

- Mondi plc

- Sealed Air Corporation

- Berry Global Inc.

- Huhtamaki Oyj

- Smurfit Kappa Group plc

- DS Smith Plc

- Sonoco Products Company

- Constantia Flexibles Group GmbH

- Coveris Holdings S.A.

- Winpak Ltd.

- FlexPrint

- Innovia Films Limited

- Klöckner Pentaplast

- ProAmpac

- Transcontinental Inc.

- CCL Industries Inc.

- Greif, Inc.

- Avery Dennison Corporation

- Toyo Seikan Group Holdings, Ltd.

Frequently Asked Questions

What is flexible packaging?

Flexible packaging refers to packaging made of pliable materials like films, foils, and papers, which can be easily molded into various shapes and sizes. It is lightweight, reduces material usage, and offers excellent barrier properties, making it ideal for a wide range of products including food, beverages, pharmaceuticals, and personal care items.

What are the primary advantages of flexible packaging?

Flexible packaging offers numerous benefits including extended product shelf life, reduced material waste, lower transportation costs due to lightweight design, enhanced convenience for consumers, and versatile branding opportunities. It also contributes to reduced food waste by preserving freshness and minimizing product damage.

Which materials are commonly used in flexible packaging?

Common materials include various plastics like polyethylene (PE), polypropylene (PP), and PET, known for their barrier and protective qualities. Other frequently used materials are aluminum foil for superior barrier performance against light and moisture, and paper for its renewable and recyclable properties. Bioplastics are an emerging category gaining traction.

How does sustainability impact the flexible packaging market?

Sustainability is a major driver, pushing the market towards recyclable, compostable, and bio-based materials. There is a strong focus on circular economy principles, aimed at reducing waste and increasing the use of recycled content. Brands are increasingly adopting eco-friendly packaging to meet regulatory requirements and growing consumer demand for environmentally responsible products.

What are the future trends in flexible packaging?

Future trends include continued innovation in sustainable materials and mono-material solutions for improved recyclability, integration of smart packaging technologies for enhanced consumer interaction and traceability, increased adoption of digital printing for customization, and further growth driven by the expansion of e-commerce and convenience food segments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted