Financial Card and Payment System Market

Financial Card and Payment System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705167 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

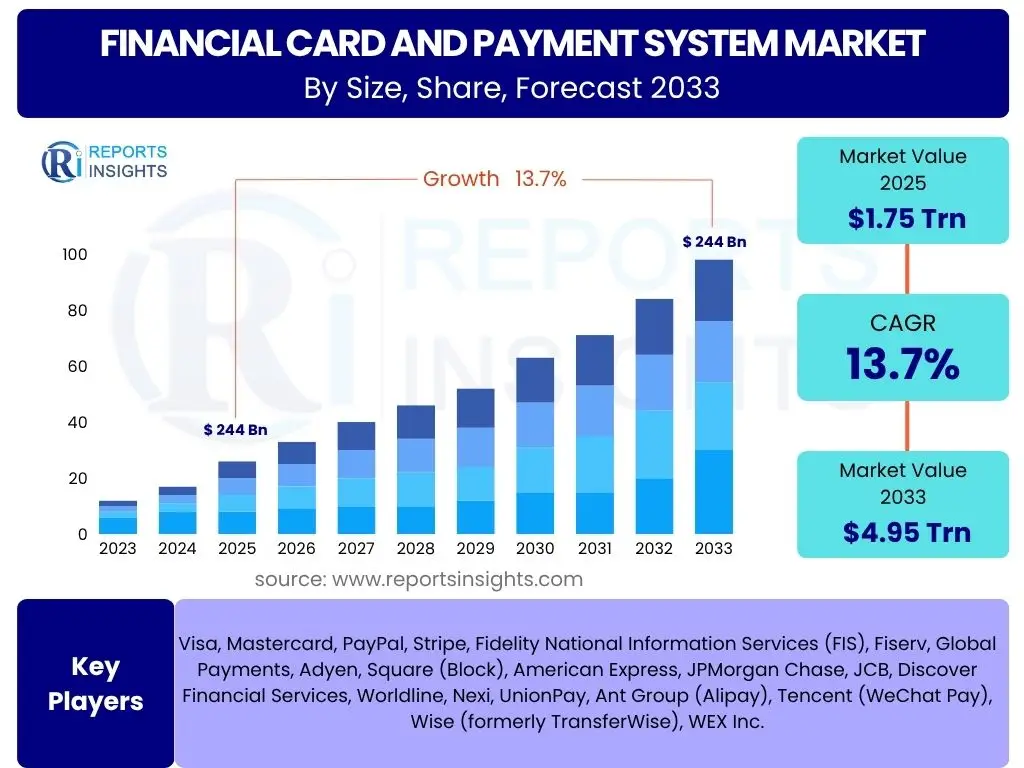

Financial Card and Payment System Market Size

According to Reports Insights Consulting Pvt Ltd, The Financial Card and Payment System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033. The market is estimated at USD 1.75 Trillion in 2025 and is projected to reach USD 4.95 Trillion by the end of the forecast period in 2033.

Key Financial Card and Payment System Market Trends & Insights

The financial card and payment system market is undergoing a profound transformation driven by rapid technological advancements, evolving consumer behaviors, and a shifting regulatory landscape. A primary trend involves the accelerated adoption of digital payment methods, moving away from traditional cash transactions. Consumers increasingly favor convenience, speed, and security, propelling the growth of mobile wallets, contactless payments, and online payment gateways. This shift is particularly evident in emerging economies where digital infrastructure is rapidly expanding, fostering financial inclusion and creating new market opportunities.

Another significant trend is the rise of embedded finance, where financial services are seamlessly integrated into non-financial platforms, such as e-commerce sites and social media applications. This blurs the lines between traditional banking and everyday activities, offering users more contextual and convenient payment experiences. Furthermore, there is a growing emphasis on enhanced security features, including tokenization, biometric authentication, and advanced fraud detection systems, to combat the increasing sophistication of cyber threats. Regulatory frameworks worldwide are also adapting to these changes, aiming to balance innovation with consumer protection and systemic stability, thereby shaping the future trajectory of the payment ecosystem.

- Proliferation of Digital and Contactless Payments: Widespread adoption of mobile wallets, NFC, and QR code payments.

- Growth of Embedded Finance: Integration of financial services directly into non-financial platforms and apps.

- Enhanced Security Measures: Increased use of tokenization, biometrics, and AI-driven fraud detection.

- Open Banking and API Integration: Facilitating seamless data sharing and innovation across financial institutions.

- Real-time Payments (RTP): Demand for instant payment processing for both consumer and business transactions.

- Personalization of Payment Experiences: Tailoring services based on individual spending habits and preferences.

- Sustainability in Payments: Growing demand for eco-friendly payment solutions and practices.

AI Impact Analysis on Financial Card and Payment System

Artificial Intelligence (AI) is fundamentally reshaping the financial card and payment system landscape, addressing critical industry challenges and unlocking new avenues for innovation. One of the most significant impacts of AI is in advanced fraud detection and prevention. AI algorithms can analyze vast datasets of transaction patterns, identifying anomalies and suspicious activities in real-time with far greater accuracy than traditional rule-based systems. This capability significantly reduces financial losses for consumers and institutions while enhancing trust in digital transactions.

Beyond security, AI is revolutionizing customer experience and operational efficiency. AI-powered chatbots and virtual assistants provide instant customer support, resolve queries, and assist with transactions, thereby reducing call center volumes and improving customer satisfaction. Furthermore, AI is crucial for personalizing financial products and services, allowing providers to offer tailored credit card limits, loan offers, and payment solutions based on individual spending habits and financial health. This data-driven personalization not only enhances customer engagement but also optimizes risk assessment and marketing strategies. The integration of AI also streamlines back-office operations, automates reconciliation processes, and optimizes settlement procedures, leading to substantial cost reductions and improved processing speeds across the entire payment value chain.

- Enhanced Fraud Detection and Prevention: AI algorithms analyze transaction patterns to identify and prevent fraudulent activities in real-time.

- Personalized Customer Experiences: AI powers tailored product recommendations, credit offers, and customized payment solutions.

- Optimized Risk Management: AI models assess creditworthiness and transaction risk more accurately, improving lending decisions.

- Automated Customer Support: AI-driven chatbots and virtual assistants provide instant assistance for payment-related queries.

- Operational Efficiency and Automation: AI automates routine tasks, reconciliations, and dispute resolution, reducing manual errors and costs.

- Dynamic Pricing and Loyalty Programs: AI enables dynamic pricing strategies and personalized rewards based on consumer behavior.

- Predictive Analytics for Market Trends: AI forecasts market shifts, consumer preferences, and potential disruptions, aiding strategic planning.

Key Takeaways Financial Card and Payment System Market Size & Forecast

The financial card and payment system market is poised for robust expansion, reflecting a global shift towards digital payment methods and increasing financial connectivity. A key takeaway is the significant growth trajectory projected through 2033, driven by a confluence of factors including expanding e-commerce, the widespread adoption of mobile and contactless technologies, and governmental initiatives promoting digital economies. This sustained growth underscores the payment industry's resilience and its central role in facilitating modern commerce and financial inclusion worldwide.

Another critical insight is the evolving competitive landscape, where traditional financial institutions are increasingly collaborating with fintech innovators to leverage advanced technologies such as AI and blockchain. This collaboration is fostering a more interconnected and efficient payment ecosystem, characterized by enhanced security, greater convenience, and broader accessibility. Understanding these dynamics is crucial for stakeholders to identify emerging opportunities, mitigate potential risks, and develop resilient strategies for navigating a rapidly transforming market. The shift towards embedded finance and real-time payments further highlights the need for adaptive business models and continuous technological investment to remain competitive.

- Significant Market Growth: The market is expected to achieve substantial growth, nearing USD 5 Trillion by 2033, driven by digital transformation.

- Technology as a Core Driver: AI, blockchain, and API integrations are fundamental to improving security, efficiency, and customer experience.

- Shifting Consumer Preferences: A strong preference for convenience, speed, and security is accelerating the adoption of digital and contactless payments.

- Emergence of New Business Models: Embedded finance and Banking-as-a-Service (BaaS) are creating new revenue streams and partnerships.

- Regulatory Adaptation: Regulators are actively shaping the environment to balance innovation with consumer protection and systemic stability.

- Focus on Financial Inclusion: Digital payment solutions are critical in extending financial services to underserved populations globally.

- Cybersecurity Imperative: Ongoing investment in robust fraud detection and data security measures is crucial amidst evolving threats.

Financial Card and Payment System Market Drivers Analysis

The global surge in e-commerce activities and the increasing penetration of smartphones are primary drivers propelling the financial card and payment system market. As consumers increasingly conduct transactions online, the demand for secure, efficient, and convenient digital payment methods escalates. This digital transformation is further amplified by the widespread availability of mobile devices, enabling anytime, anywhere payments and fostering the growth of mobile wallets and contactless payment technologies. These factors collectively contribute to a substantial expansion of the addressable market for financial card and payment solutions, moving transactions away from traditional cash.

Furthermore, government initiatives and regulatory support for digital payments play a pivotal role in market expansion. Many countries are actively promoting cashless economies through policies that encourage electronic transactions, digital financial literacy, and the development of robust payment infrastructures. Such initiatives often include incentives for businesses to adopt digital payment acceptance solutions and for consumers to use digital payment instruments. The growing global middle class and increasing urbanization also contribute significantly, as these demographic shifts lead to higher disposable incomes and a greater propensity to engage in formal financial transactions, driving demand for structured payment systems. The push towards financial inclusion, particularly in emerging markets, also necessitates accessible and affordable digital payment solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth in E-commerce & Online Shopping | +2.5% | Global, especially Asia Pacific, North America, Europe | Short to Mid-term (2025-2029) |

| Increasing Adoption of Mobile & Contactless Payments | +2.0% | Global, particularly developed economies and urban centers | Short to Mid-term (2025-2030) |

| Government Initiatives & Regulatory Support for Digital Payments | +1.8% | India, China, Brazil, UK, EU, UAE | Mid to Long-term (2026-2033) |

| Rising Disposable Incomes & Urbanization | +1.5% | Emerging Markets (APAC, Latin America, Africa) | Long-term (2028-2033) |

| Advancements in Payment Security Technologies (Tokenization, Biometrics) | +1.2% | Global, all regions | Short to Mid-term (2025-2030) |

Financial Card and Payment System Market Restraints Analysis

Despite robust growth, the financial card and payment system market faces several significant restraints that could impede its full potential. One major challenge is the persistent concern over data privacy and security breaches. High-profile cyberattacks and data compromises erode consumer trust in digital payment systems, making some users hesitant to adopt or fully commit to card and digital transactions. This concern necessitates continuous and substantial investment in advanced cybersecurity measures, which can be costly for payment providers and financial institutions.

Another significant restraint is the complex and fragmented regulatory landscape across different regions and countries. Varying compliance requirements, data localization laws, and anti-money laundering (AML) regulations create hurdles for international payment processing and limit the scalability of global payment solutions. This regulatory intricacy can increase operational costs and time-to-market for new innovations. Furthermore, the entrenched habit of cash usage in many parts of the world, particularly in informal economies and among older demographics, presents a cultural barrier to the widespread adoption of digital payment systems. Overcoming this cultural inertia requires extensive public education and infrastructure development, which can be a slow and resource-intensive process.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Privacy and Security Concerns | -1.5% | Global, especially EU (GDPR) and North America | Ongoing, Long-term |

| Complex and Fragmented Regulatory Landscape | -1.2% | Cross-border transactions, developing economies | Ongoing, Long-term |

| High Cost of Payment Infrastructure & Merchant Fees | -0.8% | SMEs, Developing Nations | Mid-term (2026-2030) |

| Resistance to Digital Adoption (Cash Preference) | -0.7% | Rural areas, elderly population, informal sectors in emerging markets | Long-term (2028-2033) |

| System Interoperability Challenges | -0.5% | Global, particularly developing fragmented markets | Mid to Long-term (2027-2033) |

Financial Card and Payment System Market Opportunities Analysis

The financial card and payment system market is ripe with opportunities, particularly driven by the growing demand for frictionless and integrated payment experiences. The expansion of embedded finance presents a significant avenue for growth, as financial services are increasingly integrated directly into non-financial applications, e-commerce platforms, and everyday consumer journeys. This allows for contextual payments and credit offerings, enhancing user convenience and engagement. Payment providers can leverage this trend by forming strategic partnerships with non-financial entities, expanding their reach beyond traditional banking ecosystems.

Another substantial opportunity lies in the underserved and unbanked populations in emerging markets. Digital payment solutions, particularly mobile-first approaches, can bridge the gap in financial access for billions of people who lack traditional banking relationships. This not only fosters financial inclusion but also unlocks vast new customer bases for payment service providers. Additionally, the continuous advancements in technologies like Artificial Intelligence (AI) and blockchain offer transformative potential. AI can enhance personalization, fraud detection, and operational efficiencies, while blockchain can revolutionize cross-border payments by offering faster, more transparent, and cost-effective solutions. Investing in these innovative technologies can create competitive advantages and open up entirely new service offerings, positioning players for future market dominance.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved & Unbanked Populations | +2.0% | Africa, Latin America, parts of Asia Pacific | Long-term (2027-2033) |

| Rise of Embedded Finance and BaaS (Banking-as-a-Service) | +1.8% | Global, especially North America, Europe, China | Mid to Long-term (2026-2033) |

| Integration of AI and Machine Learning for Enhanced Services | +1.5% | Global, all regions | Short to Mid-term (2025-2030) |

| Growth of Cross-border Payments & Remittances | +1.3% | Global, with high relevance in APAC, LATAM, MEA | Mid to Long-term (2027-2033) |

| Development of Blockchain and DLT-based Payment Solutions | +1.0% | Global, particularly early adopters in finance and tech | Long-term (2029-2033) |

Financial Card and Payment System Market Challenges Impact Analysis

The financial card and payment system market is confronted by a range of challenges that necessitate continuous innovation and strategic adaptation. Cybersecurity threats, including sophisticated fraud schemes, phishing attacks, and data breaches, represent an ongoing and escalating challenge. Payment providers must continually invest in advanced security protocols, real-time fraud detection systems, and robust incident response capabilities to protect consumer data and maintain trust. The dynamic nature of these threats means that security measures must evolve constantly, demanding significant resources and expertise.

Another significant challenge is ensuring interoperability across diverse payment systems and technologies. As the ecosystem expands to include various card networks, mobile wallets, and alternative payment methods, seamless integration becomes crucial for a frictionless user experience. Lack of interoperability can create friction for consumers and merchants, hindering wider adoption and market growth. Furthermore, the rapid pace of technological innovation and changing consumer expectations requires constant adaptation. Companies must not only keep pace with emerging technologies like AI, blockchain, and quantum computing but also anticipate future trends to remain competitive. This necessitates agile product development, continuous research and development, and a culture of innovation to meet evolving demands and regulatory complexities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving Cybersecurity Threats & Fraud Schemes | -1.8% | Global, all markets | Ongoing, Short to Long-term |

| Regulatory Compliance & Geopolitical Risks | -1.5% | Cross-border operations, highly regulated markets (EU, US) | Ongoing, Long-term |

| Competition from New Entrants & Alternative Payment Methods | -1.0% | Global, particularly tech-savvy markets | Mid-term (2026-2030) |

| Infrastructure Limitations in Emerging Markets | -0.9% | Rural areas, developing economies in Africa, parts of Asia | Long-term (2028-2033) |

| Talent Shortage in Fintech & Cybersecurity | -0.7% | Global, particularly developed economies | Ongoing, Long-term |

Financial Card and Payment System Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Financial Card and Payment System Market, encompassing historical data, current market dynamics, and future projections. The study delves into various market attributes, offering insights into market size estimations, growth rate forecasts, and key trends shaping the industry landscape from 2019 through 2033. It meticulously breaks down the market into critical segments by card type, payment type, end-user, and technology, providing a granular view of their individual contributions and growth potential. Furthermore, the report identifies the leading companies operating in this space, highlighting their strategic initiatives and market positioning, alongside a detailed regional analysis to capture diverse market behaviors and opportunities across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The scope is designed to equip stakeholders with actionable intelligence for strategic decision-making in a rapidly evolving payment ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.75 Trillion |

| Market Forecast in 2033 | USD 4.95 Trillion |

| Growth Rate | 13.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Visa, Mastercard, PayPal, Stripe, Fidelity National Information Services (FIS), Fiserv, Global Payments, Adyen, Square (Block), American Express, JPMorgan Chase, JCB, Discover Financial Services, Worldline, Nexi, UnionPay, Ant Group (Alipay), Tencent (WeChat Pay), Wise (formerly TransferWise), WEX Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The financial card and payment system market is comprehensively segmented to provide a detailed understanding of its diverse components and growth drivers. These segments highlight distinct areas of innovation and consumer adoption, reflecting the varied landscape of payment methods and their applications across different industries. By dissecting the market based on card types, payment channels, end-user applications, and underlying technologies, this analysis offers granular insights into where growth is concentrated and how different innovations are shaping specific niches within the broader payment ecosystem. This detailed segmentation aids in identifying key opportunities and challenges within each category, enabling targeted strategic planning for market participants.

For instance, the segmentation by card type distinguishes between debit, credit, prepaid, and gift cards, each serving unique financial needs and consumer behaviors. Payment type segmentation further differentiates between traditional point-of-sale transactions, burgeoning online payments, and the rapidly expanding mobile payment channels, including in-app purchases, QR codes, and NFC. The end-user segmentation provides crucial insights into the adoption patterns across various sectors such as retail, BFSI, hospitality, and healthcare, illustrating the vertical-specific demands for payment solutions. Lastly, technology-based segmentation showcases the impact of advancements like NFC, QR codes, biometrics, blockchain, and EMV chips on secure and efficient transaction processing, indicating the direction of future technological investments in the industry.

- By Card Type: Debit Card, Credit Card, Prepaid Card, Gift Card, Others

- By Payment Type: Point of Sale (POS), Online Payment, Mobile Payment (In-app, QR Code, NFC), ATM

- By End-User: Retail, Banking, Financial Services, and Insurance (BFSI), Hospitality, Healthcare, Government, E-commerce, Others

- By Technology: Near Field Communication (NFC), QR Code, Biometric, Blockchain, Magnetic Stripe, EMV Chip

Regional Highlights

- North America: This region maintains a significant market share due to its advanced digital infrastructure, high consumer adoption of credit and debit cards, and the rapid expansion of e-commerce. The United States, in particular, leads in payment innovation, with a strong presence of fintech companies and significant investment in contactless and mobile payment technologies. Canada also shows steady growth, driven by similar trends. Regulatory frameworks generally support innovation while addressing security concerns, fostering a dynamic environment for both traditional and emerging payment solutions.

- Europe: Characterized by diverse economies and a strong push towards a unified digital single market, Europe is a pivotal region for financial card and payment systems. The adoption of contactless payments is exceptionally high, particularly in the UK and Nordic countries. Regulations such as PSD2 (Revised Payment Services Directive) have spurred open banking and fostered competition, encouraging fintech innovation and the integration of third-party payment providers. Germany, France, and Italy are key markets, each with unique consumer preferences and regulatory nuances influencing payment trends.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by burgeoning e-commerce markets, rapid smartphone penetration, and a massive unbanked population transitioning directly to digital payments. China and India are at the forefront, with widespread adoption of mobile wallets (e.g., Alipay, WeChat Pay, Paytm) that are transforming the retail landscape. Southeast Asian countries are also experiencing significant growth in digital payments, driven by supportive government policies and increasing financial inclusion initiatives. The region's diverse economic landscapes present both immense opportunities and unique challenges for payment providers.

- Latin America: This region is experiencing robust growth in digital payments, driven by increasing internet penetration, smartphone adoption, and a strong need for financial inclusion. Countries like Brazil, Mexico, and Argentina are seeing a rapid shift from cash to digital payment methods, including credit and debit cards, and mobile wallets. Fintech startups are playing a crucial role in innovating payment solutions tailored to the region's specific economic and social conditions, addressing issues like high unbanked rates and the informal economy.

- Middle East and Africa (MEA): The MEA region presents significant growth potential, particularly in digital payments, as governments and private entities invest in modernizing financial infrastructure. Countries in the Gulf Cooperation Council (GCC) such as UAE and Saudi Arabia are leading in digital transformation, adopting advanced payment technologies and promoting cashless societies. In Africa, mobile money solutions are dominant, bridging the financial inclusion gap for millions who lack access to traditional banking services. The region's young population and increasing smartphone penetration are key drivers for the expansion of financial card and payment systems.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Financial Card and Payment System Market.- Visa

- Mastercard

- PayPal

- Stripe

- Fidelity National Information Services (FIS)

- Fiserv

- Global Payments

- Adyen

- Square (Block)

- American Express

- JPMorgan Chase

- JCB

- Discover Financial Services

- Worldline

- Nexi

- UnionPay

- Ant Group (Alipay)

- Tencent (WeChat Pay)

- Wise (formerly TransferWise)

- WEX Inc.

Frequently Asked Questions

What is the projected growth rate for the Financial Card and Payment System Market?

The Financial Card and Payment System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033.

What are the primary drivers of growth in the Financial Card and Payment System Market?

Key growth drivers include the rapid expansion of e-commerce, increasing adoption of mobile and contactless payments, supportive government initiatives for digital transactions, and rising disposable incomes in emerging markets.

How is AI impacting the Financial Card and Payment System Market?

AI significantly impacts the market through enhanced fraud detection, personalized customer experiences, optimized risk management, and increased operational efficiency by automating various processes.

What are the main challenges faced by the Financial Card and Payment System Market?

Major challenges include evolving cybersecurity threats and fraud schemes, complex and fragmented regulatory landscapes, intense competition from new entrants, and infrastructure limitations in certain developing regions.

Which regions are expected to show significant growth in the Financial Card and Payment System Market?

Asia Pacific (APAC) is projected to be the fastest-growing region, driven by strong e-commerce growth and mobile payment adoption. North America and Europe will maintain substantial market shares due to established digital infrastructures and ongoing innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted